Snowflake Accelerates In Revenue While Growth Stocks Sell Off

January 18, 2022

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Jan 13, 2022, 04:54pm EST

Snowflake was listed on September 2020 and the shares more than doubled on the day of the listing. It was one of the biggest tech IPOs of all time raising roughly $3 billion with a road show that attracted risk-adverse Warren Buffet.

In my deep dive published on Forbes, I noted Snowflake’s sky-high revenue growth of 173% in the year prior to the IPO. Another key metric that led to the success was the net retention rate of 158%, which was the highest for any cloud company at the time of listing; this metric is even higher now. Snowflake closed the opening day with a market cap of $70.3 billion that was more than five times its last private valuation of about $12.5 billion. Snowflake has been public for over a year and now trades at a market cap of $92.5 billion for a gain of roughly 33%, at time of writing.

Below, we revisit the product and the company’s financials now that it’s been a public company for a decent length of time. The information in this analysis is partly why we have decided to build a position with more information on what makes Snowflake stand apart provided to our premium members.

Snowflake Inc Price % Change - YCHARTS

Snowflake’s Rare Acceleration in Net Retention

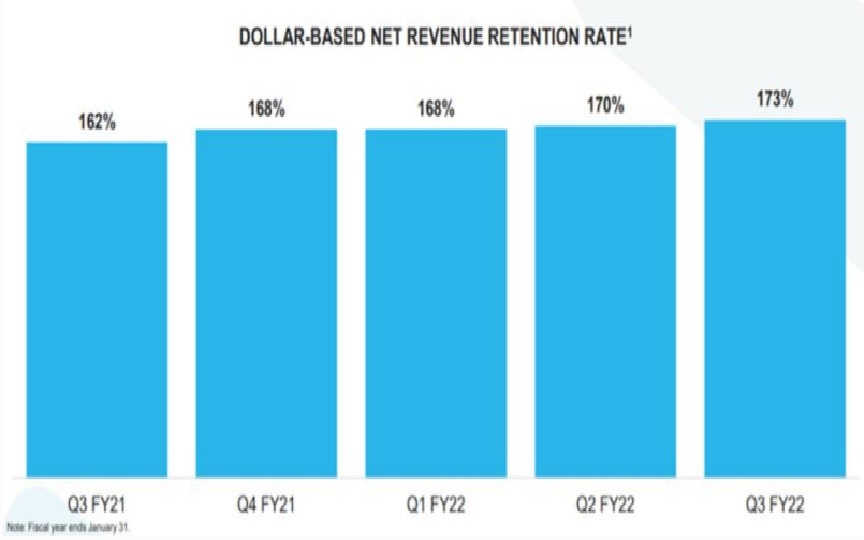

There are a few key metrics that Snowflake discloses that help investors better understand the demand for its products and the cadence of its growth going forward. One of the key metrics is its net retention ratio (NRR), which increased YoY from 162% to 173%, the highest level since it went public and a notable (RARE) acceleration.

Since Snowflake uses a ‘land-and-expand’ sales strategy, growth with existing customers is critical to scale its business. An increase in its NRR metric demonstrates that customers sign on and then rapidly ramp spending as they fully deploy on Snowflake’s platform.

However, CFO Michael Scarpelli, cautioned investors that NRR will decline going forward, but nevertheless will still remain well above 140% for a “very long time”. Specifically, he stated that, “I'm not going to guide long term. It's hard to do that. I'm just going to reiterate again what I said to Derrick is we will [keep NRR] above 160% for this year. And I do expect longer term as our customer base gets bigger and bigger and more mature, that number will come down, but I still think it will be well above 130%, 140% for a very long time”.

Dollar-Based Net Revenue Retention Rate - INVESTOR PRESENTATION

While Snowflake uses a “land -and-expand” sales strategy, it also uses a consumption billing model. For instance, Snowflake bills customers based on the amount of data they store and transfer and what resources they use. Accruing revenue based on consumption rather than a ratable subscription model decreases the predictability of quarterly revenue, but it leaves revenue uncapped. This provides revenue upside, because if consumption soars, then so will revenue. We can see with the NRR metric discussed above that existing customers are ramping consumption. Furthermore, this consumption is also contracted, meaning that a portion of forward topline growth is locked in which provides visibility into future sales.The company’s robust NRR metric of 173% discussed above also backs up management’s claim that customers often exceed their original contract amounts. Furthermore, since sales are accrued under a consumption model rather than a subscription model, there doesn’t appear to be a ceiling on customer spending. For instance, Snowflake disclosed that customers spending over $1 million (enterprise customers) grew 128% YoY to 148. Moreover, these customers accounted for 53% of total revenue, up from 46% in the year ago quarter. This implies that spending per enterprise customer increased 6% YoY to $3.4 million. While the outsized growth in enterprise count is impressive, it is also great to see spending per enterprise customer rise as well, signaling that large customers keep getting bigger.

As a result of the improvement in the metrics disclosed above, the company’s revenue accelerated by 110% YoY to $334.4 million. The topline growth was very strong and has been above 100% for at least five quarters in a row (since the company went public). Growth was led by financial, media, technology, and retail customers.

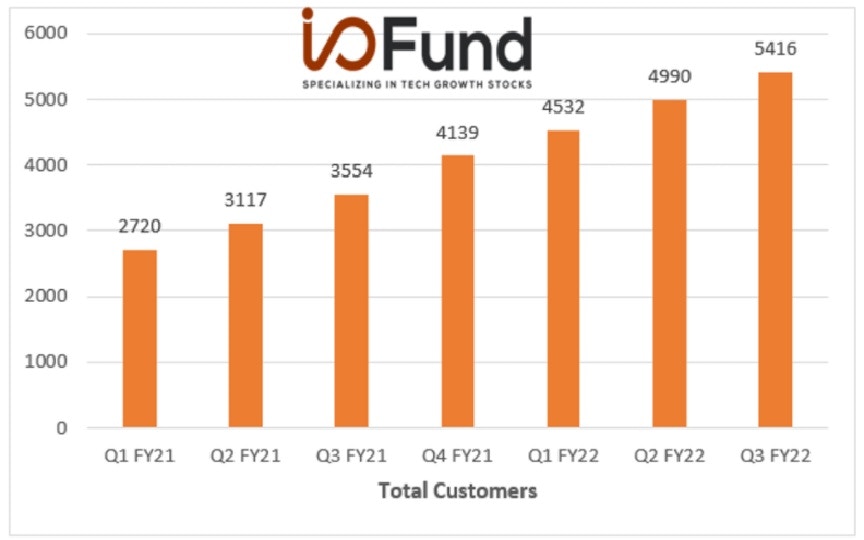

The company has a growing customer base. As mentioned above, customers with trailing 12 months product revenue greater than $1 million were 148, up 128% YoY. Furthermore, total customers increased 52% YoY to 5,416 customers, while Fortune 500 customers grew by 30% YoY to 223.

Total Customers Chart - COMPANY WEBSITE

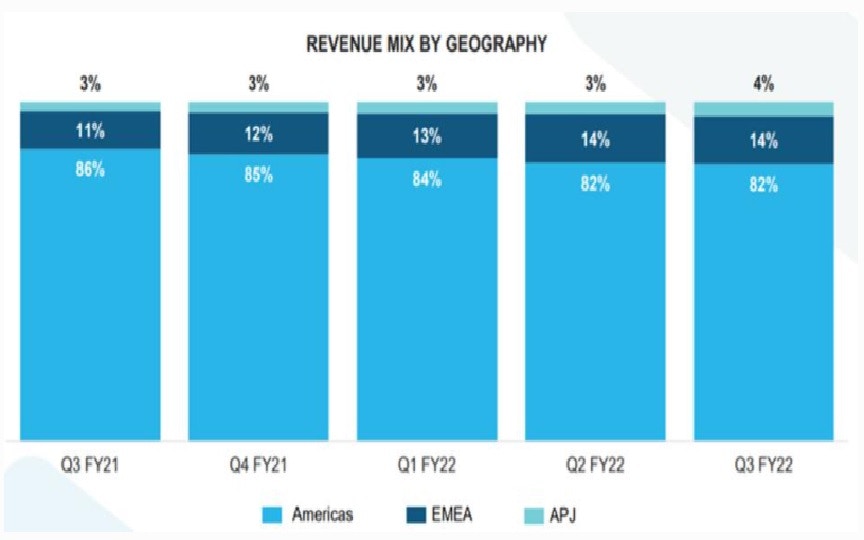

The company is also growing internationally and the growth is higher than the company’s total growth. International revenue which was 14% of the total revenue in the Q3 FY21 has increased to 18% in the Q3 FY22.

In the earnings call, Frank Slootman said, “We continued our international expansion with product revenue from EMEA and Asia-Pacific outstripping the company's year-on-year growth, up 174% and 219% respectively. We recently launched operations in three new countries Israel, Korea, and the United Arab Emirates.”

Revenue by Geography - INVESTOR PRESENTATION

Another key metric, remaining performance obligation grew by 94% YoY to $1.8 billion. This represents revenue that is contracted but not yet realized.

Of the total $1.8 billion the management expects about 55% to be recognized as revenue in the next one year. Some of the notable large multi-year deals in the recent quarter include a $100 million three-year deal to an existing customer and additional five eight-figure multi-year deals. This is a positive trend that the company has been able to win large contracts.

The company’s margins continue to show improvement. Total gross margin is 64% and adjusted gross margin is 71% when compared to 58% and 67% respectively, for Q3 FY2021. Adjusted product gross margin came in at 74.6% when compared to 73.6% in the previous quarter and 70% in the same period last year.

Net loss came in at $154.9 million or ($0.51) per share compared to $168.9 million or ($1.01) per share for the same period last year.

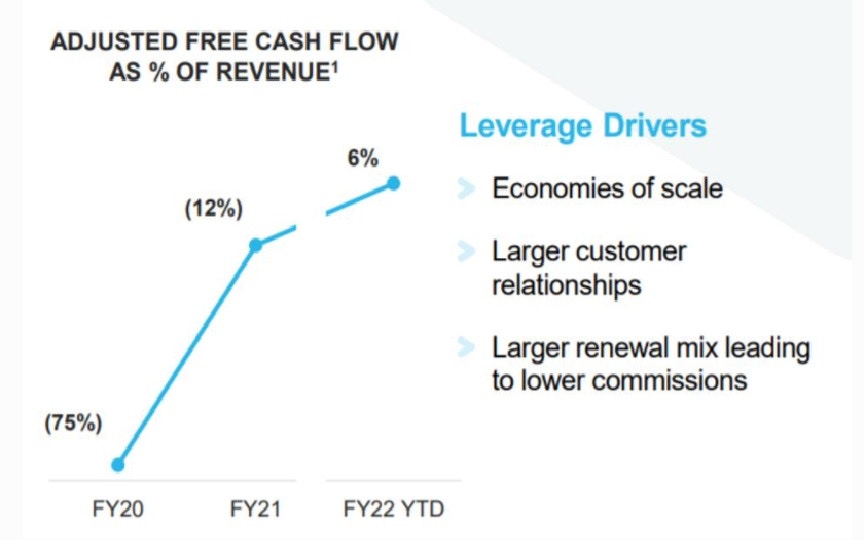

The company’s free cash flow improved to $9.5 million from a free cash outflow of $37.9 million for Q3 FY2021. Adjusted free cash flow came in at $21.5 million compared to adjusted free cash outflow of $37.1 million in the same period last year. The company has maintained a strong balance sheet as it has cash and investments of about $5.1 billion.

Adjusted Free Cash Flow As % of Revenue - INVESTOR PRESENTATION

Update on Snowflake’s Platform:

Snowflake’s decoupled architecture allows for compute and storage to scale separately with the storage provided from any cloud provider the customer chooses. By processing queries using massively parallel processing (MPP), where each node in the cluster stores a portion of the data set locally, the virtual warehouses can access the storage layer independently so as not to compete for compute power. With the competitors, such as Redshift, where compute and storage are coupled, more time is spent reconfiguring the cluster.

Snowflake calls this offering a virtual data warehouse where workloads share the same data but can run independently. This is crucial because Snowflake’s competitors combine compute and storage and require customers to size and pay based on the largest workload.

Data warehouses are centralized data repositories that collect and store information across many sources that are both internal and external. The raw data is ingested into the data warehouse and processed to answer queries. One key product differentiator is that Snowflake is not built on Hadoop, rather the company uses a new SQL database engine with cloud-optimized architecture. Overall, this translates to faster queries and also reduces costs by scaling up or down for both capacity and performance. This also allows the shift to the cloud while still honoring traditional relational database tools. Just like cloud infrastructure does not require you to hold server space for peak times year-round, a cloud data warehouse does not require you to plan, acquire or manage resources for peak data demand (i.e. elasticity).

The need for resources could change by either increasing or decreasing (scaling up or down). Customers that have a need for storage but less of a need for CPU computations do not have to pay up front and can shrink the environment dynamically. Users either pay for terabytes or are billed on a per-second basis for computations. As discussed above, Snowflake charges by execution-based usage and is not a cloud SaaS-company that charges by subscription.

Snowflake has a multi-cluster architecture which is unique from single cluster databases. The multi-cluster approach allows the clusters to access the same underlying data yet to run independently. This allows for heavy queries and operations to run very quickly and with fewer errors because the queries are not accessing the same data warehouse.

Beyond the value proposition of separating storage from compute for speed, and also scaling up or down to reduce costs, the third takeaway is that Snowflake is also much easier for customers to use as it’s designed to remove the role of a database administrator for monitoring and/or to tune query performance.

The end goal of choosing Snowflake is that you load data, run queries, and do little else – which is an immense value proposition due to the amount of time wasted prepping, balancing, tuning and monitoring traditional data warehouses originally built for on-premise.

Snowflake is capitalizing on the multi-cloud trend and growing rapidly with customers who want a choice in public cloud provider despite the cloud giants having their own data warehouse systems, such as Amazon Redshift, Azure Synapse and Google Big Query.

In our first article written at the time of Snowflake’s public listing, we discussed competitors Google’s Big Query and Amazon’s RedShift. Big Query has a strong following of about 2X customers compared to Snowflake, growing at 40% and also offers separate storage and compute. The differences between BigQuery and Snowflake include pricing structure where Snowflake is a time-based pricing model where users are charged for execution time and BigQuery is a query-based pricing model, where users are charged for the amount of data returned from the queries. Redshift has growth of 6.5% and is not as competitive due to coupling compute and storage.

In 2020, The Enterprise Technology Research study showed 80% of AWS accounts plan to spend more on Snowflake in 2020 relative to 2019 with 35% adding Snowflake as new compared to 12% adding Redshift as new. In Azure, 78% plan to spend more on Snowflake with 41% adding new. On Google Cloud, 80% plan to increase spending on Snowflake.

Granted, this study was in 2020 but this helps drive home why Big Tech owning the data centers is not a deterrent for Snowflake’s rapid adoption. Judging by Snowflake’s revenue growth, these preferences are likely still intact.

The company also launched support for unstructured data earlier this year, which is another strength compared to the SQL legacy competitors. Due to the increasing use of unstructured data, there is demand to support unstructured data for big data analytics.

Data Sharing and Data Marketplaces

Snowflake allows businesses to share their data with other external businesses on the platform. Data Marketplace allows free or monetized data sets to be exchanged. This has helped Snowflake break into new industries with use cases that other data lakes and competitors do not currently offer.

For example, earlier this year, Snowflake announced support for Unified 2.0, an open sourced and transparent identity framework that will help publishers, advertisers, and its partners identify users. When browser providers like Google plan to eliminate third party cookies, Unified 2.0 is seen as one of the potential replacements by ad tech firms.

In the Q2 earnings call, Jeff Green, the CEO and Founder of The Trade Desk, mentioned, “I think Snowflake adopting UID2 is one of the biggest headlines that has happened for UID to date and not enough has been said about it. I don't think most people understand why this is so big.” He further added, “So in the same way that Wix made it really easy for companies to build websites, Snowflake makes it really easy for companies to put their data to work.”

The management has maintained since its IPO that the opportunity in data sharing is substantial and largely untapped. In the recent earnings call, the CEO mentioned, “Generally I agree with what your assessment that we are just seeing the tip of the iceberg. Snowflake was built from the ground up as a data sharing platform and we've been at it from the beginning. You see a lot of other players following our lead in this regard, but we are in the beginning.”

The company also follows a consumption model, which makes investment decisions easier for its customers to decide which business units need the workloads. The management gave an example of the financial sector in the earnings call. The CEO mentioned, “That really mitigates the sticker shock, people can make investment decisions as they go along and as it warms it, we're seeing with some of our large banking customers as they went from recomputing loan rates on a monthly basis to doing it every night, while they had a business case for.”

In the most recent quarter, Data Marketplace grew 41%, which is “steady” but expected to could expand at a “meteoric rate” due to the non-linear way data sharing expands.The company recently introduced two industry data clouds: Financial Services Data Cloud and Media Data Cloud. The customers include companies like Allianz, Blackrock, New York Stock Exchange, State Street, Disney Advertising Sales, The Trade Desk, and Experian, among others.

Developers Building Apps with Snowpark

Snowpark offers the ability to migrate business logic with popular programming languages Python, Scala/Java Virtual Machine or Java. The library and DataFrame API allow querying and processing data without having to move data to where the application code runs. This extends programming functionality for ML model training and allows data processing to run natively in the data cloud.

Prior to Snowpark, code deployment required separate infrastructure. Building applications that interact with Snowflake’s virtual warehouses minimizes processing time and lowers the learning curve/broadens adoption of complex data pipelines by removing the need to move or copy data into other systems to overcome working with SQL.

The recent announcement of adding Snowpark for Python is key because of Python’s widespread popularity among developers. With the Snowpark Accelerator, Snowflake is courting developers to build more applications and this is likely to help Snowflake maintain a competitive advantage with a newer class of machine learning startups. The company had 23,000 developers register for the last Snow Day event.

As stated, unstructured data has recently become available in public preview, and this is being leveraged through Snowflake’s newer programmability as customers can now store new data types.

Risks

The company’s revenue growth has been exceptional. However, the company is undergoing losses. There is no clarity as to when the company will be profitable on a GAAP basis. In last year’s Investor Day presentation, the company has laid its roadmap to reach $10 billion in annual product revenue in the FY 2029 and adjusted operating income margin of 10%. So, it suggests that the competition is very high for its bottom line to improve significantly.

The company’s current revenue growth rates might not sustain long-term. The management expects long-term product revenue to grow by 30%. Overall revenue growth is down from 174% in FY 2020 to 124% in FY 2021, and for this year, analysts expect revenue to grow about 104% YoY.

Another key risk we will be monitoring is the reduction in payment terms, as Snowflake is migrating from annual upfront invoicing to quarterly upfront invoicing. This reduces the amount of cash customers have to pay upfront, which can temporarily juice sales. We will need to monitor this trend going forward to ensure that growth will be sustainable as customers fully migrate.

Another risk is the company’s consumption billing model, which is inherently unpredictable. This can make growth lumpy and some quarters may disappoint the Street. Investors should expect increased volatility in growth from Snowflake in the near term as new customers ramp consumption. However, management does expect revenue growth to smooth and become more predictable in the aggregate as customer consumption scales and matures on the platform.

Valuation

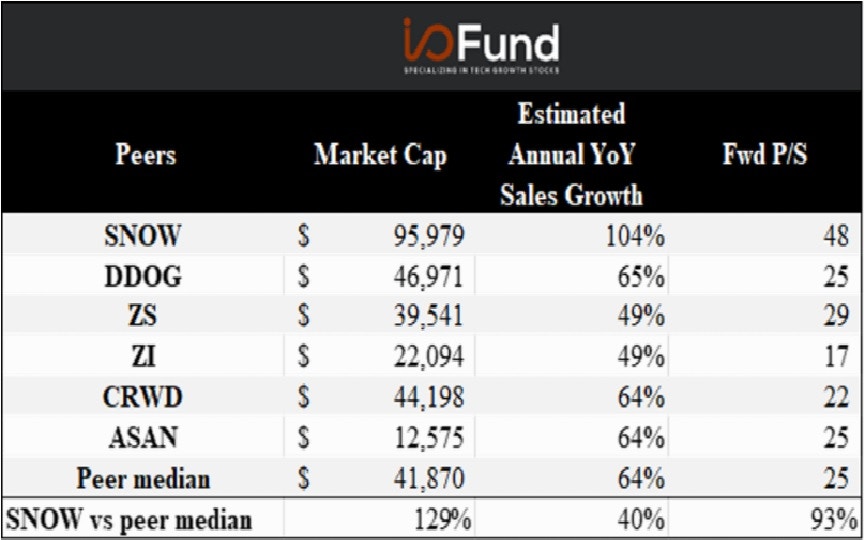

Considering the company’s strong metrics discussed further above, it makes sense that Snowflake trades at a premium multiple compared to other high growth companies. At time of writing, it’s 1-year fwd P/S multiple is 46x and Snowflake trades at a 29x 2-year forward multiple.

Table - I/O FUND

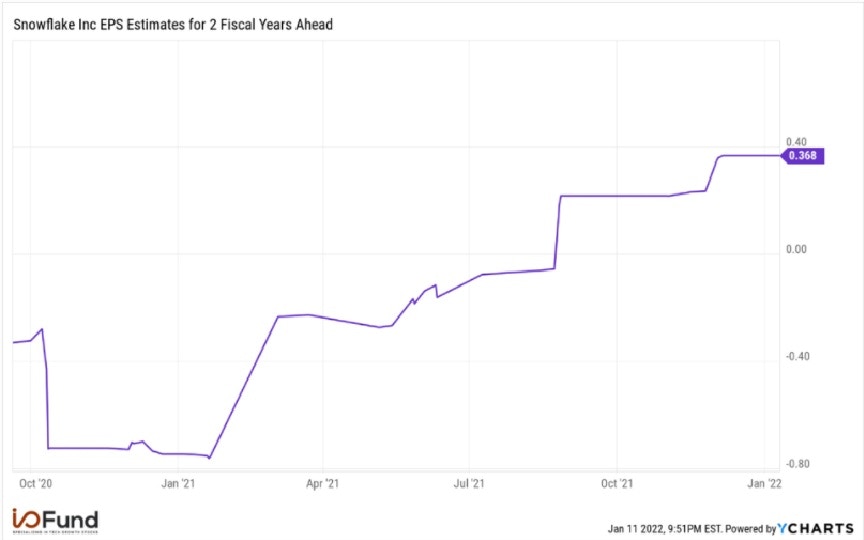

Looking forward, management guided Q4 product sales to increase 95% YoY to $348 million at the midpoint and for FY2022 product sales to increase 104% YoY to $1.1 billion. One year forward, the Street expects FY2023 sales to increase 66% YoY to $2.0 billion and then to further deaccelerate to 56% YoY growth in FY2023 and reach $3.1 billion. EBITDA is also expected to turn positive in FY2023 and then rapidly expand to over $260 million by FY2024.

Snowflake EPS Estimates for 2 Fiscal Years Ahead - YCHARTS

Conclusion

Snowflake separates compute and storage which allows companies to store large amounts of data while running complex queries at high performance. The company also drives down costs for customers newly onboarded due to its pricing model where you pay for only what is used. Snowpark now allows data processing to occur natively on the data cloud instead of external Spark clusters and is opening up complex data pipelines with popular programming languages, such as Python.

The company is disrupting legacy databases while keeping a strong focus on how to lower the barrier of entry for data applications and machine learning workflows. The product is not where the company is often disputed by investors rather it’s the valuation. Those on the sidelines for the past 1.5 years have only given up 30% in gains (in terms of market cap) and have saved themselves a rather rocky, volatile ride. Snowflake has always been a strong company yet the last earnings report was a perfect 10. We think the company may be finally gathering its strength to truly earn its valuation once and for all.

I/O Fund analysts Royston Roche and Bradley Cipriano contributed to this analysis.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

Gains of up to 403% from our Free Newsletter.

Here are sample stock gains from the I/O Fund’s newsletter --- produced weekly and all for free!

+344% on Nvidia

+403% on Bitcoin

+218% on Roku

*as of March 15, 2022

Our newsletter provides an edge in the world’s most valuable industry – technology. Due to the enormous gains from this particular industry, we think it’s essential that every stock investor have a credible source who specializes in tech. Subscribe for Free Weekly Analysis on the Best Tech Stocks.

If you are a more serious investor, we have a premium service that offers lower entries and real-time trade alerts. Sample returns on the premium site include 324% on Zoom, 601% on Nvidia, 445% on Bitcoin, and 4-digits on an alt-coin. The I/O Fund is audited annually to prove it’s one of the best performing Funds on the market with returns that beat Wall Street funds.

More To Explore

Newsletter

Semiconductor Stocks Q4 Overview: AI Gains Heat Up

Semiconductor stocks are standout performers so far in 2024, with investor appetite for AI stocks remaining elevated as AI chip leader Nvidia continues its streak of high growth.

I/O Fund Catapults to 131% Cumulative Performance Due to Leading AI Allocation: Official Press Release

I/O Fund, a tech research site that actively manages a real-time portfolio, announces returns of 57% in 2023 with a cumulative return of 131% since inception. This compares to popular tech ETFs that h

The Importance of Verified Returns and Risk Management for Retail Investors

Last year was a stellar year for investors – in 2023, the Nasdaq 100 rose 54% for its best annual return since 1999, while the S&P 500 gained 24%. The Magnificent 7 were the de facto leaders of this m

Arm Stock: AI Chip Favorite Is Overpriced

Arm Holdings is positioned to capitalize on the growing adoption of artificial intelligence (AI) technologies, leveraging its established licensing model and extensive ecosystem to drive future growth

Top 3 Ad-Tech Stocks For 2024

Ad spending growth is widely forecast to accelerate in 2024, after a challenging macro environment significantly dented budgets and growth in 2023. The US advertising market is already showing positiv

Cybersecurity Stocks: CrowdStrike Soars While Palo Alto And Zscaler Fall

This year has led to a split landscape for cybersecurity stocks, with two of cybersecurity leaders up more than 20% YTD while others are negative YTD. In the past, we’ve discussed the resiliency of th

The Magnificent 7 Are Falling Like Dominos; Only 3 Remain

The Magnificent 7 of 2023 have now become 2024’s Magnificent 3: Nvidia, Meta and Amazon. Of these, Nvidia’s saw a stellar start to the year as shares have gained nearly 60% YTD due to the GPU leader’s

Nvidia Stock Gained $1.5 Trillion To Surpass The FAANGs - Apple Is Next

Today, Nvidia surpassed a $2 trillion market cap compared to Apple’s $2.8 trillion. The company has surpassed Amazon, Google, Tesla, Meta and Netflix. The only one left standing is Apple and we have 2

Palantir Stock Surges From Artificial Intelligence Platform

Palantir’s Q4 earnings confirmed an acceleration in its US commercial business as it closed out its first GAAP profitable year. Shares are reflecting the optimism surrounding Palantir’s commercial seg

AI Driving Acceleration For Big 3 Cloud Stocks

Big Tech’s participation in the market’s push to all-time highs is becoming increasingly narrow, with Nvidia, Meta, Microsoft and Amazon serving as the primary contributors to 2024’s rally.