I/O Fund’s Preview of 7 Semiconductor Stocks Ahead of Q3 Earnings

October 20, 2021

Royston Roche

Equity Analyst

This quarter we chose Nvidia, Lam Research, Ambarella, Advanced Micro Devices, Broadcom, Marvell Technology, and Qorvo for an earnings preview. We also tried to understand what analysts are expecting from these companies. The list includes popular names in the semiconductor sector and companies like Qorvo, which has been out of favor recently in the eyes of investors.

To understand valuations across semis and how the sector is positioned moving into earnings, please reference our analysis “I/O Fund’s Semiconductor Q3 2021 Earnings Preview.”

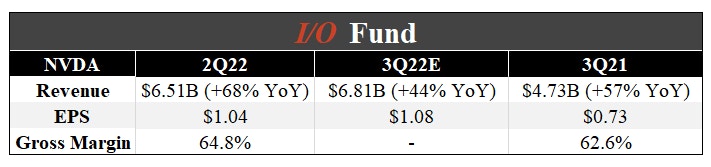

NVIDIA Corporation – Earnings on November 17th

Nvidia’s revenue growth is expected to continue to be strong. Management mentioned in the last earnings call that the QoQ growth will be led by strong demand in the data center along with other segments that are also growing steadily. They also indicated that the gross margins will be around 65.2% plus or minus 0.5%. We also expect some new comments on the Arm acquisition in the earnings call. You can read our analysis of Why the Arm Deal Should be Approved here.

KeyBanc analyst John Vinh has an overweight rating on the stock and increased the price target from $245 to $260. He mentions that “The firm's quarterly supply chain findings are mixed, as demand remains healthy, but a multitude of supply disruptions, including COVID lockdowns in Southeast Asia, power restrictions in China, and kitting issues, could result in near-term uncertainty and limit upside.”

Jefferies increased the price target to $260 from $233. They are positive on the company due to the strong performance of the company’s data center and software segments. Their report also suggests that Nvidia’s share in accelerator instances increased 1% in July to 79% on new deployments of A100 and V100 chips.

Goldman Sachs analyst Toshiya Hari said after the company’s strong previous quarter earnings report, “We increase our go-forward estimates on the back of today’s print, and importantly, continue to view Nvidia as the best positioned company to address and monetize the proliferation of accelerating computing”.

Please note, the I/O Fund may or may not agree with the financial analysts mentioned above yet we objectively report what the Street is saying. You may view our previous analysis on Nvidia below:

The Key To Unlocking The Metaverse Is Nvidia’s Omniverse

Here's Why Nvidia Will Surpass Apple's Valuation In 5 Years

Making Sense of The Nvidia-Arm Acquisition

Our premium members have been updated frequently on the company with ongoing entries at $31.50, $51.20, $97.40, $105.30, $120.60, $124.50, $123.50, $138.90, $206.60, $208.90

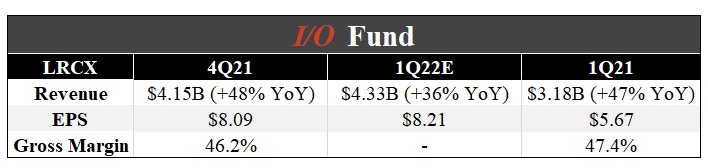

Lam Research – Earnings on October 20th

Lam research continues to have steady revenue growth. The wafer fabric equipment demand has been strong as the semiconductor industry is benefitting from the leading technologies like 5G, IoT, AI, and edge computing.

UBS analyst Timothy Arcuri who has a buy rating on the stock lowered the company’s price target to $715 from $780. The analyst sees some “potential moderation" in DRAM and NAND WFE spending moving through 2022.

Sign up for I/O Fund's free newsletter with gains of up to 1100% - Click here

Susquehanna analyst Mehdi Hosseini downgraded the stock to neutral and lowered its price target to $690 from $750. The analyst says "the beat-and-raise cycle for the company is already behind us with all the good news already dialed. With quarterly wafer fab equipment peaking in the second half of 2021, there is enough of a deceleration in spend growth rate into 2022 that cannot be offset by services and/or share gains.”

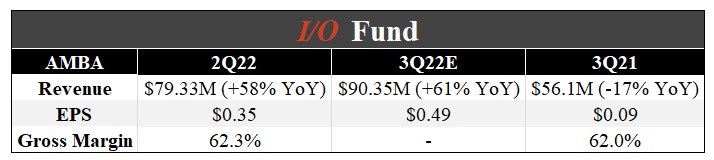

Ambarella Inc – Earnings on November 23rd

Ambarella has seen rapid revenue growth in the last quarter and consensus estimates suggests 61% revenue growth in the next quarter. The company has successfully tapped the computer vision technology market with the increasing demand for its chips for drones, VR cameras, security cameras, and automotive cameras. However, it would be prudent to note that the growth was partly due to lower comps due to Covid-19.

KeyBanc analyst John Vinh upgraded Ambarella to Overweight from Sector Weight with a $185 price target. The analyst sees "multiple favorable tailwinds" related to the adoption of computer vision within the security and automotive end markets amid limited competition with the HiSilicon ban. He also has increasing confidence in front-facing advanced driver assistance systems adoption. Further, with its "highly differentiated CV/AI assets" and adoption in auto tech, Ambarella represents one of the most attractive takeover targets in semiconductors.

Roth Capital analyst Suji Desilva believes “Ambarella represents a differentiated investment opportunity in computer vision and low-power video processors.” He has a buy rating on the stock and has raised the company’s price target to $170 from $130.

Cowen analyst Matthew Ramsay has an outperform rating with a price target of $150. The analyst said “that the business is really inflecting in terms of growth and operating leverage with upside that is no longer a leveraged story to GoPro and drones.”

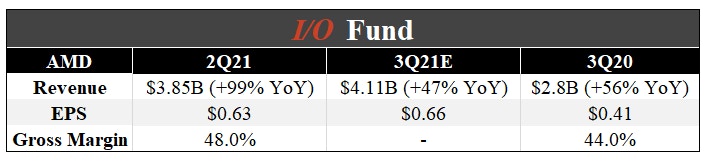

Advanced Micro Devices Inc – Earnings on October 27th

The company had a blowout last quarter. It also raised the revenue guidance for the full-year 2021 and the 5nm roadmap is on track for 2022. The company has been able to capture market share from Intel and reports suggests that Intel might cut CPU server prices.

Source: Earnings Presentation

Piper Sandler analyst Harsh Kumar has a price target of $120 and an overweight rating. The analyst says AMD is looking very solid into year-end and is very well positioned as enterprise spending returns, as the company should benefit within both the PC and server markets.

BMO Capital analyst Ambrish Srivastava has a price target of $110. He says " Considering the company's continued execution and the expansion in estimates, the shares look relatively more reasonably valued than they did earlier in the year,” argues Srivastava, who also believes there is continued upward bias to estimates through the year as AMD starts to ramp designs it has already won on the data center side.

Goldman Sachs analyst Toshiya Hari has a buy rating and a price target of $130. In his words “We believe AMD’s recent CPU/GPU wins in supercomputing have important and positive implications for the company’s forward trajectory in the data center, as design wins in supercomputing are awarded based primarily on performance with good insight into future technology/product roadmaps”.

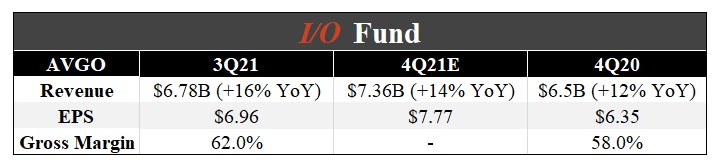

Broadcom Inc – Earnings on December 10th

Broadcom delivered record revenues in the third quarter with good growth in cloud, 5G infrastructure, broadband, and wireless. The management expects the trend to continue in the next quarter. The free cash flows were 51% of total revenue and they expect the cash flows to be strong in the next quarter.

Sign up for I/O Fund's free newsletter with gains of up to 1100% - Click here

Barclays’ analyst Blayne Curtis has an overweight rating and a price target of $540. In his words “AVGO has one of the highest exposures to the Enterprise end market (50% of semi revenue), which should continue to improve into next year. AVGO guided Wireless up 33% QoQ (in line with our model) and we see some upside into Jan given likely contents gains at AAPL (WiFi 6E, touch, wireless charging, DCM) with another potential step up in 2023 with the AAPL modem. AVGO remains one of our preferred names for 2022 given its cheap relative valuation, more resilient end markets into next year (Ent, DC, Wireless), further content gains at AAPL, and likely accretive Software M&A”.

Truist analyst William Stein has a buy rating and a $564 price target. In his words “Investors should continue to buy the stock for its 3% dividend yield and the double-digit dividend growth over the long term”.

JPMorgan analyst Harlan Sur has an overweight rating and a $600 price target. He believes that the “stock offers a solid setup for 2022 based on order visibility and product cycles”.

We’ve discussed in the past how Broadcom could potentially be a good choice for an inflation trade:

Will Dividend Stocks Become the Inflation Trade?

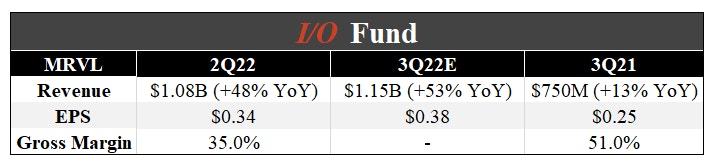

Marvell Technology – Earnings on December 3rd

The company’s revenue growth has been strong due to the growth in the data center revenues (40% of 2Q FY22 revenues). The inclusion of Inphi also provided an earnings bump. The management believes that the data center will further drive the third quarter growth along with 5G business. During the recent Investor Day the company increased the long-term growth rate to 15%-20%.

Needham analyst Quinn Bolton has a buy rating and a $75 price target. "Marvell's management highlighted the significant growth opportunities associated with cloud-optimized silicon. These growth drivers are accelerating the company's SAM, which is now forecast to grow from $20bn in 2021 to $30bn in 2024, or at a 13% CAGR, with the 5G/data center/automotive portion of this SAM growing at a 20% CAGR over this period.”

Barclays’ analyst Blayne Curtis has an overweight rating and a price target of $70. In his words “Marvell raised its growth target of 15-20% with drivers across every segment. This has been a multi-year transition but the message was very clear that the company has re-shaped its portfolio to take advantage of growth in the Cloud and Infrastructure markets with the broadest set of IP and process technologies.”

KeyBanc analyst increased the price target to $80 from $70. “Marvell increased its long-term revenue growth target to 15%-20% from 10%-15% previously. The increased growth rate is being driven by Increased focus on optimizing solutions for cloud data center growth, emphasis on auto, cloud and 5G, and expansion into autonomous compute processors, which represents a $5.3B TAM.”

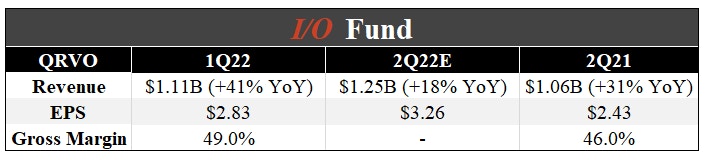

Qorvo Inc – Earnings on November 04th

The company’s 1Q FY 22 results have been good. However, the stock has failed to meet market expectations. The management’s revenue guidance for the next quarter is $1.235B to $1.265B, the midpoint $1.25B suggests a 18% YoY growth and a growth of about 27% YoY when adjusted for last year’s 14-week quarter. They also increased the top line forecast for the fiscal year 2022 to 15%-20% from the earlier of approximately 15%.

Oppenheimer analyst Rick Schafer raised the company’s price target to $250 from $220 after the company earnings beat and forecast upgrade. He is positive on the company increasing the outlook in spite of the supply constraints.

Benchmark analyst David Williams has a buy rating and $225 price target. He is also positive after the company’s strong previous quarter results. “The demand environment remains strong and he continues to appreciate incremental content gains in 5G with increasing complexity”.

Craig-Hallum analyst Anthony Stoss also raised the company’s price target to $225 from $220. The analyst cites “big bottom-line beat, with Qorvo posting a 52.5% gross margin, and operating margin of 33.1% near record levels.”

The I/O Fund is a team of analysts that share their research publicly as they build a portfolio of 30 stocks. Our team has record results for a retail Fund and we also have four-digit gains on some of our free newsletter coverage. You can learn more about our premium service by clicking here or sign up for our free newsletter here.

Our premium members have been updated frequently on Nvidia with ongoing entries at $31.50, $51.20, $97.40, $105.30, $120.60, $124.50, $123.50, $138.90, $206.60, $208.90

Disclaimer: This is not financial advice. Please consult with your financial advisor in regards to any stocks you buy.

Gains of up to 2,390% from our Free Newsletter.

Here are sample stock gains from the I/O Fund’s newsletter --- produced weekly and all for free!

+2,390% on Nvidia

+450% on Bitcoin

*as of Jun 25, 2024

Our newsletter provides an edge in the world’s most valuable industry – technology. Due to the enormous gains from this particular industry, we think it’s essential that every stock investor have a credible source who specializes in tech. Subscribe for Free Weekly Analysis on the Best Tech Stocks.

If you are a more serious investor, we have a premium service that offers lower entries and real-time trade alerts. Sample returns on the premium site include 3,900% on Nvidia, 850% on Chainlink, and 695% on Bitcoin. The I/O Fund is audited annually to prove it’s one of the best-performing Funds on the market, with returns that beat Wall Street funds.

More To Explore

Newsletter

Mag 7 Stocks Should See One More High

Optimism around the Fed could spark a continuation of the relief rally in the Russell 2000 and further rotation out of the Mag 7. Below, we look at the pros and cons of a Mag 7 rotation and how we pla

Palantir’s Stock Is Priced For Perfection

Heading into 2024, Palantir was exhibiting “multiple signs of acceleration” stemming from strong growth in its US commercial segment, driven by AIP, Palantir’s Artificial Intelligence Platform that le

Tesla’s Q2 Deliveries Strong, But What’s To Come?

After months of being the lowest performing Mag 7 stocks, Tesla saw rapid gains — up 42% in a one month rally, with 37% of those gains in eight sessions — after it reported Q2 deliveries ahead of expe

How to Participate in Tech: The Million Dollar Question (Video Highlights)

With audited returns of 131% since inception, compared to the NASDAQ-100’s 82%, portfolio manager, Knox Ridley, lays out how we have successfully maintained an overexposure to the right tech stocks, w

This AI Stock Could Outpace Nvidia’s Returns by 2030

Lead Tech Analyst and CEO Beth Kindig recently joined Real Vision’s Nico Brugge to discuss her AI outlook on leading AI stock Nvidia, while sharing which AI stock she believes may outpace Nvidia’s ret

AI PC Stocks: Emerging 2024 And 2025 Story

Currently, there is a major bottleneck right now for AI applications to where client devices are not powerful enough or energy efficient enough to leverage AI capabilities at the edge.

AI Power Consumption: Rapidly Becoming Mission-Critical

Big Tech is spending tens of billions quarterly on AI accelerators, which has led to an exponential increase in power consumption. Over the past few months, multiple forecasts and data points reveal s

With Bitcoin at All-Time Highs, Here’s What’s Next for COIN, HOOD

Bitcoin and the spot BTC ETFs have clearly seen strong investor appetite since the approval in the beginning of the year. Alongside strong initial adoption of the new ETF class, we’re also seeing majo

Here's Why Nvidia Stock Will Reach $10 Trillion Market Cap By 2030

I believe Nvidia can achieve an astonishing $10 trillion market cap by 2030. As you’ll see from the key points to my thesis, there is a bull case where a $10T market cap estimate in a little over six

Taiwan Semiconductor Stock: April Sales Soar From Advanced Nodes

Despite warning of a slowdown in the broader semiconductor industry this year, TSMC’s April sales surged 60% YoY and 21% MoM. This marks a positive start to the 20-percentage point acceleration to 33%