AWS DocumentDB and MongoDB Atlas: Friend or Foe?

July 25, 2019

Beth Kindig

Lead Tech Analyst

MongoDB outperformed the tech sector a few times over the past 12 months, most notably during Q4, when MongoDB managed to trade between $65 and $80. The stock recouped losses by early December, when MongoDB reached new highs at $90 per share. By March, MongoDB had gained more than 50% off its new highs to $152 in March.

MongoDB’s Atlas has proven to defy gravity even in the face of AWS launching a competing product called Amazon DocumentDB in January. This sent shares of MongoDB down 15 percent, with a few larger investors exiting based on the news, but the company quickly shrugged it off.

The first quarter results reported a 78% year-over-year increase in total revenue with a 82% increase in subscription revenue. Notably, the company reported first-quarter net losses of $33.2 million, or 61 cents a share, compared with losses of $26.6 million, or 53 cents per share, in the year-ago period. Adjusted losses were 22 cents a share.

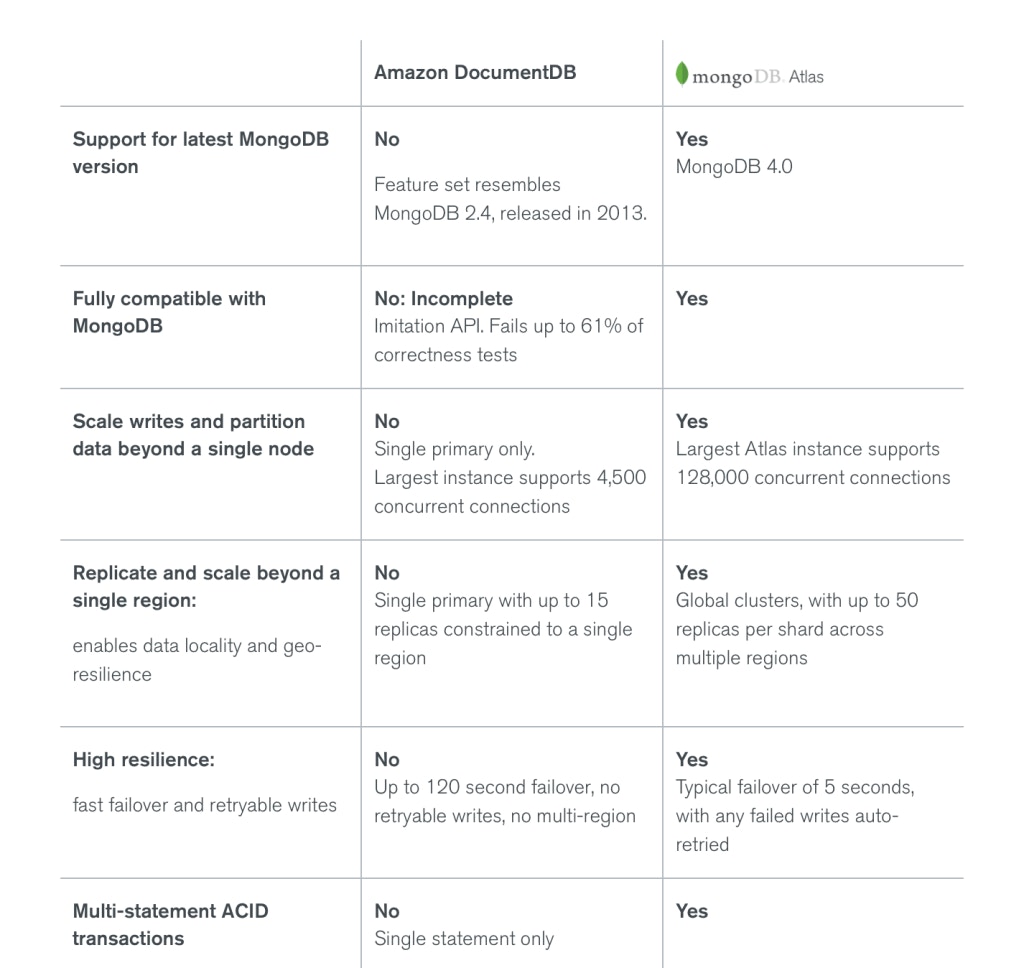

AWS Pitches MongoDB Atlas at OSCON

Amazon’s DocumentDB advertises MongoDB compatibility in its headline throughout the AWS website while MongoDB’s Atlas website focuses on the differences between the two products. AWS wants to be seen as a friend, but MongoDB thinks they are more of a foe.

Amazon’s NoSQL JSON document database is not based on the MongoDB server, however, and there are key differences which AWS’s product is unlikely to compensate for.

Here are a few:

AWS walks a razor edge between capturing the NoSQL database revenue segment or disrupting the customer base, who now have many options in cloud, including Microsoft and Google Cloud – both motivated to compete with AWS from any angle. Trying to disrupt MongoDB’s Atlas could have the opposite effect on AWS as developers are notoriously tribal.

Not surprisingly, last quarter, MongoDB announced a new business partnership with Google Cloud Platform with MongoDB’s Atlas integrated into the GCP console. MongoDB also announced new product features, including Atlas Data Lake, Atlas Full-Text Search and increased availability of MongoDB Charts. These upgrades will be hard for larger, more diversified tech companies (like AWS) to keep up with.

Needless to say, I was on the edge of my seat at OSCON when Amazon presented a keynote and pitched MongoDB Atlas to the crowd. At OSCON, Amazon stated that “AWS effectively endorses MongoDB Atlas as the segment winner” and that MongoDB Atlas is an “AWS reinvent 2019 top level sponsor.” Amazon also stated that Atlas growth has continued on the platform after the AWS DocumentDB release.

Takeaway:

The financial markets guessed wrong about AWS’s ability to compete with MongoDB. We see very little evidence that AWS’s DocumentDB has been a success with Amazon changing its tone at a recent software developer conference. One area that I have written extensively about is developer mindshare, as software developers are not easy to convince. You can access my analysis on Nvidia and developer mindshare here – the time to learn a new AI and ML platform is one reason I remained long on Nvidia during the crypto sell-off.

“Imitation is the sincerest form of flattery, so it’s not surprising that Amazon would try to capitalize on the popularity and momentum of MongoDB. However, developers are savvy enough to distinguish between the real thing and a poor imitation,” Dev Ittycheria, MongoDB’s CEO

In addition, IDC updated its forecast and expects the worldwide database software market to grow from $64 billion in 2019 to $98 billion in 2023. MongoDB’s Atlas is positioned to capitalize on this growth, especially as a flexible option for running applications on-premise, in a private cloud, or a private cloud, without being locked into any one cloud vendor.

After gaining 200% in the past two quarters, is MongoDB still a buy? Premium research members receive updated recommendations and entry/exit scenarios on tech stocks. Learn more here.

Recommended Reading:

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per