Nuclear Power Emerging as a Clean AI Data Center Energy Source

June 27, 2025

I/O Fund

Team

Nuclear energy is emerging as a cleaner solution to power future AI data centers, which require constant, clean, and reliable baseload electricity to meet around-the-clock AI demand. Over the past year, interest in nuclear has accelerated, with Big Tech signing multiple nuclear power purchase agreements while US policy aims for accelerated development of the industry.

Inference is expected to be a primary factor in surging power demand in AI data centers. Power demand for inference tasks is projected to increase at a 122% CAGR through 2028, as providers work to serve billions of requests and process hundreds of trillions of tokens. Big Tech is already showing signs of explosive inference growth with token generation up 5x to 9x YoY.

As AI data centers push for scalable, clean energy sources, nuclear energy is receiving renewed attention despite having higher costs and some of the longest time to power in the industry.

Below, we discuss nuclear energy’s potential to aid growth in AI data center power demand, its advantages and drawbacks, plus Big Tech’s increased interest in nuclear, including a record-setting deal, and more.

GPU Power Consumption Continues to Soar

One year ago, we first discussed how quickly power consumption was increasing with new GPUs in the analysis AI Power Consumption: Rapidly Becoming Mission-Critical. This trend is set to continue with Nvidia pushing towards an ultimate goal of super-sized 1MW server racks, or 8x more than GB200 racks.

Nvidia’s Blackwell lineup already brings a significant increase in power consumption, nearly double the H200’s 70 kW at 120 kW for the GB200 NVL72 and 140 kW for the upcoming GB300 racks.

Beyond Blackwell, Nvidia’s future design lineup shows continual increases in power consumption. Its Rubin generation is expected to boost thermal design power (TDP) by 50% over Blackwell at up to 180 kW per rack, with the upgraded Vera Rubin then doubling this to 360 kW per rack by 2027. In its largest configuration, the Vera Rubin NVL576, dubbed the ‘Kyber’ rack, could draw as much as 600 kW (0.6 MW), or 5x that of the GB200 NVL72 in just a two-year design timeframe.

This is paving the way for the path to 1 MW GPU server racks by the early 2030s. While not much is known about Nvidia’s Feynman generation, it is also likely to bring higher TDP versus Rubin, and a possible shift from direct-to-chip cooling to immersion cooling to handle immense thermal needs. Additionally, researchers from KAIST predict that the accelerator industry could see server racks as large as 1.54MW by 2032, or more than 12x growth from the GB200s in seven years.

This continuous upgrade cycle to more powerful GPUs is likely to further boost data center electricity demand due to the sheer increase in TDP that each generation brings combined with a path to larger cluster sizes. However, moving to 1MW servers and beyond will likely require significant advancements in cooling tech and widescale commercialization of immersion cooling to handle these intense thermal needs.

AI Data Center Electricity Demand Forecasts Show Major Growth

Driven by the explosion in AI demand over the past two years, this current acceleration in inference, and increasingly power hungry GPUs, AI data center electricity demand is forecasted to surge over the next few years. We have a handful of different viewpoints and projections from analysts and industry groups that, while differing slightly in timelines and scope, all point to the same conclusion.

First, let’s put in perspective how much power data centers need. For example, OpenAI’s Stargate data center in Abilene, Texas is expected to have a 1.2 GW capacity with its second phase under construction, or enough power to supply approximately 1 million homes. When you factor in Nvidia saying that it has visibility into tens of gigawatts of projects, that would be the equivalent of tens of millions of homes that the power grid will soon need to account for.

In a shorter-term view, Boston Consulting Group forecasts global data center power demand to rise at a 16% CAGR from 2023 to 2028, accelerating from a 12% CAGR. Hyperscalers are projected to account for 60% of this demand growth.

Within BCG’s forecast, generative AI power demand is estimated to rise at a 65% CAGR, with AI training increasing at a 30% CAGR and inference rising at a rapid 122% CAGR. By 2028, BCG estimates gen AI will account for more than one-third of global data center power demand.

Global data center power demand is expected to accelerate to a 16% CAGR through 2028, driven by generative AI and inference demand. Source: BCG

Deloitte similarly sees surging growth for power capacity in the US, forecasting 5x growth over the next decade. The firm estimated US data center power capacity to rise 24% from 33 GW in 2024 to 41 GW in 2025, before tripling to 120 GW by 2030 and rising further to 176 GW by 2035.

Goldman Sachs estimated global data center power usage at 55 GW in early 2025, far below BCG’s 82 GW figure. However, GS projects power usage to reach 84 GW in 2027 and increase further to 122 GW by 2030.

AI Data Center Electricity Share Could Reach Double-Digits

In terms of electricity share, AI is expected to account for a much larger proportion of demand by 2030, especially in data-center heavy regions.

The Electric Power Research Institute forecasts that data centers may see electricity consumption more than double by 2030, to account for 9% of the US’ total electricity demand. Globally, a report from SPhotonix estimates that data centers could account for 13% of total electricity demand by 2030.

The Department of Energy projects that data center demand could nearly triple by 2028 in its high-end scenario, accounting for 12% of the US’ total demand, compared to just 4.4% in 2023. The agency’s low-end scenario projects data centers reaching 6.7% of total demand. Meeting this increase in demand in such a short time could require between 33 GW to 91 GW of new generation capacity.

However, in more localized regions that have concentrated data center presence, such as Northern Virginia, data center electricity demand may be far higher and place further strain on the local grid. For example, Northern Virginia has more than 5.9 GW of data centers in operation, 1.8 GW under construction, and another 15.4 GW of planned projects. Per the EPRI, data centers already account for 25% of Virginia’s electricity demand, amplifying concerns that this demand will outstrip supply and cause rolling blackouts. This does not even account for the 3x growth in data centers based on the planned project backlog.

Why Nuclear is Emerging to Serve AI Data Center Power Needs

Given that time to power has been floated as a constraint by Big Tech executives recently, it’s important to touch on why nuclear is being named to address rising power demand considering other fuel sources can have much quicker time to power. Nuclear could add dozens of GW to the grid to serve data center needs, with up to 174 GW of capacity potentially able to be retrofitted at existing power plant sites.

Compared to other fuel sources such as coal, solar and wind, nuclear provides a few key advantages for AI-focused data centers:

Reliable baseload energy source: Unlike solar, wind and natural gas, nuclear provides data centers with access to highly efficient, reliable baseload power. Nuclear’s capacity factor (ratio of electrical output vs maximum capacity) can exceed 92.5%, far outpacing other renewable or preferred power sources, including wind at a 35% capacity factor (CF), solar at 25%, and natural gas at 56%. Nuclear is also not reliant on weather conditions and reduces interruptions that may be faced with wind or solar.

High energy density and zero emissions: Nuclear is highly dense, with nuclear power plants producing around 1 GW on average, or enough for five 200MW data centers per plant. Nuclear is also virtually emission-free, aiding countries or providers in meeting rising electricity demand while aligning with net-zero commitments. As seen in the graphic below, based on the average use per person of 235,000 kWh/year, nuclear’s fuel requirements are <2% of other common fuel sources with far fewer emissions.

Nuclear requires far less fuel than coal, oil or natural gas to produce equivalent output, with minimal emissions. Source: IEA

Scalability: Due to its high density, nuclear’s high output per plant makes it a suitable choice for larger data centers, as a single reactor could meet the needs of a large hyperscale data center campus or power multiple smaller data centers if used solely for that purpose.

Grid stability and on-site needs: Co-locating nuclear with AI data centers can reduce stress on the grid as nuclear’s high output could limit reliance on existing grid infrastructure, while excess power generated could be returned to the grid. Modular reactors also promise ease of providing on-site power generation either on or off grid. In the case of Northern Virginia, nuclear could ease pressure on the grid given the substantial backlog of projects planned in the region.

Large existing footprint: A substantial amount of nuclear power could come from retrofitting existing sites, with analysts from Goldman Sachs estimating that between 60 GW to 95 GW of new capacity could use existing sites, reducing costs and construction timelines. It’s also estimated that anywhere between 128 to 174 GW of nuclear capacity could be retrofitted at operating or retired coal plants.

Small modular reactor (SMR) tech: SMRs are emerging as they promise quicker time to power with shorter construction times and lower costs, while offering more flexibility in deployment versus a large-scale plant. SMRs could offer up to 300MW capacity, able to power larger data center campuses without supporting infrastructure. However, SMRs are far from full-scale commercialization, with the first reactors likely not coming online until around 2030.

For additional reading, we have covered other data center power sources in these articles:

- AI Data Center Power Wars: Brown vs. Clean vs. Renewable Energy Sources

- Unlocking the Future of AI Data Centers: Which Fuel Source Reigns Supreme in Efficiency?

A Note on Increased Policy Support

While Big Tech’s quick turn to nuclear over the past year is supporting prospects of reigniting the industry at large, increased policy support from the current administration also serves as a tailwind.

President Trump signed four executive orders targeting accelerated nuclear deployment and setting a goal of quadrupling US nuclear output by 2050. The orders call for increased uranium mining and enrichment capabilities to bolster the domestic supply chain, as well as accelerated testing of advanced reactor designs including SMRs and faster regulatory approval processes.

Last week, the DOE announced a new program to help streamline the approval process and unlock private funding for advanced reactors and SMRs, aiming to have “at least three reactors achieve criticality by July 4, 2026.” Initial applications are due by July 21, 2025.

Nuclear Energy has a Few Key Disadvantages

Although nuclear has been gaining traction for AI data center needs, there are a few key downsides, most notable time to power and cost:

High capex requirements: Capex for nuclear power plants is estimated to be 5x to 10x that of using natural gas, with nuclear costing between $6,417 to $12,681 per kW compared to $1,290 per kW for natural gas. Deloitte says restarting retired plants can significantly lower capex compared to new construction, with an estimated cost of approx. $6.2B for three plants with 2 GW capacity versus $37B for the same capacity in new construction.

Long time to power: Nuclear faces long construction timelines, with large reactors (1 GW) taking between five years to nearly 11 years from breaking ground to connection to grid. Though slightly quicker, SMRs can still require nearly four to six year timelines. With power being a primary constraint and time-to-power at the forefront of discussions for Big Tech executives, nuclear’s prolonged construction may make it a story for 2030 and beyond, given that solar, fuel cells, and natural gas provide quicker alternative options.

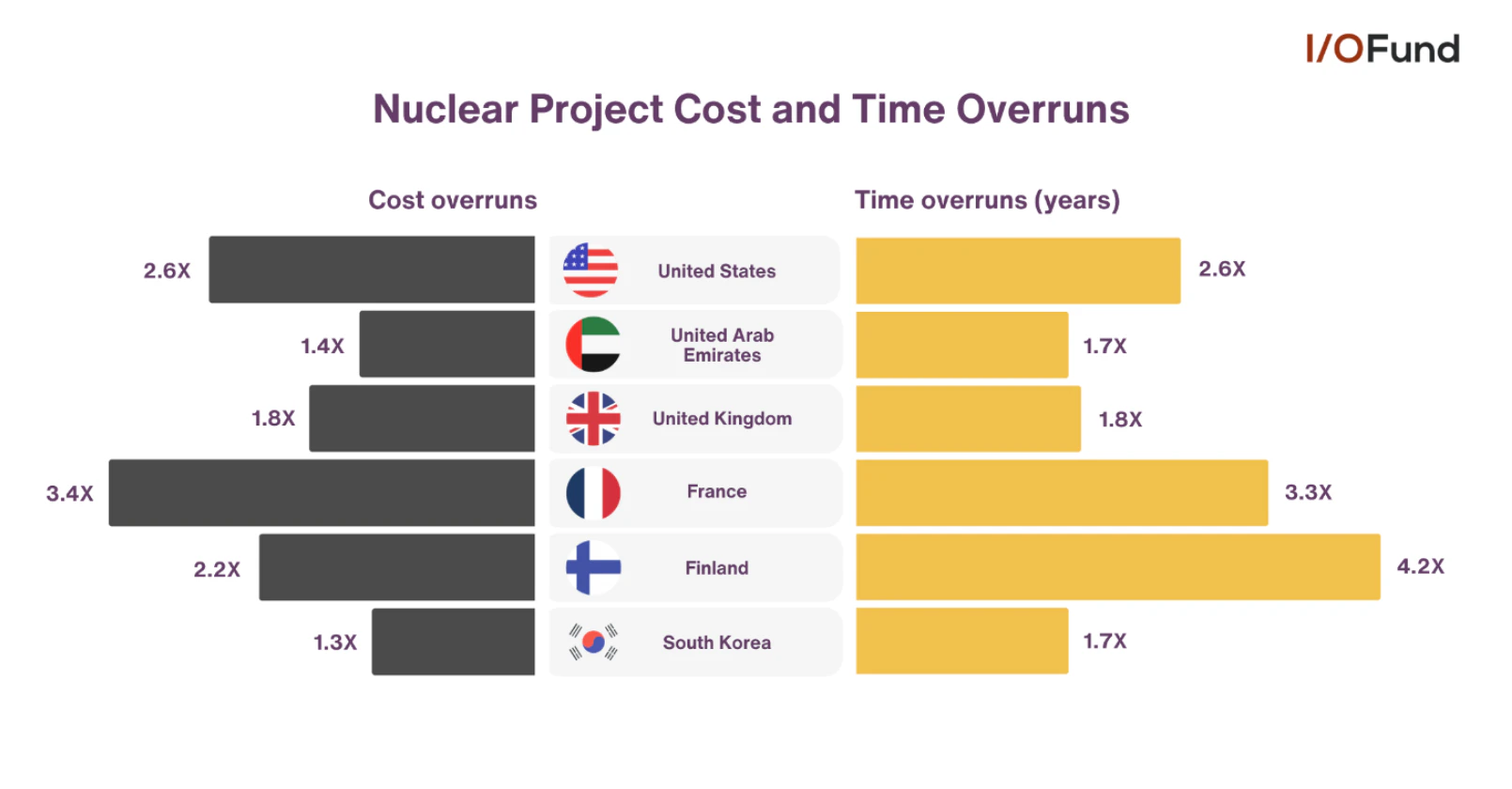

Cost and time overruns: Nuclear plants often see delays and higher costs than expected, and this is not isolated to the US. Per the IEA, nuclear projects in the US often see up to 2.6x overruns on cost and time in years, while France sees overruns greater than 3x. Break-even point for new builds tends to be ~30 years after breaking ground, with overruns potentially pushing this farther into the future.

Nuclear power plant projects often face significant time and cost overruns, prolonging lengthy construction timelines and adding to high costs. Source: IEA

Low thermal efficiency: Despite having a high capacity factor, nuclear has a rather low thermal efficiency, meaning more of its power is lost to heat. Nuclear’s thermal efficiency is typically between 33% to 40% depending on reactor type, comparable to natural gas at 35% to 42% on a simple cycle gas turbine. However, when using combined cycle gas turbines, natural gas could see its thermal efficiency as high as 62%, making it more efficient and quicker to stand up than nuclear.

Utilities Poised to Benefit from Big Tech Data Center Partnerships

Subscribe Below for Free to Access the Following:

- Info on new partnerships from Big Tech including a record-breaking multi-billion dollar nuclear deal

- An overview of nuclear stocks poised to benefit from increased AI data center power demand

- The one fuel source that is filling the gaps and meeting immediate power needs for Big Tech

More To Explore

Newsletter

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i

Google TPU v8 vs Nvidia: How Inference Is Rewriting the AI Market

In April, Google announced it would begin selling its TPUs to select third-party data center operators, which is something the market has anticipated for nearly a decade. The TPU-versus-Nvidia-GPU deb