Palantir IPO: Deep-Dive Analysis

October 04, 2020

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Sep 29, 2020,11:17pm EDT

The Economist was correct when it recently stated that Palantir is “more than a technological project, it is a philosophical, even political one.” Palantir has a mythical and esoteric reputation in the Bay Area. The name is well-known and what the company does has circulated for years, which in a nutshell, is data mining for the government — and now, commercial clients.

Until recently, a customer list and any level of transparency has gone against the core purpose of the company. Therefore, I was somewhat surprised at the leak in 2018 that Palantir was considering a public offering as it seemed odd the company would operate openly and transparently. In fact, about five years earlier, the CEO had said an IPO was unlikely as it would make “running a company like ours very difficult.”

Nonetheless, the company is wanting to attract more commercial accounts and going public should help facilitate this. The old adage, “you can’t sell a secret” may be hindering Palantir’s growth especially as artificial intelligence startups raise their first and second rounds. Now is a good time to make sure to penetrate commercial accounts before AI brings more direct competition.

Below, I go over some of the folklore that surrounds Palantir and then I discuss the S-1 filing.

The Folklore around Palantir

Palantir can neither confirm nor deny if the software was used to kill Osama bin Laden, but the CEO required a body guard as of 2013, and it was generally understood for about a decade that Palantir had only one customer: the CIA; and then three customers: the CIA, the FBI and the NSA.

By 2015, a leaked document from TechCrunch dated in 2013 confirmed twelve government agencies were using Palantir, including the “CIA, DHS, NSA, FBI, the CDC, the Marine Corps, the Air Force, Special Operations Command, West Point, the Joint IED-defeat organization and Allies, the Recovery Accountability and Transparency Board and the National Center for Missing and Exploited Children.” Palantir’s leaked document was the first time the CIA and the FBI had databases linked rather than siloed.

Nearly twelve years after Palantir was founded in 2003, that leaked document was the only record that indicated who used the company’s software. Palantir can be a divisive company that draws strong opinions from supporters and critics. Regardless of how you feel about the work Palantir does, one thing is for certain: when the stock trades on the public market, the company will dominate headlines.

Often those headlines will get it wrong in an attempt to frame Palantir in various lights. For instance, I don’t think anyone in Silicon Valley batted an eye at Alex Karp’s letter when the company exited for Denver. He stated that engineers “may know more than most about building software but they do not know more about how society should be organized or what justice requires. Our company was founded in Silicon Valley. But we seem to share fewer and fewer of the technology sector’s values and commitments.”

These sensational headlines and CEO-centric storylines can be a bit distracting. When looking at things rationally, it’s probably better that Palantir be in Denver as government is a major industry in Colorado and being centered in the country will position Palantir closer to Washington D.C. Palantir’s investors are not traditional Silicon Valley VC-firms, either. The company was likely in SF/SV to attract top talent. There is also the theory that it was Silicon Valley that turned cold towards Palantir, as voiced by a privacy and technology advocate Harrison Rudolph.

In-Q-Tel, one of the venture firms that invested in Palantir, is located in Virginia and is funded by the CIA. This group has funded many projects, including Google Maps, Gitlab, Pure Storage, MongoDB, Cloudera and FireEye – but Palantir is on a different level as the CIA was the primary customer for many years. For these other companies, the CIA was not a primary customer. In-Q-Tel does not typically disclose funding rounds, amounts or dates. However, according to CNBC, Palantir received a $2 million funding round in 2004. Other investors include Peter Thiel, Stanley Druckenmiller and Tiger Global.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

On the positive side of things, Palantir is believed to have helped with counter-terrorism, human trafficking and disaster response. On the more questionable side, the company has admitted to helping ICE deport immigrants. The company embodies taking the good with the bad. A former Marine, Samuel Reading, was quoted saying “it’s the combination of every analytical tool you could ever dream of. You will know every single bad guy in your area.” That, of course, implies having to know every good guy in the area too.

In the past, the Board has included Condoleeza Rice and former CIA director George Tenet, who said “I wish we had a tool of its power” before 9/11. The software was also allegedly used to convict Bernie Madoff.

Just when you think Palantir couldn’t be steeped in any more controversy — there’s more. In 2016, the company sued the United States Army for unlawful procurement solicitation for the Army’s internal intelligence software suite. Palantir argued the Army should be stopped from developing a risk-prone software project that would cost more than using Palantir’s software. In the end, Palantir won and the Army signed a $800 million contract over the course of 10 years.

So, why is Palantir going public now? Well, for one, it will be easier to gain corporate clients if the company becomes a stock market darling. The stock market is becoming a phenomenal source of free press and Wall Street will glamorize the company if it produces solid returns. This, in turn, will help Palantir attract more commercial customers and perhaps bury any ethical opposition.

The markets came close to burying the ethical issues around Uber. Perhaps this time it will succeed with Palantir. I also personally believe Palantir’s wide lead and lack of direct competitors (moat) will erode with artificial intelligence and machine learning. Time is of the essence to go public as AI startups need another few years before they can compete on this level.

Palantir’s Product:

Founded in 2003, Palantir is described as a company specializing in big data analytics. Palantir’s specific expertise in government intelligence and its existing ties to national security and the intelligence community differentiate its offering from competition.

Palantir will say the company does not provide the raw data, rather discovers patterns in large data sets. Investigative reporters have asserted the company helps some agencies use mass surveillance systems, and therefore, this line is blurred. Those are two of many opposing facts about this company.

The company has two platforms: Gotham and Foundry. These platforms allow organizations to combine core data with critical tools into a single platform to help users obtain actionable insights from a unified data asset. What Palantir tackles is the issue of data being siloed and ineffective for problem solving. These problems may relate to manufacturing, product development or customer experience.

The data Palantir gets is from the customer themselves and their existing databases although Palantir can crawl and scrape data that is freely available. For instance, Palantir can easily scrape public social media profiles but probably does not have access to private profiles except when the FBI issues government requests to Facebook.

The traditional deployment involves hosting Palantir servers in a customer’s data center. There is a cloud-based offering, as well, so the company can work across a range of hosting environments.

The company differs from a business intelligence solution like Tableau, Alteryx or Cloudera by answering questions that a model cannot answer. An example might be “how do we service car loans to people least likely to default” or “how do we catch fraud before it happens.” With traditional BI, it’s assumed you have the complete data set. Palantir tackles situations where a company may not have the complete data set. This is a crucial difference.

Palantir Gotham was the company’s first platform, built for government operatives in defense and intelligence sectors. The platform enables users to identify patterns hidden deep within datasets using semantic, temporal, geospatial and full-text analysis.

Here are some ways the platform is used:

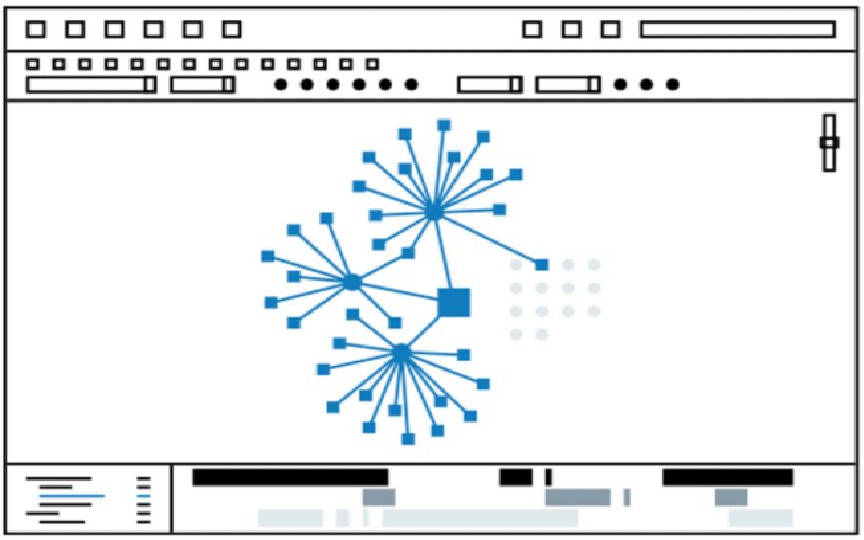

Graph: This application allows data objects to be seen as nodes and edges. Users can visualize events, filter objects and plot characteristics in a logical manner.

SOURCE: PALANTIR.COM

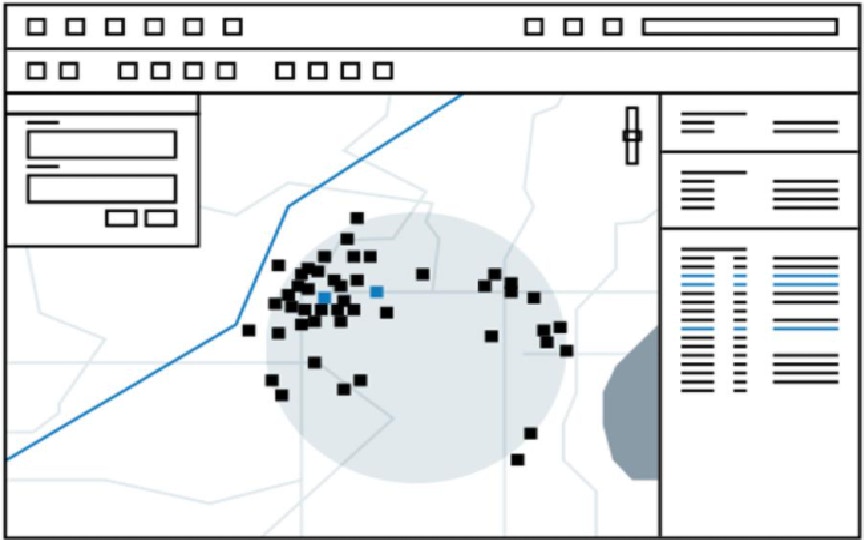

Map: This brings geospatial capabilities to track geo-located objects and events and to create heatmaps for the density of the objects.

SOURCE: PALANTIR.COM

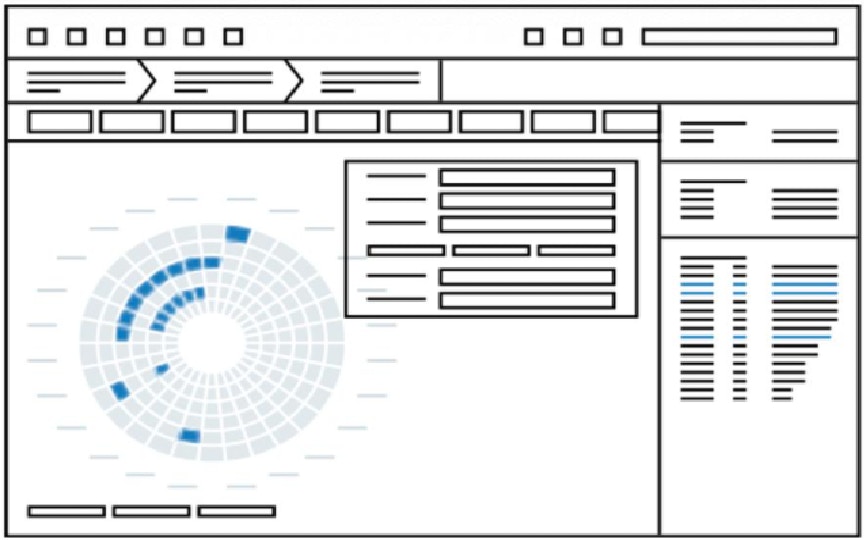

Object Explorer: This feature is powered by the Horizon in-memory database, which competes with Apache Spark by letting users query billions of objects. The database provides further analysis for Map and Graph data.

SOURCE: PALANTIR.COM

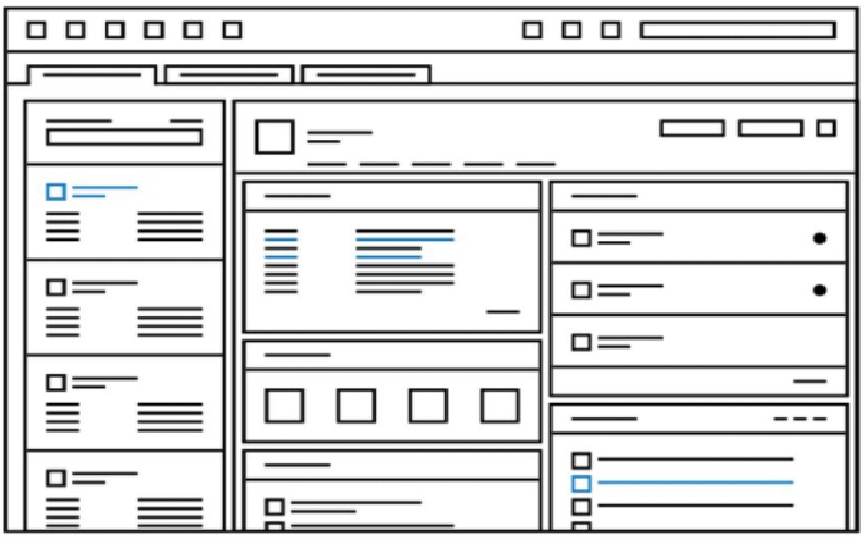

Browser: This enables search queries for investigations and surfaces information, runs relevant searches, displays key data points and answers analytical questions.

SOURCE: PALANTIR.COM

Palantir Foundry is the commercial offering and has four layers of tooling: Foundry Core, Data Foundation, Ontology and Workflows.

This four-step process does the following:

- brings volumes of data into one place,

- transforms the data into a format that analysts can work with and enables validation in any number of programming languages

- the “ontology layer” allows datasets to be turned into real-world concepts with the ability to accelerate on the company’s core ontology to reduce redundancy

- workflows is where it all comes together in an integrated environment for object exploration, point-and-click top down analysis, code authoring, time series analysis, data science and application development. When a user has a question, it answers it using all layers and tools available.

Palantir describes Gotham and Foundry as the “ability to construct a model of the real world from countless data points.” Unlike a SQL database, natural language is used to query data and return results in real-time rather than through strings.

The truest, closest competitor for Palantir is Semantic AI, which supplies graph-based analytical platforms to the DoD and other government agencies. As stated, I think Palantir’s real competition is being developed as we speak as machines will answer questions from incomplete data sets once the AI/ML market is built out.

Some real-world uses for Palantir include Hershey’s using the software for global food distribution and to correlate weather patterns with snack consumption. Chase Bank and other financial firms have used Palantir’s data analysis to identify troubled properties and ensure employees are not committing fraud (the employee monitoring took a nosedive — more on this below). Pharmaceutical companies use Palantir to expedite the development of new drugs – this being a substantial use case this year and perhaps why Palantir’s revenue has accelerated.

Palantir’s Financials

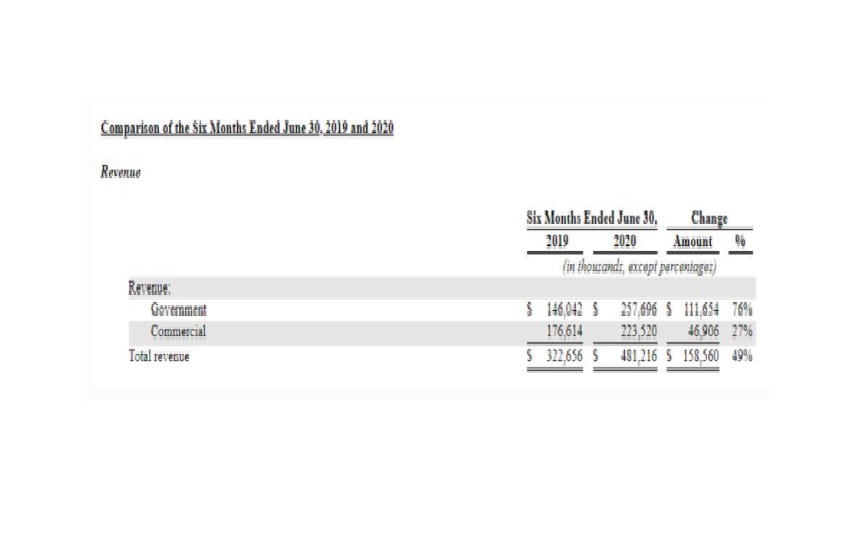

The company grew revenue 25% year-over-year to $742 million in 2019. This accelerated to 49% year-over-year to $481 million for the six months ending June 30th. According to a Reuters article in June, the company is expecting $1.5 billion in 2021, which looks easily achievable. The company’s annual run rate based on the current quarter is about $1 billion.

Link: https://www.sec.gov/Archives/edgar/data/1321655/000119312520230013/d904406ds1.htm

PALANTIR'S S-1 FILING

Net losses for 2019 of $579 million were flat year-over-year compared to net losses in 2018 of $580 million. On an adjusted basis, net losses in 2019 were $337 million. The losses are shrinking with H1 2020 reporting a loss of $164.7 million compared to $280.5 million in the year-ago period.

On an adjusted basis, the company was profitable in the first six months of this year at $17.2 million compared to a loss of $167.6 million in H1 2019. This improvement in operating results was driven by increasing revenue and reducing the number of engineers needed to install and deploy software programs.

Gross margins for H1 2020 are at 73% and the company spent only 42% of revenue on sales and marketing.

The company has cash of $1.5 billion and debt of $297.6 million as of June 30th.

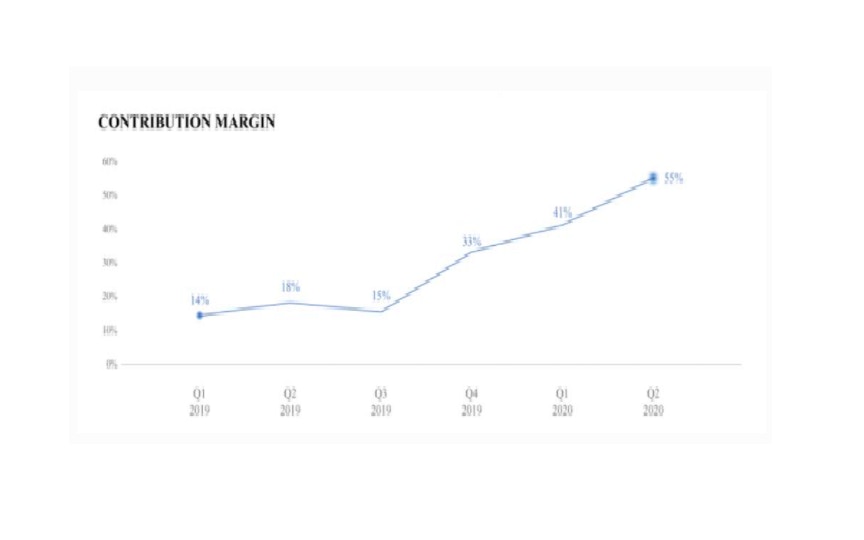

Contribution margin is a Non-GAAP key metric that represents the revenue the company generates relative to the costs incurred. It strips out variable costs related to deploying and operating the software and identifying new customers.

You can think of it as falling somewhere between gross margins and operating margins. For comparison purposes, Palantir’s gross margins are at 72.3%for the six-month ending June 30 and the company has negative operating margins of -48.5% and negative net margins of -78%.

Source: S1 Filing

The company states the addressable market is $119 billion across commercial and government sectors. The TAM in the government sector is $63 billion and the TAM in the commercial sector is $56 billion. Within the government TAM, domestic is $26 billion and international is $37 billion.

The commercial sector is the growth story. For example, Skywise is a solution that connects in-flight, engineering, and operations data to break down siloed systems around maintenance, flight management and aircraft monitoring and safety. Palantir is partnered with Airbus who offers this solution as “the leading data platform for the aviation industry.”

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

This example can extend to many industries, such as pharma for drug development data to better understand population dynamics and drug outcomes. This is for the pre-clinical and clinical stages, mapping treatment pathways, and automating reporting. Manufacturing can benefit from Palantir Foundry by managing inventory, saving on distribution costs and prevent delays while increasing sales.

There are also solutions for financial compliance, insurance, automotive and sales.

Valuation:

Palantir is doing a direct public offering (DPO), which means there will be no new shares offered and no underwriters. The goal of a direct listing is not to raise money rather to allow existing investors to sell their shares. However, unlike Spotify and Slack who did DPOs, Palantir will have a lock-up period. I find a lock-up period to be more favorable for retailers as Spotify took nearly two years to break out from its opening DPO price and Slack is taking more than a year to break out beyond its opening price.

The company’s founders, Peter Thiel, Alex Karp and Stephen Cohen, own 30.2% of the company’s stock. Peter Thiel owns additional stock through various investment management funds that own stock, such as Founders Fund. Thiel has 28.4% corporate voting power, Karp has 8.9% and Cohen 3.1%.

There will be three classes of stock: Class A, Class B and Class F common stock – which is unusual to have three tiers. Class A will allow for one vote, Class B will allow for 10 votes and Class F will share 49.99% of the voting power for Palantir. Class F is for the founders who will retain just under 50% of the voting rights at all times. This is reminiscent of Facebook where insiders control about 70% and Zuckerberg controls 58%.

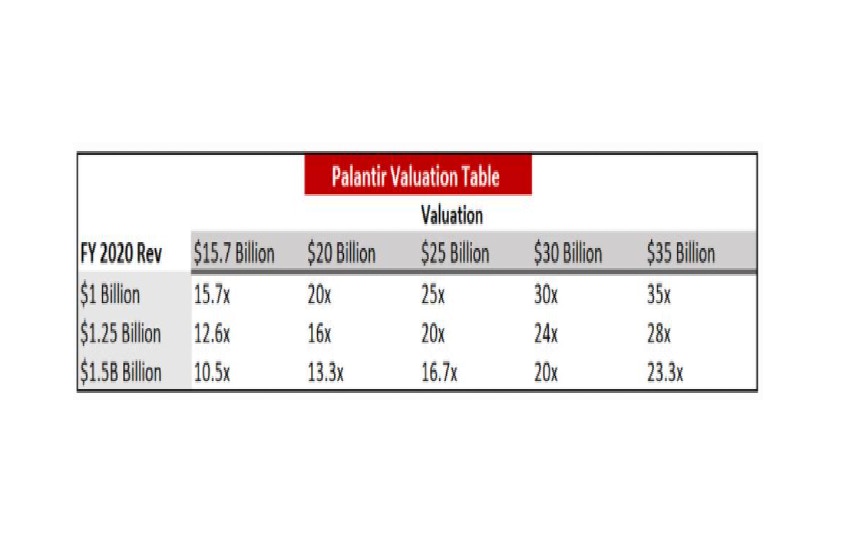

The reference price for Palantir’s direct listing is $7.25 per share, which would value the company at $15.7B. This is lower than the expected price range we saw throughout the month. Palantir was initially thought to open in a range of $10-$14, which would have given the company a $26B market cap at the midpoint. Palantir received a private valuation of $20.4B in 2015.

At the reference price, Palantir would trade somewhere between 10.5x-15.7x FY 2020 revenue depending on the estimate. At a reasonable $1.25B FY revenue estimate, Palantir would be valued at 12.6x 2020 sales. With a more generous estimate of $1.5B in 2020 revenue, Palantir would trade at 10.5x sales.

BETH.TECHNOLOGY

The reference price does not mean Palantir shares will open at this price on Wednesday. If Palantir follows the trend of recent tech IPOs, it will open trading well above its offering price. For comparison, Snowflake (SNOW) opened 105% above its offering price, JFrog (JFROG) 62%, Sumo Logic (SUMO) 21%, and Unity (U) 44%. A $25B valuation would be roughly 59% above Palantir’s reference price, a number that is in line with this trend.

Looking at the current IPO market, it’s very likely that Palantir will open above its reference price, but still well below the valuations we have seen in some recent IPOs. A few recent IPOs have traded at historically high valuations. Zoom Video, Agora, Datadog and Lemonade have all hit the 50 EV/Revenues level. More recently, Snowflake opened above 100x EV/Forward Revenue and JFrog above 40x. Early indications show that Palantir will open at a more reasonable valuation.

Below, I review the risks that may be contributing to this lower valuation.

Risks

Palantir’s biggest risk is customer concentration with the top 20 customers accounting for 67% of revenue and the dependence on government contracts at 54% of revenue. The Army’s attempt to develop a more expensive in-house solution illustrates there is a risk that government agencies eventually move away from Palantir in the future.

Reputation and social acceptance is also a risk. Tech companies often see employees engage in protests when a company contracts with the government on AI-driven war missions and privacy issues that potentially threaten human rights. Palantir’s biggest obstacle today is the work it does with ICE which pits the company’s internal employees against the CEO on social issues.

For instance, this week, Hootsuite stated the company would terminate its ICE contract due to disagreements within the company. The CEO tweeted: “We typically do not make public facing statements about specific customers or contracts. However, due to the attention around this particular case we can confirm that Hootsuite has decided not to do business with the U.S. Immigration and Customs Enforcement.”

In the past, Google ended a contract with the Pentagon when employees protested using AI for lethal purposes. Karp became controversial and challenged Google on this decision, saying it was a “loser” position.

This can backfire as Palantir may not be able to attract top talent as AI companies begin to compete from a small pool of AI developers and engineers who have proven to protest and walk-out of company projects they feel are unethical. Amazon, also, banned facial recognition for law enforcement for one year following the George Floyd protests. Therefore, Karp’s personality could be considered a risk as the tech world begins to explore and support ethical AI development.

Despite government-backing, Palantir’s products are certainly not bulletproof. The company attempted to launch a platform called Metropolis to help hedge funds with trading and to spot patterns in the markets, among other things. Metropolis, formerly known as Palantir Financial, did not succeed as hedge funds already possessed AI tools that were cheaper and the project was shut down. According to a lengthy response by Joe Lonsdale, Co-Founder of Palantir, the issue was that funds would not pay as much for the platform as other customers and the company may have been charging too much to go to mass market.

Chase Bank used the platform to monitor its 250,000 employees for fraud by mining trading data, emails and phone calls, yet this backfired when it was found out the platform had been used as surveillance for top executives. The information gathered from surveilling the executives led to a press leak (taste of own medicine, perhaps?).

There are also rumors that the CIA has been cold towards the company since the CEO chose to be more in the public eye, especially around Osama bin Laden’s death. Palantir began linking to articles asserted their software was responsible for bin Laden.

Conclusion:

To conclude, Palantir must be sensitive enough to win over commercial clients and top talent yet must not lose government contracts from being too overt. This IPO carries a great deal of speculation as there is no reason the company should not have stronger revenue growth and profits from the guaranteed government contracts. As of now, Palantir does not have product-market fit as it’s specialized and hard to scale (proven by its financials). We’ve also seen some issues with scale due to the pricing of the product, as noted by the Metropolis platform.

If you choose to be an investor, you’ll also have to get comfortable with ethical controversy as Amnesty International has now slammed Palantir’s human rights record on the eve of the IPO. Like Uber, the company is clouded by serious ethical issues. Wall Street may not care but internal employees and customers of Palantir could very well care. On that note, keep an eye out for “ethical AI” competitors in future years.

Similar to Snowflake, the headlines and FOMO can pump this company for a while, but bi-annually —- or even more often, rotations happen in tech growth. I’ve found price-to-sales revert to the mean during these rotations.

Palantir’s most promising aspect, in my opinion, is the acceleration in revenue that perhaps came from coronavirus-related research. This is something to monitor in future quarters.

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su