I/O Fund’s Overview 6 Cloud Stocks for Q3 Earnings

November 05, 2021

Royston Roche

Equity Analyst

Cloud stocks continue to do well in the market as these companies are growing very fast. This quarter we chose Cloudflare, Datadog, Dropbox, Bill.com, Five9, and RingCentral with some already reporting today and some reporting soon.

To understand valuations across cloud stocks and how the sector is positioned, please refer to our analysis “I/O Fund’s Cloud Q3 2021 Earnings Overview”

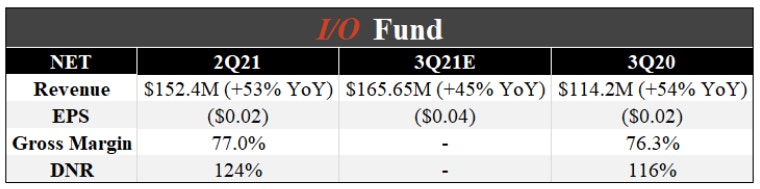

Cloudflare Inc – Earnings on November 04

Cloudflare’s Q3 sales grew 51% YoY to $172 million, which beat the consensus estimate of $166 million by 4%. The company also expects Q4 sales to grow 47% YoY to $185 million, which is 5% higher than the Street’s initial forecast of $176 million.

Source: Earnings report and YCharts

Cloudflare’s revenue grew from $85M in 2016 to $431M in the year 2020, a compounded annual growth rate of 50% during the period. In the second quarter revenue grew 53% YoY to $152M, it was primarily helped by the strong growth in paying customers. At the end of the second quarter, it had 126,735 paying customers (+32% YoY) and it also witnessed a significant addition of large customers. This growth continued into Q3 as Cloudflare beat topline estimates by 4% after reporting strong YoY sales growth of 51% during the quarter.

Going into earning, Jefferies analyst Brent Thill had downgraded the company to a hold rating from a buy with a price target of $195. The analyst is concerned of the valuation after the strong share gains. However, he continues to view Cloudflare as the "most disruptive cyber vendor with strong fundamentals," he is of the view that “the company has the richest multiple in his coverage universe at 56 times enterprise value to consensus 2023 revenue estimates” and he "would look to get more constructive at a more reasonable valuation."

Needham analyst Alex Henderson has said that the company’s move into email security as a positive. He says “just one more example of why Cloudflare will become a major company.”

Please note, the I/O Fund is objectively reporting what the Street is saying. We covered Cloudflare previously here: Pinterest and Snap Show V-Shaped Recovery; Cloudflare Guns for Zero-Trust

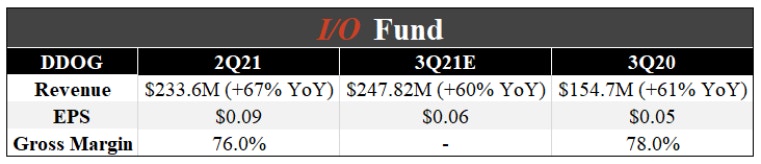

Datadog Inc reports on November 04th

Datadog reported that Q3 sales grew 75% YoY to $270 million, which bested the consensus estimate of $248 million by 9%. The company expects Q4 sales to grow 64% YoY to $291 million, which is 10% higher than initial expectations.

Source: Earnings report and YCharts

In the prior quarter of Q2, Datadog reported strong second quarter results. It beat the analyst’s revenue estimates by $21M and the adjusted earnings by $0.06. The company had also raised the full-year revenue guidance to $938M-$944M, up from the previous guidance of $880M-$890M. Datadog continued this momentum and reported a 9% top line beat during Q3 and guided Q4 sales 10% higher than initially expected.

It also witnessed strong growth of large customers (annual recurring revenue of over $100,000) as they grew to 1,610 from 1,015 from the same period last year in Q2. This quarter, large customers grew to 1,800, up 66% from 1,082 in the prior year quarter.

RBC Capital analyst Matthew Hedberg has raised the company’s price target to $176 from $154 and has kept the Sector Perform rating on the shares. The analyst expects the company to report "strong" Q3 results with upside, building off last quarter's acceleration. The analyst adds that he expects Datadog to continue to benefit from continued traction in multi-module sales, strong new customer adds, and favorable cloud adoption trends.

Our previous analysis on the company:

Podcast with Motley Fool: Big Tech Plus the 1 Stock I’d Buy Right Now

Tech Growth Earnings Review for Q3 2020 - Part 2

Video: Our Stock Picking Strategy

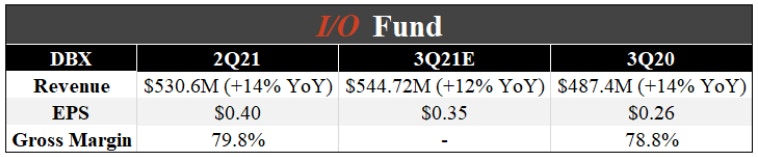

Dropbox Inc reports on November 04th

Dropbox reported Q3 sales of $550 million, which grew 13% YoY and came in 1% higher than the consensus estimate of $545 million. The company’s outlook for Q4 forecasted sales to grow 12% YoY to $563 million, 2% higher than the Street’s initial estimate of $553 million.

Source: Earnings report and YCharts

The company’s revenue growth is not very strong when compared to other cloud stocks. However, the company has got good free cash flow and it’s profitable. In the last quarter, the management has raised the full-year revenue guidance to $2.136B-$2.142B from $2.118B-$2.130B. It aims to generate annual free cash flow of $1B by the year 2024. The management revenue guidance for the third quarter is $543M-$546M, which represents a growth of 12% YoY at the mid-point.

Sign up for I/O Fund's free newsletter with gains of up to 1100% - Click here

Jefferies analyst Brent Thill has a price target of $40 and a buy rating on the stock. He believes that the company’s increased full year guidance is still conservative.

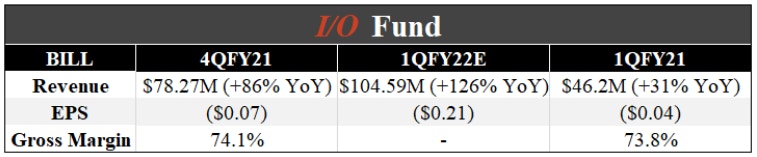

Bill.com Holdings Inc reports on November 04th

Bill’s Q1 FY22 sales were $116 million, which beat the consensus estimate by 11% and represented a 166% YoY growth rate (organic growth was 78% YoY). Bill.com guided for Q2 sales to grow 141% YoY to $131 million, which was 12% higher than initial estimates.

Source: Earnings report and YCharts

The consensus analyst’s revenue estimates are strong for the next quarter. However, we cannot compare to the previous periods as the results will include Divvy. It completed the acquisition of the spend management solutions provider Divvy, on June 01, 2021, and the 4Q results included Divvy results. The stock has been one of the best performers in the sector. However, it would be interesting to watch how the company faces competition from other players and justifies its valuation. Bill.com reported Q1 FY2022 sales that beat top line estimates by 11% and guided next quarter sales well above consensus estimates.

Jefferies analyst Samad Samana had a buy rating going into earnings and a price target of $350. The analyst anticipates organic core revenue growth to "decelerate modestly" against a tougher comp, but his 60% growth outlook is still "very healthy". Bill.com should be a "core" long-term growth holding, with the stock offering "solid upside" based on his potentially "conservative" assumptions.

Deutsche Bank analyst Bryan Keane initiated coverage of Bill.com with a Buy rating and $360 price target. He believes that “BILL is uniquely positioned in the market due to its end-to-end offering, including accounts payables (AP) and accounts receivables (AR) automation as well as electronic payment offerings like virtual cards, instant transfers and cross-border FX. He further states “We see potential for ~70% Y/Y core organic growth in 1Q22 and ~57% Y/Y for FY22 compared to guidance of ~60% Y/Y and ~45% Y/Y driven by new customers, higher engagement, and increasing take rates from mix shift with reported growth reaching as high as +124% Y/Y in FY22 including Divvy and Invoice2go.”

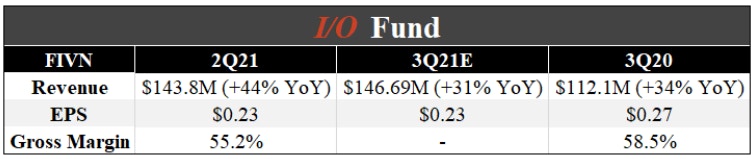

Five9 Inc reports on November 08th

Source: Earnings report and YCharts

The consensus analyst’s revenue growth is slower than the second quarter and also from the previous year. The company did not have an earnings call in the last quarter due to the pending merger transaction and the next call would have more details about growth prospects as a standalone company.

Analysts have been positive after the Zoom-Five9 deal failed to materialize. Barclays upgraded FIVN to Overweight, saying the deal's breakdown refocuses the investment case back on fundamentals. And “We don’t think lack of a deal hurts Five9’s positioning with enterprise customers."

Evercore has an overweight rating on the stock and in the words of analyst Peter Levine, "firing on all cylinders, the pending acquisition was not a distraction, partner contributions remain strong, and the numbers released in the proxy are a fair representation of the current trends in the business."

Sign up for I/O Fund's free newsletter with gains of up to 1100% - Click here

Jefferies analyst has a $180 price target and a hold rating. His checks throughout Q3 suggested demand remains solid across both UCaaS and CCaaS, he thinks Five9 "has a tough setup" given that management not providing guidance last quarter has resulted in "a wider than normal estimate dispersion." Management's 10-year financial plan in their merger proxy raised buyside expectations, but he does not expect the company to guide to the proxy levels, which may disappoint some investors.

We have covered Five9 stock in our premium site in the past.

Please find our semiconductor earnings preview here.

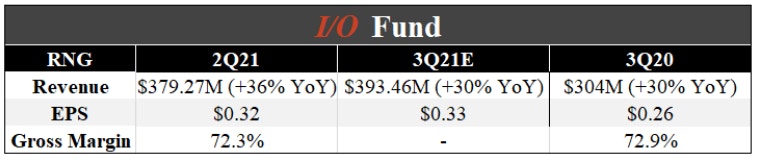

RingCentral Inc reports on November 09th

Source: Earnings report and YCharts

RingCentral has been showing steady growth. The management had raised the full-year revenue guidance to $1.539B to $1.545B, which represents a growth of 30% to 31%, which is up from the prior guidance of $1.5B to $1.51B. The third quarter revenue guidance is in the range of $390.5M to $393.5M.

Source: Earnings Slides

Jefferies analyst Samad Samana has a buy rating on the stock with a price target of $360. His checks throughout Q3 suggested demand remains solid across both UCaaS and CCaaS, which he thinks should translate into solid Q3 results.

Barclays analyst Ryan MacWilliams initiated coverage of RingCentral (RNG) with an Overweight rating and $350 price target. “RingCentral shares are attractive and RingCentral Office remains the most applicable as well as marketable solution for mid-market enterprise customers, even though Zoom Phone (ZM) and Microsoft (MSFT) Teams adoption has unfairly changed investor perception of the stock, leading to a disconnect in valuation to the company's recent quarterly performance.”

The I/O Fund is a team of analysts that share their research publicly as they build a portfolio of 30 stocks. Our team has record results for a retail Fund and we also have four-digit gains on some of our free newsletter coverage. You can learn more about our premium service by clicking here or sign up for our free newsletter here.

Disclaimer: This is not financial advice. Please consult with your financial advisor in regards to any stocks you buy.

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per