Uber IPO: Record-Breaking For All the Wrong Reasons

May 09, 2019

Beth Kindig

Lead Tech Analyst

By now, investors know that Lyft’s ride-sharing IPO didn’t reach $100 per share like many of the media talking heads stated it would, and this will likely weigh on Uber’s IPO. Two weeks prior to Lyft’s IPO, I had warned that the risk listed in the prospectus, which warned Lyft may not become profitable, was more than fine print. Ride-sharing companies use investment money to lower the cost of the ride to create demand, which means the ride you take in a Lyft or Uber is not profitable, and will likely never be profitable.

Not one analyst rated Lyft as a sell going into earnings despite earnings estimates that called for accelerating net losses from negative $3.16 EPS to negative $3.97 EPS. Going into earnings this week, twelve analysts had rated Lyft as a buy compared to eight who rated it as a hold (What is wrong with these analysts?!).

With the most recent earnings, we have confirmation that my analysis, which detailed why Lyft can increase revenue yet cannot stop the losses, was accurate with expectations of an estimated $1.1 billion in losses this year.

Reuters published in 2015 that Uber passengers pay only 41 percent of the actual cost of their trips. At the time, Reuters warned that this creates an “artificial signal about the size of the market” when Uber released limited financial data that showed losses of $708 million per quarter. Four years later, little has changed.

How Uber’s IPO Compares to other IPOs:

Uber is an IPO that has been covered extensively. You may have heard comparisons of Uber’s IPO to Facebook or Alibaba. Uber is raising $9 billion in this week’s IPO, Facebook raised $16 billion in 2012 and Alibaba raised $25 billion in 2014. Facebook and Alibaba are both doing great, seems to be the logic OR many tech companies are not profitable at the time of IPO is another costly mistake when comparing Uber to other IPOs.

Of course, these “big tech” comparisons don’t tell the whole story. Facebook had $1.75 billion in operating income, and $1 billion in net income in the year prior to the 2012 IPO. Alibaba had $1.7 billion in operating income, $1.3 billion in net income, and $2.6 billion in adjusted EBITDA in 2013, the year prior to its IPO. To compare, Uber has a $3 billion operating loss, and negative $1.8 billion adjusted EBITDA.

Notably, for anyone glancing over the prospectus, Uber sold some operations in Russia and Asia, which provided one-time income, and caused the company to post $1 billion in net income. This is why net income should be ignored as it does not reflect the operating income or adjusted EBITDA. To summarize, Uber’s prospectus points towards “an accumulated deficit of $7.8 billion” in the years ending December 31, 2017 and 2018. The year prior (2017), Uber posted $4 billion in operating loss and negative $2.6 billion in adjusted EBITDA.

Chicken and the Egg – Both Broken:

Most investors know there have been numerous lawsuits against Uber with many examples listed on page 28 of the prospectus. Here is a sample of what it says:

“We are involved in numerous legal proceedings globally, including putative class and collective class action lawsuits, demands for arbitration, charges and claims before administrative agencies, and investigations or audits by labor, social security, and tax authorities that claim that Drivers should be treated as our employees (or as workers or quasi-employees where those statuses exist), rather than as independent contractors.”

This paragraph is followed by a list of class action lawsuits and state-level Supreme Court rulings that Uber has been involved with and the various legislation or judicial decisions that could have an adverse effect on the business and financial condition of the company.

Although being sued often comes with the territory for disruptive startups, this is unique as the work force is going on strike during the IPO (this is not a competitor suing over intellectual property, etc). The drivers and customers are a chicken-and-egg scenario and Uber struggles to pacify both to successfully operate. On one hand, Uber is subsidizing rides at up to 60% to lure the customers, and on the other hand, the workers are retaliating. This is not a good formula. Most importantly, Uber has no profit to absorb a change in business model, such as being required to pay minimum wages or health care.

Here are some charts:

If you need some charts, to prove what I’m saying, there is an overabundance of charts that show the issues Uber has with subsidizing rides “to create artificial signals about the market” (Reuters words, not mine).

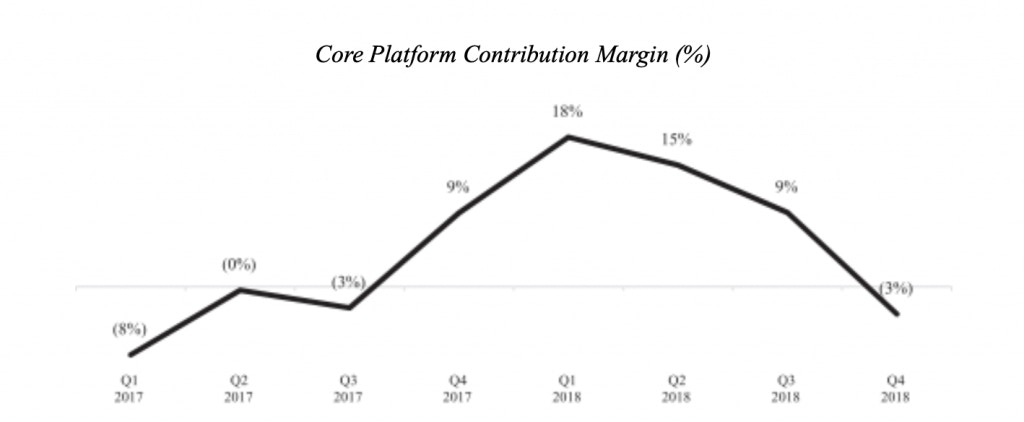

Core platform is the margin Uber generates after direct expenses. As the prospectus states, “Core Platform Contribution Margin is a useful indicator of the economics of our Core Platform, as it does not include unallocated research and development and general and administrative expenses.” Here is what the margins look like:

The reasons Uber states the Core Platform Contribution Margin goes through periods of decline is due to competition in ridesharing (translation: Uber has to subsidize rides to remain competitive) and they also state it’s due to planned investments in Uber Eats. The problem is that Uber Eats only contributed $165 million in adjusted net revenue last quarter compared to ride sharing at $2.3 billion in adjusted net revenue, and therefore, the majority of the decline is likely due to the issues I stated above (rides are priced too low for profits but price of rides must remain low for demand).

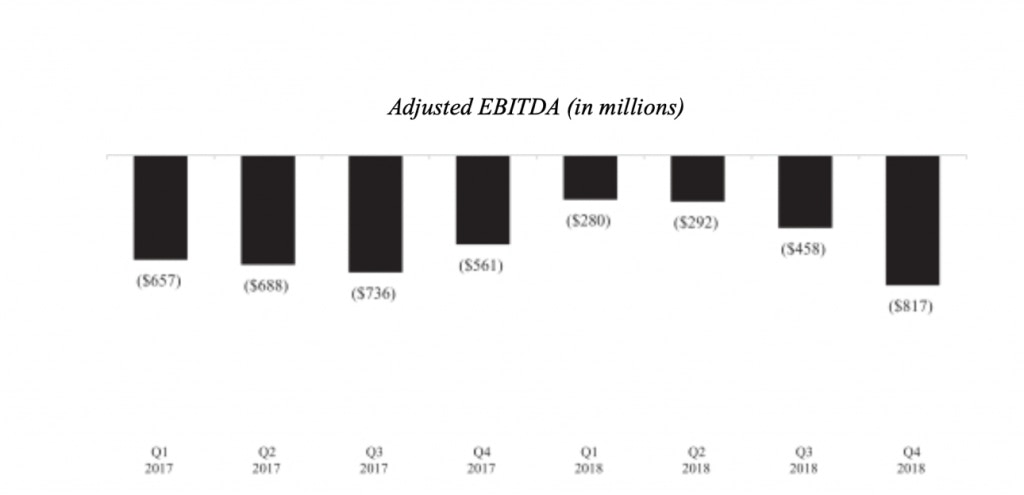

Here’s another chart that shows you what it looks like when a company subsidizes purchases with the capital it has raised.

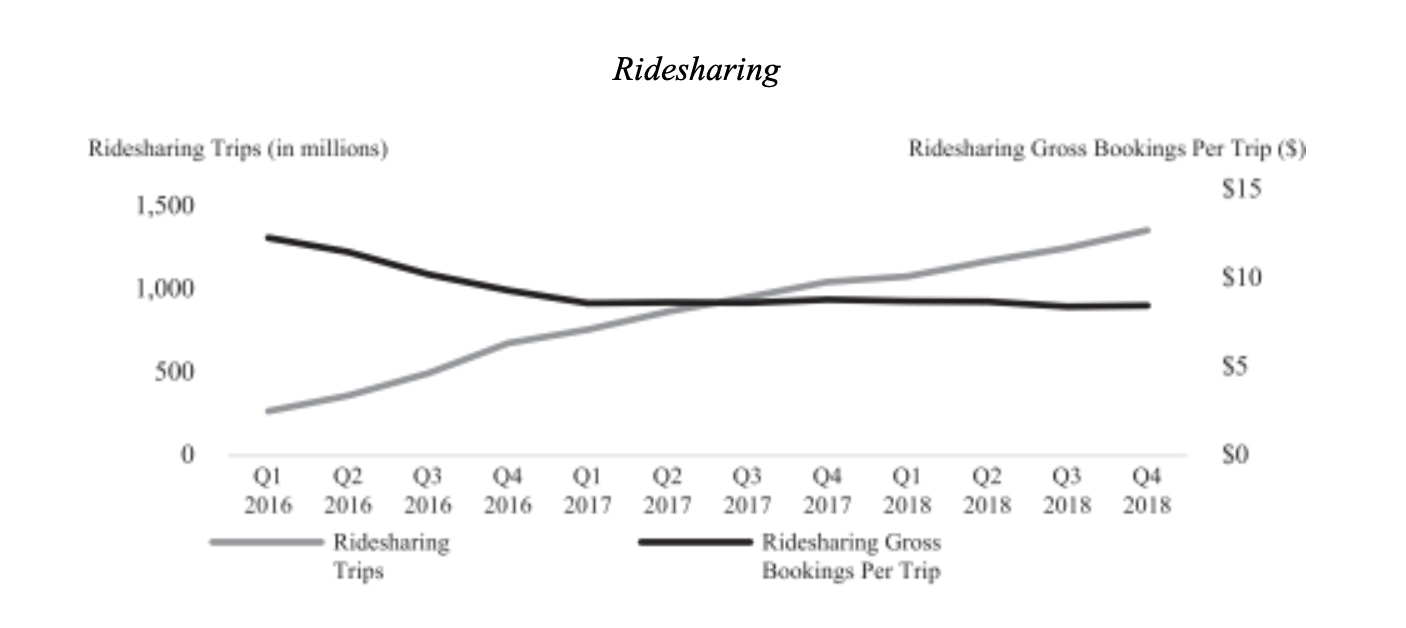

And here’s another one – perhaps the most critical as it shows the relationship between sales and profits:

As sales go up, gross bookings per trip goes down. This is a good indication that the business model requires the price of the ride to remain below fair value in order to drive demand. Although some reporters and analysts like to talk about Uber Eats, the issue is that Uber is valued at $90 billion+ and Uber Eats is a very small percentage of revenue. You can’t conclude that Uber Eats is a good investment opportunity as it makes up about 5% of Uber’s revenue and this won’t absorb the ride-sharing losses.

Notably, the chart which shows the unprofitable relationship between ridesharing trips and ridesharing gross bookings per trip is on page 106 of the Prospectus. On page one, we are presented with a sky-rocketing hockey stick chart based off the number of rides Uber has booked from 1 billion in March 2016 to 10 billion rides today. This 10x chart doesn’t tell the whole story like the charts above.

AVs – Long Ways Off:

This is where the story gets even more risky as the solution to the upset drivers is that these drivers will not be needed soon due to autonomous driving. Any company who is publicizing autonomous driving right now as a near-term way of driving profits is a good company to run from – and quickly.

We saw Lyft use this tactic to distract from their disappointing earnings this week with PR timed to the earnings report that “Waymo and Lyft partner to scale self-driving robotaxi service in Phoenix.” On closer look, Waymo will only add 10 vehicles to the Lyft app in their Arizona testing sites in Phoenix.

That aside, let’s go into the time machine for a minute to revisit stock prices relative to important product releases. Apple was priced at $11 in 2009, two years after the iPhone came out, and was priced at $35 in 2010, when the economy was doing a little better. Facebook was priced in the $25 range for years after they pivoted to a native mobile app and launched Messenger, both of which greatly contributed to the data collection and ad targeting that drives ad revenue today. Amazon was priced under $100 for nearly three years after the company launched AWS.

Point being, not only are autonomous vehicles a long way off from being commercially deployed to the public and able to generate profits, (and there is a ton of competition), but to invest in tech before it hits the market is high-stakes speculation. There is not one example where it made sense to invest in the company years before a tech product was released. Meanwhile, there are many examples where the stock price and valuations were low even after profitable products had gained traction. I’m not saying you want to be late to the market for AVs, rather I’m saying it can be just as costly to be this early – especially with companies that have ten digit losses.

Note: If you’ve read any of my previous analysis, you’ll know that I’ve been writing about the realities for autonomous vehicles for awhile now and how this does not match investors’ expectations. I won’t repeat my AV bubble thesis here but you can read quite a bit of this under my profile.

Don’t Get Duped on Uber IPO:

Sometimes investors get it wrong. We see this on the public markets frequently when a legendary investor goes all-in at the wrong time or a darling stock has a sudden drop. Well, guess what? Private investors get it wrong too sometimes. And the venture capitalists who invested in Uber and Lyft really got it wrong with ride-sharing. Their eyes lit up with the promise of a serviceable available market (SAM) and total addressable market (TAM) that would replace personal car ownership around the world. User growth is phenomenal and the brand is ubiquitous. VCs kept fueling more and more capital into the leaky ride-sharing business model and something prevented these VCs from using discipline to require proof of the following:

Question: will charging below a fair market price and subsidizing rides at up to 60% create a profit margin? Answer: No

Question: if we charge a fair market price to stop the losses, will there be enough demand? Answer: No.

The ride-sharing business model as we know it today will never be profitable. Meanwhile, the venture capitalists who bought into the world’s most valuable startup want their money back. Do you want to donate to the “pay VCs their $90-$120 billion” charity cause? If so, shares will be available Friday.

More To Explore

Newsletter

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i

Google TPU v8 vs Nvidia: How Inference Is Rewriting the AI Market

In April, Google announced it would begin selling its TPUs to select third-party data center operators, which is something the market has anticipated for nearly a decade. The TPU-versus-Nvidia-GPU deb