Is Spotify a Bandwagon Stock? 8 Key Issues Famous Hedge Funds Are Ignoring

September 27, 2018

Beth Kindig

Lead Tech Analyst

Bandwagons are easy to jump on but it can be hard to decide when it’s time to get off, especially considering Spotify stock has famous hedge funds like Soros Fund Management, Philippe Laffont of Coatue Management, and Louis Bacon’s Capital Management holding sizeable stakes. Since its IPO in April, Spotify has seen an $8 billion rally in market value for an all-time high market cap of $34 billion following Q2 earnings.

The bull storyline is that Spotify is the leader in streaming music with nearly 40% of market share in 2017 – which is double what Apple Music holds and 4x the number of Amazon music subscribers (source: Statista). There is a strong case for future earnings as 83 million monthly subscribers pay for Spotify’s premium service price at $9.99 per month to $14.99 for the premium plan.

Despite a healthy user base, I believe Spotify is reaching its peak due to hefty royalty payments, a miss in the razor-razor blade model, Apple’s recent acquisition of Shazam, and due to being a small fish in technological advancements such as AI and song services. The stock may have one or two good quarters left but investors should have a disciplined trailing stop. I expect that within 12-18 months Spotify stock will be in sell status with the potential to plummet in price on any single day in 2019 due to the following key issues:

8 Reasons Spotify Stock Will Be a Sell Recommendation by 2019:

Numbers Don’t Lie:

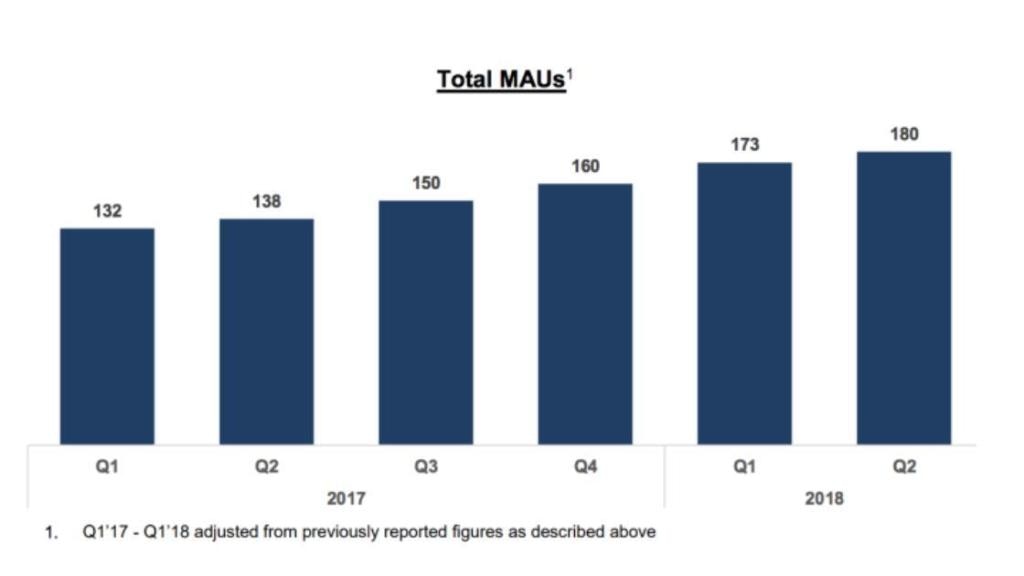

1. Numbers don’t lie – as long as you know what to look for. When a company is a leader in a technology vertical such as music streaming, you can easily substantiate the company based on past performance. Yes, Spotify has 180 million users and reported 40 percent year-over-year growth in paid subscribers for $1.49 billion in revenue. However, Spotify missed big on EPS with a loss of -2.20 euro compared to estimates of -0.68 euro in Q2 due to the high cost of royalty payments to record labels and artists.

Investors should also watch user growth closely with Spotify as the company added fewer users this quarter compared to last quarter (13 million in Q1 compared to 7 million in Q2 or 5.9% QoQ). The estimates for Q3 call for 8 million users and meanwhile, the average revenue per user (ARPU) has dropped by 12%, which is likely due to bundled offers with Hulu and family plans. The concern here is that user growth is hovering at 5-6% while ARPU is decreasing by 12%, thereby depleting the gains from user growth – meanwhile, competition continues to stiffen. In my opinion Spotify must reach at least 10% QoQ growth with ARPU increasing before I would invest in this application.

Apple Has Homefield Advantage:

2. Last month, Apple was cleared to complete the acquisition for UK-based music recognition app Shazam Entertainment for $400 million. The threat to Spotify and other competitors was enough for regulators in seven countries to contest the acquisition when first announced in December of 2017 but approval was granted to this potentially unstoppable push into enriched data and augmented reality features. To date, Shazam has had well over 1 billion downloads (last reported in 2016) and owns a wealth of information on what music is trending with over 20 million searches per day.

One thing about Apple, is that this company will not be beat on its home turf. Apple revolutionized digital music with the iPod and iTunes. With smartphone penetration, the Beats acquisition, its Homepod ecosystem and a huge push into connected car infotainment, Apple can surround Spotify in nearly every direction. Keep in mind, that 66% of the world’s paying app users are iPhone users who trend towards higher incomes (vs. only 34% on Android), so Apple users are supremely important for Spotify’s $9.99 subscriptions.

In fact, the turf war has already receded Spotify’s market share. Record industry sources state Apple is adding paying subscribers at a rate of 5 percent in the U.S. versus 2 percent for Spotify, and that Apple Music may have already taken over Spotify as the number one streaming service in the United States. Apple Music was launched only 2 years ago and has 40 million paying customers compared to Spotify’s 83 million paying customers which took 12 years to build.

My newsletter subscribers get this information first. Sign up here.

Razor-Razor Blade Model:

3. I like the Gillette analogy for tech companies and it’s one of the points I make as to why I’ve been long on Roku since its IPO. As the original set top box manufacturer, Roku players are the cheap razors that will deliver the razor blades of ad-supported content in the OTT market. (You can read more my analysis here on Roku). However, this is the same model that will ruin Spotify in the long run. At home assistants such as Alexa are designed and leveraged specifically for AI activated music services. Major record labels let Amazon offer a reduced Alexa version of the premium service at $3.99 per month and Apple is requiring users to sign in to Apple Music to power the HomePod – which completely shuts out devout Spotify. Car infotainment centers will be the next piece of real estate where Spotify is simply a guest (that will become increasingly unwelcome).

Lack of Technological Advancement:

4. Spotify states they have spent “years developing an intelligent music streaming platform that leverages proprietary artificial intelligence (AI) and machine learning (ML) tools” that tap into “datasets of over 200 petabytes.” It seems every app and platform in tech these days says they leverage AI and ML. Yet for Spotify, the evidence isn’t there in the functionality of the app. (For what it’s worth, I’m a Spotify Premium subscriber but this doesn’t mean I’ll buy their stock). Spotify is falling behind in voice-based computing with features such as asking for songs through verbal commands and voice-activated queries due to a lack of lyric recognition. The future for AI and ML, especially as it relates to music streaming, will be a world where you do not have to look at your phone to prompt the next playlist. As of last month (August 2018), even Pandora had search by lyrics with Google Assistant.

The second point here is the amount of data. Yes, Spotify has a lot of music specific data but, again, this is irrelevant when competing with Google, Amazon or Apple.

What About Spotify & Tencent?

5. As the earnings report states, “Spotify owns Tencent Music Entertainment (TME) shares and “a TME IPO would trigger a fair market value adjustment to the carrying value of our investment recognized in other comprehensive income. The gain could be significant.” This one-time, non-recurring event would generate a Net income for Spotify with a Net loss returning in the following quarters. Spotify stock holders should be aware that this one time wave may be worthwhile to hold on for, but that the long-term prospects of the company are still not proven.

6. Some speculators have suggested Spotify is a great acquisition target – which is correct. Google attempted to buy Spotify in 2014 and Tencent also tried to buy Spotify prior to the IPO sometime in 2017. Spotify was priced too high then and is most certainly priced too high now. It will have to demonstrate that it has staying power as a public company, which I believe is where Spotify will falter. Meanwhile, Spotify founders and investors can sell their shares any time as Spotify did not have a traditional lock-up period and this was cited as one of the risks to holding Spotify stock.

A Few More Points:

7. The music industry is not loyal to Spotify. Any catalog Spotify has is likely to be duplicated across all music streaming services, offering little differentiation across competitors for content. (Compare this to OTT streaming like Netflix which is highly differentiated through original content). If anything, artists dislike Spotify very much and are often bringing class action lawsuits against the company. And even though Spotify has paid over $10 billion since 2016 to artists, it’s still not a fair wage according to the musicians who see about $5,000 for every 1 million streams. In this case, Spotify is not pleasing the geese who lay the golden eggs, and this is a huge risk in their business model.

8. Pandora is a cautionary tale as it had a steady first year after its IPO until it dropped 40% in one day in October of 2015. The company reported a quarterly revenue increase of 30% year over year, which was within guidance, and advertising revenue had also grown 31% year over year. But there was a $90 million settlement related to royalties and Pandora’s active listeners only rose 2.1% year over year and declined quarter over quarter. I believe Spotify will share a similar fate in the near future.

Featured image by Gavin Whitner

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

More To Explore

Newsletter

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de