Alphabet Stock: Keep a Close Eye on Third-Party Ads

April 09, 2019

Beth Kindig

Lead Tech Analyst

Data privacy will be affecting stocks into the near future and will likely catch Wall Street off guard as the minutiae is hard to sift through. Alphabet’s data machine has the longest tentacles of any company on the public market today, yet Facebook continues to carry the headlines. There are specific reasons that Alphabet has done a much better job at handling data, which in turn, creates a safer stock for investors. Even if some of the Google’s data collection policies are at odds with privacy advocates, Alphabet is being more transparent through SEC filings and offers a disclosure around revenue sources.

Last week, there was an important insider leak reported in Adweek that Google is “contemplating a number of changes to its consumer -and advertiser-facing tools.” Criteo’s stock dropped 30% when the news broke and TradeDesk saw a 15% drop while Alphabet’s stock showed the least impact at 5%. I believe this market reaction, which penalized Alphabet the least, is due to a misunderstanding around the implications of third-party revenue for Alphabet.

This analysis will break down why the intel leaked to the ad industry late last month is important for stock investors to pay attention to.

Overview:

The official list of companies who are in a grey area with how they collect and use data is Google, Facebook, Amazon, Twitter and Snap. You can add Spotify to that list too, although their data is minor compared to the bigger players. The reason these companies are at risk is because there is a conflict of interest in collecting first-party data with people you have a direct business relationship with and brokering this to third-party companies.

Let’s reframe this so it’s easier to picture. For instance, what if your credit card company brokered your data to run ads? They have more information on you than Facebook or Google because Mastercard and Visa knows your every purchase. They would make A LOT of money if they anonymized your data, assigned you an ID number, and let advertisers target you based on what you bought with your credit card. In fact, purchase history is the most valuable data to an advertiser and they would pay much higher amounts for this than social media data or search data. Mastercard and Visa don’t do this because it’s against regulations. This is what the online and mobile industries face who are brokering first-party data to third-party companies to target people and run ads.

Going back to Google. Of the companies listed above, Google is being the most proactive and has the least amount to lose (Amazon is a close second with the least amount to lose). This is because Google makes money from search engine inquiries, with advertisements based on your search criteria, and not targeted to who you are as a person. However, there’s a chance that Google could lose up to $5 billion per quarter if the insider information to AdWeek is accurate. One reason is because if Google prevents ad networks from running ads in the Chrome browser, they will risk anti-trust if they continue to do so themselves. There is also a conflict of interest for first-party data companies to run third-party ads through a demand-side ad platform, where advertisers go online to place ads using proprietary data.

Especially if Google wants to be a leader in artificial intelligence, which will require a privacy adherent company policy, it is my prediction that Google will part with the third-party ad revenue to win big on AI in the coming years.

Intel from the Ad Industry:

Here’s an excerpt from the Adweek article Google Mulls Third-Party Ad-Targeting Restrictions: “According to sources, certain Google teams want to placate the growing zeitgeist around the protection of consumers’ data privacy, which has grown ever louder since the Cambridge Analytica scandal last year. These internal discussions also follow the implementation of third-party tracking restrictions on Apple’s web browser, Safari, and similar moves from Mozilla’s Firefox and Brave’s offering in recent months. Although the various businesses within Google advocate similar measures, the breadth of the company’s interests (i.e., the dominance of its Chrome browser and ad-tech stack) make its decision-making process more complex.”

What you need to know:

There are two issues here. As the article points out, Google will likely cut off third-party ad companies from brokering through the browser on Chrome similar to Safari and Firefox. The issue is that if Google continues to broker ads with first-party data while cutting off competition, there will be antitrust repercussions. Plus, this doesn’t address the grey area as to why Google is using first-party data to broker ads in the first place, as this is against regulations in the EU already and highly contested in the US (with Facebook taking a lot of the blame). This brokering of first-party data is what “ad-tech stack” refers to.

The leak was enough for Criteo to be downgraded from $32 to $24 by financial analysts and TradeDesk dropped from $213 to $185 the day the news broke. Alphabet stock remained relatively stable although I believe this was the market not fully understanding Alphabet’s tech stack.

Disclosure of Third-Party Revenue

In the introduction, I stated that “there are specific reasons that Alphabet has done a much better job at handling data, which in turn, creates a safer stock for investors.” The primary reason Alphabet makes a safer investment is that you can evaluate the stock for risk because the company discloses third-party revenue it makes from this grey area in their SEC filings. Facebook, and the others, do not disclose this as a separate line item, which makes it impossible to quantify the risks.

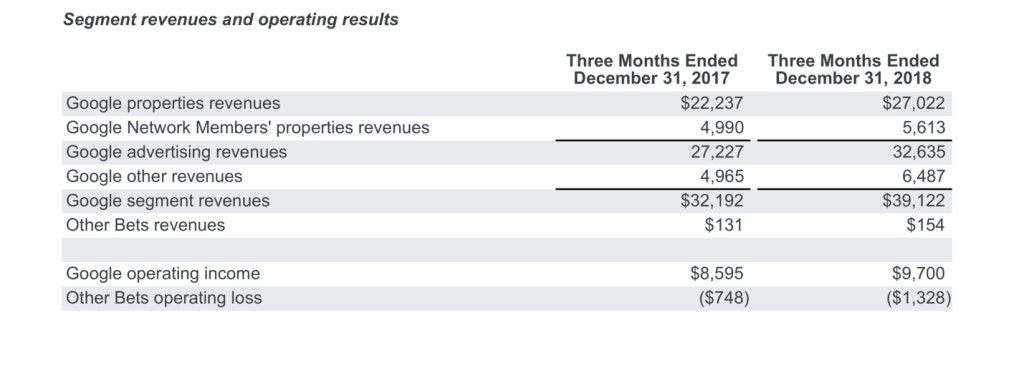

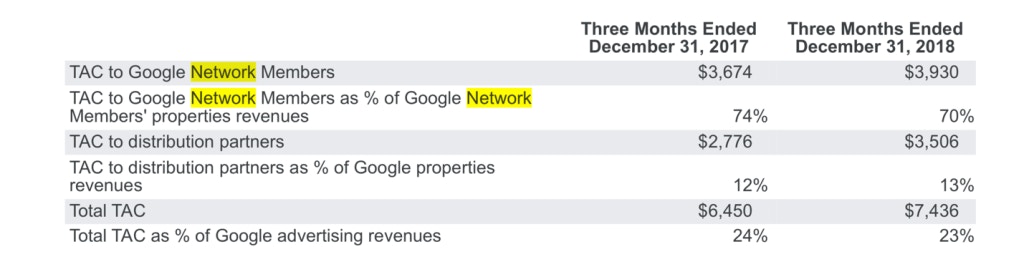

The line item that the leak refers to is “Google Network Members’ properties revenues,” which is $5.6 billion in revenue, or about 15% of quarterly revenue. The actual net income is much lower as Google pays out 70% to publishers, which is the Total Acquisition Cost, or “TAC to Google Network Members.” This leave the income for third-party sites at $1.7 billion per quarter.

Conclusions

On the Q1 2018 earnings call, analysts asked Sundar Pichai if the GDPR would affect the company. He stressed the importance of search engine revenue which is GDPR compliant, as it does not target people, rather it uses search inquiries. Although Waymo operates cars in the streets, and there have been many other speculative releases such as Google Glass, it’s important to remember that Alphabet’s revenue is 86% advertising.

Google Network Members’ revenue is at risk right now due to privacy regulations in the EU and ongoing scrutiny by regulators in the United States. It is my prediction changes will occur to Google’s third-party member sites revenue, and that the market misunderstood the impact it could have on Alphabet. Although there is no way to time exactly when this will occur, Adweek’s sources said they believe it will roll out by 4th quarter of this year.

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i