This AI Stock is Set to Surge from Inference Demand

June 13, 2025

I/O Fund

Team

Broadcom stock joined Nvidia, Alphabet and Microsoft in calling out surging AI inference demand, noting that this rapid growth could drive increased demand for custom silicon in the second half of 2026, and with it, higher AI revenue.

Despite an in-line print and guide, Broadcom’s AI revenue is tracking above Street estimates for next year towards the $30 billion mark, up nearly 150% in two years, with growing tailwinds from inference and networking as clusters increase in size. AI revenue growth is also tracking Broadcom’s addressable market forecast of a 60% CAGR.

Broadcom is cementing itself as the clear second in AI with key ingredients for success as inference demand rises. However, its premium valuation to Nvidia looks to be pricing in above-expected AI revenue growth into 2027, likely closer to a 70%+ CAGR, as there exists a $160 billion gap in AI-driven revenue between the two.

Inference Driving Possible Acceleration into 2H 26

The AI ecosystem’s pivot from training to inference, now emerging as a strong revenue engine for hyperscalers, is a structural tailwind for Broadcom's custom silicon and networking products.

We’ve seen quite a handful of signs over the last couple of months that inference demand (and revenues) are beginning to explode:

- Microsoft reported 5x YoY growth in tokens processed to 100T in Q1, with AI contributing 16 points or nearly half of Azure’s 33% growth last quarter. Microsoft’s AI run rate at the end of January was $13 billion, up more than 175% YoY.

- Alphabet reported 9x YoY growth to 480T tokens processed in April.

- OpenAI this week announced that it had crossed $10 billion in ARR, nearly doubling from $5.5 billion at the end of 2024.

- Anthropic’s ARR rose 200% in five months and 50% in 2 months to $3 billion.

With hundreds of millions of users interacting frequently with AI assistants, inference becomes the focal point for providers such as OpenAI and Google. Meeting these levels of growing demand, without significant response delays or downtime, requires more and more accelerators, networking and interconnect products.

Broadcom’s edge goes beyond the fact that custom accelerators are often multiples cheaper than Nvidia’s GPUs for inference tasks – it's that custom silicon is increasingly performant with each generation. By optimizing algorithms (software), Big Tech can drive higher performance from large language models (LLMs) -- which helps to drive down costs while also increasing output for specific workloads. For example, a rough idea as to how much it costs Nvidia to make merchant GPUs is estimated around $3,000 to $5,000 whereas the company charges $25,000 to $30,000 – hence the AI leader’s excellent margins. Reducing Nvidia’s high pricing power is what Big Tech is after and this can be accomplished both in the hardware costs but also through optimizing the workloads for specific use cases.

Big Tech is prominent in Broadcom’s custom silicon customer list, which includes Google and Meta. ByteDance reportedly emerged as the third customer last summer, though some reports surfaced earlier this year that this project could be cancelled. OpenAI and Apple are also heavily rumored to be prospective customers.

Why Big Tech Is Chasing Cheaper Inference

For the providers in the AI ecosystem, monetizing GPUs depends on inference, and thus revenue becomes a function of GPUs and tokens and profits become a function of cost. Nvidia’s Blackwell offers a massive leap in performance and can train models such as Meta’s Llama 3.1 405B in as little as 27 minutes, yet the cost advantages offered by custom silicon can translate into higher margins in the long run from lower inference serving costs.

For example, Google recently announced that its upcoming seventh-gen TPU Ironwood is its “most performant and scalable custom AI accelerator to date, and the first designed specifically for inference.” Ironwood comes in two sizes, a 256 and a 9,216 chip configuration, with the larger size offering up to 42.5 exaflops of performance.

Google adds that Ironwood offers 2x the performance per watt as last-year’s generation Trillium, with 6x more HBM and 4.5x the HBM bandwidth. This allows it to deliver more capacity per watt at a time when power is a primary constraint, and provide customers with more cost-effective AI workloads.

This is exactly what Broadcom sees arising from this inference growth curve, as CEO Hock Tan asserted that the company has quite a bit of visibility into “increased deployment of XPUs next year, much more than we originally thought and hand-in-hand with it, of course, more and more networking.” The necessity of networking in larger clusters means demand is likely to remain robust even given custom silicon will not keep pace with Nvidia’s merchant sales into the hundreds of billions.

Higher-than-expected deployments of custom silicon combined with strong demand for networking should provide robust tailwinds for AI revenue growth beyond 2026. Broadcom currently has enough visibility to place possible demand acceleration for 2H 2026 on the table, and this could easily persist through 2027 and beyond should inference demand flourish and as the path to 1 million accelerator clusters materializes.

Assuming Broadcom can maintain another 60% YoY growth in FY27 on stronger demand and potential conversion of its 4 current prospects, AI revenue would close in on $50 billion, or up to 60% share of revenue. Even if growth then slows to 30% YoY in FY28, Broadcom would still be more than doubling its AI revenue to $65 billion in just three years.

Broadcom Reports 170% YoY Growth in AI Networking

Broadcom has cemented itself in second place in AI revenue as it closes in on $20 billion this fiscal year in AI revenue -- with a line of sight toward $30 billion by the end of fiscal 2026. AI revenue accounted for more than 50% of Semiconductor revenue for two quarters in a row and nearly 32% of total revenue in Q2.

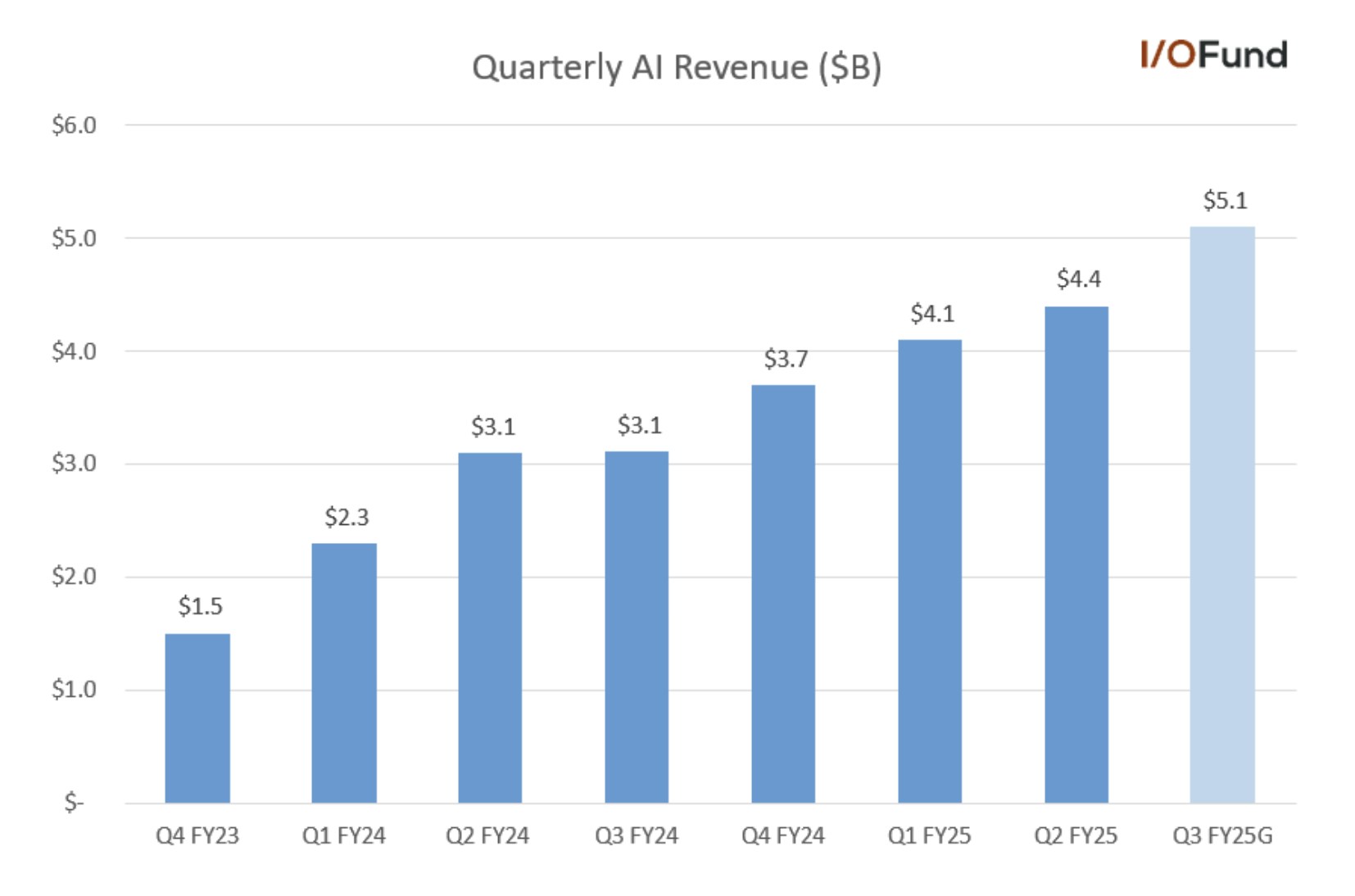

AI semiconductor revenue rose 46% YoY to $4.4 billion, in line with management’s guidance. Although this was a deceleration from 77% YoY growth in Q1, Broadcom forecast $5.1 billion in AI revenue in Q3, pointing to a rebound to 60% YoY growth – marking ten consecutive quarters of growth.

In the current quarter, the 46% AI semiconductor growth was driven by networking, which was up 170% YoY and represented 40% of AI revenue. In the opening remarks, the CEO stated the following regarding this outsized growth: “As a standard-based open protocol, Ethernet enables one single fabric for both scale out and scale up and remains the preferred choice by our hyperscale customers. Our networking portfolio of Tomahawk switches, Jericho routers and NICs is what's driving our success within AI clusters in hyperscalers.”

Broadcom’s AI revenue was forecast to reaccelerate in Q3 to 60% YoY to $5.1 billion. Source: I/O Fund

Q3’s guidance was ahead of some analyst expectations for $4.9 billion in AI revenue in the quarter, ticking higher as Google’s TPU v7p (Ironwood) begins to ramp. Q3 would also mark the largest sequential growth in over a year on a dollar basis, at ~$700 million.

Additionally, analysts look to already be penciling in further strength in Q4, with Bernstein’s Stacy Rasgon suggesting that Broadcom could be eyeing $5.8 billion in AI revenue in Q4 assuming it sustains 60% YoY growth. Given that Broadcom’s 1H revenue was up more than 57% YoY, this seems a reasonable assumption, especially considering management is eyeing near 60% growth in FY26.

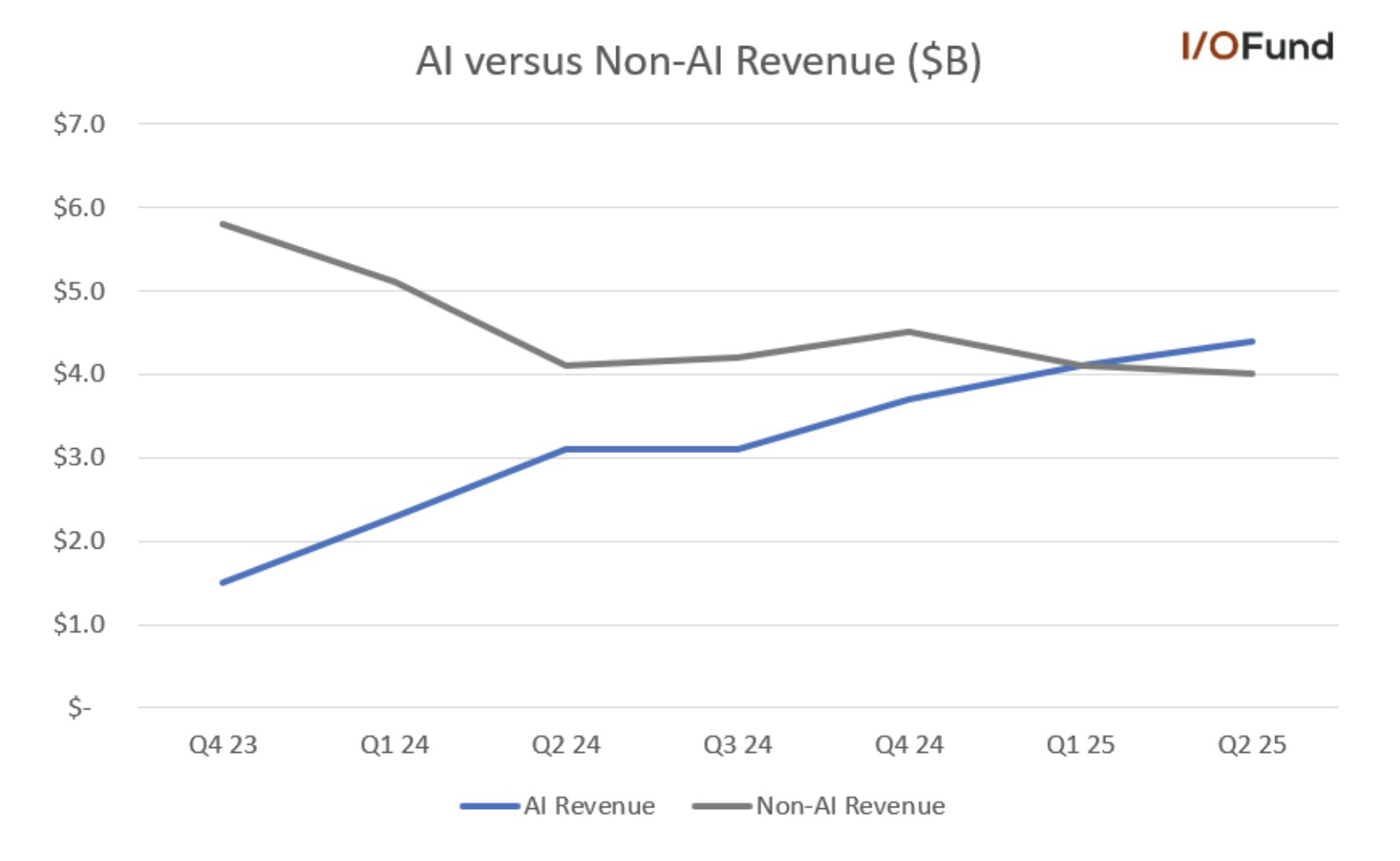

More importantly, AI’s strength is masking persisting softness in non-AI revenue, which could continue to be pressured due to Broadcom’s high consumer exposure. Broadcom noted that non-AI revenue “is close to the bottom” but it “has been relatively slow to recover” with revenue down (5%) YoY to $4 billion in Q2.

Broadcom’s AI revenue accounts for more than 50% of Semiconductor revenue, masking persisting softness in non-AI revenue. Source: I/O Fund

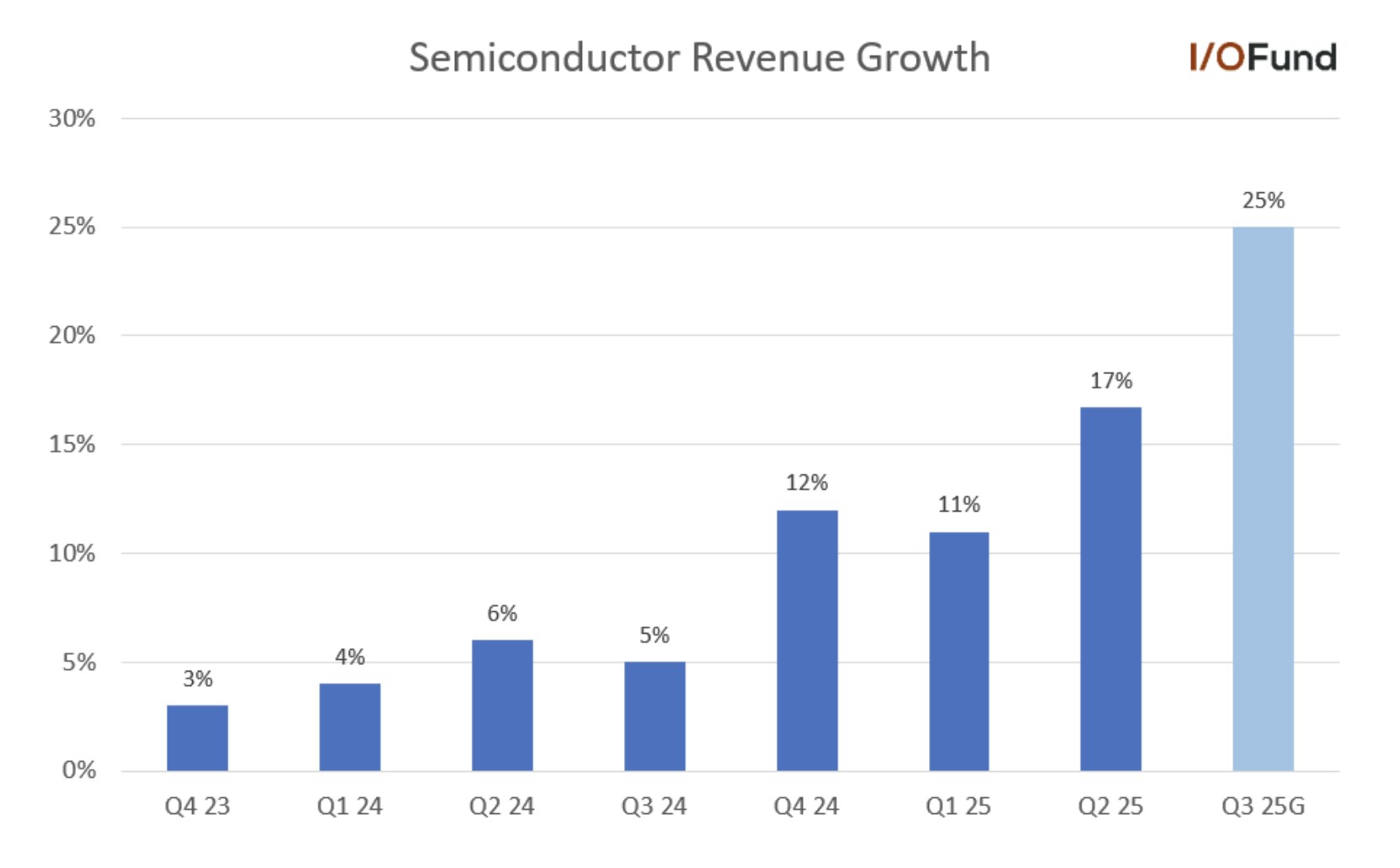

Despite this weakness extending into Q3 with revenue expected to be flat QoQ at $4 billion, semiconductor revenue is accelerating – growth accelerated from 11% to nearly 17% in Q2, with the $9.1 billion semiconductor revenue guide pointing to an acceleration to nearly 25% growth in Q3.

Should non-AI revenue soon find the bottom and begin to recover, this will provide support for continued Semiconductor growth. However, any persisting weakness in non-AI stemming from this elevated consumer and Apple exposure that AI revenue must absorb presents a real risk that investors should keep in mind through the rest of the year. Broadcom is also one of the more exposed semiconductor companies to China with tariffs, with more than $10 billion in revenue from the nation in fiscal 2024.

Broadcom’s AI revenue strength is evident as Semiconductor revenue was guided to accelerate 8 points to 25% YoY despite flat non-AI revenue. Source: I/O Fund

Broadcom Stock to See Lift from AI Inference

Broadcom is aiming to capture growing inference tailwinds, with management explaining that the recent surge in inference demand is driving increased confidence in their FY26 AI revenue growth rate.

CEO Hock Tan said that Broadcom’s hyperscale clients are “doubling down on inference in order to monetize their platforms,” and as a result, he expects Broadcom could “actually see an acceleration of XPU demand into the back half of 2026 to meet urgent demand for inference on top of the demand we have indicated from training.” This new dynamic is what is driving Tan’s confidence in stronger growth in FY26, saying that he now anticipates the “fiscal 2025 growth rate of AI semiconductor revenue to sustain into fiscal 2026.”

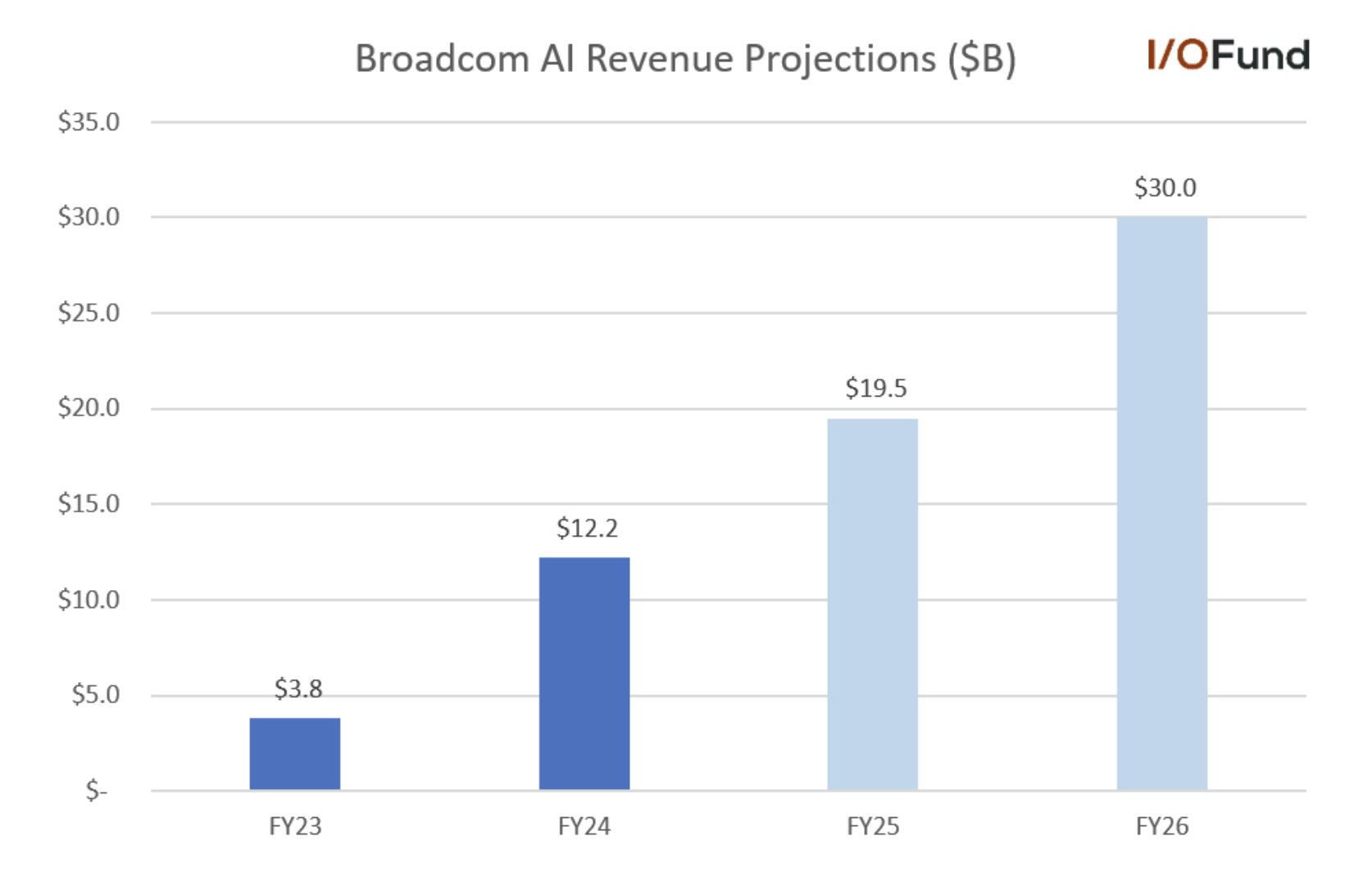

This commentary plus potential demand acceleration in 2H 26 suggests that Broadcom has visibility into $30 billion AI revenue potential next year. Broadcom has not provided a full FY25 AI revenue guide yet, but it is on track to deliver approximately $19 to $20 billion in AI revenue in FY25, up ~60% YoY assuming 60% growth to $5.9 billion in Q4.

Broadcom’s AI revenue is projected to grow approximately 60% YoY in FY25 and maintain that growth in FY26. Source: I/O Fund

Maintaining 60% growth through FY26 would project AI revenue to $30 to $32 billion. This trajectory indicates Broadcom is likely driving AI revenue ahead of expectations over the next four to six quarters, with Morgan Stanley saying that $26 to $30 billion in AI revenue is “higher than what is in Street models.” Evercore is modeling 58% AI revenue growth in FY25 and 50% in FY26, implying $28.9 billion.

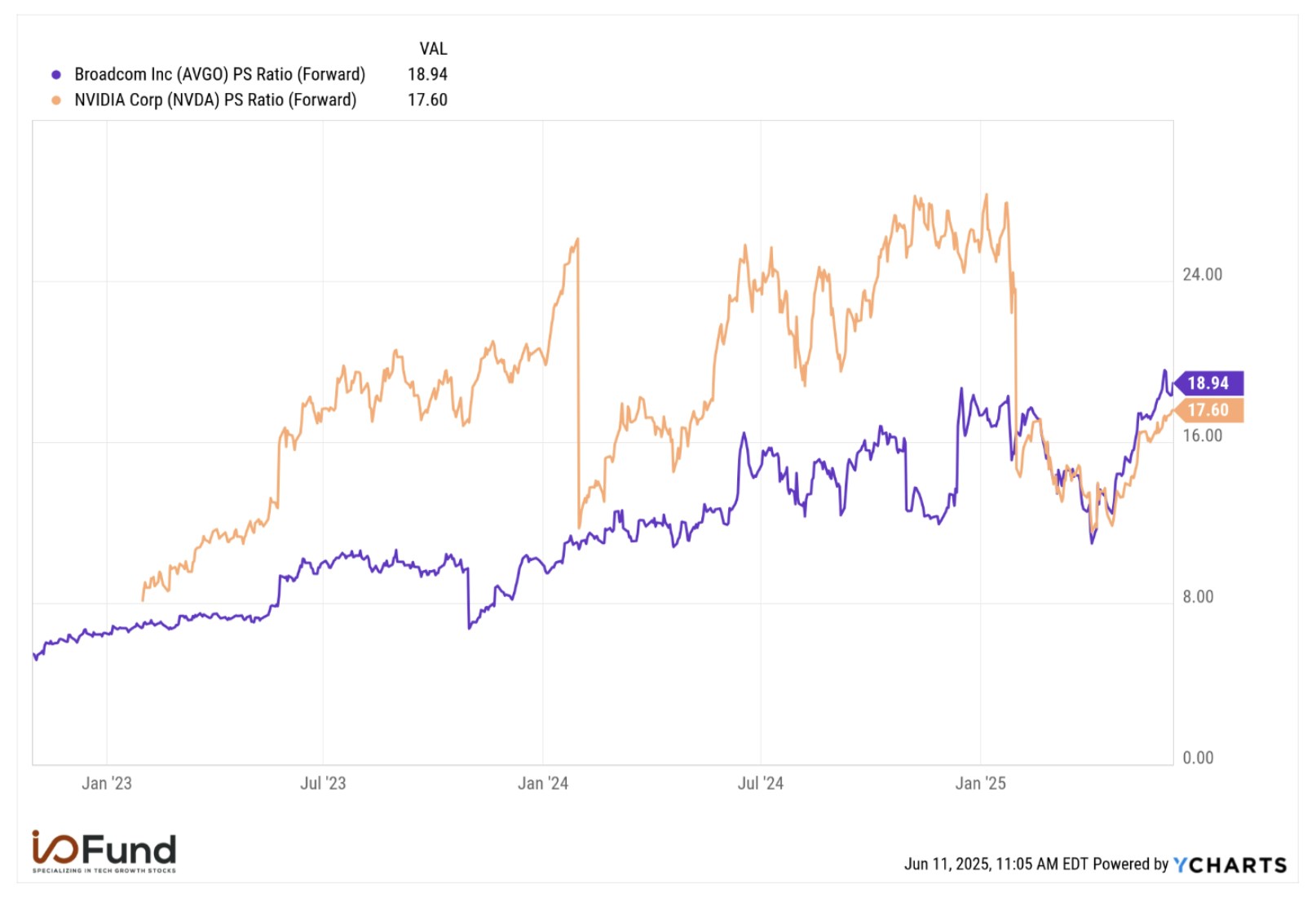

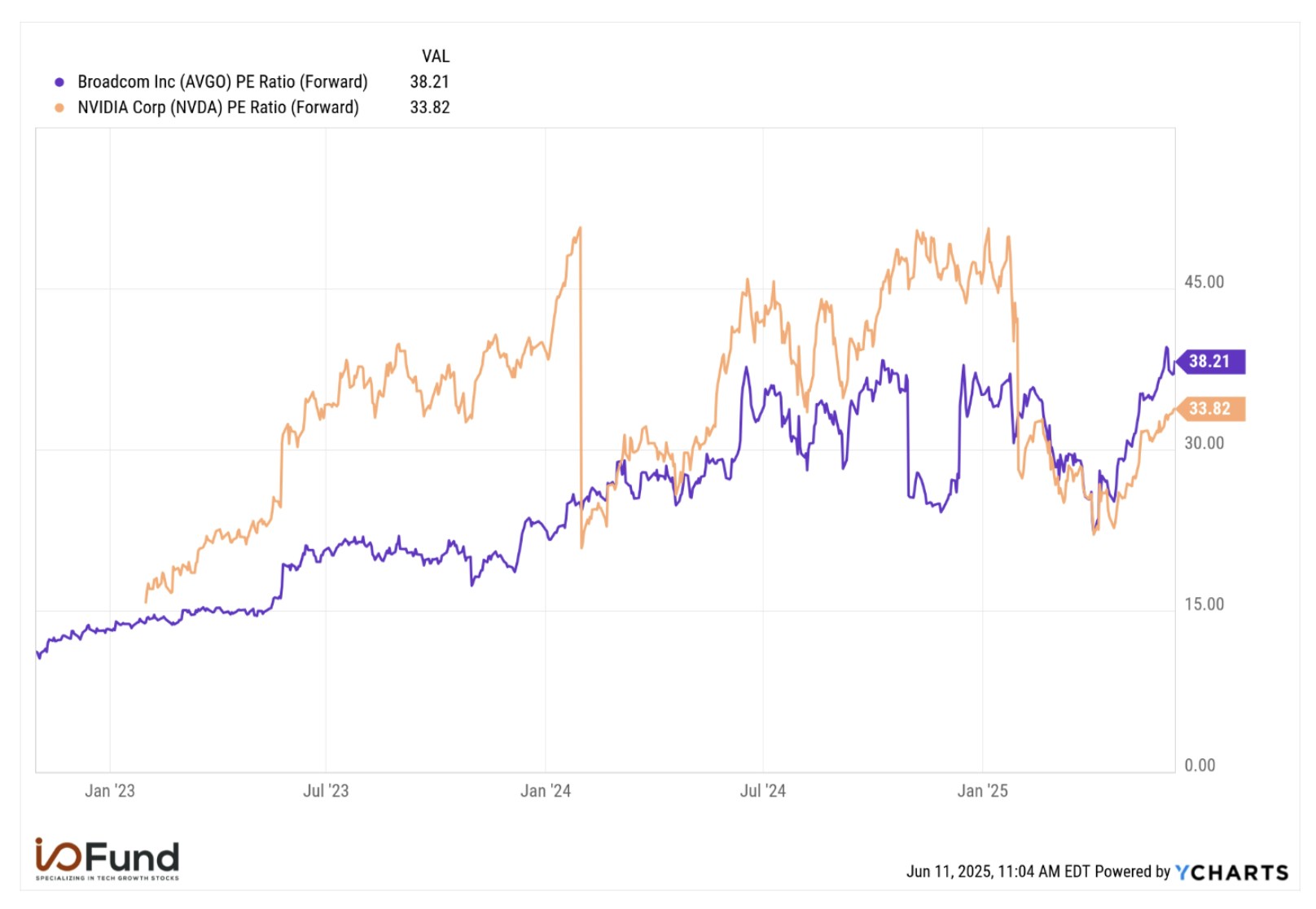

Broadcom Passes Nvidia Stock's Valuation – First Time in 9 Years

There’s no denying that Nvidia is the outright leader in the AI accelerator market with an estimated $200 billion in revenue this year with roughly $180 billion of that from AI data center whereas Broadcom will report $20 billion this year.

Who is in second place is no contest yet what is second place worth when there is nearly a $160 billion gap? Broadcom clearly has key ingredients to have earned this second-place position yet there is also exposure to China and exports via Apple and ByteDance, one of its rumored customers.

Meanwhile, for the first time in nine years, Broadcom has a higher valuation than Nvidia.

On the top-line, Broadcom trades at nearly 19x forward revenue, an almost 8% premium to Nvidia’s 17.6x multiple. AVGO stock was at a 14% premium heading into Q2’s earnings. This is also 65% higher than Broadcom’s 5-year average 11.4x forward revenue multiple.

Broadcom is currently valued at an 8% premium to Nvidia on a forward price-to-sales basis. Source: YCharts

On the bottom line, Broadcom trades at 38.2x forward earnings, a 13% premium to Nvidia and a more than 18% premium to the semiconductor industry at 32.3x. Broadcom has strong margins – 65% adjusted operating margin and 52% adjusted net margin – driving strong EPS growth, at a 25% expected CAGR through FY27; however, the custom silicon ramp presents some headwinds to gross margin as it grows its mix share.

Broadcom trades at 38.2x forward earnings, a 13% premium to Nvidia and a more than 18% premium to the broader semiconductor index on a forward PE basis. Source: YCharts

Broadcom’s competitiveness with Nvidia on margins and its ability to drive strong EPS growth via operating leverage, while capitalizing on growing accelerator and networking demand lend to its valuation, as it is a clear second to Nvidia and far ahead of smaller peers Marvell and AMD in AI revenue. However, this premium valuation looks to price in above-expected AI revenue growth through 2026, likely closer to a 70% or even 75% CAGR through 2026 as Broadcom is currently tracking its SAM CAGR at 60% through FY26.

Is Broadcom Stock a Buy?

Subscribe for Full Access to the Article

Behind the Paywall is the Following information:

- It’s often subtle commentary – and not the headlines – that reveals the biggest opportunities. Find out the one thing Broadcom CEO stated that all investors MUST hear to help position for 2025-2026.

- The clear catalyst within Broadcom’s product portfolio and timing for this product to help push forward the next leg up in AI revenue growth.

- The I/O Fund’s trade setup – exclusive only to subscribers. We detail buy zones we are eyeing for the #2 stock in AI given its immense demand yet stretched valuation.

Paid subscribers, click here to view the full article

Not ready to subscribe but want more thoughtful analysis from a top-performing team in tech? Every week, we publish free research. 👉 Sign up here.

Please note: The I/O Fund conducts research and draws conclusions for the company’s portfolio. We then share that information with our readers and offer real-time trade notifications. This is not a guarantee of a stock’s performance and it is not financial advice. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis. Beth Kindig and the I/O Fund do not own shares in AVGO at the time of writing and may own stocks pictured in the charts.

Recommended Reading:

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su