Alphabet Stock Shows Underlying Strength Compared To Facebook (Meta Platforms)

May 04, 2022

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Apr 28, 2022,10:45pm EDT

If an investor were to believe market price action this week, it would appear Facebook had strong earnings while Alphabet stumbled. Yet, the opposite is true. Primarily, it was strength in retail ads that led to Alphabet reporting healthy growth of 23%. Meanwhile, Meta Platforms (Facebook) reported revenue growth of 9.7% and is guiding for roughly 0% growth from $28.5 billion in Q2 2021 to $29 billion, at the midpoint for Q2 2022. This analysis looks at why Alphabet is able to provide higher revenue guidance despite 80% of its revenue coming from ads while Facebook is guiding for flat growth.

Notably, Q2 is particularly hard because there are three heavy macro headwinds: supply chain issues, Ukraine-Russia situation, and the transition that Apple has forced with changes to attribution and measurement on iOS. When you add the one-time event of Covid, which plummeted ad spend in Q2 2020, only to lead to a surge in ad spend the following year Q2 2021, the hurdle to clear for revenue growth is at a historic high. We believe those ad-tech stocks that can show top line growth right now are providing important clues for when macro headwinds clear.

BACKGROUND:

The ad-tech industry remains in a whirlwind of changes following iOS privacy changes that limit third-party tracking on Apple mobile devices. I am hyper focused on identifying who the winners and losers will be following these changes, as it will determine who will lead ad-tech going forward. This issue is important because it impacts leading FAANG ad-tech companies, such as Facebook (Meta) and Google (Alphabet). Wall Street particularly likes ad-tech’s bottom line, and will aptly reward those stocks that can capture more ad spend.

In the below analysis, I review Google’s Q1 2022 results and focus on its ad platform (I am ignoring Google Cloud for now) and look for hints if Google is being impacted by the recent iOS changes. You’ll find that Google has held up well relative to other app-based advertising platforms, such as Facebook, following the changes to third-party identifiers. This is because Google has a first-party data advantage, which is critical during a time that attribution and measurement is limited by third parties. I explain why in more detail below.

Google’s Q1 Ad Growth Remains In-Line

While the market is still digesting the macro headwinds previously mentioned – supply chain and Ukraine-Russia; the third headwind of attribution and measurement changes is the headwind that investors should pay most attention to as it leads to a material change in story for ad-tech companies. Meanwhile, the other two headwinds will resolve in time.

Q1 earnings are provide valuable data of who is most and least impacted. Two critical data points will be Facebook’s and Google’s Q1 results, as most of their sales come from mobile ads. Google recently reported that sales grew 23% YoY to $68 billion, which were in-line with estimates. Furthermore, Google’s Search business slightly outperformed and grew 24% YoY to $40 billion. This follows the outperformance in Q4 as Search sales grew 36% YoY in Q4 while total Q4 sales grew 32% on a year-over-year basis. It may appear that Alphabet’s search revenue is slowing from 30% in the year-ago quarter, but the deceleration in search revenue is due to the tough comps, and relative to Facebook, is outperforming.

The strength in Search highlights the advantage that having first-party data provides. This is because Search is primarily done on a browser, allowing Google to capture valuable first party data from ownership of Google Chrome, Google Search and also from Android OS. Moreover, Google is releasing new products, such as Topics API, which enables behavioral targeting. This is a direct shot at Meta Platforms, who is known to be quite competitive on behavioral targeting through taxonomies.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

However, while Search remained strong, both YouTube and Google Network sales underperformed during the quarter. For instance, YouTube grew sales just 14% YoY to $7 billion, a steep slowdown from the 25% and 49% YoY growth rates from last quarter in Q4 and Q1 2021, respectively. Google Network sales increased 20% YoY to $8 billion. This also represented a deacceleration from the 26% YoY growth rate in the prior quarter.

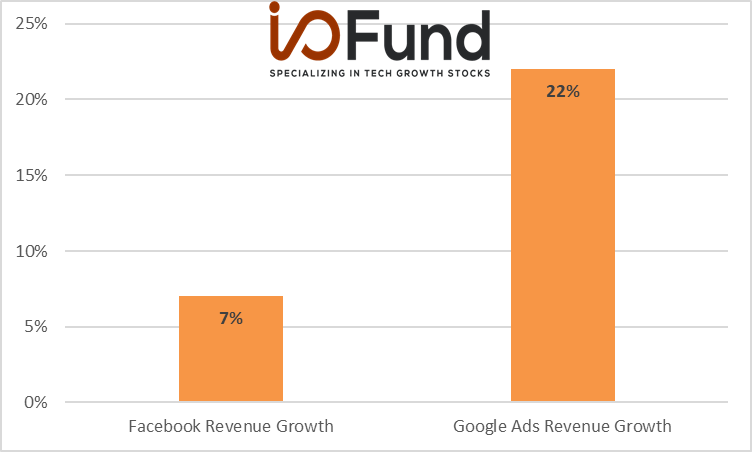

In aggregate, total ad sales increased 22% YoY to $55 billion, a deacceleration from the 33% YoY growth rate in the prior quarter. It is notable that despite the headwinds in YouTube and Google Network, Google’s sales vastly outpaced Facebook’s Q1 revenue growth. As shown below, Google’s ad sales grew nearly 3x faster than Facebook’s 7% growth.

I/O Fund

I believe this outperformance was driven by Google’s first-party data advantage. Moreover, YouTube revenue was the biggest laggard during the quarter and YouTube sales grew 14% YoY to $7 billion during the last three-months (fun fact: YouTube is larger than Google Cloud). The slowdown in YouTube may suggest that ads have been impacted by iOS changes, but its important to consider that YouTube grew sales 49% YoY in the year-ago quarter, leading to a tougher comparable base period.

During the Q1 call, Google’s management team explained that the tough comp and “modest” growth from direct response advertising had also impacted the segment, but noted that brand advertising remained an area of strength. The diversification across content types and ability to offer at true omnichannel strategy across mobile, browsers and CTV likely contributed and suggests that brands have shifted ad budgets to YouTube, likely due to its ability to measure ROI at the expense of competing platforms.

Google also reiterated this point during their Q1 Conference Call when CBO Philipp Schindler explained that being able to fully measure what users do after they click on an ad is critical to measuring ROI. He added that “Measurement is also obviously a key component to success [in CTV], and we want to make sure that advertisers can fully measure their YouTube CTV video investments across YouTube and YouTube TV for an accurate view of true incremental reach and frequency and so on”.

CBO Schindler’s comments highlight the importance of measurement, a key aspect of digital advertising that has been challenged following the changes to iOS cookies. If advertisers cannot measure ROI, they tend to limit their ad expenditures, so its critical that ad platforms find solutions to measure ROI in order to sustain growth.

Perhaps the most important comment during the Q1 Conference Call was a statement by management that Google continues to see strength in Retail, reiterating comments made during the Q4 2021 Earnings Call that retail (e-commerce) continues to be strong.

This brief statement is very important, as it adds support that Google will not be as impacted by the iOS changes. Given the signal loss from iOS changes, e-commerce has been one of the hardest hit verticals. Google’s strength here is likely due to its first-party data advantage.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Here is what Facebook CFO David Wehner said about Google’s strength in the retail vertical during Facebook’s Q4 2021 Conference Call:

“e-commerce was an area where we saw a meaningful slowdown in growth in Q4. … But on e-commerce, it's quite noticeable -- notable that Google called out, seeing strength in that very same vertical. And so given that we know that e-commerce is one of the most impacted verticals from iOS restrictions, it makes sense that those restrictions are probably part of the explanation for the difference between what they were seeing and what we were seeing.”

Google’s statement that it continues to see strength in retail suggests that it is not as impacted from the iOS changes relative to app-based peers such as Facebook. Importantly, Search is often based on a web browser (Google Chrome), allowing Google to capture first party data and limiting the signal loss from the removal of cookies on mobile based apps.

Our thesis is that in this new cookie-less world, owners of first-party data will outperform going forward. We expect that Google will remain strong given its ownership of first-party data on both its Search platform and also its YouTube platform. However, Facebook will likely continue to struggle here due to its reliance on third-party data and not owning “the real estate,” or essentially the device and/or operating system while needing to collect data from this device in order to support its high ARPU. We wrote about this for Forbes recently: Facebook Stock: A Permanent Change to the Business Model

Two weeks ago, I held a webinar that discussed Facebook’s business model change and why I believe there will be meaningful erosion to ARPU. This is a thesis we first published four years ago in 2018 when we warned this FAANG faced considerable headwinds. In the webinar below, we discuss why we believe Meta Platforms (Facebook) will continue to underperform and who the winners will be from this shift, including first-party data owners, supply side platforms, and contextual advertising publishers and platforms.

Conclusion

Notably, Q2 is particularly hard because there are three heavy macro headwinds: supply chain issues, Ukraine-Russia situation, and the transition that Apple has forced with changes to attribution and measurement on iOS. When you add that the one-time event of Covid, which plummeted ad spend in Q2 2020, and later led to a surge in ad spend the following year Q2 2021, the hurdle to clear for revenue growth is at a historic high. We believe those ad-tech stocks that can show top line growth right now are providing important clues for when macro headwinds clear.

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per