Q3 Stock Earnings Preview - What to Expect for 7 Ad Tech Stocks

October 15, 2021

I/O Fund

Team

This quarter, we chose to go over Roku, Snap, PubMatic, The Trade Desk, Magnite, Pinterest, and Digital Turbine for an earnings preview on what to expect from these ad-tech companies. This list was chosen by those with the most forward growth, those with the highest valuations or those that have recently completed an acquisition so we can look deeper into what the Street is expecting from management.

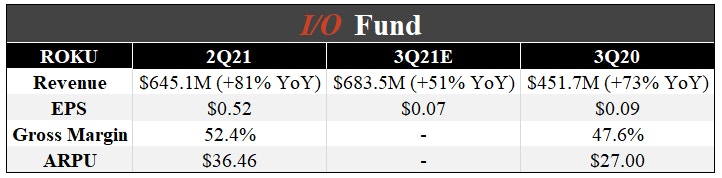

Roku Inc– Earnings on November 05th

Below is a chart of Roku’s financials from last year, last quarter and what is expected in the upcoming quarter.

The consensus estimates suggests that the revenue growth will be slowing down in the next quarter. Below are the analysts’ views on Roku.

- Wells Fargo analyst Steven Cahall has recently downgraded the stock to Equal Weight and reduced the price target from $488 to $350. He states that "The primary reason we go from Overweight to Equal Weight is, while there may still be a long ARPU runway, it's far better understood," Cahall writes in a note. "Consensus CY22E/CY23E ARPU is +50%/+47% over the past year to now $50/$60. In our January deep dive, we called CY22E ARPU of $55 a bull case scenario; but current consensus shows our alpha has decayed. The Q2 ARPU beat slowed a lot from Q1."

- On the other hand, Guggenheim analyst Michael Morris says that the recent sell-off is a good opportunity to buy the shares as he upgrades the stock from a neutral rating to a buy with a price target of $395. “We expect the connected television ad marketplace will continue to grow at a rapid pace and that Roku will be a primary beneficiary — this view is unchanged,”

- KeyBank analyst Justin Patterson has said that the New Amazon fire TV’s as an incremental positive to the company and its competitive position. He notes that Amazon’s devices appear to be similar to Roku’s offering.

Please note, the I/O Fund does not necessarily agree with the financial analysts mentioned above rather our goal is to objectively review companies. Our premium members have been updated frequently on Roku and we have been able to buy this stock very early before the market understood the true potential of this cord-cutting and AVOD play.

You may view our previous analysis on Roku below:

Video: Is the Bottom in for Roku?

The Crucial Difference Between Roku and Netflix

Will Roku Go Boom or Bust This Year

Roku’s Stock Price: Will There Be Another Pullback?

Roku Q3 Earnings: Choppy But Unshakeable Long-Term

Update on $ROKU – Will Roku Miss Earnings?

3 Reasons Why Roku Will Be The Next Tech Darling

Here’s Why Roku Stock Will Surpass $100 In Next Two Years

Long on Roku – Even if they Miss Q1 Earnings

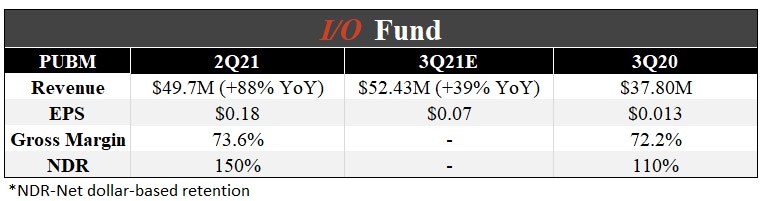

PubMatic Inc – Earnings on November 15th

PubMatic revenue growth rate is expected to show a notable deceleration in comparison with the recent quarter although margins remain high. We will be keeping an eye on the net dollar-based retention ratio in the next quarter. The management has raised the 2021 revenue growth forecast to 38% to 40% and 25% next year.

Macquarie analyst Tim Nollen has an outperform rating on the stock with a price target of $37. He believes that the company benefits from “a strong advertising backdrop in which traditional advertising is shifting to digital, open Internet players are gaining share from walled gardens, and ad spend is consolidating around fewer SSPs,".

Macquarie further states “PubMatic is banking on real CTV growth coming from open exchange, where the OpenWrap bidding engine will be able to grow alongside that migration - though that still needs time to play out”.

“And on an enterprise value/sales basis, it's trading at roughly a 3.5x discount to its closest peer, Magnite and a 5x discount to the broader ad-tech universe.”

You can find the ad-tech companies which had their growth estimates updated in the last few months here.

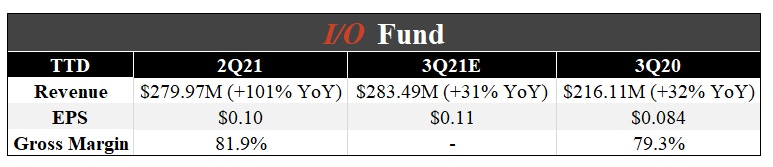

The Trade Desk Inc – Earnings on November 05th

The consensus revenue estimates for the next quarter suggests a sharp drop in the revenue growth, as well. One of the primary reasons for the strong revenue growth in the second quarter was due to lower comps as Q2 2020 revenue fell 13% YoY.

Needham analyst Laura Martin has a buy rating with a price target of $100 and her 3Q21 revenue estimate is $284M.

She is of the view that “Digital markets have proven themselves to have winner-take most economics, and we believe TTD is the winner among DSP’s (demand side platforms). 30% of TTD’s revenues come from CTV which should accelerate TTD’s growth trajectory since CTV revenues are growing 3-5x faster than other digital media categories. About 15% of TTD’s 1H21 revenues came from outside the US, and offshore is growing faster than the US, suggesting a longer growth runaway”.

Sign up for I/O Fund's free newsletter with gains of up to 1100% - Click here

Citi analyst Nicholas Jones has a price target of $85 and a neutral rating. He believes: “Trade Desk is a dominant and best-in-class adtech player, but continues to see risk associated with technology disruption and privacy regulation”.

You can view our previous analysis below:

The Trade Desk: Effects Of Lower Ad Demand In 2020

8 Predictions For Tech Stocks In 2020

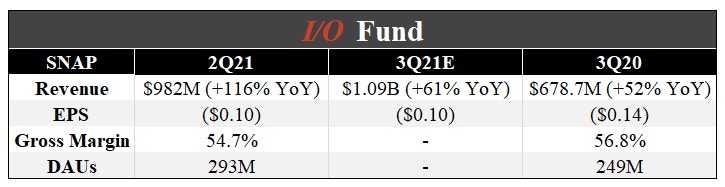

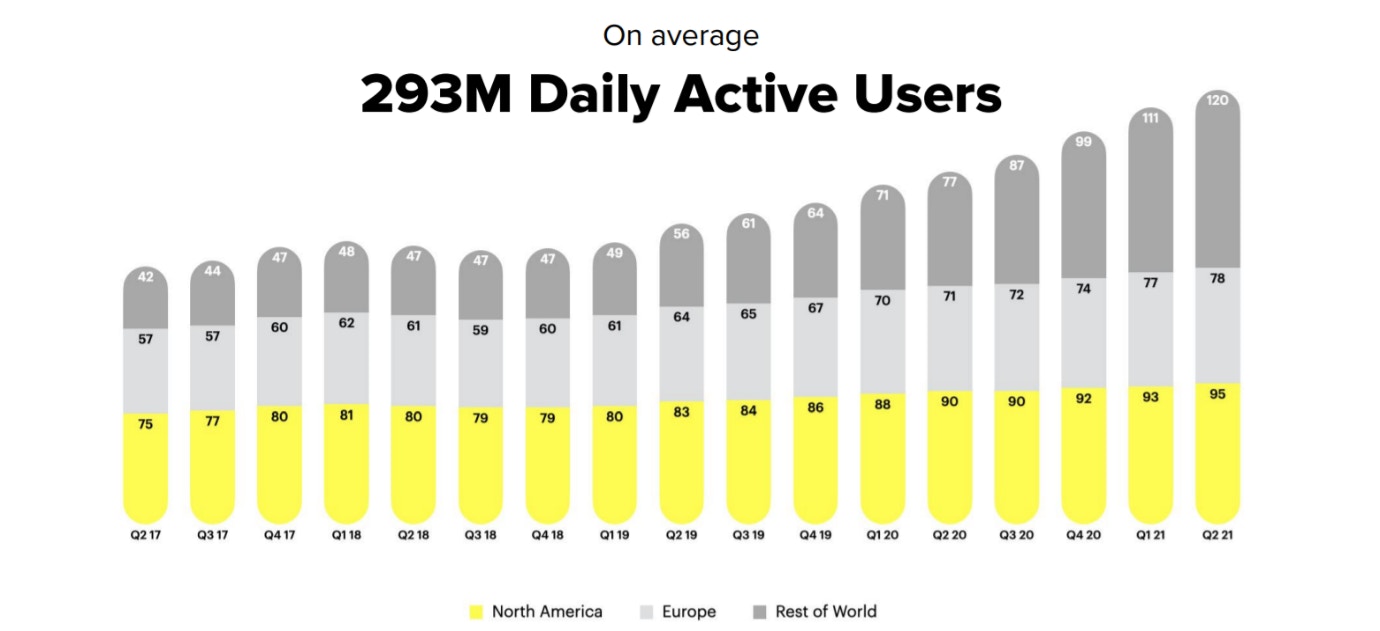

Snap Inc – Earnings on October 21st

The revenue growth is expected to be lower than the second quarter but higher than the previous year. The adjusted EBITDA in the second quarter showed a strong growth when compared to the previous year. The management also expects to show an improvement in the third quarter.

Goldman Sachs’ analyst believes that the company has a high chance to achieve its target of 50% plus revenue growth in the next three years. Goldman Sachs also believes that the strong growth will be accompanied by margin expansion with the EBITDA margins improving from -13% in 2021 to 40% in 2026. It has a price target of $90.

Source: Investor Presentation

RBC is also positive on the company. They have initiated coverage on the company with an outperform rating and a price target of $88. According to the analysts “Snap has everything pointed in the right direction to become a top social media business, stable footing in an attractive secularly growing ad market, an evolving direct response/ad-load/downfunnel commerce narrative leading to potential ARPU [average revenue per user] and profitability upside and finally, new products that could invite broader usage and incremental monetization.”

Channel checks were more mixed, but the analysts think the possibility of adverse near- or medium-term effects “seems low” compared to the stage of the company’s developing monetization.

You can view our previous analysis below:

Pinterest and Snap Show V-Shaped Recovery; Cloudflare Guns for Zero-Trust

Social Media Projected to Lead Global Ad Spend in 2021

Magnite Inc – Earnings on November 09th

The company is benefitting from the strong growth in digital advertising. However, as discussed earlier the super growth was partly due to the M&A with SpotX.

Analysts are positive on this stock as Berenberg analyst Alexandra Ross has initiated coverage with a buy rating and a price target of $37. Other analysts who are positive about the company include Susquehanna analyst Shyam Patil. He likes the company as a CTV play and is also optimistic about the recent acquisitions of SpotX and SpringServe.

Earlier this year, Truist analyst Thornton said, “Magnite is well positioned in the connected-TV advertising space, with secular growth in connected TV estimated to represent more than half the company's overall revenue by 2024”.

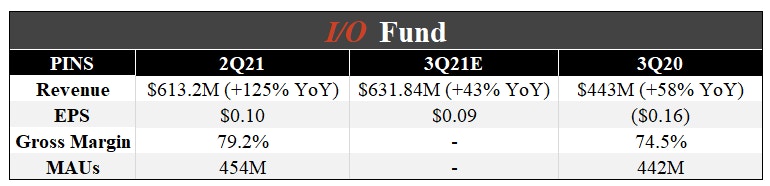

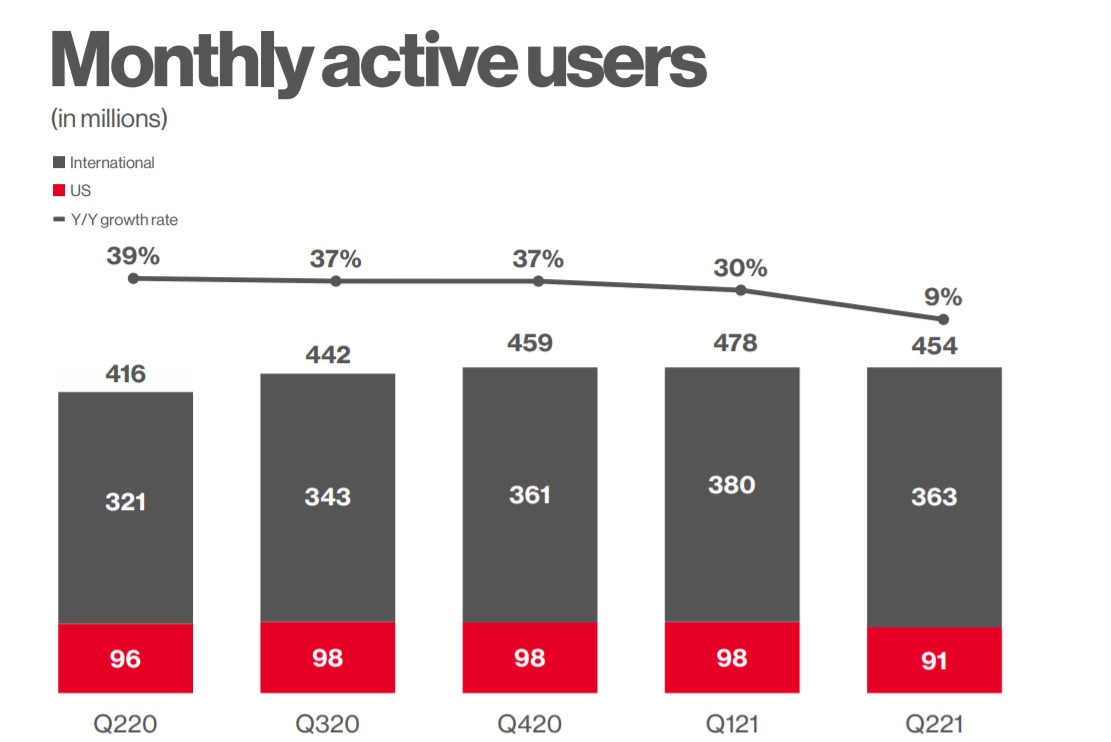

Pinterest Inc – Earnings on October 28th

The stock fell after releasing the 2Q 21 results as the company failed to meet the consensus global monthly active users (MAUs) in spite of beating the revenue and EPS consensus estimates. The management in the earnings call mentioned that due to the lack of visibility they will not be giving guidance for MAUs for this quarter.

Source: Earnings Presentation

RBC Capital analyst Brad Erickson initiated coverage of Pinterest with a Sector Perform rating and $58 price target. “We believe user growth is likely closer to plateauing than not and our channel feedback indicated that outside of targeted categories, conversion needs improvement, particularly vs FB where we think user crossover is virtually 100%. Expectations have come down after last quarter’s miss. However, we need to see an improving content or commerce experience before getting more constructive”.

Sign up for I/O Fund's free newsletter with gains of up to 1100% - Click here

Piper Sandler analyst Thomas Champion has a neutral rating and a $68 price target. He believes “that the post Q2 earnings selloff may be overdone. Recent monthly active user declines seem driven by non-mobile app users, which contribute less to the financial model”. He sees a more favorable setup for the stock into year-end.

Earlier this year, Argus analyst downgraded the stock to neutral in response to lower user growth in the second quarter. “The disappointing guidance reflects the decline in online sales as traditional stores reopen and users spend more time away from home. But it has strong brand recognition in the U.S. and prospects for growth in international markets over time."

You can view our previous analysis here:

Social Media Projected to Lead Global Ad Spend in 2021

Snapchat Reported Accelerating Growth. Here’s What to Expect From Pinterest

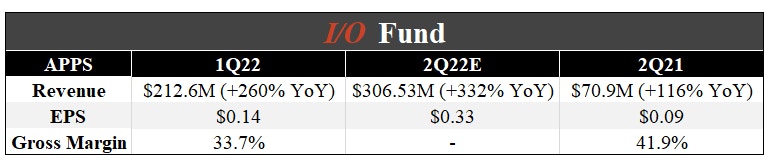

Digital Turbine – Earnings on October 29th

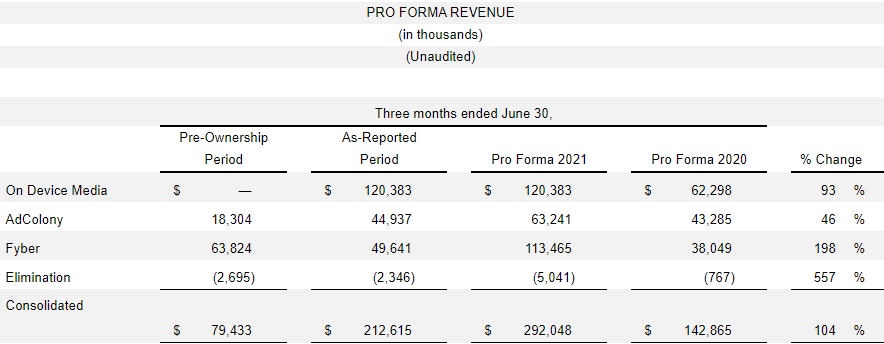

As discussed, Digital Turbine’s revenue growth was partly due to the company’s acquisitions which were completed in the quarter.

Below are the details of the proforma revenue which will helps to give a better picture as the growth is around 104% for fiscal Q1 2022.

Source: 1Q FY2022 earnings release

Canaccord analyst Austin Moldow has upgraded the stock from a hold to a buy. He also raised the price target to $95. “The company has now gotten stronger with its transition into "a full phone lifecycle monetization engine" thanks to the addition of in-app advertising, which grew the total addressable market. He further notes that the Digital Turbine's valuation has "become more reasonable" and the fundamentals have improved up to justify the valuation”.

On the other hand, Macquarie analyst Tim Nollen has initiated coverage on the company with a neutral rating and $60 price target. He's unable to determine the relative position of Digital Turbine's on-device software versus ironSource's (IS). Digital Turbine's in-app advertising business has only just now come on board, and while these acquisitions are growing fast, they are notably smaller than peers”.

Oppenheimer analyst Timothy Horan reiterated an Outperform rating and $100 price target. "Single-Tap could be a revolutionary product, akin to the transition from banner ads to video. Despite the already significant dollars, Single-Tap is very early in its growth phase, with APPS being very selective on the brands being allowed to participate. The moat on Singe-Tap is sizable: IP, hundreds of millions of devices scale, as well as huge investment in last-mile measurement and attribution."

Bradley Cipriano and Royston Roche contributed to this article.

Disclaimer: This is not financial advice. Please consult with your financial advisor in regards to any stocks you buy.

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su