Facebook Stock: When Free Cash Flow Isn’t Enough

February 04, 2020

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Jan 30, 2020,03:32pm EST

Facebook’s free cash flow and profit margins are some of the best in the S&P 500. Profit margins are at 35 to 40 percent, free cash flow margins around 19%, and annual growth has exceeded 25 to 30 percent for many consecutive years.

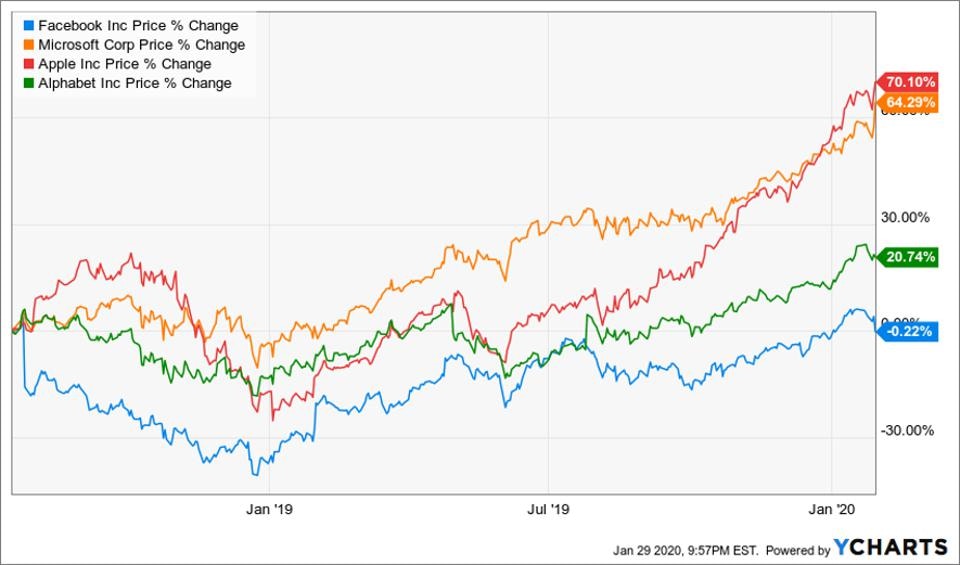

Despite this, Facebook’s stock price has struggled to keep up with the stellar gains of its mega-cap tech peers. Facebook’s previous share price high was in July of 2018 at $217.50. Recently — and very briefly — the stock traded a few dollars higher at $222 leading into the earnings report yesterday. The stock failed to hold and is now down 6% following earnings.

The issues that Facebook has encountered are not easily found in the financials. Facebook fires on all cylinders when considering Warren Buffet’s investing discipline to seek companies with strong free cash flow and no debt. Instead, Facebook’s issues are at the product level, which discounted cash flow analysis does not help to detect.

Primarily, the critical risk is that Facebook’s product, as it was built, was not designed to co-exist with privacy. The concerns that both consumers and regulators are raising require much more than a bandaid; they require an entire overhaul.

You can see some evidence of this in the number of privacy engineers the company employs — totaling 1,000 per the Q4 earnings call. This is double the amount of Google at 500 engineers, despite Google making twice the ad revenue as Facebook.

Before the stock dropped in Q2 2018,I had covered a few of the technical issuesFacebook was facing across its suite of apps. I encouraged investors to consider Cambridge Analytica the norm rather than a fleeting headline scare by breaking down the complexity of Facebook’s privacy issues. Nearly two years later, these complexities continue to haunt the company.

Investors who chose Facebook over Microsoft, Apple or Google saw very few gains over the past eighteen months while tech peers gained up to 70%.

Review of Facebook’s Q4 Earnings

Facebook beat on the top and bottom line on Wednesday with EPS of $2.56 compared to analyst estimates of $2.53. Revenue rose 25% to $21.08 billion compared to estimates of $20.89 billion with an average revenue per user of $8.52.

Key metrics, such as daily active users (DAU), came in as expected with DAUs of 1.66 billion compared and monthly active users (MAUs) of 2.5 billion.

However, costs and expenses for full year 2019 rose 51% to $46.71 billion compared to full year 2018, and this partly caused the stock to decline. On a quarterly basis, expenses grew 34% compared to the previous quarter.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Net income was up only 7% at $7.3 billion compared to 61% growth in 2018. Net income declined 16% from full year 2018 to full year 2019.

Privacy issues are driving some of these expenses, with over 1,000 engineers working on privacy and a headcount that has grown 26% year-over-year to nearly 45,000 employees.

Guidance also wasn’t as encouraging as analysts had hoped, with Chief Operating Officer, Dave Wehner, stating they expect some deceleration in Q1 compared to Q4’s growth rate on a year-over-year basis.

Facebook’s Product: Move Fast, Break Things

Facebook’s products have inherent issues that are hard to see in the financials. What weighs on the company are not the fines or the privacy regulations, per se, as many tech companies have been able to comply with Europe’s GDPR and California’s CCPA with little impact.

What weighs on Facebook’s stock is that the company’s value proposition to advertisers is they provide the best audience data on the market, which requires tracking people on mobile devices and browsers.

Perhaps one of the more important notes on the earnings call was the release of a new statistic, “Family Average Revenue per User,” which will divide revenue by total users across Facebook, Messenger, Instagram and Whatsapp. Wehner confirmed the company would no longer share Facebook-only stats by late 2020, which implies the company expects Facebook to be weaker than Instagram in the long-term.

As of now, Facebook is stronger than the family suite with $8.52 ARPU versus $7.38.

The term “Family Average Revenue per User” is a bit misleading because Facebook has a product called Audience Network that is not included in these statistics. Facebook’s Audience Network is an ad exchange that brokers ads and collects data across many applications that Facebook does not own.

Advertisers on Audience Network place the ad through Facebook’s news feed even though the ads often don’t appear on Facebook or Instagram. This is one example of how tracking users is engrained in Facebook’s products. (On a side note, the word Family can hardly apply to any ad exchange with this level of ad serving which extends to 40% of the top 500 apps that Facebook does not own and 1 billion+ users that are outside social networks).

Mobile software, called software development kits, are powerful enough to detect your activity across the other applications on the device. Advertising companies also use pixels as you browse the web.

As I had pointed out nearly two years ago, the untangling of this data collection will not be easy nor cheap.

If regulations or reputation issues truly force Facebook to build privacy into the products, then Facebook won’t be quite the cash machine that it is today. For instance, Facebook’s average revenue per user in the United States is at $41 ARPU in the United States and $7 ARPU globally compared to Snap’s $2 global ARPU and Pinterest’s $1 ARPU. This premium that Facebook charges comes from having more data on their users that extends beyond the data collected in Facebook’s family of apps.

There were a few fissures in this earnings report and on the earnings call that show the effects that privacy changes can have on Facebook’s products. For instance, Google and Apple have begun to limit Facebook’s tracking across browsers and operating systems, which is what I described would happen when many thought privacy was a temporary issue.

“First the recent regulatory initiatives like GDPR and now CCPA have impacted, and we expect will continue to impact our ability to use such signals. Secondly mobile operating systems and browser providers, such as Apple and Google, have announced product changes and future plans that will limit our ability to use those signals ...”

Q4 2019 Earnings Call: https://s21.q4cdn.com/399680738/files/doc_financials/2019/q4/Q4'19-FB-Earnings-Call-Transcript.pdf

What’s Next for Facebook

We’ve seen Facebook attempt to pivot away from ads and data collection with Oculus Rift, the augmented reality headset acquisition for $2 billion, and Libra, the cryptocurrency project that dissolved. Facebook may have a chance to reinvent itself with the upcoming launch of Whatsapp Pay. This is a nod towards WeChat’s WePay, a popular method of payment in China through the popular WeChat social network.

Moving forward, Facebook will need to rest on the strength of its applications, rather than on the data collection methods the company has used outside the Family of apps to collect audience data. The company certainly has impressive levels of cash to accomplish this.

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i