Facebook Stock: A Permanent Change To The Business Model

April 20, 2022

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Apr 14, 2022,11:41pm EDT

When a company has an earning miss, the first thing I try to determine is whether the cause of the earnings miss is due to something transient or if it’s due to a permanent change in the story. If the miss is temporary and the market deeply penalizes the company, then there could be substantial alpha. However, we do not think that is the case with Facebook given the company’s guide for 3% to 11% growth next quarter. Instead, we believe Facebook faces a permanent change to its business model.

Below, we discuss the nuances of Facebook’s ad model compared to other mobile ad players and how we came to predict nearly three years ago that Facebook faced insurmountable issues with its product Audience Network. In 2018, we stated the revenue generated from Audience Network was between $5 billion to $10 billion. Fast forward three years, management is stating “the impact of iOS overall as a headwind on our business in 2022 is on the order of $10 billion, so it’s a pretty significant headwind for our business.”

In a series of seven articles including this one on Forbes “Advertising Stocks Face New, Major Challenge with Apple’s iOS 14”, I discussed why third-party data was a significant source of revenue for Facebook despite the company not breaking this out in their earnings reports. Facebook’s business model is fairly complex in how the company collects data, which is why investors are not able to differentiate why Facebook will see a permanent change to its business model while other companies that are dependent on mobile revenue will not.

Below, we go into more detail as to what is unique about Facebook’s business model causing this permanent change following the iOS updates, and why the revenue headwinds could actually exceed $10 billion.

Please note: My firm, the I/O Fund, will hold a one-hour special webinar and Q&A for investors who would like to know more on Thursday, April 21st at 6 p.m. Eastern. Follow me here for more details.

Summary of IDFA Changes:

We want to provide a quick summary on Apple’s IDFA changes for the context of the article. For a more in-depth look, reference my previous analysis here.

The IDFA is a number tied to the device that allows ad exchanges to track user interactions and behavior. The primary function is very similar to cookies in that it helps ad companies store data profiles and preferences for personalized messaging, regardless of which device you are logged into. In addition to targeting, the IDFA also helps with attribution and measurement.

Apple’s IDFA enables the following: user tracking, marketing measurement, attribution, ad targeting, ad monetization, programmatic advertising including DSPs, SSPs and exchanges, device graphs, retargeting of individuals and audiences. Unlike cookies on the web, where there is a tag on the browser, mobile identifiers have much stronger tracking capabilities.

What investors may not realize is that advertising cash machines are largely dependent on tracking software for the high CPMS (cost per thousand views) and CPIs (cost per install) they charge because they can track actions on a granular level even days after a mobile user has seen an advertisement. The mobile users are not aware they are being tracked by many companies they do not have a first-party relationship with (but the developer or publisher does). These developers and publishers must now obtain permission. Without permission, the inventory on mobile becomes less valuable.

Apple Owns the Real Estate

The changes were originally set to take effect in September of 2020 and this was extended to September of 2021. We had covered for MarketWatch in 2019 in an editorial “Governments can’t stop Google and Facebook but Apple Can” that governments had made futile attempts to rein in Facebook’s data collection, but Apple was certainly capable of curbing Facebook and making a serious dent on their business model. In the simplest terms, this is because Apple is the real estate owner. We wanted to make it crystal clear that the market had likely become complacent with near-daily headlines on privacy, but that Apple’s iOS changes were not something to underestimate.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Here is what we wrote in 2019 before Apple had announced plans to remove the IDFA:

“The only force that can stand up to the complex tracking methods used by Google and Facebook will be an opposite, yet equal, force. It will not come from governments, which think that paying for search results is the problem. Rather, the problem is the pervasive code and software that continually tracks people, which no competitor can compete with.

Turns out, there is an opposite and equal force in magnitude that has chipped away at the anti-competitive tracking that occurs in the browser with Intelligent Tracking Prevention (ITP). Yet it has not done so on the leakiest device of all: mobile. And that would be Apple.”

We repeated this in 2020 for Forbes when we said:

“This is a problem for the ad industry because it goes well beyond personal sentiments and niceties around privacy and slow-moving government regulations and pits tech giant against tech giant in the black box world of ad software, user tracking and engineered loop holes. There is little question who will win as Apple goes up against Google, Facebook and many others. After all, its Apple’s device, Apple’s operating system and Apple’s app store. The only question is why this hasn’t happened sooner.”

Given that Apple delayed the release of the IDFA changes, we reiterated (again) that we believed Apple’s changes were a reason for investors to stop the music and pay close attention:

“We think when Big Tech goes up against Big Tech, that investors should watch the outcome closely. Our stance for the past two years is that Apple owns the real estate on iOS, and everyone else is renting […].”

We provided the following statistics to support an upcoming Facebook miss. Primarily that models were suggesting a 7% decline if 20% of iOS users opt-in and Flurry had stated about 20% were opting in. Meanwhile, according to Bloomberg, some agencies were reporting that companies went from spending “nearly all” of their budget on Facebook to more around two-thirds or half of their budget due to the iOS tracking changes.”

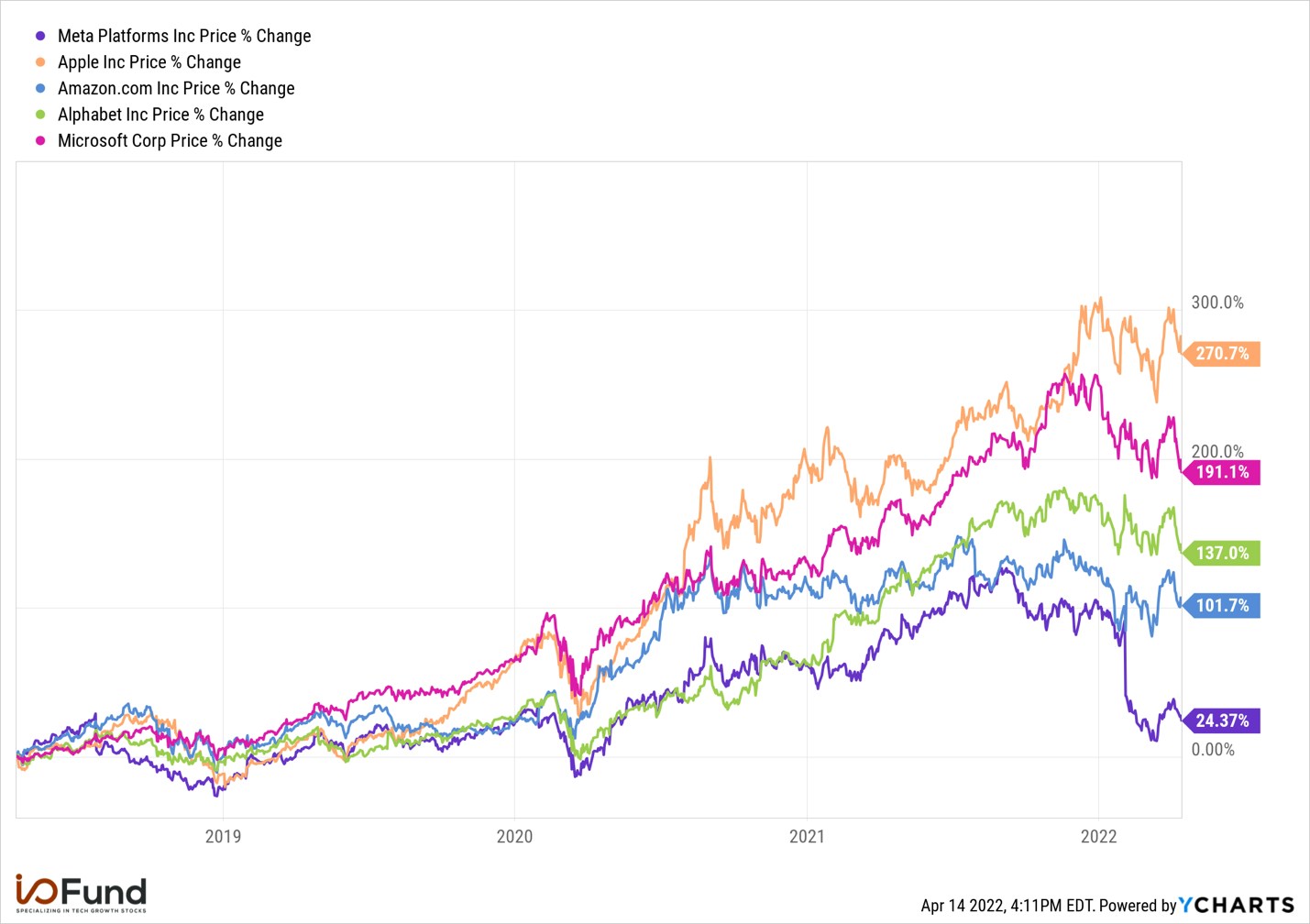

Pictured Above: Since the time of my first analysis that Facebook would stumble in April of 2018, other FAAMGs have returned nearly 4X to 10X more. Compare this to the 448% returns from Facebook in the previous five years (2013-2018). - I/O Fund

Notably, Google is a large real estate owner too and Facebook mentioned in their most recent earnings call that “search ads could have access to far more third-party data for measurement and optimization purposes than app-based ad platforms like ours” – meaning, Google will fare the changes quite well.

Audience Network and Third-Party Data

Facebook is not unique in making the bulk of its revenue from mobile ads as it’s joined by companies such as Unity, Snap, Twitter, Pinterest, Spotify, Tik Tok and more. However, there are key differences to how Facebook generates high ARPU compared to these other mobile applications.

Audience Network is unique in the advertising world as it mixes together first-party data and vast amounts of third-party data to broker ads outside of Facebook’s applications. In this case, the reason Audience Network is unique is because Facebook is able to mix data from its 2 billion users to broker ads across 40% of the top 500 apps on the market. Unity and The Trade Desk play similar roles on the supply side and demand side, but they do not mix first-party data as a publisher with third-party data as an advertising platform. Audience Network blurs these important lines on how data is used (notably, Google does too, and Twitter/MoPub).

The last time Facebook reported Audience Network numbers, it served advertisements to over 1 billion people per month at the end of 2016. To compare, Instagram had 500 million users in 2016. This also means Audience Network reached twice as many people as Whatsapp at time of acquisition, which was valued at $19 billion with 484 million users.

Here’s a statement issued by Facebook on Audience Network’s reach in 2016: “We talk about reaching a billion people every month, and these are real people," said Brian Boland, VP of publisher solutions at Facebook. "We're not talking about cookies or browsers or devices or ID, where one person can look like six things. We're talking about legitimately 1 billion people that can be reached on the audience network."- Q4 2016

When I estimated the revenue of Audience Network to be $5 billion to $10 billion in 2018, I was based this on Google monetizing 2 million websites and 650,000 apps for $17 billion in third-party network revenue. Yet, Facebook Audience Network has a larger reach on mobile than Google’s ad network. This is why MediaPost put FAN’s value at $5 billion by 2020 without websites.

Why Audience Network Could Have a Bigger Impact than $10 Billion

The number one thing to understand about Facebook moving forward is that the company enjoyed peak conditions for its data collection practices, but those days are gone. The mobile device is especially leaky in terms of data compared to browsers and Facebook was able to capture a moment in time when that data was freely collected, even by third-parties (in Audience Network’s case, Facebook is an unauthorized third-party).

There are two major impacts that limiting third-party data can have on Facebook. The first impact is accounted for in the $10 billion headwind discussed by CFO David Wehner, which is that Audience Network is rendered useless without proper attribution and measurement. The second impact is that Facebook will have to work with weaker data for their ads on their own properties, as well, which means investors must answer this question: what will Facebook’s ARPU be when targeting is not informed by vast amounts of third-party data?

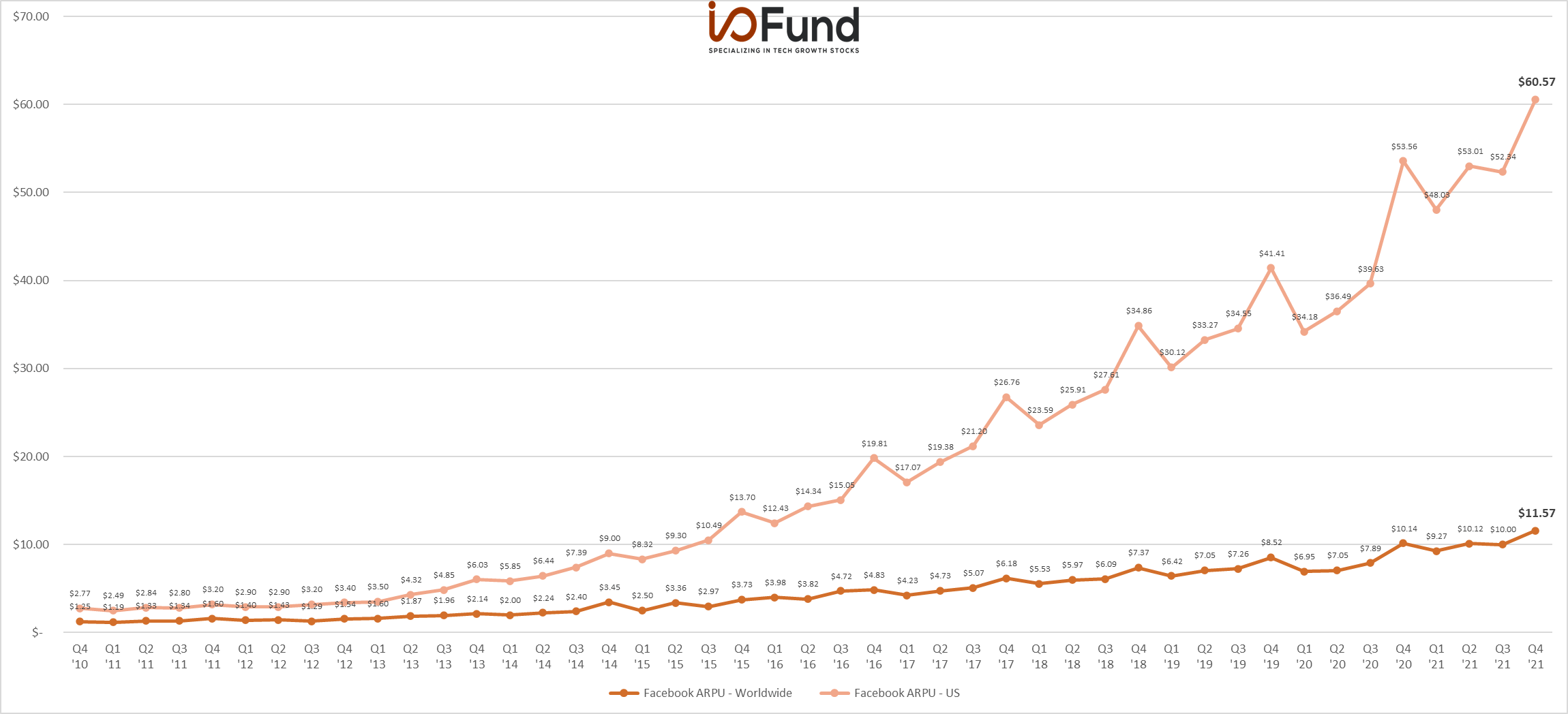

Facebook’s ARPU graph - I/O FUND

If you look at the graph above, you’ll see something began to change for Facebook’s ARPU around the year 2016. Interestingly enough, user growth on Facebook flatlined a while back and yet average revenue per user skyrocketed.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

In the 2016 earnings calls, Facebook also warned of ad load issues due to limited real estate in social networking apps. Despite the limited amount of real estate a social media app has to work with, and flat user growth in the United States and Canada, we see that North America ARPU had some sort of catalyst in 2016 that changed its trajectory.

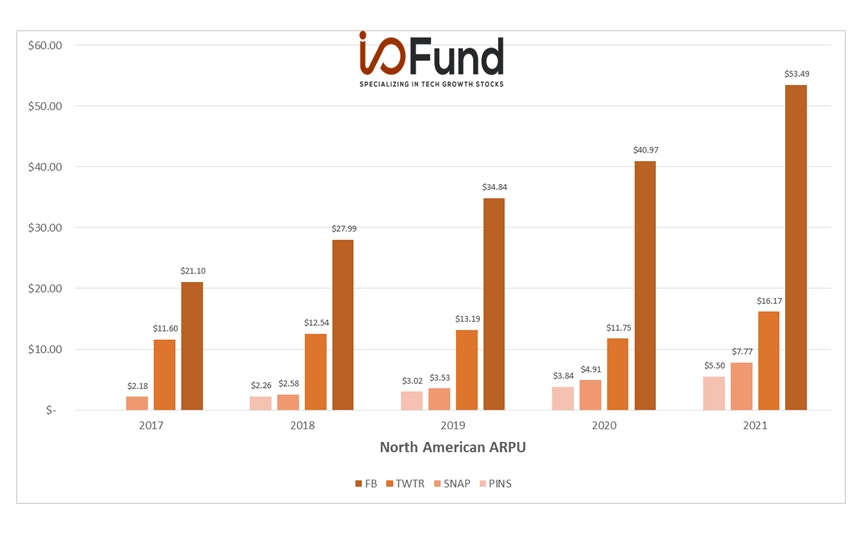

North American ARPU - I/O FUND

The unusual trajectory that began in the United States and Canada in 2016 has led to outsized ARPU compared to other social media apps. I believe some of the unusual ARPU growth pictured above was supported by Audience Network as the ad network can help eliminate ad load issues. In 2016, Audience Network had scaled to the 1 billion user mark and beyond.

During this time, Facebook doubled the number of advertisers from 3 million to 6 million. It’s true that Facebook has 2 billion users but the far majority are located outside the United States. If we narrow down United States users, which are at 193 million, then it makes little sense that Facebook is able to monetize at such a higher ARPU. Snap has 92 million users in the United States. The only difference in business model is the third-party data, which has now been eliminated.

Please note: we are not predicting a beat or a miss on Facebook’s Q1 earnings report. The I/O Fund clearly plays the long-game with our theses as we first covered this three years ago. However, we believe ARPU erosion will occur over time and will be irreversible unless there is a new catalyst.

What Facebook’s Management Said

Facebook is guiding for sales of $27 to $29 billion in Q1, or growth of 3% to 11%. The company stated the first quarter is impacted by headwinds to both impressions and price growth with iOS changes mainly affecting price growth.

In the earnings call, when asked for clarification on the $10 billion impact, Facebook management stated the following: “Yes, Mark, on the headwind, we're just estimating what we think is the overall impact of the cumulative iOS changes to where 2022 — our 2022 revenue forecast is. So if you kind of aggregate the changes that we're seeing across iOS, that's sort of the order of magnitude. We can't be precise on this. It's an estimate. We've got ranges on the impact to our business. So we think it's a substantial — the substantial headwind to work our way through.”

Management also stated there’s “a clear trend where less data is available to deliver personalized ads” and that “Apple created two challenges for advertisers: one is that the accuracy of the ads targeting decreased, which increased the cost of driving outcomes, the other is that measuring those outcomes became more difficult. These challenges are complex and interrelated.”

Despite Facebook stating they have advertiser tools, such as aggregated event measurement, the company still expects “the overall targeting and measurement headwinds to moderately increase from Apple's changes and from regulatory changes in Q1 and throughout 2022.”

In contrast, after stating advertisers would need to adopt new tools in Q3, Snap went on to report Q4 revenue growth of 42% to $1.29 billion.

Conclusion:

In the same year that we predicted Facebook would stumble at the share price of $219, we also predicted that Nvidia would become an AI leader at the share price of $160. If you put your money into Nvidia at the time of our coverage instead of Facebook, the returns would be 420% compared to 28%.

We firmly believe that knowing product provides a substantial edge to tech investing and this is one example of where nuances are critical to getting in front of the market. On that note, we believe there are substantial tailwinds for a handful of ad-tech companies due to IDFA changes as now first party data is more valuable ever.

The adage that “your loss is my gain” is certainly true in the competitive industry of ad-tech. The $10 billion+ that Facebook has stated they will lose from Apple’s changes will migrate somewhere. We will discuss further where we think the ad dollars could migrate to in an upcoming webinar on April 21st at 6:00 p.m. Eastern. Follow me here for more details.

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i