Google And Facebook Stock: Is Weak Ad Demand Priced In?

April 18, 2020

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Apr 13, 2020,01:14am EDT

Facebook, Google and Twitter have warned that Q1 is going to be lower than originally forecast. Media analysts have also weighed in with a consensus that ad demand will be weakened this year. Meanwhile, little has been provided for future guidance, which will test the belief that the effects of the Coronavirus has been priced in.

There is no doubt that many of these companies will have a comeback. The timing of this relies on many factors, especially consumer spending, which is intricately tied to unemployment. In other words, ad demand will return but the path may be as the fickle the advertisers who fuel the industry.

First, the Good News for AdTech stocks …

Usage across mobile and over-the-top television has been skyrocketing. Facebook reported an increase of 50% in messaging in countries where the coronavirus was hit the hardest. In Italy, there was 70% more time spent across apps. This was reported on March 24th and one can only imagine what the United States’ usage has been over the past few weeks as some of this usage falls into the second quarter. Group calling increased over 1,000% - which is no surprise for anyone work-from-home trends. (I wrote a full length analysis on Zoom Video here).

Pinterest delivered some positive news this week stating first-quarter sales and user growth were better than expected. The company stated first quarter revenue will be between $269 million to $272 million. Monthly active users in Q1 of 365 million to 367 million are well above the consensus of 352.7 million users.

Along with its social media peers, Twitter reported an increase in total monetizable daily active users (mDAU) of 23% year-over-year and an increase of 8% quarter-over-quarter.

Over-the-top media usage has also received a lot of attention from investors and for good reason. With more people spending time indoors, nearly every application has increased its footprint. Total streaming hours were up 24% between March 1st to March 16th from a year ago, according to Comscore, with Roku and Amazon up 16%.

According to a survey from Consumer Technology Association, 26% of American households started using online streaming services for the first time during the coronavirus pandemic. Meanwhile, 48% are watching streaming services more often than before.

Live TV is also benefiting from the surge in usage with viewership up 102% from a year ago across the seven channels surveyed.

Now, the Not-So-Good News for Adtech Stocks …

Typically, an increase in usage is linear with an increase in ad revenue. It makes sense that the bigger the audience, the more ad space (especially on mobile) and the higher the ad rates. In this rare quarantine situation, however, major advertisers have closed for business, are reporting layoffs and cutting costs in unison, leading to lower ad spend despite the increase in eyeballs.

There is simply no frame of reference for the effects a quarantine can have on advertisers. As of now, we only have reports that skyrocketing usage is not correlating to more ad spend.

Twitter has stated first quarter revenue will be down compared to the year-ago quarter after the company pulled guidance. In the press release, the company stated, “the near-term financial impact of this pandemic is rapidly evolving and hard to measure.”

This means Twitter could see a loss of 10-15% of revenue from its previous guidance of $825 to $885 million despite mDAU being up 23%. This is calculated based on the company stating revenue will be down slightly from the year-ago quarter, which was $786 million.

For a frame of reference, Twitter reported 21% growth in mDAU in Q4 which correlated to 11% increase in revenue. This further supports impact for Q1 falling in the the 10-15% range if “revenue is slightly down” year-over-year.

Mark Shmulik of Bernstein raised his price target for Twitter to $29 from $27 while stating he is on the sidelines partly due to concerns about Twitter’s ability to monetize its active user base. According to MarketWatch, Shmulik recently stated “We caution about placing too much stock into engagement as (1) everyone has seen a spike in engagement (2) unclear what happens to engagement levels post-COVID, and (3) it’s valueless if you can’t monetize.”

Facebook did not offer many details in their release other than to state “we don’t monetize many of the services where we’re seeing increased engagement, and we’ve seen a weakening in our ads business in countries taking aggressive actions to reduce the spread of COVID-19.”

According to LightShed partners, 12 of the top 50 advertisers are ailing auto makers; another 11 are quick-serve restaurant chains. This matches channel checks by Needham that showed lower spending in travel, retail, consumer packaged goods and entertainment, which represents 30 to 45% of Facebook’s total revenue.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

MarketWatch recently covered the revised analyst estimates on the outlook for Facebook, including statements from Needham and a variety of analysts. Q1 is being revised from $18.56 billion to $17.99 billion with EPS of $1.95 revised to $1.85 a share, according to FactSet as of April 6.

EMarketer released data showing a decline of $20 billion in ad revenue. As Twitter pointed out, the situation is evolving rapidly and this estimate is already insufficient as the data was collected up until March 6th, prior to San Francisco and New York going into a quarantine. The data also did not take into account the Olympics being postponed until 2021.

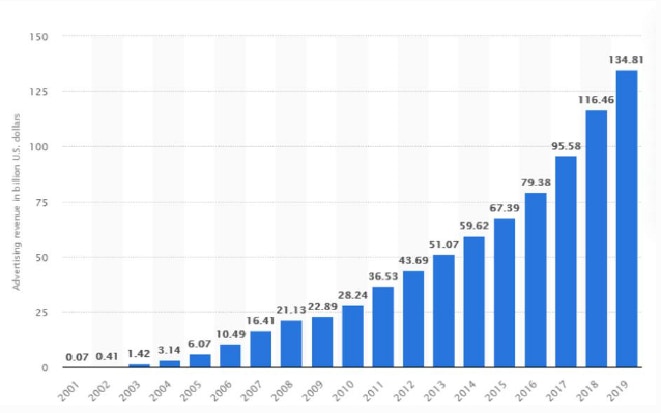

Cowen & Company estimates Google and Facebook will see “$44 billion in worldwide ad revenue evaporate.” This reflects a 18% decline in revenue for Google and a decline of 19% for Facebook compared to Cowen’s previous forecast. Cowen believes the ad business will bounce back in 2021. In a trickle-down effect, Cowen predicts Twitter will also see a decline of 18% and Snap a decline of 30%.

If Cowen’s forecasts are correct, this will be the first time that Google and Facebook will report negative revenue year-over-year since the companies were founded in 2001 and 2004, respectively. Google’s annual revenue last year was $160.7 billion with Cowen currently forecasting $127.5 billion this year in revenue. Facebook’s revenue last year was $69.66 billion with Cowen forecasting $67.8 billion for the upcoming year.

Google and Facebook have plenty of cash, yet smaller ad-tech companies may be more exposed to the spiraling effects of losing business rapidly.

Snap has not released a formal statement in regards to guidance but there’s evidence the company is not entirely insulated. In support of Cowen’s estimates, some of Snap’s largest advertisers are exposed to reduced ad spend, such as movie and media brands Disney, Comcast and AT&T, and also consumer brands Coca-Cola and Hershey’s.

Roku is harder to determine as the company generates revenue from ads and also licensing fees and/or commissions from other content apps. Most analysts believe the lower ad demand will not offset the other segments with a forecast of 15% decline this year. Michael Pachter of Wedbush lowered estimates for Roku’s average revenue per user (ARPU) from 30% to 21% in Q1 and from 40% to 26% in Q2. For the rest of the year Pachter sees a recovery with FY20 only decreased from 24% to 20%.

Notably, LightShed pointed out that digital ad spend will see the effects more immediately while television ads will see more of the effects in Q2. This is because advertisers make commitments to buy from big TV networks months in advance.

Conclusion:

In my opinion, the situation is hard to quantify. We are on the brink of earnings reports, where more will be revealed, yet these earnings will show minimal impact as ad spend was likely reduced only at the end of the quarter in March.

Next quarter is where the majority of the effects will be felt. If companies decline to provide forward guidance, which seems to be the trend thus far, the market will have to rely on sell-side analysts for guidance. I think this is a disadvantage as companies have a more sobering outlook.

For instance, JP Morgan is predicting 23% GDP growth in Q3 of this year, yet Apple is rumored to be delaying the 5G iPhone release in September. This information does not line up. Similarly, ad-tech companies must consider that revenue growth and earnings growth will require travel, sports, restaurants and consumer packaged goods returning to their former state of a 10+ year economic boom. In other words, JP Morgan has the liberty to withdraw bold predictions as the situation evolves while tech companies cannot so easily release new information.

I personally believe we will not see ad spend return to pre-Coronavirus levels until 2021 at the earliest and 2022 at the latest. Many advertisers are under extreme conditions of balancing a lack of demand for their products, furloughed work forces, and will need to hoard cash to sustain the recovery period until demand returns.

As of now, there is an undeniable red flag in ad-tech as usage is not linear to revenue. This has not occurred in the history of any ad company currently only on the market. The next three months will split the market into two camps: those who believe the market has “priced in” the full effects of the Coronavirus and those who believe there is too little information to price and predict the length of the recovery.

No camp is right or wrong, we simply haven’t been here before.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i