Pinterest Stock: Price-to-Sales Risky

May 16, 2019

Beth Kindig

Lead Tech Analyst

Despite Pinterest’s stock climbing from its initial public offering last month, analysts are expecting a first-quarter loss of 16 cents a share, adjusted, compared to a 10-cent loss in the year-ago quarter. With that said, analysts are expecting revenue of $197 million, reflecting growth of 50%, however there are discrepancies between the user base that is growing and the user base that is monetizing, which is what is causing the losses.

Last month, I wrote an article on how mobile application companies hide user attrition and how Pinterest and Snap bury important key metrics in 10-Ks and S-1 filings. One thing I stated is that financials in tech companies can be misleading when not accompanied by scrutiny of the underlying business.

The key metrics to watch for when evaluating Pinterest stock include monthly active users (MAU), daily active users (DAU) and average revenue per user (ARPU). I’ll review some information here from my last analysis before I go into why Pinterest is seeing an increase in revenue yet a slight decrease in net income.

Pinterest Stock: Company Struggles to Monetize International Audiences

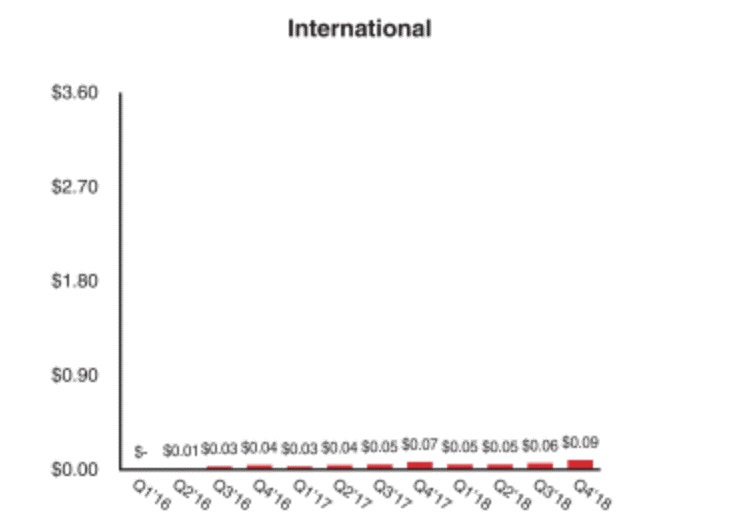

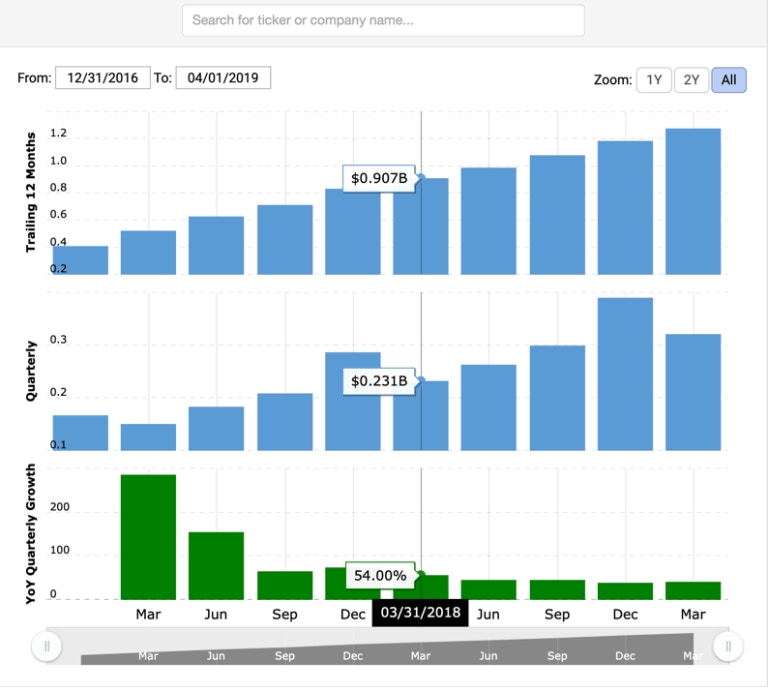

Thus far, Pinterest has struggled to monetize global users. The difference in average revenue per user (ARPU) in the United States compared to the global users is astonishing – and uncommon for social media. We see the United States users monetize at $9 average revenue per user while the international users monetize at a mere 25 cents per user. This is what the graph looks like:

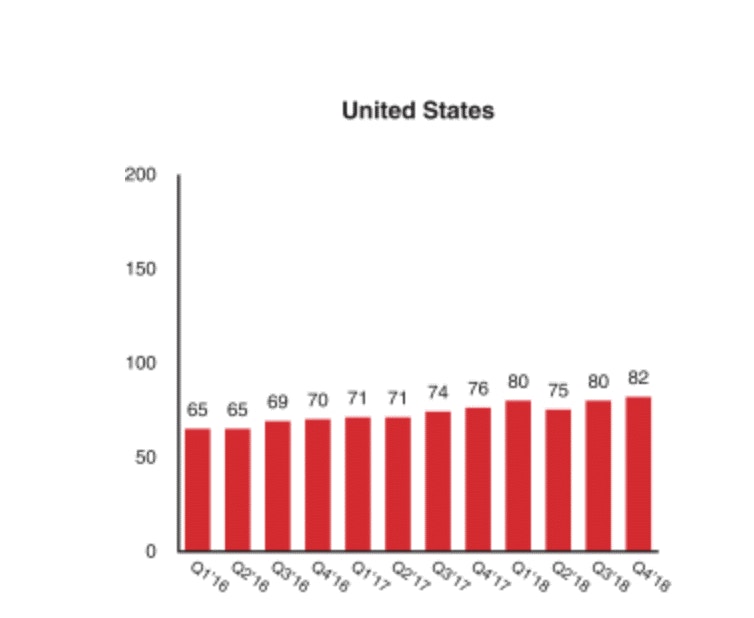

The user growth in the United States shows saturation in previous quarters with flat to declining growth between Q1 2018 to Q4 2018. This means the areas where there actually is user growth (international) does not contribute to profits as the costs of operations likely exceeds 25 cents per user annually. Facebook’s international ARPU is currently at $7 and has never been below $1.50 as a public company even with the stock struggled in 2012. Twitter has seen below $1 international ARPU as reported in 2017 but was also hovering at 5 price-to-sales during some of this time period compared to Pinterest’s 20 price-to-sales (more on this below).

Meanwhile, Snap which is a more direct comparable as both companies are newer to the public markets, shows nearly 1500% more ARPU in the Rest of World region. Yes, you read that right – 1500% with 9 cents from Pinterest ROW compared to $1.24 ROW.

This helps complete the issues Pinterest faces globally as the user growth is coming regions which result in losses. I believe this may be the culprit as to why Pinterest is expected to post 50% revenue growth yet slightly higher losses from -10 cents per share to -16 cents per share. You’ll see below that the United States has stagnated.

According to data from Apptopia, a provider of app intelligence that partnered with Bloomberg in February, Pinterest downloads in Brazil surpassed United States downloads for the first time on Android. This gives us a glimpse as to where the user growth is coming from; which are regions that create a loss.

The information above means investors are doing one of the two:

- Betting the United States will monetize higher than $9 per user

- Betting the global audience will monetize higher

My best guess is that number one is likely to occur while number two will present a challenge. The issues here are surmountable and we may see some progress here in the next earnings report; however, I do not believe we will see enough from this quarter’s earnings to justify Pinterest’s stock price due to the flat United States base and the lack of revenue coming from the international base. This leads me to ask how overpriced is Pinterest stock?

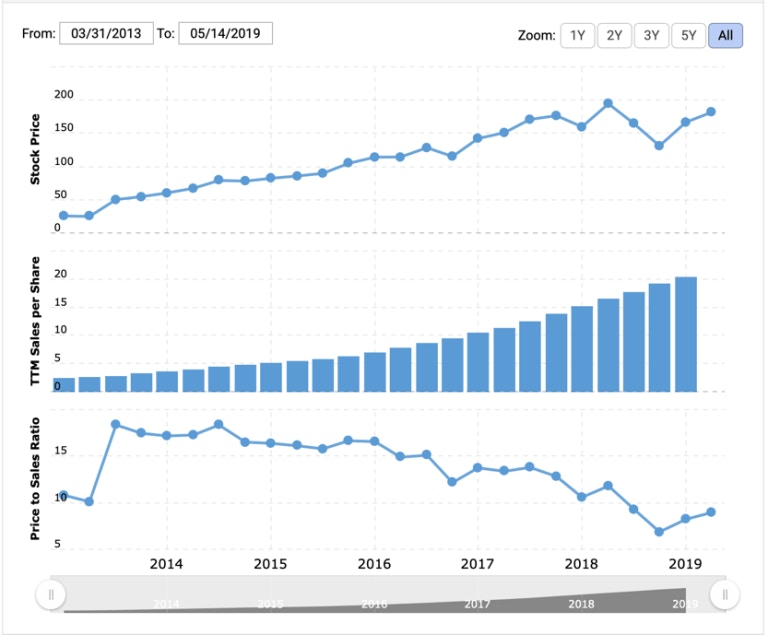

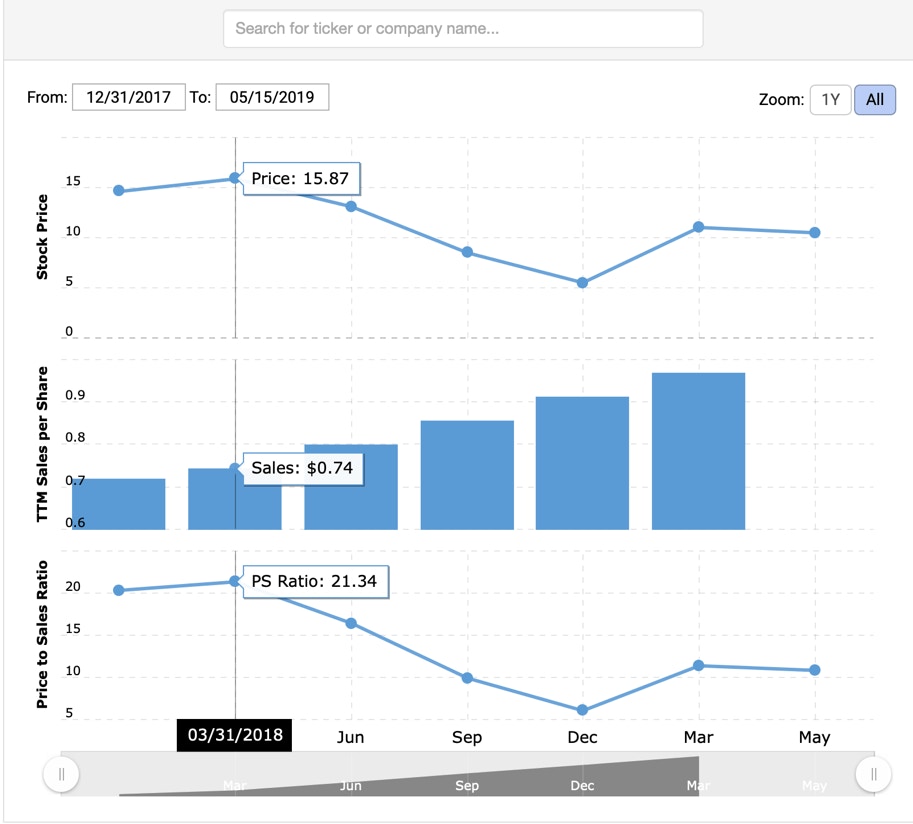

Pinterest Stock Trading 30-50% Too High

Pinterest’s IPO stock price was originally $15-$17 and went public at $19. My analysis points to this pricing being correct while the current trading price of $28.50 at time of writing is 30-50% too high due to the constraints of social media valuations.

With total revenue at $775 million in 2018 and a market cap of about $15 billion, Pinterest stock is at a 19.3 price to sales ratio. When adjusted for 50% revenue growth this quarter, Pinterest will have about $100 million more in revenue for the past twelve months, which puts the price to sales at 17.14 – if the price remains the same. If investors run up the price after earnings due to revenue growth, we will be right back where we were with a 19 or 20 price-to-sales ratio. This will be on revenue of about $197 million with 50% growth same-quarter YoY.

Meanwhile, Facebook is at 8.8 price-to-sales with 26% same-quarter YoY revenue growth at $15 billion per quarter, Twitter at 8.8 price-to-sales with 20% same-quarter YoY growth on $787 million quarterly revenue and Snap with 39% same-quarter YoY growth on $320 million quarterly revenue at 10.8 price-to-sales.

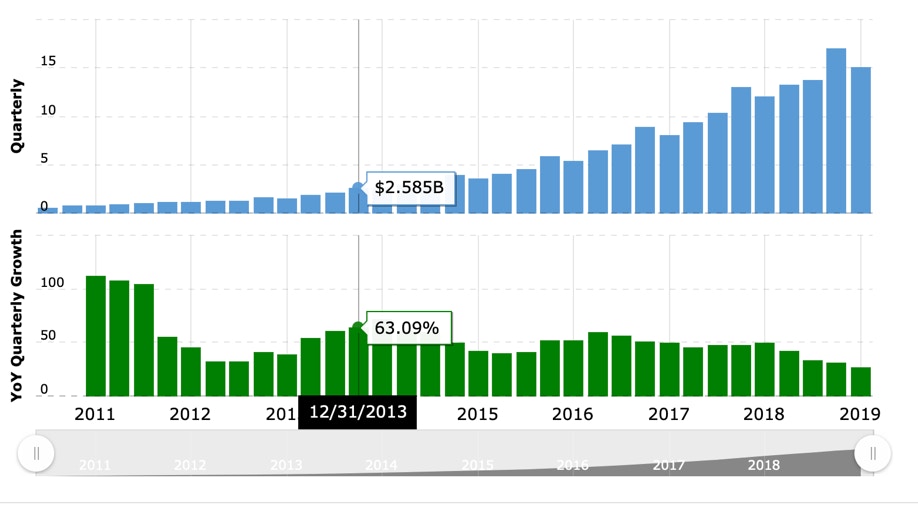

Historically, Facebook did trade at a price-to-sales above 15 between 2013 and 2016, however, we see that the time period when Facebook was able to command a price-to-sales above 15 was when the company had crossed 1.2 billion monthly active users and was growing towards 2 billion monthly active users. At that time, the company posted 63% YoY growth with $1.5B to $3.0B in profits. With this user base, Facebook is an outlier. Pinterest’s stock is a better comparable to Twitter and Snap with all three social media companies having users in the 270-325 million monthly active user range, with Pinterest being the smaller user base of all three.

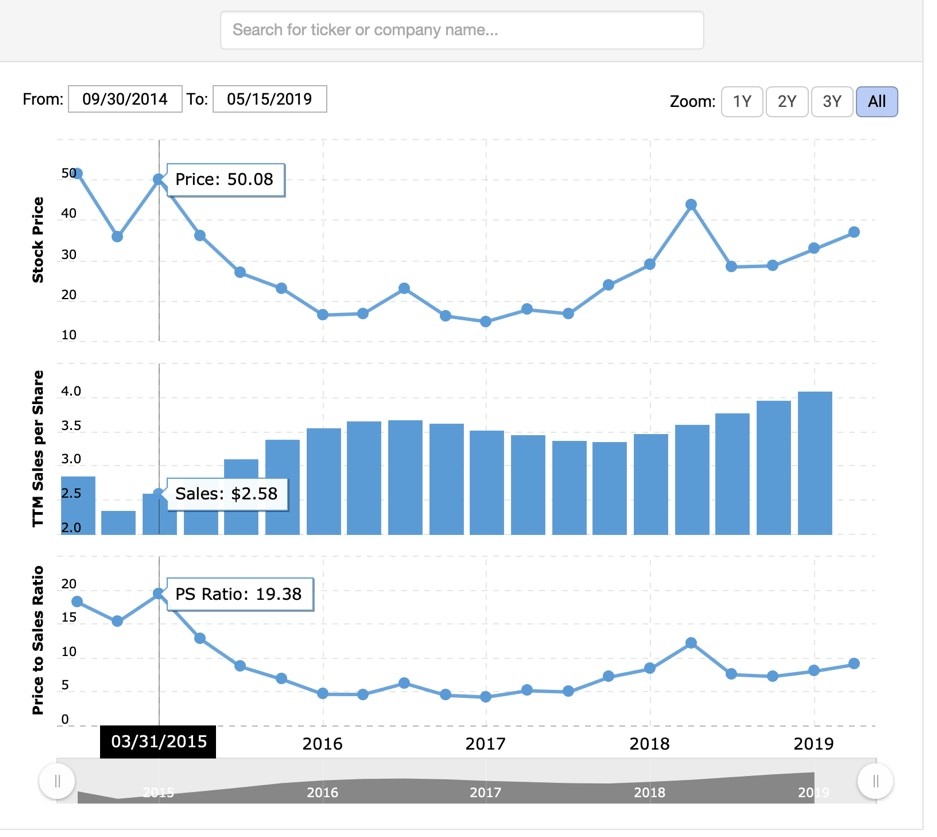

Twitter’s price-to-sales history has also been at a high price-to-sales ratio over 15 when posting over 75% growth (Pinterest is expecting growth at 50%). Even with solid growth, Twitter’s price-to-sales did not last long at the 15-20 range and the price was down nearly 50% within two quarters. The second time Twitter tried to get above 10 price-to-sales in early 2018, the price again corrected the following quarter to below 10 price-to-sales.

Snap has met a similar fate of having a short-lived price-to-sales above 15 before correcting to 10 or below where it has been for the last few quarters. Again, the correction in price-to-sales happened despite Snap reporting 50% YoY quarterly growth.

Takeaway: Do you remember Twitter at $50? Snap at $20? Pinterest at $28-$30 is kinda like that. Social media companies with a 10 or higher price-to-sales ratio have not fared well in the immediate quarters that followed with both Twitter and Snap seeing their value cut in half when reaching the price-to-sales where Pinterest is at today.

The market has created a valuation that will be hard for Pinterest to live up to. Pinterest priced correctly at the IPO as I believe the price should be in the $15-$19 range as this would be in the reasonable 8-10 price to sales range. Even if Pinterest beats expectations and we see a bump up in price, I stand by my analysis that the stock’s price-to-sales is 30%-50% too high – and the valuation will be short-lived.

More To Explore

Newsletter

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i

Google TPU v8 vs Nvidia: How Inference Is Rewriting the AI Market

In April, Google announced it would begin selling its TPUs to select third-party data center operators, which is something the market has anticipated for nearly a decade. The TPU-versus-Nvidia-GPU deb