I Predicted Facebook Would Miss Q2 Earnings: Here's What Investors Need To Know For Q3

July 27, 2018

Beth Kindig

Lead Tech Analyst

This is a crucial time to point out to investors that my predictions were correct. Last April, I published an in-depth analysis on Seeking Alpha along with predictions for Facebook (FB) stock. The analysis urged readers to ignore post-Cambridge Analytica hype as Facebook’s quarterly earnings would miss as a result of GDPR. Specifically, I stated the culprit would be revenue and data sources outside of the Facebook “family of apps.” However, with this article, I’d like to explore this point even further and explain with granularity why the issues have only begun and what Facebook isn’t telling you (source for Facebook earnings report: NASDAQ).

Tech companies are complex, especially as it relates to data science, and it’s unlikely a financial analyst or hedge fund whose expertise is in finance understands what exactly Facebook does with data and how this impacts average revenue per user (ARPU) or future earnings.

There’s more to Facebook than a “family of apps” which is causing confusion in the markets.

Have you heard of Audience Network? As an investor, it’s essential that you know what this is. Facebook makes money off third-party websites and applications through a platform called Audience Network. This is an advertising network, which powers advertisements to 40% of the top 500 applications. This is indicative of Audience Network’s overall presence in the mobile app market of approximately 40%. While it is well known in the mobile industry as the most dominant ad network in the mobile market, don’t be surprised if you’ve never heard of it.

Facebook Inc. doesn’t like to talk about Audience Network. You’ll be hard pressed to find any mention of it in their SEC filings or on earnings calls. Even among advertisers, who pay billions of dollars into Audience Network, the ad platform is notorious for its lack of transparency and is known to be a black box.

And, it’s a very profitable black box. The last time Facebook reported Audience Network numbers, it served advertisements to over 1 billion people per month at the end of 2016. That’s more than Instagram today, and this incredible base should be more like 2 billion in 2018 assuming it followed the same trajectory of adding 1 billion users every 2 years (Audience Network was launched in 2014).

With Audience Network, advertisers see 16% more reach on average globally than on Facebook and Instagram alone, and a 12% increase in website conversions with Facebook and Audience Network combined.

What could possibly have more reach than Facebook or Instagram?

Whoa – higher reach than Facebook and Instagram? And higher conversions? And all of this to over 1 billion people outside of Facebook’s “family of apps”?

Why is Audience Network so widely used in the mobile industry? Because it’s augmented with proprietary data from Facebook’s social apps. In order to power ads across hundreds and thousands (maybe even millions) of applications at a higher conversion than the world’s best advertising platforms (Facebook and Instagram) would require using data in ways that you would never want your users to find out about.

My newsletter subscribers get this information first. Sign up here.

I mean, what Facebook user would want their private information brokered to hundreds of applications to power advertisements in websites and applications that they didn’t authorize or have relationships with? From the backlash we saw after Cambridge Analytica, I’m guessing not many would like this.

Let me stop because this is where a lot of confusion begins. I’ll give you an example as to how this works. Let’s say you buy items from the retailer Target (NYSE: TGT) every week. Maybe you buy toilet paper, dish soap and laundry soap. How would you feel if Target used that data in a partnership with Hulu or NBC or CBS to show you advertisements later on your television? That evening, Hulu or NBC or CBS would start to show you toilet paper ads and laundry soap ads based specifically off your private purchases and information shared at the cash register.

Target would make a lot of money if they brokered your private cash register data – but they don’t. Apple (NASDAQ:AAPL) has been very upfront about the billions of dollars they have opted to not make by keeping data private. This is what Tim Cook is referring to. Investors should know that it’s very, very rare for a company to risk the customer relationship in this way.

Meanwhile, Facebook is doing this across hundreds and thousands of applications using private data shared in what should be a privileged customer relationship. Not only that, but Facebook takes your private data from application partners (in this fake example, that would be Hulu, NBC or CBS) – so now they know what you were watching that night – but you never gave consent for any of this.

Data collected from the Audience Network software development kit (SDK) installed in iOS and Android applications continues to enrich Facebook proprietary data sets and drive up cost per impressions on advertising and average revenue per user. This business model of being a “data-broker-and-ad-network-without-consent-and-for-profit-beyond-social-media” is where some of the fallout from Cambridge Analytica began to occur. But this is miniscule compared to the data exchange (dare I say, data leakage?) through Audience Network.

Ethics aside, what investors need to know about Audience Network is that it violates some important regulations put into place by the GDPR as data is being used by both partners in ways that are explicitly without consent (Facebook users have NO IDEA how their private data is being used beyond the “family of apps.” On that note, investors don’t either because all Facebook ever talks about on earnings calls is the “family of apps” – never referring to Audience Network by its name).

The applications who share data with Facebook are at risk and Facebook who brokers proprietary data with partner applications are at risk if they continue this practice. In 2020, these regulations will also go into effect in the State of California. Facebook will have to slowly wean Audience Network out of existence or face major fines. As this weaning takes place, the revenue earned from 40% of the top 500 apps (plus more) will slowly dwindle.

How Much Are We Talkin’?

Quite a few people have asked me to estimate the value of Audience Network. I want to be clear that Facebook has provided very little information here. While the exact number of how much Audience Network is impossible to predict with pinpoint accuracy (insert: lol) the important thing to understand here is that the average revenue per user will drop on Facebook social because they will no longer store data and use that data from partner applications.

One reason there is limited information is that Facebook runs Audience Network ads through their Newsfeed feature, and therefore, uses this loop hole to count the revenue as Facebook revenue. This is very misleading to not provide transparency. Compare this to Alphabet which clearly discloses third-party websites and application revenue as a separate line item in their SEC Filing of roughly $17 billion per year.

Here’s one of the only statements issued by Facebook on Audience Network’s reach:

“We talk about reaching a billion people every month, and these are real people,” said Brian Boland, VP of publisher solutions at Facebook. “We’re not talking about cookies or browsers or devices or ID, where one person can look like six things. We’re talking about legitimately 1 billion people that can be reached on the audience network[2].”-Q4 2016

This means Audience Network is larger than Instagram today (Instagram has 800 million users). This also means Audience Network was 2 times larger than Whatsapp at the time of acquisition when Whatsapp had 484 million users – enough to claim the largest acquisition price tag in history of $19 billion.

This is how I estimated the net value at $5 billion minimum up to excess of $10 billion net to Facebook (after 70% revenue share with publishers).

- Audience Network serves approximately 40% of the mobile apps on the market today which means Facebook likely monetizes every person with a smartphone (i.e. over 3 billion people rather than the 2.2 billion on Facebook social apps). Plus, they monetize this 3 billion many times over across unlimited inventory.

- Google monetizes 2 million websites and 650,000 apps for $17 billion in third-party network revenue. Facebook Audience Network has a larger reach on mobile than Google’s ad network and the SDK could be in up to 2 million iOS and Android applications (figuring 40% of applications).

- Facebook warned of ad load issues due to limited real estate in social network apps in earnings calls in 2016, however the exact opposite happened. Revenue skyrocketed and Facebook doubled the number of advertisers from 3 million to 6 million. This growth would have been supported by Audience Network as the ad network would eliminate ad load issues. Facebook added $23 billion in annual revenue since warnings of ad load. A large portion of this would have been supported by Audience Network alleviating ad load.

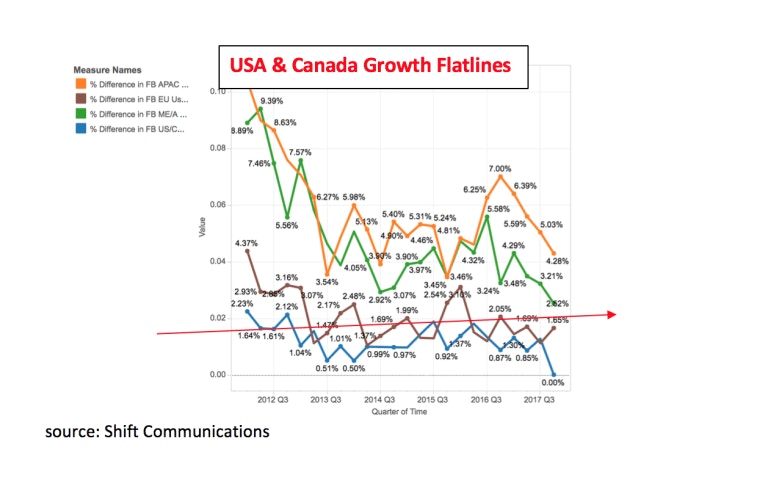

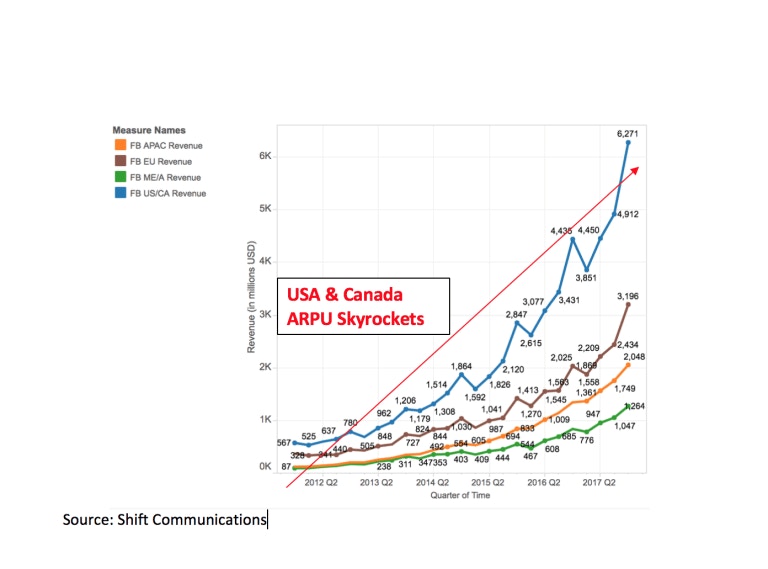

Most importantly, Facebook does not have to net anything off Audience Network in order to increase average revenue per user on its own social media apps. Growth in the United States and Canada flatlined a long time ago, meanwhile the ARPU (average revenue per user) skyrocketed. Data extracted from Audience Network would have substantially contributed to this ARPU growth. This is essential for investors to understand.

Therefore, any ARPU made after the warning of ad load issues in 2016 and 2017 are questionable as the enriched data and targeting capabilities from Audience Network likely contributed to this ARPU growth.

Images from Shift Communications can be found here

Additional Considerations for Facebook’s Q3 Earnings:

- User attrition and slowing user growth has been occurring for some time in the United States and Canada, yet earnings previously remained strong with ARPU climbing to $26 per user in these coveted markets. Therefore, a small user attrition of 1 million European Users from a base of 2.2 billion monthly active users is not why we are seeing the first revenue miss with Facebook executives warning of more decline to come. To believe the stock dropped because of infinitesimal decimal point user attrition is a dangerous theory propagated on earnings calls because your next thought will be whatever revenue lost from the Facebook user base could easily be made up by Instagram or one of the other “family of apps.” If you believe this storyline, then you will continue to hold onto this stock without having all of the information.

- The other Facebook domain properties such as Instagram, Whatsapp, and Oculus should be ignored for now. Yes, Instagram has potential but this is not what you are investing in when you buy Facebook stock. It is sheer speculation and if Instagram was a standalone company, you wouldn’t be paying these stock prices. You bought Facebook, Inc and to hype up Instagram as the central business model in 2018 is senseless.

- First-party data uploaded to Facebook by advertisers has weakened. The GDPR has a trickle-down effect by weakening the data advertisers upload to the Facebook newsfeed. This reduces the targeting power and the CPMs they can charge. I made this point in my Seeking Alpha article that “many brands will undergo the same regulations as to how they obtained their data.” In addition, Facebook is shutting down the self-serve tool that allows advertisers to import data from third-parties. This will also continue to erode earnings.

Conclusion:

Investors cannot expect transparency from Facebook executives. This company has better trained actors than Hollywood (sorry, but true). There are many instances in prior earnings calls where they purposely covered up revenue sources, such as Audience Network, in order to keep Wall Street confidence high leading up to these quarterly earnings (I’m working on a follow up article citing these specific omissions). They played down the impact of the GDPR and have omitted third-party mobile applications and websites revenue from SEC Filings. It is nearly impossible to evaluate the stock with what little information has been provided by Facebook, Inc.

But remember, this is a company that has misled the general public, Congress, and most importantly their users on important facts about their business model and revenue streams – especially that they use the data from Facebook across a huge network of applications and websites without authorization from their users. Quite simply, investors have been caught in the cross fire of Facebook’s attempts to cover up privacy issues with their users.

While the drop yesterday was “startling” for investors caught unaware, my readers on Seeking Alpha and beth.technology were fully informed with insider knowledge as to the underlying forces which are at play with Facebook, Inc and mobile advertising. You can subscribe to my newsletter here.

Any information or analysis contained herein and published or referenced elsewhere should be appropriately credited to Beth Kindig of beth.technology

This article appeared on Seeking Alpha.

More To Explore

Newsletter

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s