Hybrid Work Is Here To Stay And Asana Will Be A Key Beneficiary

December 22, 2021

Beth Kindig

Lead Tech Analyst

Hybrid Work Is Here To Stay And Asana Will Be A Key Beneficiary

December 17, 2021, 11:47am EST (originally published on Forbes)

Hybrid and work from home environments are a fundamental tailwind for cloud-based tools that help facilitate this key micro trend. Due to the inherent benefits of hybrid/remote environments, such as decreased fixed expenses (rent) and increased access to global talent, along with the necessary infrastructure in place from the rise of cloud computing, this trend will gain momentum going forward.

Asana is one of the key cloud-based tools that facilitates efficient hybrid work environments and stands to benefit from the structural shift underway that is transforming how people work. Asana is a work management platform that helps teams orchestrate work across an entire enterprise, connecting teams around the globe in an easy-to-use platform. The thesis is fairly easy: do you think workers will go back to being in-office full-time? If not, then more cloud-based tools will be required to perform work efficiently. Notably, these tools were already rising in popularity prior to Covid based on the efficiency factor alone.

Customers use Asana to improve team collaboration and workflow management, helping teams track their progress on projects, assign tasks and responsibilities to employees, set deadlines and keep a record of data related to their work. The company was founded in 2008 by Facebook executives Dustin Moskovitz (co-founder of Facebook) and Justin Rosenstein in 2008.

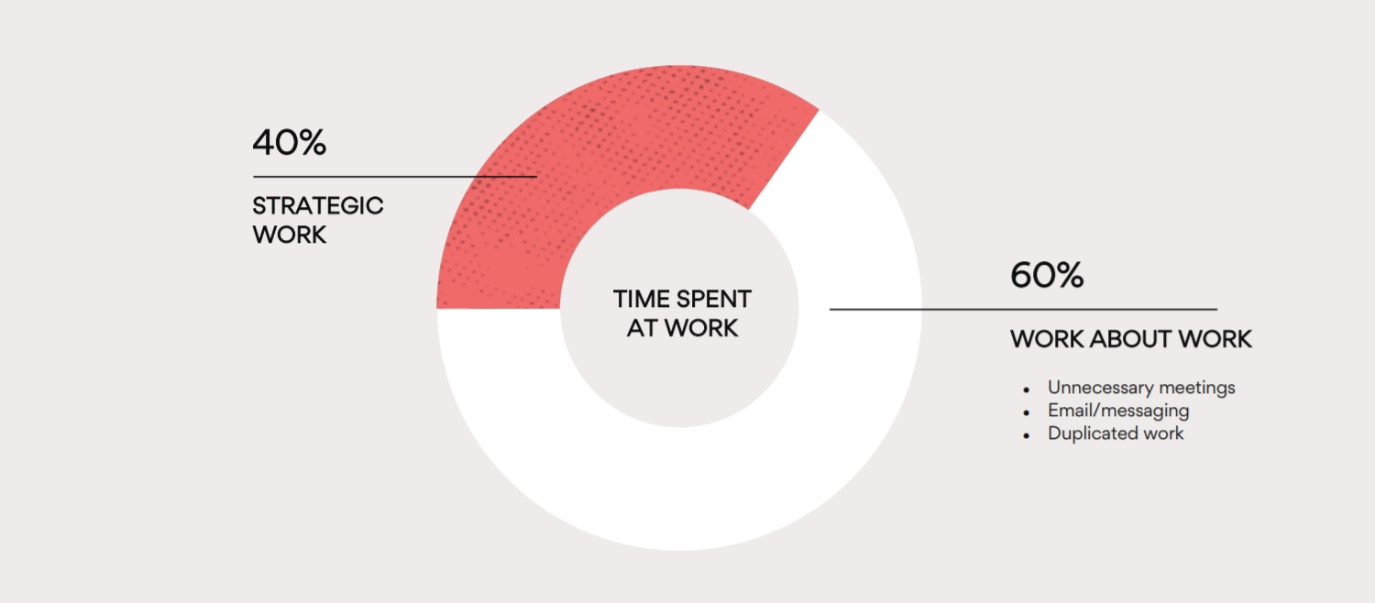

The two had worked together at Facebook and experienced firsthand the coordination challenges the company faced as it rapidly scaled its business. The two realized that they were spending a significant amount of time trying to figure out who was responsible for what, essentially creating ‘work about work’. This unproductive bottleneck inspired them to create a product that would help organizations coordinate their work.

One of the company’s main focuses has been to increase employee productivity by helping them focus on priority tasks and avoid distractions. Asana has been used by a wide range of companies for multiple uses, such as product launches and marketing campaigns. It helps its users know in real-time what each member of the team is working on and allows managers to easily check project progress to ensure that tasks are completed successfully and on time.

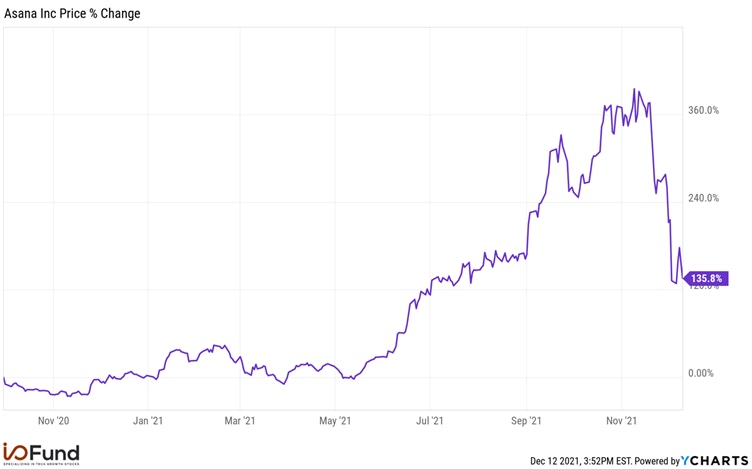

With the rise of remote work environments, Asana’s solutions have experienced rapid growth and demand for its solutions has been especially strong with enterprise customers. Asana went public via a direct listing in September 2020 and the company’s stock is up about 135% since its listing and had gains of about 390% during its peak a month back. Despite the recent pullback in Asana’s stock price, the company remains well positioned to continue to gain share in the rapidly growing work management market (i.e., same story a month ago at a discounted price).

Hybrid-work-from-home will be the future working environment for many organizations, with 73% of employees wanting a flexible remote work option. I am bullish on this micro trend and believe that companies in this space will continue to grow going forward. Asana is a beneficiary of hybrid work environments, evident in its exceptional strong revenue growth, which recently accelerated to 70% in the most recent quarter. The I/O Fund noticed Asana’s rapid growth earlier this year and took a position, realizing an 85% gain in under a month.

Asana, at the time, was quite undervalued based on their expected growth, so we initiated our 1st buy in February at $40. We decided to ride the volatility in Asana in March, and instead looked for breakout, which manifested in May when we added again at $33.25. We became fully allocated in Asana on May 20th, and set our targets above. We trimmed this position 3 times, locking in gains between 65%, 115%, and 224%. We closed the position on November 8th for a 285% gain. Recently, we started accumulating again in the $70s and again in the $60s.

We still like Asana at the I/O Fund, however it’s a position we decided to actively manage rather than buy-and-hold. It could turn into a buy-and-hold but for now requires a more active stance. In the article that follows, I discuss Asana’s market opportunity, product roadmap, financial performance, competitive landscape, and key risks that investors should be aware of.

Market opportunity

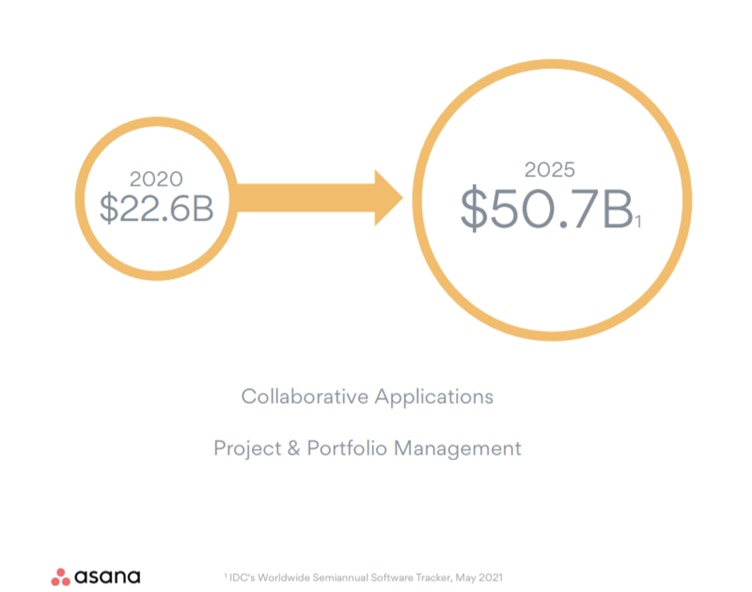

The company operates in a large market that is rapidly expanding. According to Allied Market Research, the team collaboration market size is expected to grow at a compounded annual growth rate of 13% for the next decade and reach a total addressable market of $27 billion by 2027. Furthermore, Grand View Research estimated that the global productivity management software market was $43 billion in 2020 and is expected to grow at a CAGR of 14% from 2021 to 2028. In Asana’s recent presentation, they estimate that their total addressable market for workplace solutions will be nearly $51 billion by 2025.

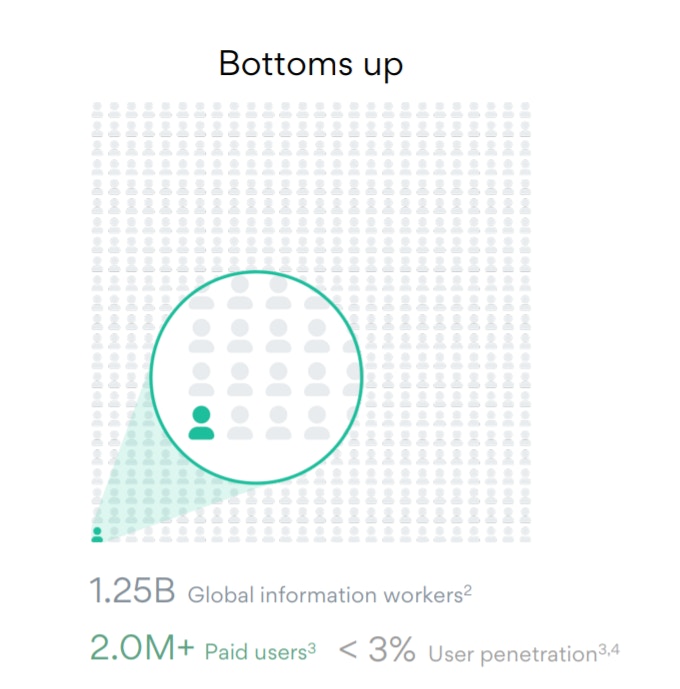

To give a sense of the large market opportunity in front of the company, a recent Forrester Research report estimates that there are about 1.25 billion information workers that would benefit from using Asana’s solutions. The company believes that it is still in the early innings of its the market opportunity and estimates that its market penetration is less than 3% of its addressable population of information workers. Looking forward, there is ample room for Asana’s topline to continue to expand as more information workers take advantage of work management solutions.

Product Roadmap

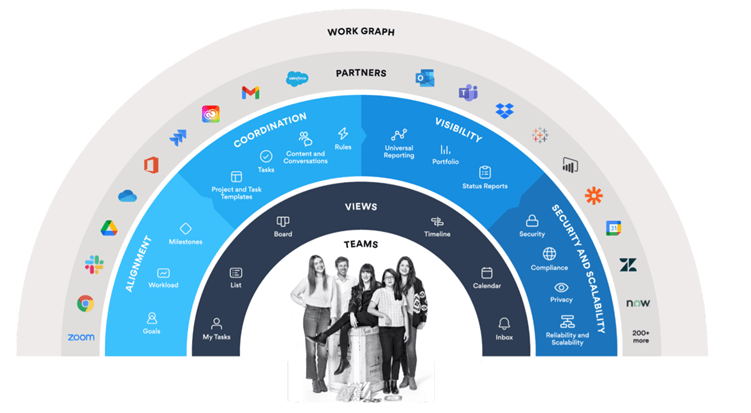

The company’s platform is built on its proprietary, multi-dimensional data model that it calls the Asana Work Graph. It has features like boards that allow users to easily create tasks for the team, view what other team members are working on, and create different views like calendar list views. Furthermore, the timeline feature allows decision makers to quickly learn the status of a task, who is responsible for executing the work, and helps reduce redundancies.

There are also reporting tools that provide key information about work, such as files, comments and metadata. The result is that Asana helps teams collaborate across an entire organization and ensures that projects are completed on time and efficiently. Asana’s benefits compound in large, complex hybrid work environments such as large enterprises, which I touch on in more detail below.

Another key advantage of the Asana platform is that it has integration capabilities with major apps, such as Microsoft Teams, Okta and Dropbox. These integrations and partnerships with other cloud-based tools help further facilitate the transition to hybrid work environments and improve efficiencies.

With the rising number of information workers who are increasingly working remotely, Asana’s products help employees coordinate core projects, improve productivity across the enterprise and remove information silos that have historically separated teams across an enterprise. Asana’s solutions also yield a solid return on investment for its customers. According to a study conducted by the IDC, respondents reported that Asana has increased organizational efficiencies by reducing time spent on emails by 33%, improved process execution by 42%, and has yielded a 224% 1-year return on investments for its customers.

Asana has also partnered with numerous technology firms to add more features and functionality to its platform. A standout that management highlighted during the Q2 earnings call was Zoom’s integration within Asana. This unique feature allows Asana customers to create a Zoom meeting while they are performing a task directly inside the Asana platform. Once the Zoom meeting is over, the Zoom recording and the transcript can be added to Asana and tasks discussed during the meeting can be assigned to owners. This functionality improves the efficiencies of meetings and helps reduce the amount of time spent “working on work”.

As mentioned above, work complexity compounds as organizations increase in size and become more dispersed with hybrid work environments. Asana’s Work Graph helps reduce the growing complexity for enterprises and replaces micro-management with macro-management, “by aligning [leaders] around key objectives and the work needed to achieve them no matter where they are in the world” (Q3 Earnings Call). We can see the success that Asana has had reducing hybrid complexities by observing growth trends with large enterprise customers, which have accelerated recently. I discuss this trend and Asana’s financials in more detail next.

Financials

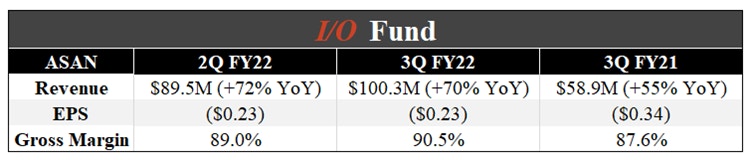

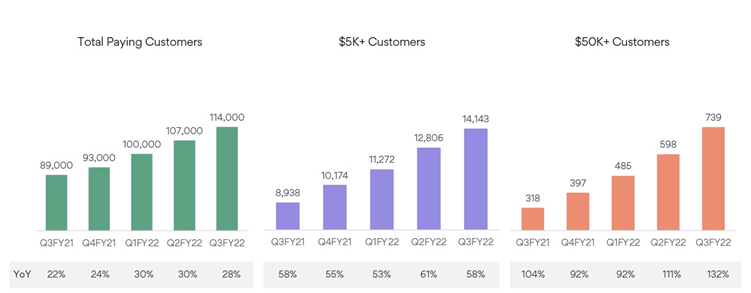

Asana released its Q3 FY2022 results on December 02, 2021, which beat both on the top and bottom-line. Revenue growth accelerated to 70% YoY and quarterly sales were $100 million, which beat analysts’ estimates by $6 million. Revenue has increased sequentially for at least 11 consecutive quarters and Asana now has an annualized topline run rate of over $400 million. The growth was led by strong customer metrics as total paid seats surpassed 2 million and total paying customer increased 28% YoY to 114,000.

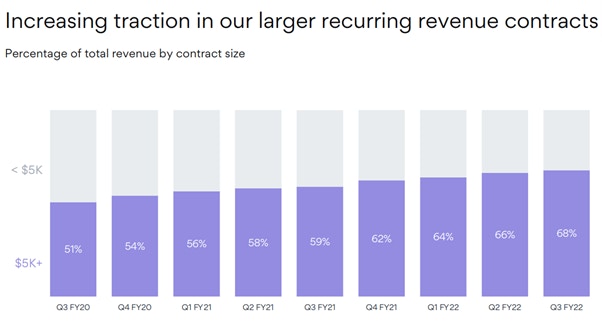

However, the real story is Asana’s success with enterprise customers, which generally pay more and sign longer-term contracts. Because of this, enterprise customers are generally the most valuable type of customers for a software provider. Asana’s success with this cohort speaks to the overall value that its workplace solutions provide.

For example, while total paying customers increased 28% YoY to 114,000, customers spending $50,000 or more per year (enterprise customers) grew by 132% YoY to 739. This represented an acceleration from the 111% and 92% YoY growth rate in enterprise customer count in Q2 and Q1 FY2022, respectively. The accelerating growth in enterprise customer count highlights the benefits that Asana provides to large, complex hybrid environments. Further highlighting this strength, Asana’s dollar-based net retention ratio for enterprise customers was 145%, up from 140% in the prior Q3 period and exemplifying that enterprise customers are expanding their usage of Asana overtime, a sign of strength.

Some of the large key customer wins in the quarter included Warner Music Group, which chose the company’s enterprise solutions “to organize, manage and track the end-to-end process of how they identify, evaluate and bring new artists into its various labels faster and more effectively”. Asana also expanded its deal with a Japanese customer, which is one of the largest automotive manufacturing companies in the world. Management explained that the Japanese auto customer’s expanded agreement was to help manage their software and product developments (Q3 2021 Conference Call). These customer wins highlight that Asana is useful across multiple industries and different geographies.

It is noteworthy that while Asana is growing its enterprise customer base, it is doing so on a global scale. This provides support that Asana is still early in its topline run rate and has amble room to expand both domestically and globally. Furthermore, Asana is preparing for global growth as it recently expanded its support to 13 different languages, which will help the company capture customers is numerous markets around the world.

Looking forward, Asana expects Q4 revenue to be in the range of $105 million to $106 million, representing a 53% to 54% YoY growth rate. While this represents a deceleration from recent growth rates, the company is likely being conservative with their topline guide. For instance, management guided Q3 sales to grow 59% YoY (at the mid-point) and actual Q3 sales growth came in at 70% YoY.

Management also expects Q4 adjusted operating loss of $53 million to $51 million and adjusted net loss per share of ($0.28) to ($0.27). This represents a larger loss than the Q3 adjusted operating loss of $41 million and adjusted loss per share of ($0.23). While the guide for larger losses is somewhat concerning, the company is investing to grow rapidly to capture market share in the large, untapped work productivity market. As a result, Asana is front-loading investments today that will pay dividends in the future.

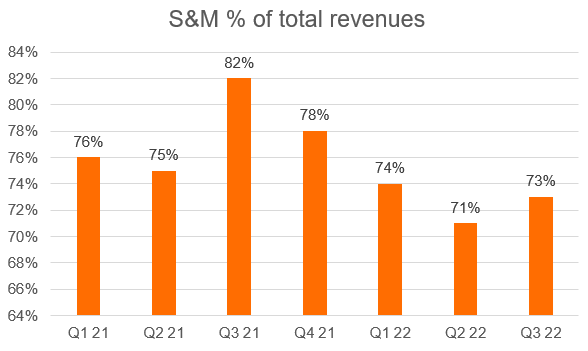

We can see the front-loading of expenses by observing trends in sales and marketing (S&M) expense. As shown below, the company’s S&M expense increased as a percentage of total revenues to 73%, which was up 200 bps QoQ but down 900 bps YoY. Asana’s COO Anne Raimondi explained on the Q2 call that the company has been ramping hiring to support international expansion. Specifically, she stated that the company has been “increasing sales and marketing capacity across all of these new offices and regions. So, lots of hiring to support our customers”. Ultimately, I am not concerned with the rise of S&M expense margin since the company is investing in its future growth, which will help the company quickly scale its operations, improving both earnings and cashflows in the long run.

Moving to cashflows, quarterly free cash flow was -$30 million as of Q3 FY2022, down YoY from -$20 million for the same period last year. However, YTD free cash flow -$46 million, an improvement from the prior year metric of -$58 million. Cashflows can be lumpy, but as enterprise customers continue to increase as a percentage of total sales, their recurring upfront cash payments will lead to improving cashflows overtime.

Stock-based compensation and insider purchases

It is also noteworthy that Asana pays some of its salaries with stock-based compensation (SBC), which cosmetically improves the presentation of cashflows. For instance, in the latest quarter, Asana issued $26 million in SBC, up from $9 million in the prior year quarter. However, quarterly free cashflow improved $18 million YoY, or $1 million absent the benefit from increased stock-based compensation. The increase in free cashflow after adjusting for the rise in SBC highlights that Asana has been able to leverage its scale to a degree. Nonetheless, cashflows will remain lumpy going forward and SBC growth may outpace free cashflow generation in the near term.

A benefit of rising SBC is that it makes employees owners in the business, giving them a vested interest in the company’s success. This in turn should improve employee retention and lower turnover, which will help Asana better scale its operations as seasoned employees are generally more efficient than new hires.

Management has also been purchasing shares, which can be a sign that management believes that the company is undervalued. For instance, board member Lorrie Norrington recently purchased 3,733 shares on December 6th for a total purchase value of $248,000 (~$66.51/share). This was the second time she had purchased shares this year after spending $199,000 for 6,200 shares in March 2021(~$32.12/share). Ms. Norrington’s purchases follow a drop in Asana’s price following the general tech sell off that occurred in the back half of 2021. Given the company’s continued strength with enterprise customers discussed above, Asana may be at a decent risk/reward right now.

Another insider that has been purchasing shares is CEO-founder Dustin Moskovitz. CEO Moskovitz has purchased over 6 million shares year to date, which is generally a very bullish signal. However, the purchases likely relate to the redemption of a convertible bond that CEO Moskovitz holds in a trust. As disclosed in Asana’s 10Q, the company elected to convert a convertible note that was “held by a trust affiliated with Mr. Moskovitz and the shares were accordingly issued to the trust. The conversion of the Convertible Notes therefore increased Mr. Moskovitz’s voting power”. Nonetheless, the increase in CEO Moskovitz ownership further aligns his incentives with shareholders, which is generally a positive development.

Competition and why Asana is winning

The work management platform space is very competitive and there are numerous public and private companies competing with Asana. Asana’s main publicly traded competitors are Atlassian (Jira) and Monday.com, but they also compete with Smartsheet and other private companies such as Airtable. For the sake of brevity, I will only be discussing Monday.com and Atlassian’s Jira offering and what sets Asana apart from these competitors.

One of the key pillars separating Asana from Jira is that Asana is built for all teams within an enterprise, while Jira was specifically designed for software developers. Asana claims that Jira is not flexible enough to be applied to teams across an entire enterprise, while Asana was built to be applicable to all employees within an organization. However, the two are not mutually exclusive and users are able to integrate the Jira cloud within the Asana platform, brining Jira’s software development focus into Asana’s easy to use workflow platform. This integration allows all employees to remain in sync and helps various teams, such as business and software development, collaborate across the organization. To remain competitive, Atlassian bought Trello in 2017.

Possibly Asana’s most direct competitor is Monday.com, which went public in June 2021. The two are the leading providers of workflow solutions and both are growing strongly. Asana differentiates itself by being easy to use, transparent and user friendly, making it accessible to all users in an organization, even the non-technical ones. On the other hand, Monday.com claims that it is a Work Operating System, that is more advanced and customizable.

Without getting into the differences in the platform offerings, the key differentiator between the two is likely price. Given that enterprise customers are important to both of these companies’ success, and that neither company directly discloses enterprise pricing, I relied on enterprise customer metrics to get a sense of which platform is favored by large organizations.

As mentioned above, Asana’s enterprise customers growth recently accelerated from 111% to 132% YoY growth, the fastest pace of YoY growth in FY2022. Similarly, Monday.com also reported an acceleration in enterprise customer growth, as customers with annualized recurring revenue >$50,000 grew 231% YoY, up from the Q2 growth rate of 226% YoY.

While Monday.com is growing enterprise customer’s faster than Asana, Asana’s enterprise growth is accelerating more rapidly. For instance, Asana’s enterprise customer growth accelerated 2,100 bps in the most recent quarter, versus to 500 bps acceleration for Monday.com.

Moreover, Asana had 739 enterprise customers in the latest period, which was 20% higher than Monday’s 613 enterprise customers. However, Monday.com was founded in 2012 while Asana was founded in 2008, so Asana’s head start may be the reason why Asana currently has more enterprise customers.

Unfortunately, neither company directly discloses enterprise pricing, but Asana did announce that they have some seven and eight figure deals, highlighting how not all enterprise contracts are not the same. It is noteworthy that both companies report high gross margins, with Asana reporting a GAAP gross margin of 91%, which is about 300 bps higher than Monday.com’s GAAP gross margin of 88%. Asana’s higher gross margin suggests that it is not sacrificing price to drive sales growth, which can be a sign of competitive strength, especially given its recent acceleration in enterprise growth. However, both companies have very similar metrics and are valued about the same (Asana’s market cap is $13 billion while Monday.com market is $12 billion as of publication).

The market likely needs more time and information to fully understand who the winner will be in the work management platform space. However, recent trends suggest that Asana may be pulling ahead given its rapid acceleration with enterprise customers and higher gross margins. We are still early in Asana’s growth story, and there are plenty of risks ahead of the firm, which I discuss in more detail next.

Risks:

Asana faces significant competition in the fast-growing work management space and it is not yet clear who the winner will be. Furthermore, larger companies could very well enter the space and compete with Asana’s solutions, possibly turning customers into competitors.

Asana has also experienced rising losses as it scales its business. The company’s operating expenses are expected to be high as it invests in human capital and office space to expand its operations globally. There is also no clarity as to when the company will be profitable, and shareholders may be diluted if cashflows do not improve going forward. Furthermore, the company recently reported a deceleration in bookings growth, which may forewarn a broader slowdown in sales in the near term. CFO Tim Wan addressed this concern during the Q3 call and explained that bookings are not a great barometer for growth, due to the large amount of customers still on monthly billing plans. Since monthly customer do not impact deferred revenue, they skew the calculation of bookings. Nevertheless, bookings growth will need to be monitored going forward since it is an important metric for Software-as-a-Service companies.

Conclusion

Looking forward, Asana appears well positioned to continue to capture share in the work management space. Hybrid and remote work environments are a structural tailwind that will drive demand for work management solutions. Furthermore, these tailwinds will likely gain momentum due to the inherent benefits they provide to both employees and employers. Asana recently reported an acceleration in topline growth, and enterprise customer metrics accelerated even faster. While it is not yet clear who the winner will be in the work management space, Asana appears well positioned given its high gross margins and strong customer metrics. Asana has a large addressable market in front of it and its penetration is very low, suggesting that we are still very early in the company’s growth story.

Royston Roche contributed to this article.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis. The I/O Fund has owned Asana stock in the past and currently owns Asana stock at time of writing. There are no plans to change the position in the next 72 hours.

Follow me on Twitter. Check out my website or some of my other work here.

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per