Q1 Earnings Analysis for Etsy, Square, and Palantir

May 27, 2021

I/O Fund

Team

As earnings season winds down, we review earnings reports for popular growth tech stocks Etsy, Square, and Palantir.

Regarding Etsy, e-commerce valuations have come down as a result of the correction in growth tech, and when compared with other e-commerce stocks that are facing tougher comps, Etsy is showing slowing projected growth of 32% this year.

We also discuss Square, a fintech stock whose topline beat was driven by a surge in Bitcoin revenue. Excluding Bitcoin revenue, the company still reports decent growth of 44%. We look at Square from both perspectives below.

Palantir is guiding for Q2 revenue growth of 43%, but to prove product-market fit, the company needs to show higher growth in commercial revenue. Beth Kindig previously wrote about this in Forbes when she analyzed the product at its IPO.

Etsy:

Like many beneficiaries of Covid-19, e-commerce benefitted from the economic shutdown through an acceleration in revenue. In 2020, consumers spent approximately $861B online with U.S. retailers, up 44% YoY, nearly three times the growth in 2019 at 15.1%, according to estimates from Digital Commerce 360.

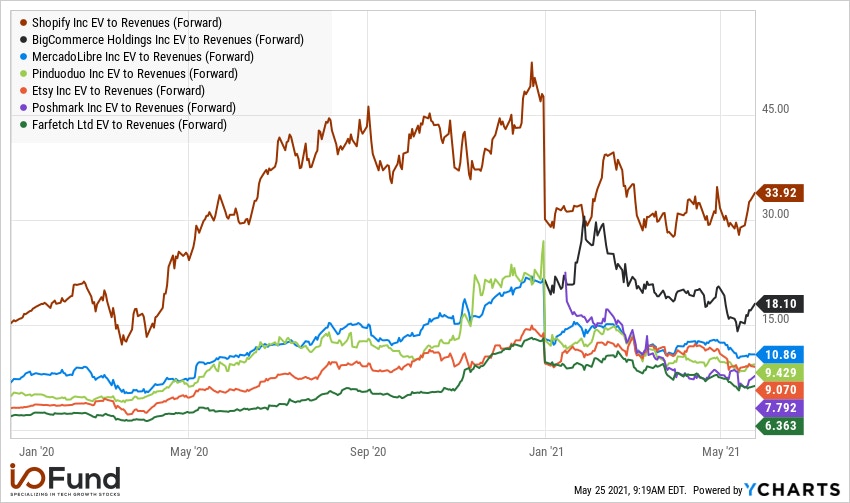

E-commerce valuations peaked for the industry in early 2021 as investors worried about more difficult comps. As you can see from the chart below, Etsy’s valuation peaked at 15x forward revenues, based on data from YCharts. As of May 25, Etsy was trading at 9x forward revenues.

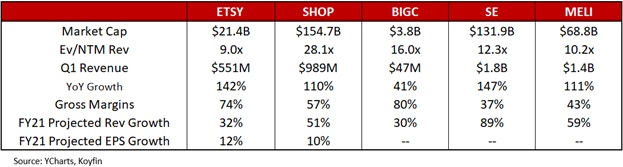

Etsy is projected to show slower revenue growth of 32% this year than popular e-commerce stocks like Sea Limited, 89%, Mercado Libre, 89%, and Shopify, 51%. Etsy is facing noticeable deceleration from its 111% YoY revenue growth in 2020.

Revenue growth for Etsy is on par with BigCommerce, which is valued at 16x revenue versus 9x revenue for Etsy. Meanwhile, Etsy is already profitable with 74% gross margins and projected EPS growth in 2021 of 12%. The company also beat on its top and bottom lines with 141% YoY revenue and EPS of $1.

GMS represents total sales and is an important metric for e-commerce stocks. In Q1, consolidated gross merchandise sales (GMS) for Etsy was up 132.3% YoY to $3.1B, while Etsy marketplace GMS was up 144.1% YoY to $2.9B. Etsy estimates that stimulus payments drove approximately 8% of GMS growth in Q1. In its guidance for Q2, Etsy is estimating consolidated GMS growth of 5% to 15% YoY.

In Q1, the Etsy marketplace reported the highest growth rates for active buyers, repeat buyers, and habitual buyers since becoming a public company, acquiring 16.3M new and reactivated buyers. Active buyers grew 91% YoY; repeat buyers who made two or more purchases in the last year grew 114%; while habitual buyers, the company’s most loyal consumers, grew more than 205%.

Conclusion

Like many e-commerce stocks, in 2020 Etsy benefited from Covid-19 through an acceleration in revenue. The company is now facing tougher comps and is guiding for decelerating growth. E-commerce valuations have contracted, and Etsy is not the cheapest e-commerce growth stock we analyzed above.

As of May 25, Etsy was trading at 9x forward revenue versus 6.36x for Farfetch and 7.78x for Poshmark, which we previously covered. Unlike other popular e-commerce stocks, Etsy is profitable with a gross margin of 74%, and projected revenue and EPS growth in 2021 of 32% and 12% respectively.

Square:

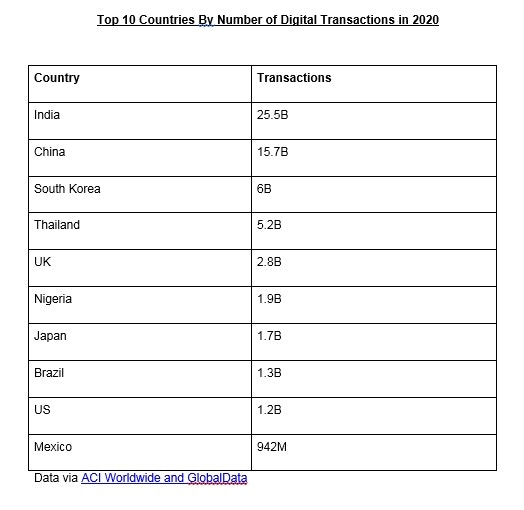

Covid-19 accelerated the trend towards digital payments, with more than 70 million transactions being processed globally in 2020, representing growth of 41% YoY, according to a recent report from ACI Worldwide and GlobalData.

The value of those transactions rose 32.8% YoY to $69T, while the share of digital transactions was 9.8%, up from 7.6% in 2019.

Digital payments are nascent with plenty of room for growth, according to the report.

Digital transactions have a projected CAGR of 12% by 2025, with the fastest growth of digital payments from 2020 to 2025 in Croatia, 374.4%, Columbia, 112.7%, Malaysia 83.9%, Peru, 74.4%, and Finland 71.4%.

North America is expected to be the fastest growing region, with a CAGR from 2020 to 2025 of 36.5%.

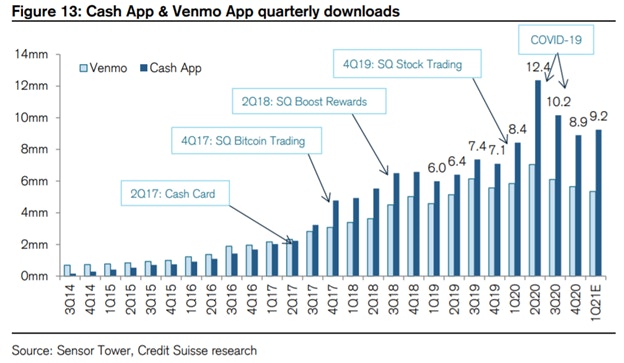

Square, a popular fintech stock, allows users to trade Bitcoin via its mobile application. Square’s Cash App has outpaced PayPal’s Venmo in quarterly downloads every quarter since launching Bitcoin trading in Q4 2017, based on data from Sensor Tower.

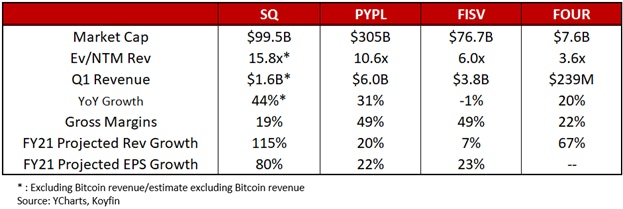

Square reported Q1 earnings May 6, beating on the top and bottom lines, driven by a surge in Bitcoin revenue. Revenue of $5.06B, up 266% YoY, beat by $1.73B. Excluding bitcoin, total net revenue was up 44% YoY to $1.55B.

Cash App revenue was $4.04B, up over 650% YoY, with gross profit of $495M, up 171% YoY. Cash App generated Bitcoin revenue of $3.51B with gross profit of $75 million. Excluding Bitcoin, Cash App generated revenue of $529M, up 139% YoY.

Gross profit grew 79% YoY to $964M. Seller generated revenue of $1.02 billion, up 19% YoY, and $468 million of gross profit, up 32% YoY.

To bring in new customers, last March, Square began offering Cash App users the ability to send Bitcoin for free. During the quarter, Square also integrated Square Loyalty into Cash App, which it says is “a flywheel for seller and buyer discovery, engagement, and retention.”

Square officially launched its industrial bank, Square Financial Services, last March. It is expected to launch business checking and savings accounts, according to a recent report.

Excluding Bitcoin revenue, Square trades at a premium compared to peers PayPal, Fiserv, and Shift4. However, for 2021, Square is projected to grow revenue 115% YoY and EPS 80% YoY, which is higher than other fintech stocks. Gross margins for Square are lower than its competitors, as Bitcoin boosts revenue but reduces gross margins.

Conclusion

Moving forward, Square faces increasingly difficult comps and trades at nearly 16x forward revenue, which is a premium compared to peers and related to its higher revenue growth.

Palantir:

Total commercial revenue grew 19% YoY to $133M, while US commercial revenue grew 72% YoY. Commercial growth was more muted due to the ongoing impacts of Covid-19, including in Europe, according to the report.

Palantir is continuing to make progress on commercial customer growth, according to the report. CEO Shyam Sankar struck a bullish tone, reporting a substantial increase in new leads:

“We see strength and forward looking indicators and customer interest,” he said. “Since the beginning of February, qualified commercial opportunities in the US and the UK are up 2.5 times. Active commercial pilots across the business have more than doubled and opportunities across the US and UK government continue to develop at pace.”

Right now, the closest competitor to Palantir is Semantic AI, a private company headquartered in San Diego, but more competitors are likely being developed in the startup ecosystem. We cover this and more in a previous write-up by Beth Kindig here.

Last April, Palantir demonstrated Apollo for Edge AI. The product is now live and takes a “pioneering approach” to AI using micro models, Sankar said:

“Apollo for Edge AI is the next evolution to transform AI into alpha, enabling customers to train, manage and deploy multiple independently versioned chained models to the Edge with ease,” he said.

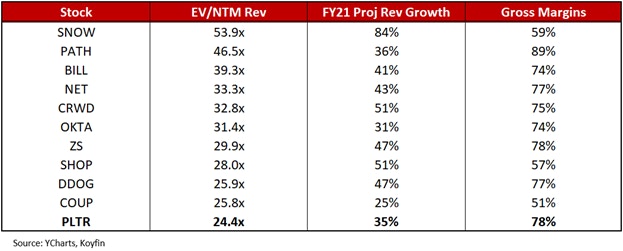

Below we compare Palantir with other high growth tech stocks. While Palantir has healthy gross margins of 78%, projected 2021 revenue growth is lower than growth tech stocks like DDOG, SHOP, and ZS, which also trade at valuations under 30x.

Conclusion

Although Palantir is guiding for revenue growth of 30% or more through 2025, we believe the company will needs to do a lot to execute in the Commercial market against the thriving AI startup ecosystem. However, it may take a few years before AI startups can effectively compete against Palantir. The number to watch will be commercial revenue growth, which was low at 19% this past quarter. Without more growth here, the product may not show signs of product-market fit in the commercial sector.

Disclaimer: The author, Jessica Ablamsky, owns shares of Etsy and Square. The content in this article is intended to be used for informational purposes only. The author has not received any compensation from any third party or company discussed in this article. The content is the expressed opinions of the author and is intended for educational and research purposes. Any thesis presented is not a guarantee of any particular stock’s future prices, so please factor this risk into your own analysis. It is very important that you do your own analysis before making any investments based on your personal circumstances. The author is not a licensed professional advisor. Please seek counsel form a licensed professional before acting on any analysis expressed in this article, to see if it is appropriate for your personal situation.

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per