Out of Favor With Investors, Poshmark Has Long Term Potential

March 25, 2021

I/O Fund

Team

Poshmark sits at the intersection of three key trends: non-new, sustainability, and social e-commerce. A consumer-to-consumer online marketplace for pre-owned items, Poshmark is a fashion-oriented platform that offers apparel, accessories, beauty and wellness, footwear, home goods, toys and games, and a new pets category.

The app makes online shopping social, with a user experience similar to Etsy, Instagram, and Pinterest. Poshmark encourages users to follow each other, and like and share items for sale in users’ closets. It also offers video through Posh Stories, free virtual events known as Posh Party Live, and virtual meetups. Prior to the pandemic, Poshmark also supported in-person events.

As the largest fashion-oriented online C2C marketplace in the U.S., Poshmark’s IPO generated significant excitement. The company initially planned to offer 6.6 million shares at $35 to $39, but due to demand priced the IPO at $42.

In its first day of trading Jan. 14, the stock opened at $97.50 and closed at $101.50, with an intraday high of $104.98. The stock has been falling ever since and reached a new low March 25 when it closed under $39.

Now that the valuation has come back down to earth, Poshmark may offer a good opportunity for investors who believe the future of ecommerce will be social. Below we look at competitors, fundamental, quarterly results, market opportunity, and potential tailwinds.

Ebay Posts Record Growth

To understand the potential opportunity in Poshmark, first we need to look at one of the largest online marketplaces in the world, Ebay. As more shopping moves online, specialized ecommerce platforms like Poshmark are fighting for current and potential Ebay customers.

Founded in 1995, Ebay is the grandfather of the online auction. Like its much larger rival, Amazon, Ebay facilitates B2C and C2C sales through its website and makes money on transactions. Unlike Amazon, which has strict guidelines around used items, sellers can list almost anything on Ebay.

But it has faced stiff competition from a new generation of online marketplaces that cater to niche interests, including public companies like Poshmark, Mercari, and The RealReal, which encourage users to clear their closets to make extra cash.

In the universe of private companies, there is also a platform for every niche, from gently used children’s apparel on Kidizen to used tech on Gazelle.

After years of declining growth, Ebay may have turned a corner last year. Due to tailwinds from Covid-19 and the resulting economic lockdown, the company reported double digit revenue growth in 2020. Here are the full year 2020 highlights:

- Revenue was $10.3 billion, up 19% on an as-reported basis.

- Gross merchandise volume (GMV) was $100 billion, up 17% on an as-reported basis and an FX-Neutral basis.

- GAAP and non-GAAP operating margin were 26.4% and 31.3% respectively.

Due to a strong holiday season, Ebay also reported strong Q4 results:

- Revenue of $2.9 billion, up 28.1% YoY, beat expectations by $160 million.

- Non-GAAP EPS of $0.86 beat by $0.03.

- GAAP EPS of $1.12 beat by $0.48.

- GMV was $26.6 billion versus consensus of $25.18 billion.

- Annual active buyers grew 7% to 185 million.

Still, this pales in comparison with high growth e-commerce marketplaces, not all of which are young companies.

Overstock, founded only a few years after Ebay in 1999, grew 2020 Q4 revenue 84.4% YoY. Wayfair, founded in 2002, grew Q4 revenue 45.1% YoY. Fintwit favorite Etsy, founded in 2005, grew Q4 revenue an astounding 128.7%.

With the tailwinds from Covid looking ready to expire for Ebay, and the entire ecommerce sector, the market is dubious about whether Ebay can continue growth and beat tougher comps. Executives were upbeat in the most recent report, noting the progress the company made in executing on the three pillars of its long term vision:

- Defend the core business by building compelling next-gen experiences.

- Become the partner of choice for sellers.

- Cultivate lifelong trusted relationships with buyers.

It is clear from the report that Ebay executives are aware of the risks to its core business from other ecommerce platforms. To execute on its strategic vision, Ebay is focusing on seasonal opportunities and non-new, including refurbished, which was a top trend for holiday shopping.

How Big is the Opportunity in Non-New?

The online U.S. resale market for apparel and footwear was estimated at $7 billion in 2019 and is expected to grow to an estimated $26 billion in 2023, according to data from GlobalData cited in Poshmark’s S-1.

A report last June by Poshmark competitor Thredup, which filed for IPO recently and is expected to begin trading on the Nasdaq March 26, valued the secondhand apparel market at $28 billion and predicted it would reach $64 billion within five years. It said the resale market grew 25 times faster than the overall retail market in 2019, with an estimated 64 million people buying secondhand products.

Good opportunities attract competition, and competition for the online secondhand apparel and accessories market is fierce.

In addition to Poshmark, Depop, Grailed, Mercari, Thredup, Tradesy, The RealReal, other notable competitors include Vestiaire Collective, a French company that recently raised $216 million in fresh funding, and Vinokilo, a German company that has not raise any venture capital and has been consistently profitable.

Luxury brands and platforms are also starting to consider controlling the lifecycle of their own products. For example, luxury marketplace Farfetch launched Farfetch Second Life in November 2020. It allows customers to trade in high-end bags in exchange for a credit to shop new collections.

Authentication is a key feature of the luxury resale market, such as designer handbags, shoes, and apparel. As part of its strategic vision, Ebay rolled out its own authentication program for secondhand watches over $2,000 and sneakers over $100 last fall.

Based on the results, it is a potentially profitable niche for Ebay, and validates part of the opportunity Poshmark and its competitors are trying to exploit. Ebay saw a double digit increase in GMV growth in Q4 versus Q3 for watches over $2,000, while sneakers over $100 grew triple digits YoY in Q4.

Investors should note that authentication has been controversial for sites such as The RealReal, an online and brick-and-mortar marketplace that offers authenticated luxury clothing, jewelry, and watches.

The RealReal has been plagued by claims in the media, and on social platforms, that fraudulent products slip past low paid authenticators and are sold on the platform. The RealReal is also being sued by Chanel, which alleges that The RealReal is selling counterfeit Chanel bags.

Poshmark has faced similar claims from users. So far, accusations against The RealReal seem to be more prevalent and much higher profile. The potential risk is real to any company that claims 100% authentic designer goods.

Tailwinds from Sustainability

Consumers are increasingly aware of the fashion industry’s impact on the environment. The U.S. sustainability market is projected to reach $150 billion in sales this year, according to Nielsen.

In Europe, 67% of surveyed consumers consider the use of sustainable materials to be an important purchasing factor, and 63% of consumers consider a brand’s promotion of sustainability in the same way, according to July 17 report from McKinsey & Company on Sustainability in fashion.

Secondhand is inherently more environmentally friendly, as it extends the life of consumer products.

Seller Ecosystem: Size is a Moat

Sellers create marketplaces by offering the products that attract consumers. That is why one of one of Ebay’s three key priorities for its long term vision is becoming the partner of choice for sellers. In a virtuous cycle, sellers create the marketplace that keeps buyers coming back, which keeps sellers engaged.

For example, of all buyers who activated on Poshmark between 2012 and 2018, 34% also activated as sellers by the end of 2019. Of all sellers who activated between 2012 and 2018, 39% activated as buyers by the end of 2019, according to the company’s S-1 Registration Statement.

For sellers, every marketplace has advantages and disadvantages. Poshmark’s fees are less complicated than Ebay’s but significantly higher:

· Poshmark. For sales under $15, Poshmark charges a flat rate of $2.95. For sales above $15, the fee is 20%.

· Ebay. Ebay has been working to simplify its notoriously complicated fees. For most categories on Ebay, managed payments customers pay 12.35% up to $7,500, plus 2.35% on the portion of the sale over $7,500.

Poshmark has been criticized for its high fees. But the company acknowledged in its S-1 the potential for future reductions:

“In the future, we may be unable to attract new sellers or retain current sellers at these fee levels, as they may choose to sell their merchandise on other platforms with lower fees. Furthermore, pricing pressures and increased competition generally could result in having to decrease fees, which could cause reduced revenues, reduced margins, or losses, any of which would harm our business, results of operations, and financial condition.”

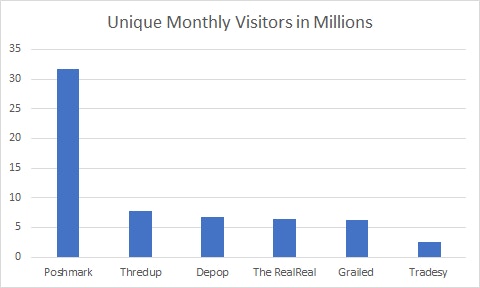

For Ebay, size is a moat. With its gargantuan user base, that moat is not easy to disrupt. The same may be true of Poshmark, which is the leading C2C marketplace for fashion, according to data from May 2020 from Statista, a German company that specializes in market and consumer data.

Founded in 2011, Poshmark has grown significantly larger than other fashion oriented secondhand marketplaces, most of which were founded around the same time.

Notable competitors in secondhand fashion include Depop, founded in 2011; Grailed, founded in 2014; Mercari, launched in the U.S. in 2014; The RealReal, founded in 2011; Thredup, founded in 2009; and Tradesy, founded in 2009.

Mercari, a Japanese company, had 3.4 million monthly active users in 2019, according to a company press release. It can be difficult to sell on platforms with much smaller user bases, although it helps to offer desirable brand names, according to user reviews.

Some sellers dislike Poshmark’s social aspects—it creates extra work by forcing sellers to like and share items, and negotiate with potential buyers—the size of the marketplace means sellers and buyers keep coming back. In 2020, Users who spent an average of 27 minutes daily on the app continue to re-engage over time as buyers and sellers, according to Poshmark’s Q4 report.

Fundamentals: User and GMV Growth

Poshmark launched in the U.S. in 2011 with a valuation of more than $600 million. The company has an asset light model and does not own or manage inventory, as items are listed, sold, and shipped by sellers.

In May 2019, Poshmark expanded to Canada, growing its community to more than 1.4 million users in that country within the first year.

International GMV was $6.4 million in 2019, according to the company’s S-1. It grew to $32.6 million in the nine months ended Sept. 30, 2020. For each of these periods, revenue from international operations was less than 10% of the company’s net revenue.

As of Sept. 30, 2020, Poshmark had 31.7 million active users in North America, 6.2 million active buyers, and 4.5 million active sellers, according to the S-1.

Executives did not update the total number of active users or active sellers in the Q4 report. It did note an increase in active buyers to 6.5 million, a 20% increase YoY from 5.4 million in Q4 2019. Social interactions also grew 48% to 30.4 billion in 2020, according to the Q4 report.

Poshmark Active Buyers (Thousands)

Source: S-1

Poshmark doubled the number of active buyers from June 30, 2018 to June 30, 2020, which it says has been a key driver of GMV growth.

GMV in Millions

The company plans to continue growing through increased engagement, new product categories, and international expansion, starting with English-speaking countries. Last month, Poshmark launched in Australia.

Poshmark chose Australia as its first market outside of North America due to the well-established thrift shop culture, high rates of e-commerce adoption, environmentally conscious consumers, said Chief Executive Officer Manish Chandra, in an interview with Bloomberg.

Quarterly Results and Valuation

Poshmark had a market capitalization of $3.35 billion and an enterprise value-to-sales ratio of 12.60 as of March 24. The company reported Fiscal Q4 2020 earnings March 11 for the period ending Dec. 31.

In Q4, Poshmark achieved its third consecutive quarter of profitability and had revenue of $69.3 million, a 27% increase from $54.7 million in the fourth quarter of 2019, according to the report.

Income from operations was $1.6 million, compared to a loss of ($15.1) million in the fourth quarter of 2019. GMV was $387.2 million, an increase of 28% YoY from $302.1 million in Q4 2019. Quarterly GMV has increased YoY for the past 11 quarters.

Adjusted EBITDA was $4.2 million which increased from a loss of ($12.6) million in the fourth quarter of 2019. Adjusted EBITDA margin was 6.1%.

GAAP diluted net loss per share attributable to common stockholders was ($0.31). Non-GAAP diluted net income per share to common stockholders was $0.05 a share and excludes non-cash expenses related to convertible notes and warrants due to the increase in the fair market value of our common stock share price.

For the full year 2020, income from operations was $23.4 million, compared to a loss of ($49.8) million in 2019. Net revenue was $262.1 million, a 28% increase YoY from $205.2 million in 2019.

GMV was $1.4 billion, an increase of 29% YoY from $1.1 billion in 2019. GMV has increased YoY since the company was founded in 2011.

Trailing 12 months Active Buyers reached 6.5 million in the fourth quarter of 2020, a 20% YoY increase from 5.4 million from Q4 2019. The company did not update the number of active sellers. Adjusted EBITDA was $34.3 million which increased from a loss of ($37.1) million in 2019. Adjusted EBITDA margin was 13.1% in 2020.

GAAP diluted EPS attributable to common stockholders was $0.22. Non-GAAP diluted net income per share to common stockholders was $1.25 a share and excludes non-cash expenses related to convertible notes and warrants due to the increase in the fair market value of our common stock share price, and the impact from the undistributed earnings attributable to participating securities.

Cash, cash equivalents, and marketable securities were $262.1 million as of Dec. 31, 2020. During the third quarter, Poshmark issued a $50.0 million three-year convertible note which converted into 1.4 million shares of Class A Common Stock upon completion of the IPO on Jan. 14, 2021.

Guidance for Q1 2021 is $76.5 at the midpoint versus $80 million expected, with adjusted EBITDA of $1.5 million at the midpoint.

The company plans to continue executing on its four growth strategies: focus on innovation to drive user engagement, growing international footprint and capability, growth through category expansion, and deliver robust, easy-to-use, effective seller services, according to the report.

As part of that plan, in 2020 the company launched two new product categories: Beauty & Wellness and Toys & Games and launched several new features. Poshmark also completed the rollout of “Posh Stories,” the company’s first video feature which enables sellers to showcase and sell their listings with short videos and photos, released “Drops Soon,” feature that allows Poshmark sellers to pre-market items not yet available for purchase, and launched Reposh, a feature that provides users with a one-click way to resell items purchased on the marketplace.

Conclusion

Poshmark is the largest online C2C marketplace in the U.S. that specializes in fashion, in a space with fierce competition. Its success is not limited to the U.S. After expanding to Canada in 2019, Poshmark grew its community there to 1.4 million users within the first year. Users apparently enjoy the social aspect of the platform, which uses an asset light model that been profitable for the last three quarters.

The pandemic has created uncertainty for Poshmark, and the entire ecommerce sector. But with the recent expansion to Australia, and the launch of new categories and features, Poshmark has room to grow. It benefits from long term tailwinds, including an increased interest among consumers in sustainability and the rise of social commerce.

Some investors have criticized the company’s social platform, saying it is a waste of time for sellers who will leave the platform. Poshmark has also been criticized for its high fees. We think these are relatively minor complaints about a platform with a record of success.

Any company can lose market share to competitors. But Poshmark’s competitors have a lot of catching up to do. Now that the valuation has come down to earth, and sentiment with it, the stock may provide a good long-term opportunity—even if the growth is not what hypergrowth investors are used to.

Disclaimer: This article represents the opinion of the writer, who may disagree with the official position of Beth Kindig and I/O Fund. Jessica Ablamsky does not currently own shares of Poshmark but may initiate a position within the next 72 hours. Beth Kindig and the I/O Fund does not currently own shares of Poshmark. The content in this article is intended to be used for informational purposes only. The author has not received any compensation from any third party or company discussed in this article. The content is the expressed opinions of the author and is intended for educational and research purposes. Any thesis presented is not a guarantee of any particular stock’s future prices, so please factor this risk into your own analysis. It is very important that you do your own analysis before making any investments based on your personal circumstances. The author is not a licensed professional advisor. Please seek counsel form a licensed professional before acting on any analysis expressed in this article, to see if it is appropriate for your personal situation.

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su