Q3 2020: Tech Growth Earnings Review - Pinterest, Snap, Microsoft And More

November 04, 2020

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Oct 29, 2020,11:49pm EDT

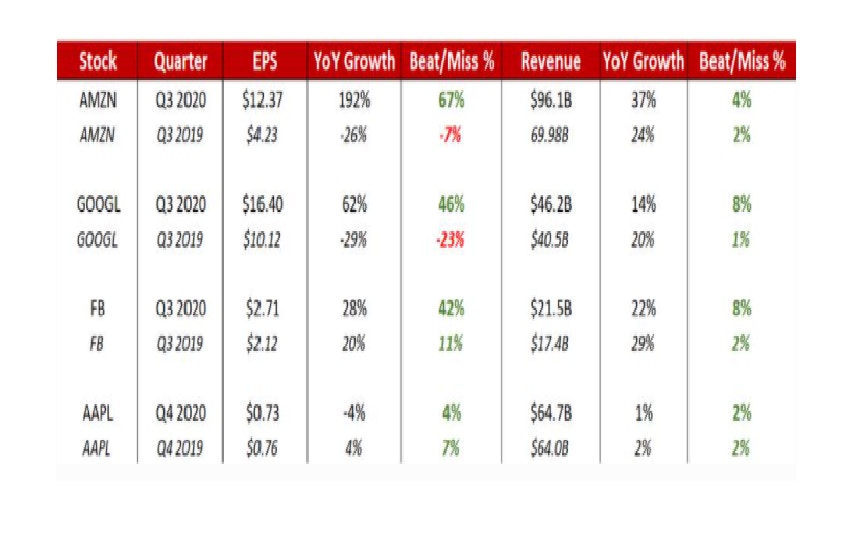

Before breaking out the earnings reports from the high-growth universe, here are the results from Big Tech earnings today. Each company beat on both the top and bottom lines. Other than Alphabet, they are all trading down after-hours following these results as the market digests the magnitude of the beats, and in Apple's case, the lack of guidance.

BETH.TECHNOLOGY

Snap:

Snap reported Q3 results on October 20th, beating both the top and bottom lines. The ongoing recovery of advertising budgets helped to boost Snap's revenue growth to 52% YoY in Q3, which now sits just below the 58% pre-COVID growth rate the company recorded during Q1.

Notably, the reacceleration that Snapchat reported is the highest Q3 growth rates since 2017. According to management, some of the user growth highlights from this quarter include Lens Studio, which saw creative applications to use AR as a way to try-on products from brands including Sally Hansen for nail polish and Champs for sneakers.

Other product features released contributing to this quarter's beat include Brand Profiles, Minis, Places on the Map, Dynamic Ads, Bidded AR Lenses, Dynamic Lenses, Camera Kit, Snap ML Lenses including the Anime Lense.

The company also attributes the growth to linear TV and sports being featured on the social media platform at a time when content is seeing a surge.

Here is what the company said about Dynamic Ads and AR Ads on the earnings call:

For example, last quarter we launched Dynamic Ads globally, which combine product catalogs with our optimization capabilities to reward advertisers who invest in our platform with ROI at scale, and we are already seeing strong adoption rates from Retail, CPG, Restaurant, and Gaming verticals, among others.

While Dynamic Ads recommend items to Snapchatters based on their interests, AR try-on takes this a step further and allows Snapchatters to visualize the item in real life. For example, Clearly, an eyewear retailer, leveraged our sponsored AR Lenses to enable our community to try on different pairs of glasses, which resulted in 33 seconds of average playtime and a 5.3% share rate. Clearly was able to drive a full-funnel impact for their brand, achieving a 7-point lift in brand awareness and a 5-point lift in brand consideration while also driving a 46% lift in unique page viewers on their site and a 3.3% lift in purchases.

Daily active users rose 18% to 249M, topping the consensus of 243M. For user base demographics, Snapchat reaches over 90% of Gen Z and 75% of Gen Z and Millennials in the United States, the UK and France. This is one reason the company believes its augmented reality platform is seeing early success with brands as this demographic is more likely to engage with AR advertisements. Snapchat also has a gaming platform with new releases every quarter.

The majority of Snap’s growth came from the Rest of World category, at 43% growth. North America grew 7% and Europe by 10%. Meanwhile, North America and Europe carried the majority of the revenue growth at 56% year-over-year and 49% year-over-year, respectively.

Snap also recorded its most successful quarter ever in terms of monetizing its user base with a global ARPU of $2.73, coming in well ahead of the $2.23 consensus estimate.

Even though the company did not offer guidance for Q4 due to COVID uncertainties, SNAP stock surged over 20% following the results. Kids being schooled virtually, especially college-aged, is likely contributing to the company’s record Q3 usage and monetization.

Pinterest:

Pinterest rose with Snap following Q3 results as investors anticipated a similar recovery in ad spend for the social media company. The company delivered outstanding Q3 results that easily cleared consensus expectations.

Total revenue rose 58% YoY in Q3 with 49% growth in the US and 145% growth internationally. Monthly active users jumped 37% overall to 442M and ARPU rose 15% (US +31% and international +66%) to $1.03.

Perhaps most impressive was management’s 60% YoY growth guidance for Q4:

Additionally, we expect our business to maintain its momentum in Q4, with revenue growing around 60% year-over-year.

And then finally, this brand safety concept, especially post-July and the boycotts that we saw, I would imagine that we're seeing a sustained benefit just due to the election season. But I think it's a secular trend where advertisers want to be around positivity as they build their brands, and that that's contributing to our growth as well. That's what we're hearing.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Management did state there is a level of uncertainty with this guidance due to Covid and tailwinds the company saw from being “brand safe” during the election (i.e. attracting ad spend typically given to Facebook).

Here is what the company said when asked if the beat came from factors inherent to the product or due to the macro conditions of ad spend being thin in Q2.

Yes, I mean, Ross, it's really hard to parse. I mean, I would love to be able to disaggregate that and say, we're getting X amounts from the technology investments we've made. We're getting Y amounts on demand returning from a macro perspective, or insights give us a certain amount and the brand safety equates to the remainder, in reality, it's the combination of all the above. Ads are working. I think we went through this a little bit on Brian's question, but making it easier for especially medium-sized advertisers to on-board and automate spending their budgets effectively against their desired online conversion and sales objectives has been a big driver for us …. [some parts omitted here for brevity]

So it's a mix of product and technology, macro recovery, the insights that we're able to deliver, and the brand safety and positivity that Pinterest uniquely brings and the world of social media.

Twilio:

Twilio pre-announced Q3 revenue would come in ahead of previously issued guidance from the company of $401 million to $406 million, with analyst consensus at $404M. Expectations were already high going into the earnings report and Twilio went on to beat revenue estimates by 10% for revenue of $448 million and growth of 52% year-over-year. This was the largest beat by dollar in Twilio’s history, as referenced by analyst Khozema on the earnings call.

Twilio also handily beat on earnings at $0.04 EPS compared to analyst consensus of -$0.03 EPS.

For Q4, Twilio expects revenue of $450M-$455M (37% YoY growth) vs. consensus of $432.1M. The net retention rate came in at 137% for TWLO in Q3. The guidance the company provided for earnings next quarter did not match expectations with an operating loss ranging between $10 to $15 million.

Twilio is on an expansion streak fueled by acquisitions. The company completed the acquisition of SendGrid in early 2019, launched the Flex platform, and has now acquired Segment to “enable developers and companies to unify customer data from every touchpoint.” The guidance provided does not include Segment which is expected to close in the current quarter and will modestly impact the top and bottom line.

On the earnings call, the company highlighted the importance of health care with Twilio’s products:

In healthcare, the innovative solutions that have been built on top of Twilio to address the COVID-19 crisis, provide an opportunity for the industry to advance the use of technology to better deliver outcomes for patients and create tools that fit seamlessly within a physician's workflow. This has always been the vision, but the coronavirus crisis highlighted the urgency, immediacy, and magnitude of that need.

Most importantly, CEO Jeff Lawson and the management does not see these trends slowing down with a vaccine or return-to-normal and specifically addressed this:

The other thing I would just point out, though, is that some of the acceleration that we've seen, for example, in healthcare and education, e-commerce, but we also think that those use cases are going to be pretty resilient. I don't think they're going to be ephemeral at all. In fact, I think we see a lot more opportunity in some of those industries. And so I think that's going to provide ongoing tailwind over the medium-term as well.

You can access the Investors Day presentation here where the company guided for 30% growth over the next 4 years.

Shopify:

Shopify announced outstanding Q3 results, with revenue growth of 96% year-over-year and Gross Merchandise Volume growth of 109%. The revenue number came in 18% above consensus estimates while GMV was 13% above forecasts.

The company announced subscription revenue grew 48% during the quarter, merchant revenue rose 132%, and monthly recurring revenue grew 47%. Non-GAAP EPS of $1.13 came in well ahead of estimates calling for $0.50, and operating margin increased to 17.6% vs. an 8.7% consensus. This compares to an adjusted loss of $0.29 EPS.

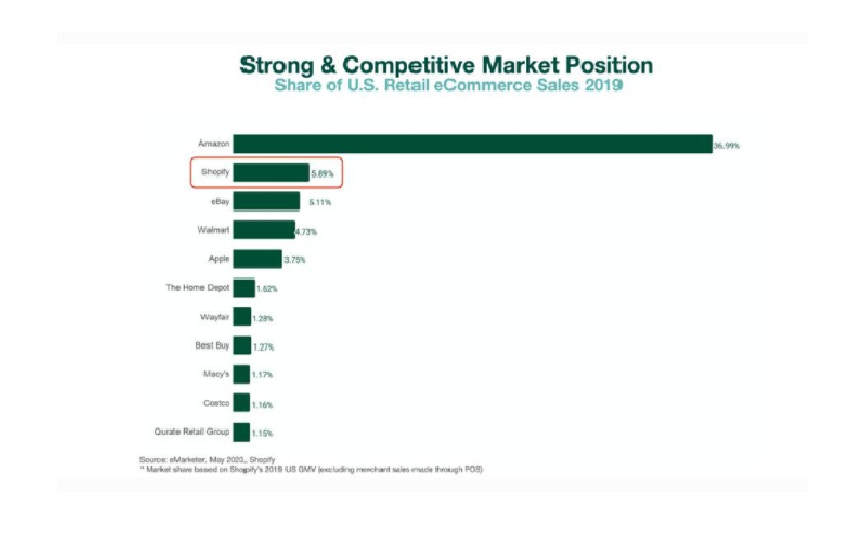

EMARKETER

Shopify gave away a 90-day free trial with this cohort transitioning from a free trial to paid merchants in Q3, which had a “double cohort effect” on merchant revenue growth of 132%. The company does not expect the Q4 demand for subscriptions on a year-over-year MRR growth rate to match Q3. This note was addressed by Amy Shapero, CFO, in the earnings call:

So, I want to just highlight that we did have a record quarter in Q3 for merchant growth due to the double cohort effect that I talked about in my opening remarks. But I think it's really important to emphasize that even excluding the 90-day free trial as who converted in Q3, we still would have seen an acceleration in our merchant growth over pre-COVID levels, which tells you that more merchants are coming to the platform with this shift to online commerce and COVID.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

The free trial was addressed again here as to how the key metrics compare to the 14-day trial with lower conversions but higher retention:

So, the new store creations in Q2 were the new stores coming on the platform associated with the 90-day free trial. So, we were not able to count them as merchants in Q2. We saw many of them convert to paying merchants in Q3. The conversion rates that we've seen on the 90-day free trials is slightly lower than cohorts historically on 14 day free trials, but we think that's okay, because they're more intentional when they convert because they've had a longer time period. The data that we have in the three months in some of the earliest 90-day free trial cohorts and converted suggests that those merchants that have a higher retention than 14-day free trial. As we know, many of them coming online in Q2 were established businesses looking for a multi-channel platform. And so we believe that those 90-day free trials will be more sticky than the 14-day free trials cohorts historically.

Notably, Shopify incredible B2B brand power with philanthropic efforts to support Black entrepreneurship with $130 million dedicated to supporting businesses with diverse ownership. The company also launched a Tiktok channel that allows merchants to market their products using TikTok for Business. The collaboration allows for in-feed video ads to expand their paid and organic reach.

You can view Shopify’s earnings presentation here.

Microsoft:

Microsoft announced FQ1 2021 results on October 27th, outperforming on headline metrics led by strong Commercial Cloud and Azure growth. EPS of $1.82 came in ahead of estimates of $1.54 EPS while 12.4% YoY revenue growth represents a 4% beat above consensus.

Intelligent Cloud revenue of $12.99B was well ahead of the $12.73B consensus, while the 48% YoY growth in Azure was better than the expected 44% growth. Management issued a somewhat tepid outlook for FQ2, expecting weaker Consumer PC growth and intelligent cloud revenue in line with forecasts, along with stronger Processes and Business Productivity revenue.

The reason for the lower-than-expected guidance is due to softer business demand that will cut into Windows licensing revenue. We also saw commercial PCs crater 22% after support for Windows 7 ended and the coronavirus pandemic forced more people to work from home.

However, these are not the segments that would cause an investor to choose Microsoft as a portfolio holding. For the most part, the bull thesis centers around Azure and the line of horizontal products under the Azure infrastructure and PaaS umbrella: Azure Arc, Azure Synapse, Azure SQL Edge, Azure Machine Learning, Azure Space and Microsoft Cloud for Healthcare. Azure saw a slight acceleration of 1% this quarter. Gross margins on Commercial Cloud are an impressive 71% when including an accounting change on server equipment from two to four years.

Notably, when asked about the effects a decline in on-premise and transactional revenue could have on Microsoft, CEO Satya Nadella answered that the strategy for Microsoft is distributed computing with the public cloud and edge (and presumably these will make up for any decline seen from transitioning on-premise).

One is, the approach we have always taken is that distributed computing will remain distributed. So, the cloud and the edge is what will be the distributor fabric for applications. So, if you look at where our growth is coming from for the all-up number in Intelligent Cloud, it's coming from the infrastructure layer, the flexibility that we have around hybrid deployment, things like Azure Arc, a very differentiated. The same thing with data, that's one of the big future innovations, even in the last quarter was the ability to deploy, for example, Azure data in any cloud, including the edge.

The more interesting note came at the end of the earnings call by Brent Bracelin of Piper Sandler, who pointed out Azure had grown to 17% of revenue — larger than Windows – and up from 45% just three years ago, according to his model.

I wanted to follow up on Azure. This is a segment that’s grown now to 17% of revenue. I think, that’s up from 4% just three years ago. You talked about the number of petabyte-scale applications doubling. And from a size standpoint, it looks like in my model, Azure is bigger than the Windows business for the first time ever. My question really is around where are we at in the journey around Azure? How important is this to the Microsoft model? And ultimately, how big could it be looking out over the next three to five years?

This provided an important glimpse into Azure’s ongoing importance and the evolution of Microsoft.

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su