The IPO Glut of 2020: Why Valuations Have Gone Too Far

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Jun 18, 2021,12:43am EDT

There is an outsized risk with Snowflake, AirBnB, DoorDash and Roblox’s IPOs showing an extreme increase in valuation since the last private funding round that will be hard for the public markets to absorb. I dug up some comparative research between 2019 IPOs and 2020 IPOs and describe this outsized risk, which is 10-fold from the IPO class of 2019.

More times than not, IPOs lead to losses for retail investors and there are specific reasons as to why. These reasons have only gotten worse with loosened IPO regulations. We also look at why raising capital at the same time as a Direct Listing shifts too much risk to the general public.

The IPOs of 2020: Snowflake, AirBnB, DoorDash and Roblox (2021)

Despite the hype that flashy IPOs draw, more than 60 percent of the 7,000 IPOs from 1975 to 2011 had negative absolute returns five years later. However, the 40% odds for success through 2011 are better odds than what investors face today.

IPOs in Review: 2019

Before we talk about the serious red flags in the IPO scene of 2020, I want to visit what 2019 looked like as a reference point.

In 2019, Zoom Video and Crowdstrike went public with the fastest growth levels the tech industry has ever seen. We will use these two as a baseline because their top line financials at time of IPO continue to exceed any tech IPO we have seen since.

Source: Snowflake IPO: In-Depth Analysis

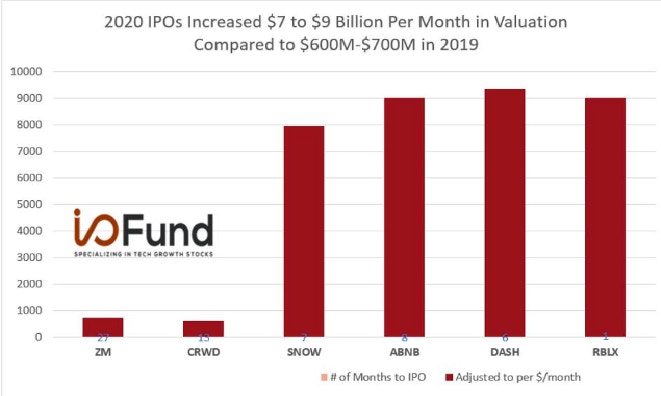

In the case of Crowdstrike, the company’s last private valuation prior to going public was in May of 2018 for $3 billion. The initial price that institutions paid was $7 billion and the shares began trading at a $11 billion valuation. When we average out the premium paid between the last private valuation and the opening price of $8 billion on a per month basis for the time it took to go public, retailers paid a premium of $615 million per month across 13 months.

Crowdstrike went on to have a volatile trading history in the first year with a peak to trough drop of roughly 50% within six months.

YCHARTS

Zoom Video’s last private valuation prior to going public was $1 billion in April of 2017. The initial price institutions paid was $9.2 billion in April of 2019 with shares opening at a $20 billion valuation. When the $19 billion is averaged out across the 27 months between Zoom’s last private round, the premium retailers paid on valuation is $703 million per month. This is about $90 million more per month than Crowdstrike.

Notably, I covered Zoom Video as the “Best Silicon Valley IPO” at the time of its listing but the I/O Fund waited until the following January 2020 to enter the stock at $62. Despite perfect earnings beats, it took Zoom Video an entire year before it consistently traded above its opening price

The point of this is to illustrate that tech’s top growth companies had their valuations increase an average of $600 to $700 million per month range since the last private valuation. These opening prices, which ranged from an increase in valuation of $5 to $10 billion required a year to absorb.

IPOs of 2020 and 2021:

The opening valuation for Zoom Video caused Barron’s to call Zoom Video’s IPO a Crazy Bubble. If that’s a crazy bubble, then I’m not sure what the words are for 2020. The word “glut” comes to mind as Snowflake, AirBnB, DoorDash and Roblox increased their valuations from the last private by an order of magnitude compared to the IPO class of 2019.

Let me explain:

Snowflake’s last private funding round was at a valuation of $12.4 billion in February 2020 with an initial price of $33 billion and an opening price of $68 billion in September of 2020. That means Snowflake opened trading at a premium of $8 billion per month since the last private valuation compared to Zoom’s $700 million and Crowdstrike’s $600 million. Snowflake essentially 5X’d it’s valuation in 7 months while revenue declined.

This also means the market must absorb a $35 billion premium on top of the initial price. How long do you think that will take considering it took Zoom Video a year to recoup a $10 billion premium? It’s impossible for a valuation to spike that much in one day without it taking a substantial amount of time for the valuation to catch up to financials.

This is a tough pill to swallow as we’ve published favorably on Snowflake as a company and a product. Yet, there is no real valuation here if the last private valuation was $12 billion within the last year; it’s simply pie-in-the-sky pricing that insiders hope will last. The company did not change and there were no catalysts.

Consumer favorites AirBnB and DoorDash came public recently and the difference in private valuation versus public valuation is even more absurd as these companies carry a higher risk in terms of performance post Covid. AirBnB’s last private valuation was on April of 2020 for $18 billion. Eight months later the initial pricing was at $42 billion and the opening price at $90 billion.

2020 IPOs Increased $7 to $9 Billion Per Month in Valuation Compared to $600M-$700M in 2019 - I/O FUND

AirBnB’s opening price equates to $9 billion in valuation per month in premium that retailers are paying on a company that was worth $18 billion earlier in the year with the same growth numbers and revenue. In fact, AirBnB only grew revenue by $1 billion in 2019 before declining by $1 billion in annual revenue in 2020 due to Covid. The forward revenue for this year is $300 million more than the revenue in 2019. Most certainly, growth did not drive the opening valuation.

DoorDash carries the most risk of the four names we are analyzing as the economy opening up will translate to fewer food deliveries. This company had a $16 billion valuation in its last private round in June of 2020. The initial price was at a $34 billion valuation and the opening price at a $72 billion valuation.

Technically, DoorDash should be valued below its Covid valuation as there’s more risk with the economy opening up as to how the company will perform. All Covid winners have taken a hit to their valuations: Zoom, Crowdstrike, Peloton, etcetera.

Roblox is another blatant example of how IPO valuations are overpriced for retailers. The company raised a private round at $29 billion in February of 2021 before going public at a $39 billion valuation one month later. This means retailers were charged at $10 billion per month premium. We will have to check back this time next year to see how long it took for Roblox’s stock price to permanently absorb the $10 billion it charged retailers. Notably, all of these examples do well in bull markets while the real impact comes out during downturns.

I/O FUND

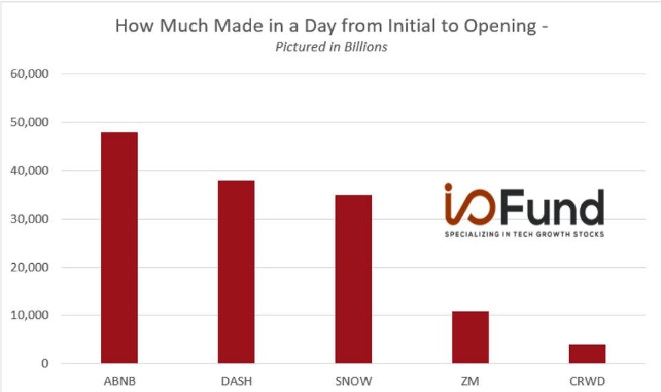

Often times, retailers will cheer on 15% or 30% gains in one day when a stock really pops. Yet, most IPOs are seeing 80% to 100% gains for an average of $30 billion generated in one day between the initial price and the opening price. What retailers must understand is that valuations have a ceiling and this means the company must earn this $30 billion pop in valuation over time.

How Much Made in a Day from Initial to Opening - I/O FUND

SEC IPO Regulations that Have Changed:

Here are a few of the new regulations being leveraged:

· Direct listings can now raise capital, which means retailers are exposed to more companies that have no lockup expiration. The company can list at a high valuation and insiders can liquidate as soon as it’s listed. You’ll see below examples of failed direct listings, such as Spotify and Slack. Prior to the recent change, direct listings could not raise capital.

· According to Forbes, SPACs made up 50% of the IPO market last year. The volume is high because SPACs allow companies to go public faster. Although there are some gems that have come from reverse mergers, SPACs often have a complicated business history and some proxy statements have become the subject of litigation.

· SPACs also come with fees known as “the promote” which allows 20% of the shares to go to the SPAC manager. The 20% of shares is effectively taken from investors plus 5% in other fees.

· The SEC may start to treat warrants as liabilities which could slow the pace of SPACs; this comes after nearly 250 SPACs went public last year and 340 have already gone public this year. The percentage of IPOs that were SPACs is at 72% this year, up from 55% this year. The speed in which SPACs go public has created byzantine filings.

· Traditionally, lockup periods lasted 180 days yet we are seeing many creative ways of approaching lockup periods, such as partial lockup expirations that come sooner or opportunities for employees to sell before investors. “Blue Sky Laws” were put into place to help protect investors by ensuring full lockup period yet this has become looser over the last few years. If a company has a partial lockup period expire, they often bury this in the S-1 filing.

A Note on Direct Listings

Retailers have no voice on Wall Street, and this is evident by the way that venture capitalists openly criticize the IPO process because they’d like to see the fat surplus between the initial price and the opening price go to the company and other insiders rather than institutions.

Translation – it’s okay to keep charging high prices to retail, but instead, make sure the cash is funneled to the right people. Direct listings accomplish nothing when it comes to the outsized risk that IPOs have presented in the last year; which is raise money, continue to charge the $7 to $9 billion per month in valuation to retailers, and have no lockup expiration (rarely, does a private company increase $7 to $9 billion in one year let alone one month)

Direct listings propagate high valuations because the stock does not need to perform for six months; it can immediately fail and still provide an exit. In this case, 100% of the risk is transferred to retail at the open trade and there are crumbs left in terms of reward.

I was critical of Slack’s DPO two years ago and also Spotify’s DPO. Notably, Slack is a stock my company ended up owning after it plummeted more than 50% from its DPO opening price. From experience, the I/O Fund has concluded there is too much downward pressure from DPOs and the immediate exit for insiders is a flag as a serious company will look for long-term investors.

I/O FUND

You can access my previous analysis on Slack’s DPO here where I stated:

Slack is not looking to raise money, and has chosen a direct listing as opposed to a traditional initial public offering. This means insiders will initially sell their stock and there will be no lock-up period. Eliminating the lock-up period creates even more risk than usual compared to traditional IPOs that have six-month lock-up periods.

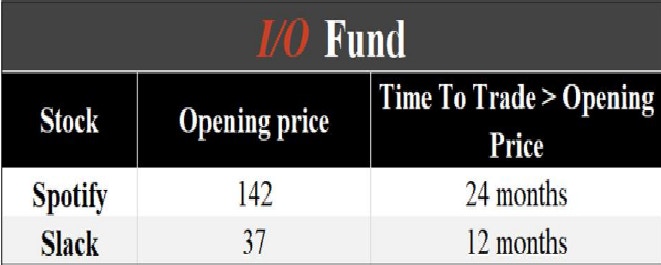

Around the time of Slack’s DPO, we discussed why we did not like this process. We cited Spotify as an example as Spotify took twenty-four months to reach its opening price again, and Slack – arguably one of the best products to come out of Silicon Valley – only touched its opening price again 12 months later after Salesforce announced they were acquiring the company.

That’s a very long time to park your money with no return not to mention the scary roller coaster ride on the way down.

Know Who Your Advocates Are:

Retailers need representation and better information on IPOs and valuations. As advocates for retailers, we often hold off from buying IPOs until after the lock-up period, and we always disclose every entry and exit we make with real-time notifications. If we do participate, it’s with an active stance and the understanding we may exit before the lock-up period expires if the chart looks weak. We will then re-enter when the stock stabilizes – usually a year or so after the IPO.

In the case of the new class of IPOs, there’s a chance the companies don’t stabilize for many years as the true valuation is likely the initial price that institutions paid (i.e., there’s a reason they paid that price and not a penny more – both sides have teams of professionals to fairly price the transaction for a funding round).

Confirmation bias is also commonly used against public investors. In this case, because DoorDash and Airbnb are well-known and well-loved consumer brands, the opening price was especially lavish. I had gone to great lengths to warn retailers about Uber while many talking heads said the stock could reach $100 or higher. That analysis is worth a read as it became one of my best calls in terms of protecting losses for my readers.

Conclusion:

There is undeniable evidence that something odd happened in 2021 in terms of the run-up in valuation on IPOs as we saw the premium retailers pay grow from $600-$700 million to $8-10 billion per month since the last private valuation. The glut in the IPO process will eventually catch up to market as this run-up is not sustainable without a meaningful change in story or re-acceleration in growth (the opposite happened; there was as deceleration in growth in all four companies).

The loosening of IPO regulations leading to outsized risk is reminiscent of loose lending laws during the financial crisis. If history is any indication, the banks will be bailed out and the individual will suffer. Therefore, we do our best to avoid participating in frenzies as there is no magical market where valuations don’t have a ceiling, rather they can hit a ceiling very quickly and take time (years) to be absorbed.

Note: If we do keep our Snowflake position, we will plan to exit on any weakness. This is distinct from the list of stocks we hold with no plans to exit.

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per