IPO Report card:

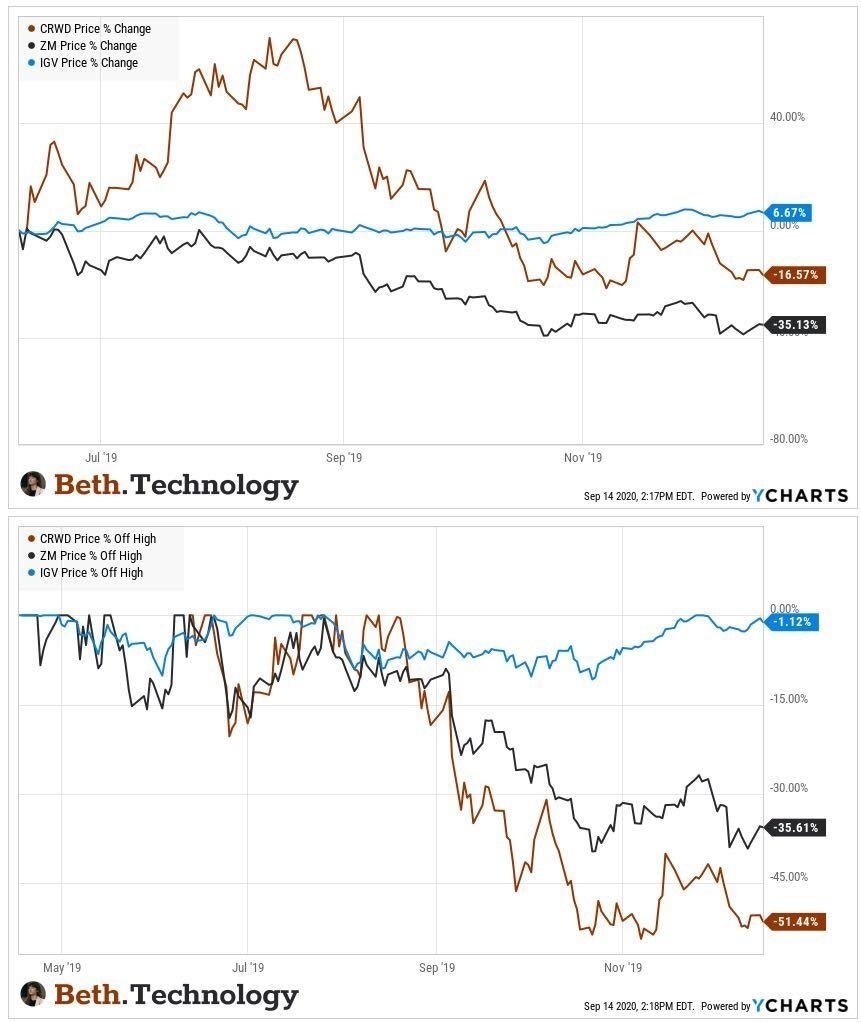

As of late, the underlying goal of IPOs appears to be how to get retailers to pay as much as possible until the lock-up expires. It doesn’t matter if Berkshire invests unless you get a chance to buy at the same price. Your shares could lose 50% and Berkshire would break even. That’s not a public offering by any stretch of the word. Please keep in mind, that many winners in tech retrace well below their opening price (up to 50% below opening price in the case of Crowdstrike).

Prior to Snowflake raising its opening price (for the fourth time), I had cautioned that: “the biggest risk of all is how much alpha will be left in the first year of trading by the time retailers are offered the crumbs.” When I wrote that, I did not imagine we’d see the opening price of $245. It was, in a word, astounding.

Like Warren Buffet says, the best part of investing is you don’t have to hit every ball. On that note, I can confidently say Berkshire would not be hitting the ball at 98X NTM revenue – but they sure hope you do.

Snowflake went public with an IPO price of $120. It opened at a 105% premium of $245, and closed on its first day of trading just under $254. Based on its opening price, this gave the stock a valuation of 98x NTM revenue if generously calculating 121% growth across all four quarters.

Keep in mind, in the chart below, companies over 40x NTM revenue are profitable.

Regarding their business, Snowflake reported 121% revenue growth YoY with a net retention rate of 158%. As stated, the company is not profitable. In the six months ending in July, they spent roughly $190.5 million on marketing while making $149 million in gross profit.

I discussed Snowflake’s product strength in detail in my previous analysis, stating it demonstrated: “triple-digit growth, clear product differentiation, key metrics that prove product-market fit and gravity-defying management.” However, the price of the stock has become untethered from reality. As stated in the Forbes article, there is little alpha left over the next year and that is the primary risk.

JFrog

JFrog opened trading at a $71.20, which is 62% above its offering price. This gave the stock a valuation of 40x NTM revenue, which was the highest forward multiple in enterprise software at time of IPO until SNOW started trading about an hour later. The company provides DevOps software to organizations globally, enabling those businesses to build and release software faster and more securely.

JFROG posted an impressive 50% growth rate in its latest quarter with 81% gross margins and positive 11% FCF margin, which is why they commanded such a high premium. However, the company faces a bevy of competition including Google Cloud, Amazon Web Services, and Microsoft Azure. JFROG is a pure play, which I tend to favor; however, this IPO valuation is over its skis.

Sumo Logic

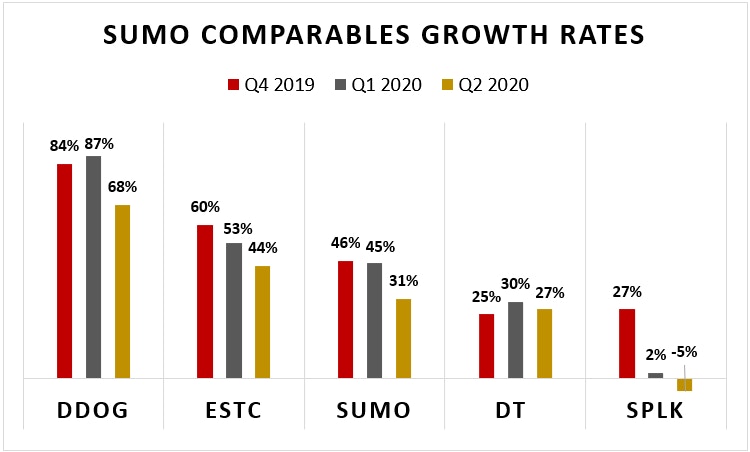

Sumo Logic began trading September 17th with an initial offering price of $22 a share. The first trade was 21% above the premium at $26.50 and closed at $26.88. Regarding key metrics, Sumo Logic stated that its dollar-based net retention rate has fluctuated between approximately 120% and 135% for each of the past nine quarters, which is notable. Their forward price/sales based on their opening price gives the stock a valuation of 8.3x NTM revenue.

Sumo Logic’s biggest risk is their competition. Companies such as Splunk, Elastic, Datadog, Dynatrace, Microsoft and Google all have bigger budgets, greater name recognition and a larger customer base.

Amwell

Amwell (AMWL) is a mobile and teleheath platform that connects patients with doctors over video. The stock went public on September 17th with an IPO price of $18. It began trading with 42% premium at $25.51, and closed the day at $23.95.

Amwell’s YoY revenue growth accelerated from 31% year-over-year in 2019 to 77% year-over-year in H1 2020. Based on their opening price, this gave the stock a valuation of 8.4x NTM revenue.

Unity

Unity (U) is set to open trading September 18th at an expected price range of $44-$48. This would value the company in the range of $11.6B-$12.6B. At the high end of the proposed range, Unity would trade at 14.2x NTM revenue.

Unity grew revenue 39% YoY in the first half of 2020 and increased its net-retention rate to 142%, a strong indication of increased spending within its existing customer base. With 93 of the top 100 gaming studios already Unity customers, it is crucial for the company to continue to drive higher spending among existing customers.

Here’s how the string of tech IPOs stack up this week:

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su