Oracle Hit From All Sides: Iaas Cloud and Programmatic

June 25, 2018

Beth Kindig

Lead Tech Analyst

Summary: Infrastructure as a service (IaaS) is the fastest growing cloud segment and will continue to be with AI, machine learning and connected cars. Gartner, an authority in tech analysis, placed Oracle in the “niche player quadrant” (not the leader quadrant) for Infrastructure as a Service (IaaS) May 22. In addition to IaaS, Oracle’s Data as a Service business model will weaken as marketers fail to get proper consent for ad targeting.

Cloud infrastructure is hot right now and for good reason. The world increasingly relies on cloud data centers due to server virtualization, smartphones, movies and entertainment, chatbots, office productivity, software as a service, and social media, to name a few.

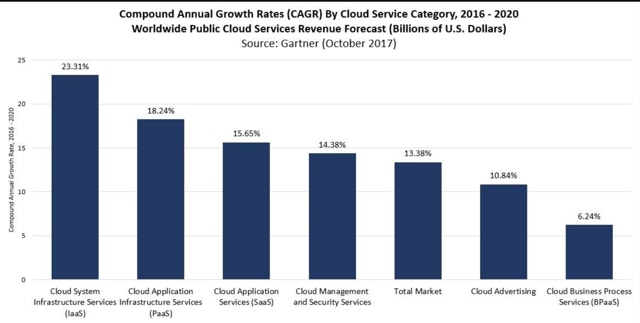

Gartner predicts the worldwide public cloud services market will grow to 21.4 percent in 2018 to $186.4 billion. The fastest growing segment is infrastructure as a service (IaaS) forecast to grow 35.9 percent in 2018. As we store more data in the cloud from AI and machine learning, this sector will continue to expand. For instance, fully automated cars will produce an estimated 25 Gigabytes of data per hour or 300 TB per year. Therefore, any savvy investor should place bets in this sector for 2021 and beyond.

No Medal for 4th Place in Cloud Infrastructure

Oracle (ORCL) is a long-time enterprise cloud powerhouse with billions invested in engineering and strategic acquisitions. On the quest to build and defend a range of cloud services, the company is expanding hybrid-cloud technologies, investing in customer-success programs, and benefiting from a less-than-expected decline in on-premise revenue. On the other hand, the transition to the cloud is taking longer than expected, according to Keybanc analysts, and is at risk for lagging behind Amazon (AMZN), Microsoft (MSFT) and Google (GOOG) in the Infrastructure as a Service category, the fastest growing category in public cloud services.

Last quarter, Oracle beat earnings estimates but came in slightly below expectations for revenue at $9.77 billion vs. $9.78 billion. The adjusted earnings of 83 cents beat the consensus estimate of 72 cents and was up 20% for its fiscal third quarter, which ended February 28. The better than expected earnings were not enough to convince investors in Q3 as the stock fell 4 percent after earnings were reported, then fell an additional 8 percent in pre-market trading. The stock is at $46.16 today compared to $52.90 before Q3 earnings.

One major concern is Oracle’s low share of cloud infrastructure and platform revenue, which came in at $415 million with 28 percent growth compared to Amazon at $5.11 billion revenue at 45 percent growth. It doesn’t help that Gartner, an authority for accurate tech analysis, placed Oracle in the “niche player quadrant” in the Magic Quadrant (not the leader quadrant) for Infrastructure as a Service (IaaS). Notably, financial analysts from JP Morgan and Murphy lowered Oracle targets yesterday, however, Gartner published this magic quadrant on May 22nd and it is likely what these analysts based their predictions on.

Meanwhile, in another category, cloud software (SaaS) revenue was up 33% last quarter for Oracle at $1.15 billion with notable competitors SAP and SalesForce. The remaining revenue is primarily on-premise revenue of $6.42 billion, and software license revenue of $1.39 billion.

While Oracle has maintained a name for itself in cloud services, it’s offerings are not strong enough to earn a medal as a front runner, which will spell trouble for earnings as Data as a Service (DaaS) undergoes regulations.

DaaS: Programmatic Will Crash

Oracle pursues many strategies and acquisitions for cloud services because it knows it has to be seen as a cloud company in order for Wall Street to invest in its future. However, one of Oracle’s main market positions is Data as a Service (DaaS). From 2012 to 2014, Oracle went on a tear of acquisitions to increase their marketing stack and to cement their position in the digital advertising space. In May of 2012, Oracle bought social marketing solutions provider Virtue for an estimated $300 million, the marketing automation firm Eloqua for $810 million in December of 2012, Responsys for $1.5 billion which is a business to consumer solution and the data management platform, BlueKai, for $400 million in 2014. This totaled an estimated $3 billion in collective marketing tech acquisitions to enhance DaaS.

Programmatic is the automatic trading of advertising which is augmented by data for superior digital advertising. Oracle’s DaaS is essentially a way for companies to upload their data and potentially enrich their data by anonymously sharing and matching data sets. Oracle calls this “making your data smarter.”

Notably, BlueKai was a private company that captured the data boom with 9,245% growth from 2009-2012 – although competitors in the market saw a whopping 21,337% revenue growth (Data Xu). BlueKai was originally a buyer and seller of consumer data and pivoted to become a seller of data analytics and management technologies. These acquisitions were designed to help Oracle enable private data sharing. This is where the marketing ecosystem ingests first-party data and brokers marketing communications (MarCom) and advertisements in a second- party data transaction. While the data is not being sold, the information is being shared to third-parties without consent for the purpose of more advertisements.

My newsletter subscribers get this information first. Sign up here.

As the Oracle BlueKai deck states, here are some examples:

- Hotel chain sharing data with a bank to target customers who do not have bank rewards cards

- Online broker sharing data with a social media site for audience based targeting

- Social media site sharing data with a technology company

While Oracle Blue Kai may not come directly under regulation because they are the middleman, and not the company with a direct relationship to the user, their business model is likely to weaken due to the way the data is being used. Marketing platforms and data management platforms will increase a marketers liability if they choose to transfer and trade private, first-party data. For these marketers, under the GDPR, consent must be given for each processing operation need and cannot be bundled together. Therefore, there will be less advertising and Marcom data to process, lowering Oracle’s revenue.

My Prediction: Cloud infrastructure will continue to grow as data storage increasingly provides the infrastructure for technological advancement. Amazon, Microsoft and now Google have been upgraded while Oracle has been downgraded during a key growth stage for IaaS. In addition, Oracle acquired many companies in the DaaS space which will continue to wane as regulations increase on customers using Oracle for targeted data. Couple this with fierce competitors in the IaaS and SaaS space, and Oracle will see lower than expected earnings this year.

I consult for financial firms. Inquire here.

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i