Zoom Discusses Two Important Catalysts In Q1 Earnings

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Jun 3, 2021,11:31pm EDT

Zoom has had record-breaking earnings results for four quarters now and the market is growing complacent with this stock. The company has (again) posted the highest growth in the cloud software category with revenue at of $956.24 million, or 191% year-over-year growth. The bottom line is also the best in its category (yet again) with adjusted EPS of $1.32 and free cash flow of $454.2 million – which is nearly double the consensus of $280.4 million.

Meanwhile, we saw very little reward in terms of price action. This could change as there was 19 institutional analysts on the call; a surprisingly high number. Zoom also had the Head of Zoom Phone join the call, Graeme Geddes, who announced there are now 1.5M seats of the Zoom Phone, which means the company added 500K new lines in 5 months.

As offices reopen, the growth of the Zoom Phone will be particularly important for investors who want to see more than a web conferencing app. As evidenced by Q1, we continue to see great demand for Zoom Phone, which bodes well for Zoom as they begin to face difficult comps in the second half of 2021.

Geddes also discussed the momentum and accelerating growth the company has observed with Zoom Phone: “At the end of December, we announced reaching 1 million seats of Zoom Phones sold. Well, that momentum continues and I am excited to announce that we have now surpassed 1.5 million seats of Zoom Phones sold as of the end of September. It’s been absolutely amazing to see the growth continue to accelerate.”

In the Q1 Conference Call, Zoom management announced their new device category, the Zoom Phone Appliance. The head of Zoom Phone & Rooms, Graeme Geddes, discussed the new device category in the company’s conference call:

“Our new Zoom Phone Appliances allow our customers to take advantage of the powerful audio and video capabilities of Zoom and they are a great solution for touchdown spaces, huddle rooms and executive offices alike.”

Founded in 2011, Zoom previously described itself as a leader in modern enterprise video communications. The CEO states that Zoom is enabling greater effectiveness in human-to-human interactions over a distance with use cases that are not possible with legacy systems. The key words here are “not possible with legacy systems.”

Zoom’s ongoing goal will be to disrupt all legacy systems with cloud-native communications – and this means every possible method of communication that is not currently done on the cloud and/or is currently on the cloud but is too cumbersome of a process due to walled gardens.

According to Gartner, by 2022, 65% of meeting solutions users will take advantage of SIP/VoIP-based audio-conferencing tools. This is up from 20% in 2017, while 40% of meetings will be facilitated by virtual concierges and advanced analytics. This means prior to Covid, audio-conferencing was predicted to grow substantially.

International Growth

After growing rapidly in the United States, Zoom is now eyeing international expansion as the key to sustaining its trajectory. According to the most recent earnings results, Zoom has been making strategic investments to improve its international presence, which paid off in the Q1 results. The company’s combined APAC and EMEA revenue grew 288% YoY to approximately 34% of revenue, up from 25% a year ago.

Here is what the CEO said on the call:

Number two is really about the international market expansion. There is a huge opportunity. From 25% to more than 30%, I think we do see a lot of opportunities from other, EMEA, APAC, Japan, a lot of opportunities, right.

The company has indicated that international channels are about a year behind the United States:

“And then in terms of international expansion, specifically around the channel, this is a really great question. We had a discussion about that in the last couple of weeks. So, the team has done a really good job in focusing on our U.S. channel strategy, especially around Zoom Phone and building out our master agent program and we are now working on building that out internationally. It’s probably guessing, but we are probably where we were in the U.S. a year ago or so. So, it’s probably about a year behind in terms of our international channel strategy.”

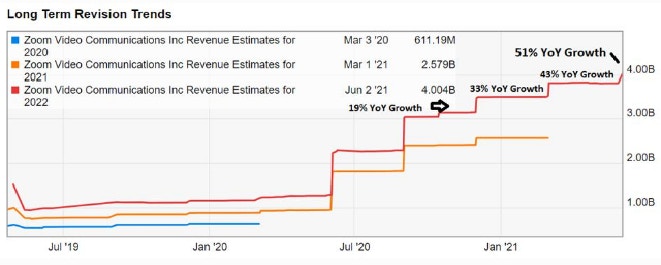

Zoom’s Consensus Raised 3 Times This Year:

At the start of this year, the consensus on Zoom was for 19% year-over-year revenue growth. We have only seen Q1 earnings, thus far, and the company is now expecting 50% YoY growth.

Chart: David Marlin

We’ve emphasized Zoom’s exceptional financials in previous analysis at IPO, in the first month of Covid and prior to this earnings report. In September of 2019, we also stated the company has a viral mechanic prior to the product going viral from shelter-in-place. That’s important to understand because the growth Zoom is reporting is inherent to the product, not due to the one-time event of Covid.

We discussed this in-depth in our analysis on Zoom Video here:

“Competitors such as Cisco Webex, Microsoft Skype and LogMeIn require bulky user accounts, downloaded applications and software, which restricts the one-to-many model. Technically, Google Hangouts also wants you to be logged into a Gmail account. This doesn’t work for enterprise teams on Microsoft Outlook. Corporate teams are also increasingly mobile, switch between devices, and need to join meetings very quickly.

Again, joining a video conference without downloading an application or software may seem minor but it’s actually a driving force in adoption and virality. This micro improvement has an effect on the speed at which Zoom’s conference URLs are shared from one-to-many users.”

There is a saying from John Maynard Keynes that “the markets can remain irrational longer than you can remain solvent.” In this case, I don’t think the market can remain irrational long enough to outlast Zoom’s strong product growth. If Zoom keeps putting up impressive numbers on the scoreboard then the market’s “efficiency” will eventually relent.

More To Explore

Newsletter

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de