I/O Fund’s Overview of 7 Cloud Stocks for Q3 Earnings - December Edition

November 25, 2021

Royston Roche

Equity Analyst

I/O Fund is covering the preview for the second part of earnings for cloud stocks. It includes seven of the leading cloud security, productivity tools and data analytics companies.

We covered the first round of cloud earnings at the beginning of November.

We now cover:

- Zscaler Inc

- CrowdStrike Holdings Inc

- Elastic N.V

- Snowflake Inc

- Okta Inc

- DocuSign Inc

- Asana Inc

These earnings previews help our readers keep track of changes in trends and where to focus for new opportunities. It also helps to hear what analysts are saying about key companies prior to earnings reports.

We noticed that cloud companies with solid stock performance on the run-up to the results beat estimates. For example, Cloudflare stock rose 67% a month before our coverage and the company had a blowout result. We identified in this analysis that the company is adding numerous customers and, also, the trend continued in its third-quarter results.

To better understand recent valuations across cloud stocks and how the sector is positioned, please refer to our analyst Bradley Cipriano’s analysis, “I/O Fund Q3 2021 Cloud Stock Earnings Preview – December Edition”.

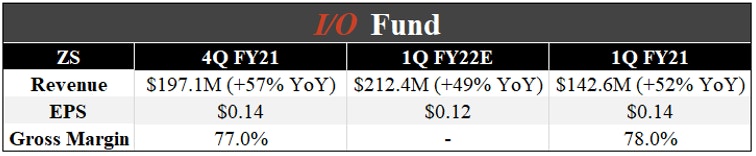

Zscaler – Earnings on November 30

Source: YCharts and Earnings Reports

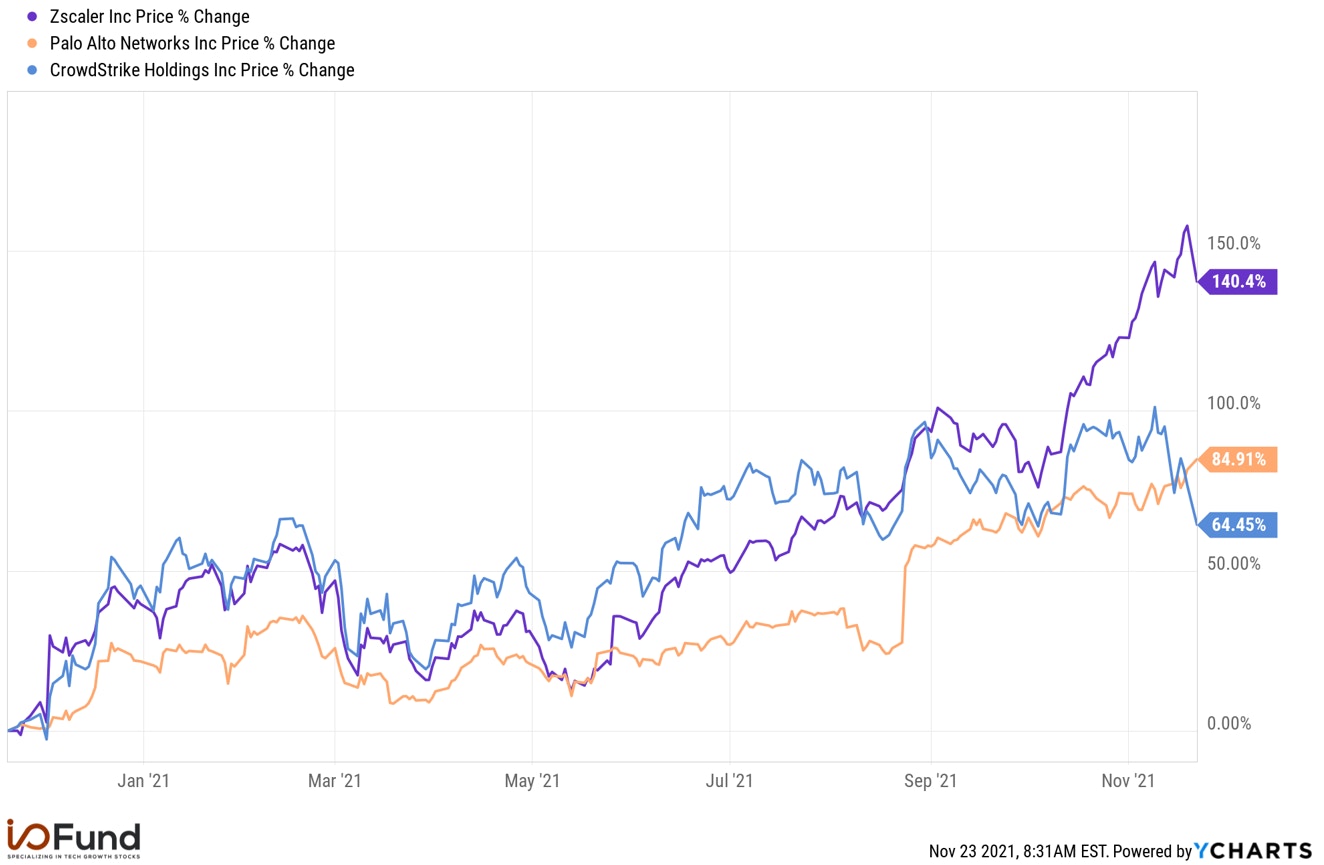

Zscaler Inc has recently rescheduled the release of its results a day earlier as peer companies are releasing on December 1st. The consensus revenue estimates suggest a 49% YoY growth and are slightly higher than the management’s revenue guidance of $210M to $212M. Zscaler is up around 140% in the past year and has been outperforming cybersecurity peers.

Source: YCharts

Mizuho analyst Gregg Moskowitz raised the firm's price target to $385 from $320 and has a buy rating on the company. The analyst says software valuations have "continued their ascent in recent weeks" and that he's raising price targets to reflect recent appreciation in comp multiples.

BTIG analyst Gray Powell has a buy rating and raised the firm's price target to $401 from $324. The analyst states that his discussion with an industry expert and his checks over the last few weeks indicate a positive spending environment across the majority of categories in the space. Powell adds that the expert described the Zscaler business as one that continues to accelerate, following "strong" demand trends observed for the company in October.

Sign up for I/O Fund's free newsletter with gains of up to 1100% - Click here

Daiwa analyst Stephen Bersey initiated coverage of Zscaler with a neutral rating and a $266 price target. The analyst says the stock's trading multiple is near a level that he believes is appropriate. While Zscaler's recent sales growth results have been well above many of its peers, a 28x sales multiple more than accounts for its strong top-line growth and earnings potential.

Please note, I/O Fund is objectively reporting what the Street is saying. We covered Zscaler previously below:

Tech Growth Earnings Review for Q3 2020 - Part 3

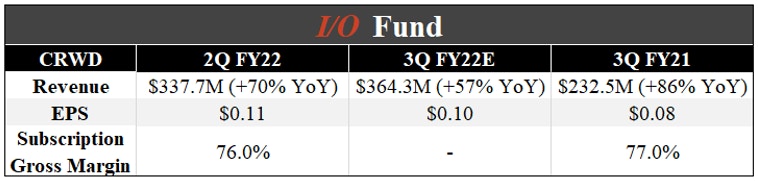

CrowdStrike – Earnings on December 1

Source: YCharts and Earnings Reports

CrowdStrike’s revenue accelerated 70% in the 2Q to $337.7M and subscription revenue increased by 71% YoY to $315.8M. It added a net 1,660 subscription customers, raising the total to 13,080 subscription customers. Recently, it announced new security products to expand its reach in extended detection technology (XDR).

DA Davidson analyst Rudy Kessinger initiated coverage of CrowdStrike with a buy rating and a $320 price target. The analyst is positive on the company's "superior" cloud-native technology that has significant network effects driving sustainable competitive advantages, along with its large and expanding total addressable market. Kessinger further cites CrowdStrike's multiple drivers to sustain high rates of growth and its "significant operating margin expansion" that is likely over the next several years.

Morgan Stanley analyst Hamza Fodderwala has undertaken coverage on the stock with an underweight rating and a price target of $247. He said in a research note that CrowdStrike has benefitted from the shift toward digitalization and remote work over the past two years and gained a leading position in the area of what’s called endpoint detection and response (EDR) security.

However, Fodderwala said that checks within the security industry "indicate CrowdStrike's early leadership position is now increasingly challenged by more competitive next-gen EDR alternatives." Fodderwala said that competitors have come in and undercut CrowdStrike's prices by at least 15% to 20%, and that "this competitive dynamic will make sustaining [CrowdStrike's] current pace of share gains more difficult" through 2022 as working from home becomes commonplace.

Read our previous analyses below:

Nasdaq100 Levels to Watch for the Next Leg Higher

Tech Growth Earnings Review for Q3 2020 - Part 3

Momentum is on CrowdStrike’s Side: Will it Last?

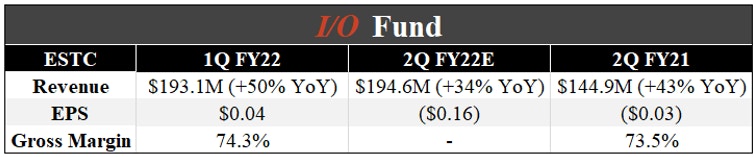

Elastic – Earnings on December 1

Source: YCharts and Earnings Reports

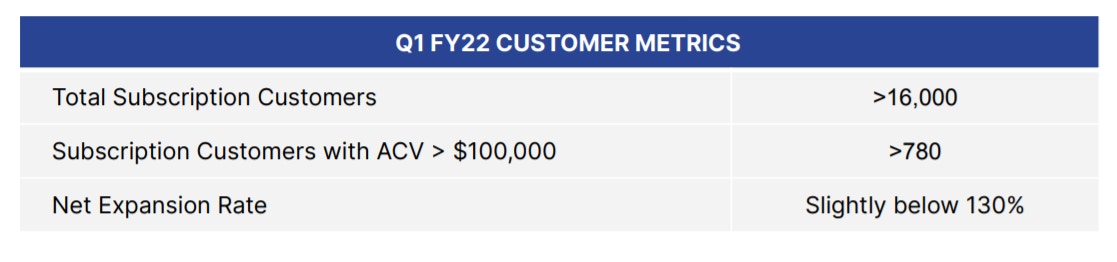

Elastic N.V’s revenue grew by 50% in the last quarter and Elastic Cloud revenues increased 89% YoY to $61.5M (accounts for about 32% of total revenue). The company had over 16,000 subscription customers at the end of Q1. However, growth is expected to slow down in the next quarter. Management’s revenue guidance is between $193M to $195M, representing a YoY growth of 34% at the mid-point.

Source: Investor Presentation

Barclays analyst Raimo Lenschow raised the firm's price target on Elastic to $200 from $185 and kept an overweight rating on shares. In a research note, Lenschow informs investors that over the next few months, investors will move to 2023, their new base year for valuations. For software, "with its high growth rates, this move is important as valuation levels often see a meaningful step down," says the analyst.

Oppenheimer analyst Ittai Kidron has an overweight rating and a price target of $185. The analyst notes Elastic reported a "strong" Q1 well ahead of consensus, reflecting broad-based demand across search, observability, and security; continued SaaS momentum; strong customer adds; and steady expansion metrics.

Read our previous analysis on the stock here: Tech Growth Earnings Review for Q3 2020 - Part 3

Snowflake – Earnings on December 1

Source: YCharts and Earnings Reports

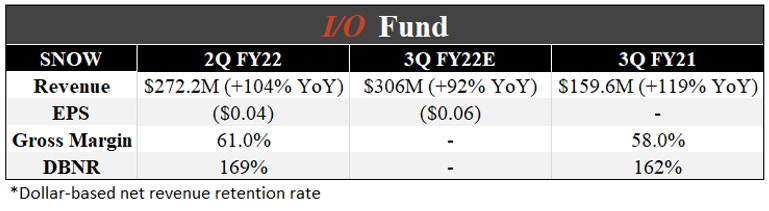

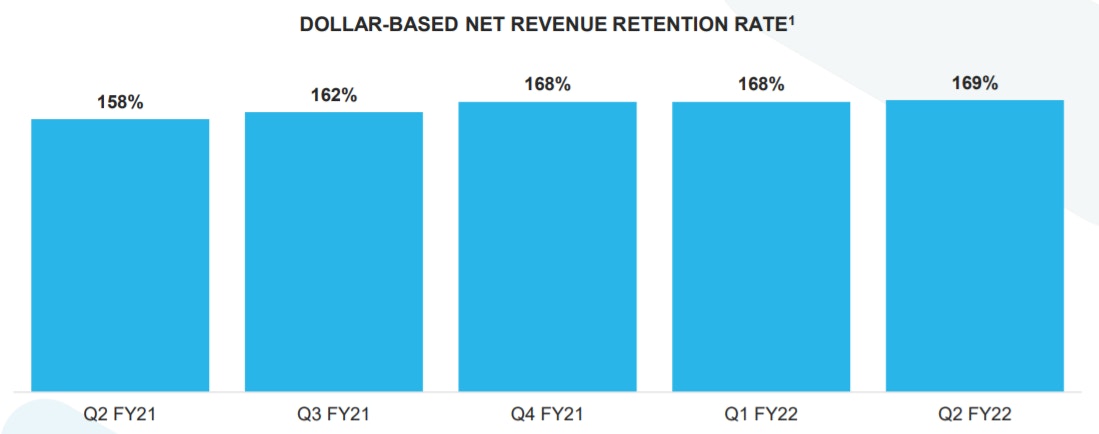

The company’s revenue growth has been solid. During 2Q, total revenue accelerated 104% YoY and product revenue accelerated by 103% YoY to $255M. The remaining performance obligation (RPO) grew to $1.5B at the end of the second quarter. It also reported adjusted free cash flow for the third consecutive quarter.

For the next quarter, revenue is expected to decelerate slightly and management has given product revenue guidance in the range of $280M to $285M.

Source: Investor Presentation

Credit Suisse analyst Phil Winslow initiated coverage of Snowflake with an outperform rating and a price target of $455. Winslow views Snowflake as a true pioneer in cloud-native data analytics and believes the company will play an increasingly important role across the entire data value chain– telling investors, in a research note, that Snowflake is helping drive strong new customer acquisition, robust customer expansion, and attractive unit economics that can be sustained longer than the market appreciates.

Sign up for I/O Fund's free newsletter with gains of up to 1100% - Click here

Rosenblatt analyst Blair Abernethy downgraded the stock from a buy rating to a neutral rating. At the same time, he raised the price target to $370 from $300 and believes most near-term gains are already priced into the stock.

Read our previous analyses:

Snowflake: IPO In-depth Analysis

Podcast: My favorite picks for 2021, Zoom Video, and IPOs/SPACs

Analyzing the IPO Glut of 2020: Snowflake, AirBnB, DoorDash and Roblox

Okta – Earnings on December 1

Source: YCharts and Earnings Reports

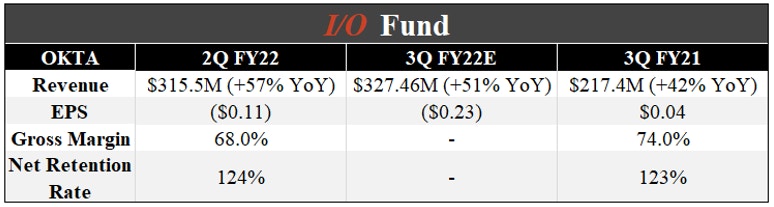

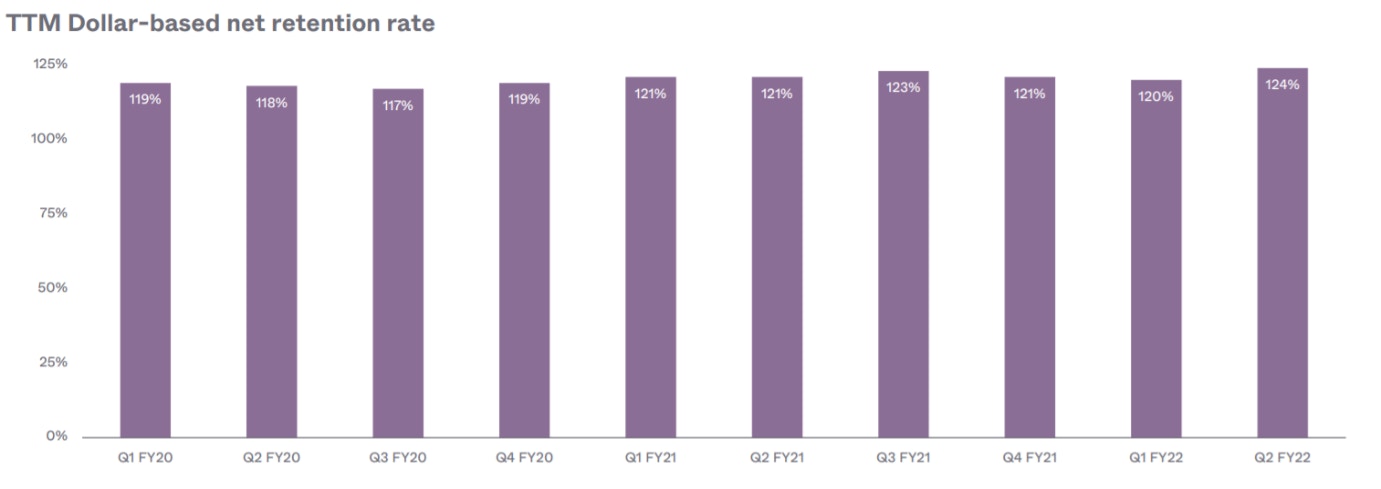

The company’s revenue in the 2Q grew by 57% YoY to $315.5M. On a standalone basis, Okta revenue grew by 39% YoY and it was the first quarter that included Auth0 revenues. The company’s TTM Net Retention rate has been quite stable and, in the most recent quarter, it came at 124%.

Source: Investor Presentation

Morgan Stanley analyst Hamza Fodderwala has updated the company to an overweight rating with a price target of $315. In his words, “After slower topline over the past year, an improving demand environment and more buy-in with developers should drive stronger growth and upside in estimates going forward.”

DA Davidson analyst Rudy Kessinger initiated coverage of Okta with a Buy rating and $315 price target. The analyst says Okta is a "best-of-breed" cloud workforce identity and access management provider that is still in the early innings" of growth. He sees sustainable 35%-plus growth and "compelling" margin expansion through fiscal 2026 for the company.

Read our past analyses on the company:

Podcast with Motley Fool: I’m Bullish on These Trends for 2021

Okta Earnings: More to Squeeze From Valuation?

DocuSign – Earnings on December 2

Source: YCharts and Earnings Reports

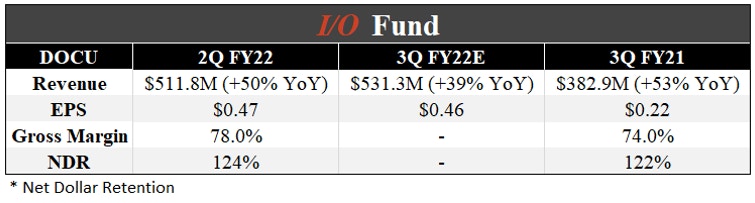

DocuSign’s revenue in the 2Q increased by 50% YoY to $511.8M. The international business grew by 71% YoY to $114M. The company’s Net Dollar Retention rates have improved in the past few quarters, and, for the most recent quarter, it was 124%. The management anticipates revenue of $526M to $532M in the 3Q.

Source: Investor Presentation

Needham analyst Scott Berg raised the firm's price target on DocuSign to $340 from $275 and keeps a Buy rating on the shares. The company reported a "strong" Q2 with "typical" upside to revenue and profitability. He further adds that while DocuSign's sales metrics and growth decelerated sequentially, this was at a much slower rate than the Street was anticipating.

Asana – Earnings on December 2

Source: YCharts and Earnings Reports

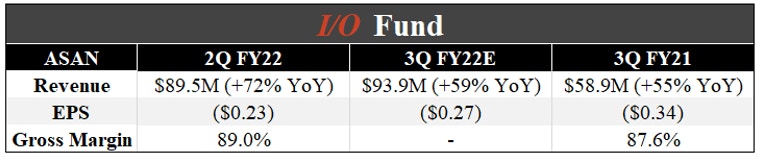

This company’s revenue growth in the 2Q was strong as it grew 72% YoY and 11% QoQ. It added 7,000 net paying customers, exceeding 107,000 in total. Management has raised full-year revenue guidance to $357M-$359M, representing a YoY growth of 57% to 58%, up from previous guidance of $336M to $340M.

Piper Sandler analyst Brent Bracelin raised the firm's price target on Asana to $140 from $85 and kept an overweight rating on the shares. The analyst says multiple third-party data inputs across domain traffic, job postings, and application downloads give him an upward bias to street estimates of 59% growth for Q3 and 33% growth next year. While the stock's risk/reward is less favorable after the 345% year-to-date run, Asana remains a "compelling high margin and high growth model that is still in the nascent stages of adoption with fewer than 2 million paid users.”

Jefferies analyst Brent Thill downgraded Asana to Hold from Buy with a price target of $135, up from $115. The analyst cites valuation for the downgrade, with shares up 348% year-to-date. He continues to view Asana as a "differentiated solution for work management in a large and growing market" but says the valuation is full at current levels. Thill looks to get constructive at a "more reasonable valuation."

You can read our previous analysis here: Asana Setup (5/20/21) - up 85% in a month

I/O Fund is comprised of a team of analysts who share their research publicly as they build a portfolio of 30 stocks. Our team has record results for a retail Fund and we also have four-digit gains on some of our free newsletter coverage. You can learn more about our premium service by clicking here or sign up for our free newsletter here.

Disclaimer: This is not financial advice. Please consult with your financial advisor in regards to any stocks you buy.

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per