Winning Cybersecurity Stocks From Q1 Earnings

June 14, 2022

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Jun 10, 2022,12:19am EDT

The market has indiscriminately penalized tech stocks across the board and cybersecurity stocks are simply caught in the cross fire. Q1 earnings proved that cybersecurity stocks are insulated from supply chain issues and remain a number one priority across corporate budgets. Specifically, cybersecurity-related companies reported top line and bottom line beats plus a handful raised guidance while consumer-related tech and less cash efficient cloud verticals lowered or missed guidance this past quarter.

The analysis below looks at why cybersecurity is a more insulated trend and a few of the cybersecurity stocks that stood-out.

Cybersecurity Budgets are Expanding in 2022

Enterprise spending is expected to increase in 2022 from the previous year, according to Chief Information Security Officer (CISO) surveys. Considering the level of cloud spending in both 2020 and 2021, an increase on already high budgets is impressive. The CISO survey states that 44% increase budgets to increase in 2022 compared to 41% in 2021 and only 2% expect a decrease compared to 6% the previous year.

In a similar study from PricewatershouseCooper, 69% predict a rise in cyber spending for 2022 and 26% expect a surge of 10% or higher spending year-over-year. This survey was done across a broader C-suite and executive sampling.

According to a Gartner survey, 88% of the Board of Directors viewed cybersecurity as a business risk. According to Paul Proctor, VP at Gartner, “The influx of ransomware and supply chain attacks seen throughout 2021, many of which targeted operation- and mission-critical environments, should be a wake-up call that security is a business issue, and not just another problem for IT to solve.”

Gartner has also reported from a CIO survey that cyber and information security is the top priority of planned investments for companies for 2022 with 66% planning to increase investments.

Monika Sinha, VP at Gartner, said, “There is a continued need to invest in cybersecurity as the environment becomes more challenging. A high level of composability would help an enterprise recover faster and potentially even minimize the effects of a cybersecurity incident.

According to Global Market Insights, the cybersecurity market is expected to reach $400 billion by 2027 from $170 billion in 2020, representing a compound annual growth rate (CAGR) of 15% during this period. The report mentions that rapid technological advancement is driving the shift to cloud-based solutions. The increasing use of the digital world increases cybercrime, which increases enterprises' spending on cybersecurity.

Cybersecurity Stocks Report Strong Q1 Earnings

We had stated on Fox Business News that a small cohort of companies emerged this past quarter to increase the top line while also reporting narrowing losses on the bottom line. We feel not losing site of opportunities during selloffs is how generational wealth is built.

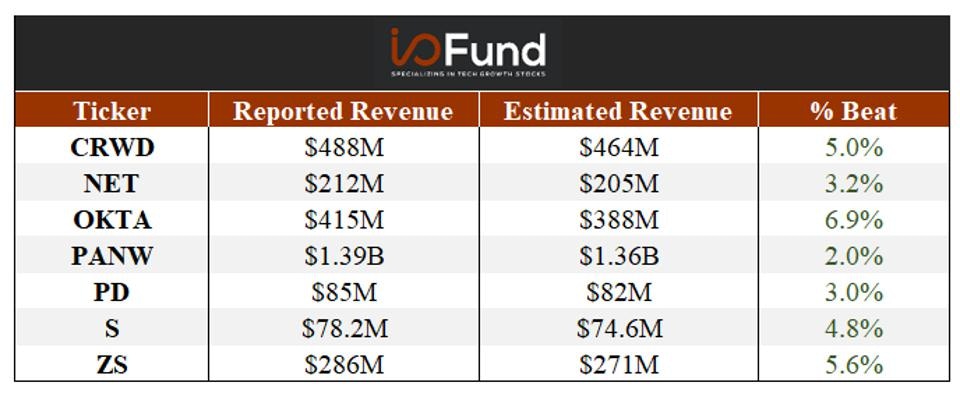

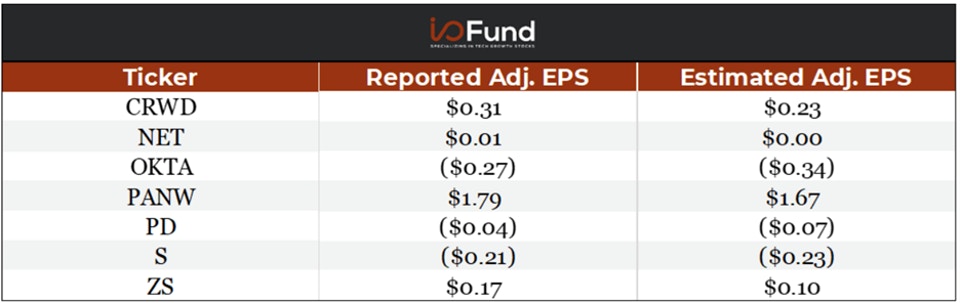

This quarter, we saw on average a 5% top line beat above guidance across major cybersecurity stocks, including Crowdstrike, Okta, SentinelOne and Zscaler. This is coupled with a beat on the bottom line across all major cybersecurity stocks with both Crowdstrike and Palo Alto Networks proving the sector can be profitable and also increase cash efficiency at scale.

Source: YCharts and Investor Relations (I/O Fund)

Zscaler’s Q3 FY 2022 revenue accelerated by 63% YoY to $286.8 million in the recent quarter. It was the seventh consecutive quarter of above 50% growth. The growth was led by the strong adoption of the company’s Zero Trust Platform. Zscaler has a free cash flow margin of 15% and management expects this to expand to a free cash flow margin of 20% for the full-year ending July 2022.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Credit Suisse analyst Phil Winslow lowered the company’s price target to $310 from $410 and kept an Outperform rating. He said, “Zscaler reported strong Q3 results, with revenue growth greatly surpassing consensus estimates and operating margins and billings also exceeding consensus. He believes a meaningful runway exists for the company.

CrowdStrike stole the show this quarter with a beat on both top and bottom line; but it was the raised guidance line that stood out. Revenue accelerated by 61% YoY to $487.8 million and annual recurring revenue (ARR) also accelerated by 61% YoY to $1.92 billion. This company has an impressive cash flow margin of 32%.

Crowdstrike also raised revenue guidance for FY 2023 ending January to $2.19 billion to $2.21 billion from the earlier guidance of $2.13 billion to $2.16 billion, representing a YoY growth of 52% at the mid-point of the revised guidance. It also raised guidance of adjusted income from operations from a midpoint of $300.5 million to $312.2 million. Similarly, the adjusted net income from a mid-point guidance of $262.4 million to $289 million.

Morgan Stanley analyst Hamza Fodderwala upgraded the stock to overweight from equal weight. The analyst said, “CrowdStrike (CRWD) is seeing further adoption based on conversations with Chief Information Officers and is seeing 100% growth from its non-endpoint offerings, which now account for 15% of its annual recurring revenue, showing that its total addressable market could be $30B bigger than first thought.”

(I/O Fund)

Cloudflare company reported 54% revenue growth, beating estimates by 3%, with 49% growth expected next quarter. The company raised full year revenue guidance to $957 million, at the mid-range, for growth of 46%.

There is additional supporting evidence that growth is not an issue for Cloudflare, including remaining performance obligations (RPO) up 57% year-over-year and dollar-based net retention up 400 bps YoY. Customers paying over $100K increased 63% year-over-year to 1,537. This outpaced total customer growth of 29%. Large customers contributed 58% of revenue. There was solid growth in the >$500K customer base of 68% year-over-year growth, and >$1 million customer base grew by 72% year-over-year.

Needham analyst Alex Henderson has kept the buy rating but lowered the company’s price target to $100 from $245. He reduced the target multiples in his valuation model to enterprise value to expected FY23 sales of 23-times, down from 64-times, given the sell-off in growth equities, but maintains that Cloudflare should be a core long-term holding in all growth portfolios and recommended that investors buy the recent weakness.

Palo Alto’s Q3 FY 2022 revenue grew by 29% YoY to $1.4 billion. The billings and remaining performance obligation grew by 40% to $1.8 billion and $6.9 billion, respectively. The management mentioned in the earnings call that it was the highest billings growth in the past four years. The company raised the full-year ending July revenue guidance from a mid-point of $5.46 billion to $5.49 billion, representing a YoY increase of 29% at the mid-point.

Wedbush analyst Daniel Ives lowered the company’s price target to $580 from $660 and kept an Outperform rating on the shares. He said, “The shift to cloud is a massive tailwind for Palo Alto as the company is in the right spot at the right time to benefit from this multiyear tidal wave of cybersecurity enterprise spending.”

Conclusion:

Cybersecurity is a top priority in budgets and the results are showing up. We found a strong pattern with cybersecurity stocks sustaining growth rates and strong bottom lines this quarter. The cybersecurity sector overwhelmingly beat estimates compared to other sectors within tech and investors may want to take notice.

Royston Roche contributed to this article.

More To Explore

Newsletter

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i

Google TPU v8 vs Nvidia: How Inference Is Rewriting the AI Market

In April, Google announced it would begin selling its TPUs to select third-party data center operators, which is something the market has anticipated for nearly a decade. The TPU-versus-Nvidia-GPU deb

The AI Networking Stock That Beat Nvidia by 7X YTD for Returns of 135% YTD

AI networking stock Lumentum is among the key I/O Fund winners in 2026. We allocated heavily to LITE in January—a month before Nvidia backed the company. While most investors couldn’t stomach taking a