Zoom May Be the Best Silicon Valley IPO of the Year

April 16, 2019

Beth Kindig

Lead Tech Analyst

This post originally appeared on FATrader.com on April 16th, 2019. Beth later appeared on Yahoo Finance discussing this analysis.

This may be hard to believe, but on Thursday, Silicon Valley will have a company go public that is already profitable. If you’ve used Cisco’s Webex for meetings, then you’ll understand Zoom. The company provides web conferencing that is simple for users to join and has a lot of features to assist in virtual meetings.

Zoom has a “bottoms-up” viral customer base, which means junior employees evangelize the service at the company. These are often some of the most loyal customers. For instance, 55% of $100,000 or higher revenue customers were started with a single employee’s free trial.

Financials

Zoom’s financials outperform successful software-as-a-service companies on the public markets today, such as Workday and Okta. Here’s a snapshot of the S-1 Filing showing $60M in revenue in 2017, $151M in revenue in 2018 and $330M in revenue in 2019. The company has been posting 100%+ revenue growth for three years with gross profit margins in the high 70% to low 80% range compared to more mature SaaS companies currently on the public market posting increasing net losses (Okta and Workday).

In the year ending January 31st, 2019, Zoom became profitable with $7.58 million in net income or 3 cents EPS. The year prior, Zoom posted a net loss of $4.8 million. Compare this to Okta’s net loss of $125M on similar revenue this past year or Workday’s net losses of $418M on approx. $2.8B revenue.

Zoom’s IPO price continues to change daily. The shares are now being priced 8 percent higher than previously estimated last week with a valuation around $9 billion. This is up 9x from the company’s most recent private funding round, which was priced at a $1 billion valuation. SalesForce Ventures has agreed to buy $100 million Class A stock at the IPO.

Zoom has disrupted Cisco’s WebEx, which is clunky and more intensive software for video conferencing. Some Wall Street analysts have speculated Cisco and Microsoft are a threat to Zoom, although the opposite is true.

Zoom’s CEO Eric Yuan, owns 19 percent of the stake in the company, and was a former engineer at WebEx before it was acquired by Cisco. On a similar note, I would not be surprised if SalesForce acquired Zoom given its large stake and the loyal customers Zoom could bring to a predominant SaaS platform. Yuan has adamantly stated he would not sell a company after his experience with the WebEx acquisition, although this may be too idealistic for a standalone conferencing product. Long story short, it is likely Zoom will agree to an acquisition in the future.

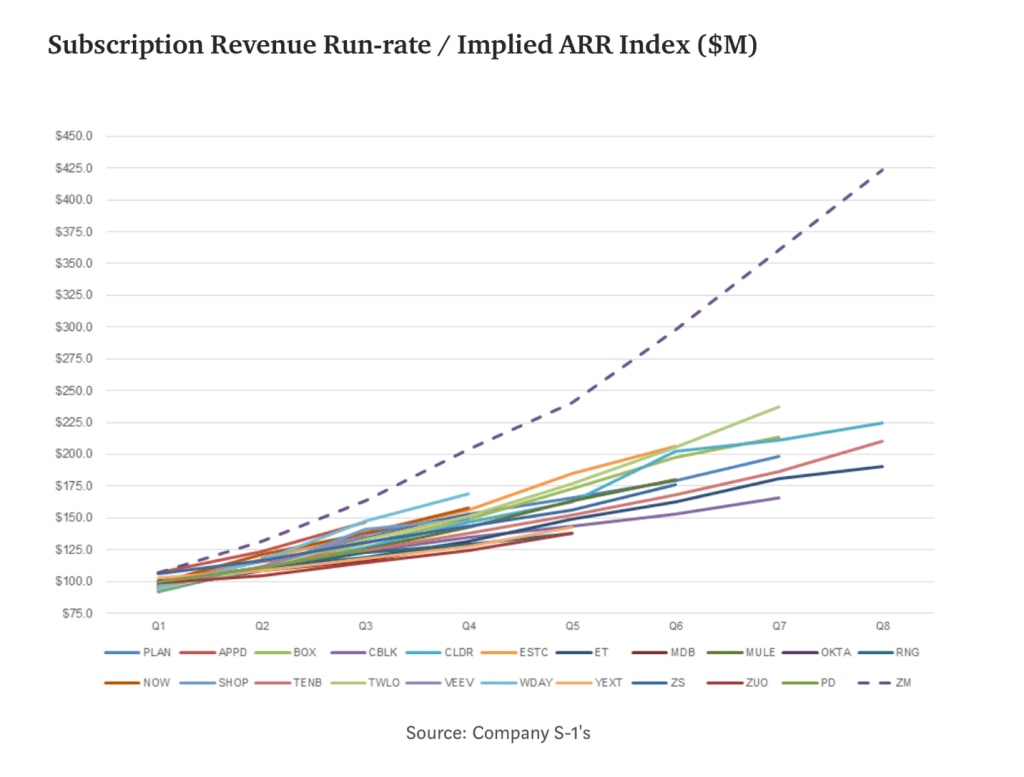

SaaS Metrics

There is a breakdown of Zoom by venture capitalist Alex Clayton of Spark Capital. It bears mentioning that many of the software-as-a-service VCs support one another in public offerings and Clayton is a little too enthusiastic about Zoom. However, Clayton does a good job of visualizing the data. I’ll summarize some of what he says here and point out a few things you should consider when looking at the data that comes from the VC side.

Software-as-a-service (SaaS) has unique key metrics that venture capitalists look for when privately funding a SaaS startup. Subscription revenue run-rate is one metric used, although it can be overly simplistic.

Annual Revenue Run Rate = Monthly Revenue * 12 months

ARR does not account for churn or growth. Zoom’s ARR likely looks better than the more mature companies on the public markets (which are contrasted below) because Zoom is a smaller company and has gone through periods of hyper growth. For this chart to be completely accurate, you would have to compare growth from the same year of a company’s inception as Zoom is going public early compared to the other companies in this chart, and therefore, demonstrates hyper growth compared to a more mature company that files to go public.

Private investors typically calculate the monthly recurring revenue, which calculates the amount of revenue you have in the beginning of the month plus the revenue you gain during the month minus downgrades or customer churn.

Zoom has an advantage over many other public SaaS companies by posting positive net income. Many of the SaaS companies on the market today trading at 30x price to sales are not profitable. Okta, especially, may appear overvalued after Zoom’s IPO as the company posts similar annual income but with staggering net losses. Zoom is not in the same category as Okta, as Zoom is web conferencing and Okta is identity management. However, they share the same SaaS subscription-based business model and more financial clarity for investors in this business model will likely shift perception of how a SaaS company should perform on the public markets. Basically, Zoom’s financials are a safer bet.

Takeaway

Zoom is likely to be a popular IPO due to being a profitable SaaS company. With many companies like Okta, WorkDay, and Twilio trading at 15-30 Price to Sales ratios, and many not profitable, you can image the excitement that will follow Zoom. I am going to allocate a small percentage to Zoom’s IPO, provided it remains at a $9 billion valuation. I am considering a short on Okta as of Zooms’ S-1 Filing as the stock has climbed 80% from December lows.

As many FATrader analysts have pointed out, IPOs are risky.

I am a tech analyst, not a financial advisor.

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per