COVID’s Impact On Cloud Software Stocks

October 13, 2020

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Oct 8, 2020,11:23pm EDT

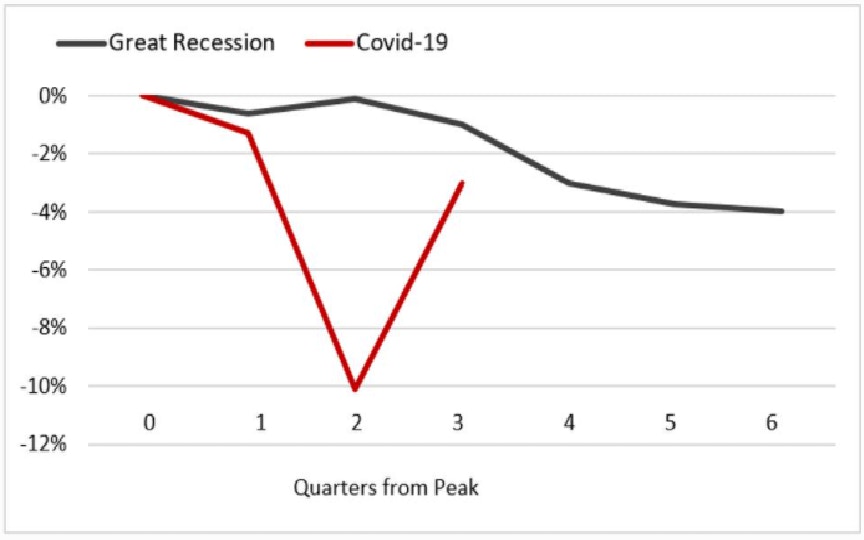

Rebound numbers from Q3 will look spectacular following the paralyzing effects of strict shelter-in-place orders in Q2. The economy is officially in a recession after posting two negative quarters of GDP growth at (5%) in Q1 and (32%) GDP in Q2. The latest estimate from Atlanta’s Fed GDPNow for Q3 2020 is showing a record rebound of 35.3%.

This represents an increase of 7.9% quarter-over-quarter and 3.1% below the pre-recession high. For comparison purposes, the Financial Crisis of 2008 bottomed at 4.0% below its pre-recession during the third and fourth quarters of its recession.

The chart above shows the projected Q3 rebound of 35.3% from the Atlanta Fed’s GDP Now released on October 6th, 2020.

Cloud and IT Budgets: Staying Objective

Some will argue the market is not the economy (which is true), however, cloud software can’t stop the spiraling effects of lower IT/cloud spending and tighter budgets that follow a weaker economy. One area that companies might reduce costs is to trim down on the number of cloud software and tools they use. Unemployment could exacerbate this if the subscriptions are paid per employee.

Spiceworks recently released a survey that shows 80% of IT-decision makers expect IT budgets to grow or stay steady over the next 12 months. This supports the notion that even during periods of uncertainty, IT and cloud are central and critical to operations.

With that said, the decision-makers polled stated the primary drivers in IT budgets are noted to decrease year-over-year except covid-related budget allocations. In the past, drivers such as employee growth, security concerns, and the need to upgrade IT infrastructure were expanding to support higher budgets.

Perhaps more indicative is the decrease in revenue that is being forecast across the 1,000 IT-decision makers that were polled. One-third of businesses expect revenues to increase from 2020 to 2021 which is down from 58%. One-third also expects revenues to decrease YoY which is up significantly from the previous two years when only 7% expected a decline in revenue.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

As the survey illustrates, cloud software will be more resilient than many other categories. However, there will be some cloud software companies that see an impact on one side of the equation or both sides of the equation – this means either fewer new customers or more churn or downgrades in existing customers or both. There are three points where weakness can occur (fewer sign-ups, churn, and downgrades). Notably, companies that have annual recurring revenue will be more protected.

In this article, we go back through earnings calls to see what management is saying in each respective company:

These companies had positive things to say about budgets …

Twilio:

“Our customers in nearly every industry have had to identify new ways to communicate with their customers and stakeholders, from patients to students to shoppers and even employees essentially overnight… Twilio was built for this. The things we've always brought to our customers, digital engagement software agility and cloud scale are enabling organizations to innovate now even faster than ever. Messaging, email voice and video are allowing companies to engage with their customers safely while reimagining their digital engagement strategies in ways that will be resilient for years to come…And now we're seeing the strength of that diversification really play out during COVID, as we've seen new industries, new use cases offset some of the more negatively impacted areas.” - CEO Jeff Lawson Q2 Earnings Transcript (8/4/20)

Fastly:

“The need for a trustworthy and modern edge platform has never been greater. Developers and security operators are at the center of the transformation and they can only drive transformation effectively if they can build quickly and securely…Fastly is in this unique position to be a usage-based model with the most innovative companies in the world. And so when you stack on, the most — the largest innovators and you look just at their results, whether it be Pinterest or Shopify, the list goes on and on.” CEO Joshua Q2 Earnings Transcript (8/5/20)

Crowdstrike:

…. “even in this challenging macroeconomic backdrop, cybersecurity is mission-critical and more important now than ever, as the threat environment escalates and the attack surface continues to grow…as organizations rapidly adapt to the new distributed workforce paradigm and move more workloads to the cloud, it has become clear that the endpoint is the new security perimeter, and the inadequacies of the complex brittle patchwork of legacy solutions continues to be exposed.” — CEO George Kurtz Q2 Earnings Transcript (9/2/20)

Bandwidth:

“The second factor driving our outperformance was the increased usage driven by COVID-19-related remote work requirements which peaked in April and thereafter dissipated throughout the quarter, but remained at elevated levels as compared to pre-pandemic period…While it is becoming increasingly difficult to differentiate COVID-19-related usage from organic usage growth, we estimate that COVID-19 revenue impact in the second quarter to be in the range of $4.5 to $5 million.” — CFO Jeff Hoffman Source: Q2 Earnings Transcript (8/2/20)

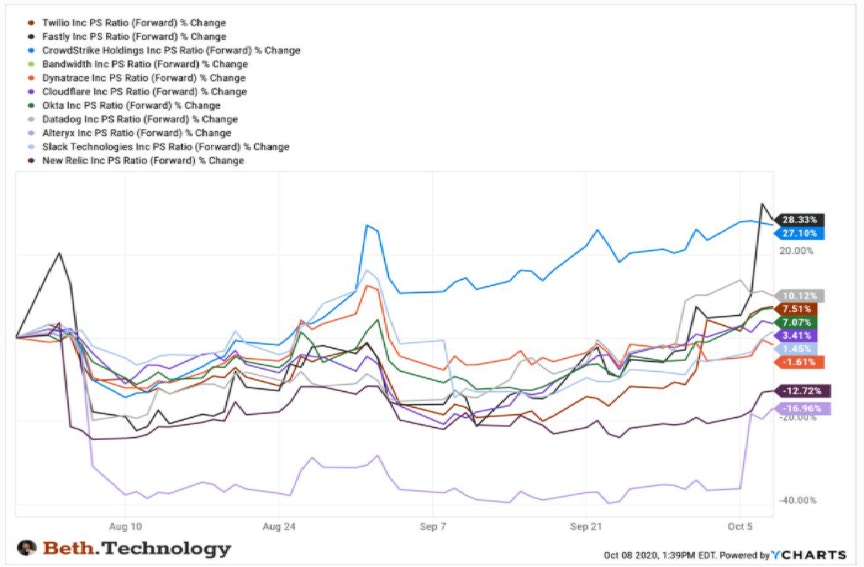

Price-to-sales change for the stocks covered in this analysis since the start of cloud software earnings reports on August 1st, 2020.

These companies were more some headwinds and some tailwinds cancel each other out for a neutral outlook …

Dynatrace:

“Despite the global pandemic continuing to delay some new sales cycles…Customers tell us that they consider Dynatrace an essential element of executing a successful digital transformation as they drive towards greater agility, efficiency, and business effectiveness…what we’re seeing is that as digital transformation accelerates, the need for a Dynatrace class solution even goes up. And that’s what we saw the beginnings of it in our fiscal Q1 and we continue to see it as we look out into Q2 and beyond with the sales cycles we’re now in.” - CEO John Van Siclen Q1 Earnings Transcript (7/29/20)

Cloudflare:

“We believe the pandemic forced companies [to] distort their vendors into two buckets, nice to have and must have. All indications from the quantitative metrics we’re watching as well as the qualitative conversations we’re having with customers are that Cloudflare is squarely in the must have bucket…COVID-related concession requests peaked in early April and had been tailed off. We came in well below what we forecast for potential downside…our sales cycle has kicked up by a few days in Q1 and trended back down in Q2 and remains well under a quarter and at the low end of our historic range.” - CEO Matthew Prince Q2 Earnings Transcript (8/7/20)

Okta:

“So we're obviously pleased with the results of the quarter and the strength in the quarter. We did see those mild pandemic headwinds. Frankly, they were not as strong as we thought they would be. And so I think what the movement of companies to decentralizing how they're working with the fact that companies are seeing with their customers, they're transitioning to more of an online relationship with those customers are both just big impacts for us, big tailwinds for us that are just accelerating some of the overall mega tailwinds we've talked about before, and that's really what's happening.” -Bill Losch, CFO Q2 Earnings Call (8/27/20)

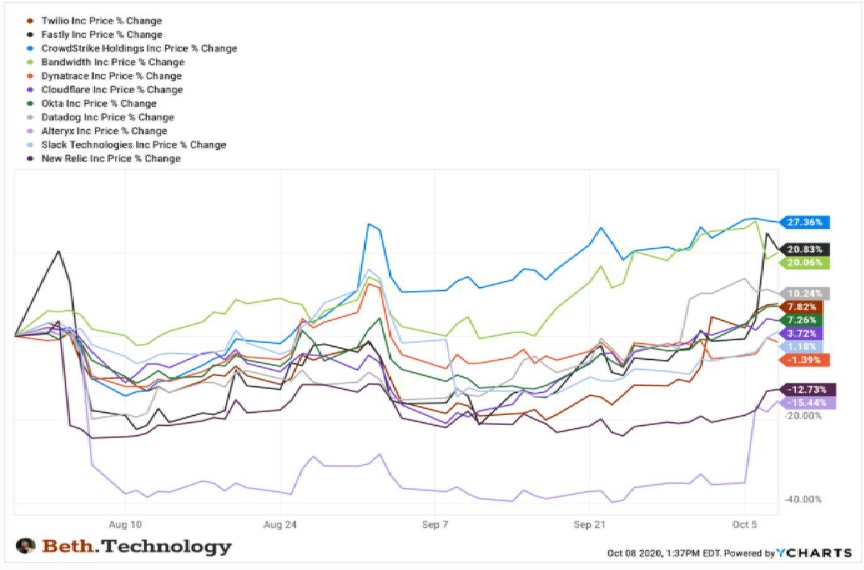

Change in price for the stocks covered in this analysis since the start of cloud software earnings on August 1st, 2020.

These companies were more conservative in their comments about budgets …

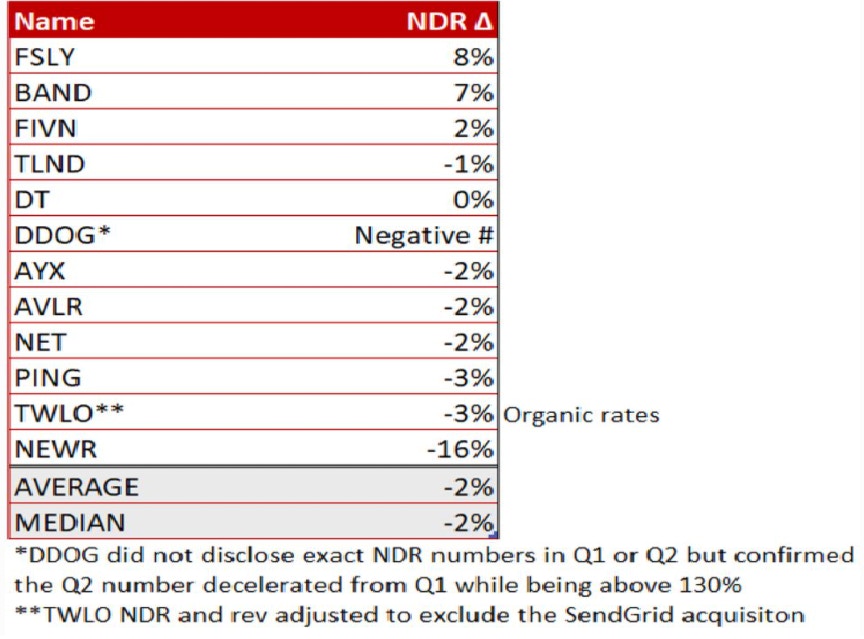

Datadog:

“The macro environment did have some impact on our top line results, and in particular on growth of existing customers. Our customers continue to grow usage of our platform in Q2, but the rate of this growth was below the trends we saw before the pandemic. This dynamic was primarily seen in our larger customers, who already had sizable cloud environment. Given macro uncertainty, we saw these customers look to conserve cash where they still could and therefore, optimize the consumption of cloud infrastructure…To put it plainly, customers with large cloud deals from AWS, Azure or GCP look for short-term savings. Note that this is not a new motion, as we see many enterprises go through these optimization exercises on a regular basis. What was unusual this quarter was to see a large number of companies going through it at the same time.” -CEO Olivier Pomel Q2 Earnings Transcript (8/7/20)

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Alteryx:

“The global dislocation experienced as a result of the COVID pandemic followed by shelter in place orders, altered our customers buying behaviors in Q2. We observed notable changes such as higher levels of scrutiny on spending across all sectors resulting in longer sales cycles, smaller deal sizes and less favorable linearity in the quarter…Based on what we see today, we do not anticipate a material improvement in business conditions during 2020.” - Former CEO Dean Stoecker Q2 Earnings Transcript (8/7/20)

UPDATE (10/5): Alteryx currently expects that total revenue for the third quarter ended September 30, 2020 will be in the range of $126.0 million to $128.0 million, representing 22% to 24% year-over-year growth, ahead of the previously issued guidance of $111.0 million to $115.0 million

Slack:

“In Q2, calculated billings were impacted by approximately $4 million of COVID-related concessions and contract duration related headwinds. This brings the total concessions-related billings headwind in the first half to approximately $11 million.

Although we’ve seen a slowdown in concession requests over the past couple of months, it’s still not possible to forecast the effects of the pandemic on our customer base over the next few quarters. We plan to continue to help customers manage through this unique time and expect calculated billings to be negatively impacted and less useful as a measure of underlying growth during the COVID-19 crisis.” -Allen Shim, CFO Q2 Earnings Call (09/09/20)

New Relic:

“On the other side of the equation of customers are reducing their spend. So in the quarter, that number was also – we had $5 million to $6 million of downgrades that were COVID or macro related.” – CFO Mark Sachleban Q1 Earnings Transcript (8/5/20)

Conclusion:

We think it’s important to remain objective when evaluating cloud stocks. They have already proven to be affected by budgets per second quarter earnings calls and this could extend into Q3 for cloud software business models that are dependent on (1) number of employees, (2) new customers, (3) low churn, or dependent on (4) upgrades.

IDG released a survey stating that 81% of survey respondents were using cloud infrastructure compared to 73% in 2018. Even more bullish than the universal acceptance of cloud is that only 9% of environments are cloud-only with the large majority having a mix of cloud and on-premise at 83%. This will grow to 16% cloud-only over the next eighteen months.

Therefore, regardless of any temporary setbacks, cloud as a category still has quite a bit of runway.

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su