Q3 Earnings: Zoom Video, Okta, Snowflake, Crowdstrike And Elastic

December 26, 2020

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Dec 10, 2020,11:25pm EST

In this analysis, we review the recent earnings reports from Zoom Video, Okta, Snowflake, Crowdstrike, ZScaler and Elastic.

Zoom Video Q3 Earnings

Zoom Video provided a nearly flawless earnings report for the first full quarter that followed initial work-from-home orders. The company reported lower-than-expected churn and market-leading growth on both an annual and quarterly basis. Notably, margins were thinner on both a YoY and QoQ basis due to free accounts. Regardless, it's hard to find fault with Zoom Video's current level of profitability in relation to other tech growth stocks (outlined below).

Strong forward guidance also provides a glimpse into Zoom's traction as the company expects revenue growth to continue at a similar rate year-over-year and also quarter-over-quarter. Revenue grew 367% in Q3 with customers that have more than 10 employees growing 485% year-over-year.

Quarterly revenue is at $777 million or a $3 billion run rate – or 500% growth from FY2019 revenue. Quarterly revenue beat the top-end of guidance at $690 million with the company reporting "lower-than-expected" churn. Customers generating more than $100,000 in trailing 12-months revenue grew 136% year-over-year for an increase of more than 300 customers compared to Q2.

The blend of Zoom Video having virality across consumers from its freemium model combined with enterprise is the company's strength strategically as the competitors do not have the virality component. In Q3, customers with more than 10 employees represented 62% of revenue with net dollar expansion rate of 130%. Globally, Zoom exhibits strong growth, as well, with revenue from APAC and EMEA growing 629% year-over-year.

Gross margins were a weakness in the report at 68.2% compared to 82.9% last year and 72.3% last quarter. The company is providing the service for free to many users including K-12 schools during the pandemic. From my perspective, the temporary margin hit in exchange for virality and establishing consumer behavior is a good trade-off.

Adjusted operating margins improved year-over-year but were slightly down quarter-over-quarter at 37.4%. Adjusted EPS was $0.99 which exceeded guidance by $0.25. RPO totaled $1.6 billion, up 215%, from $517 million year-over-year which is a strong sign the growth will continue. The company ended Q3 with $1.9 billion in cash (nearly unheard of for a tech growth company at this stage).

Guidance for the next quarter is in the range of $806 million to $811 million with adjusted earnings of $0.77 to $0.79 EPS. Fiscal year guidance is for revenue of $2.57 billion to $2.58 billion, representing 314% year-over-year growth (currently company is in Fiscal Year Q3 2021 and the fiscal year ends next quarter). The adjusted operating income for FY2021 is forecast to be $865 million to $870 million for nearly 900% growth and equal to $2.85 to $2.87 EPS.

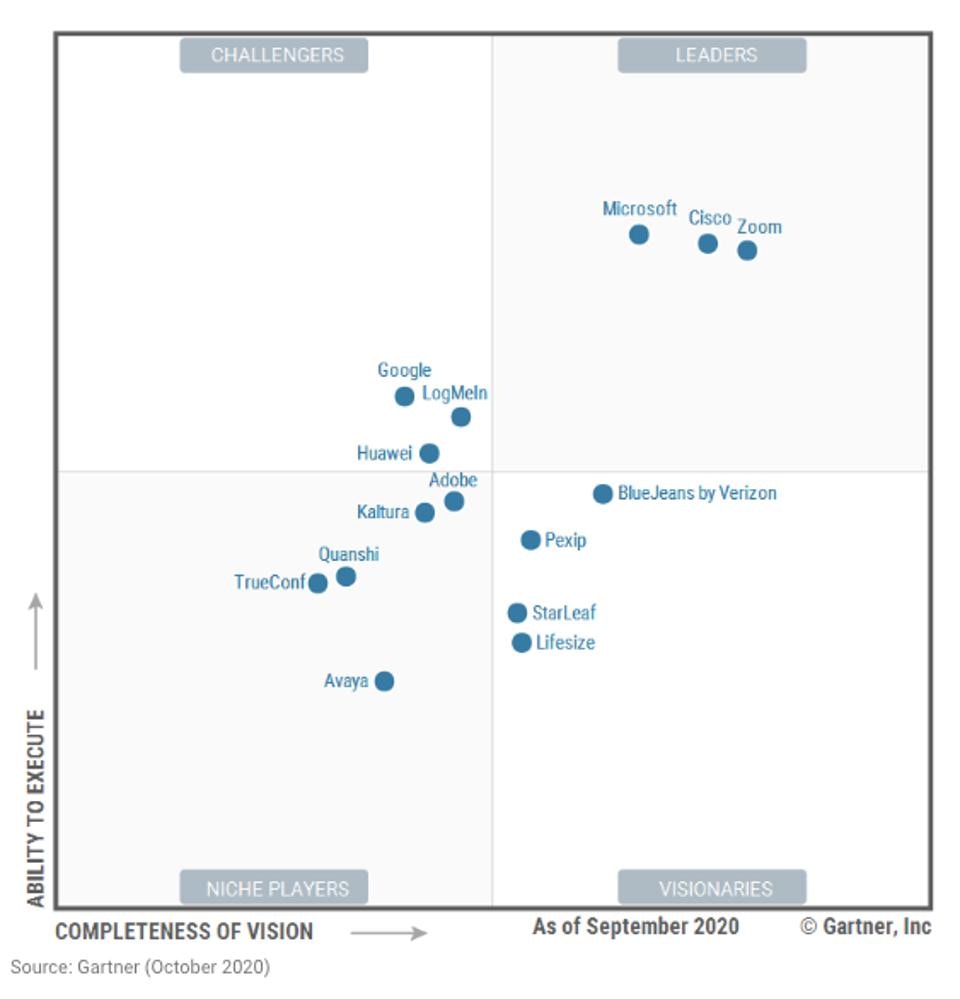

The Gartner report that Zoom Video references canbe found here. The bigger revelation is not that Zoom Video is listed as a leader but that Gartner forecasts only 25% of enterprise meetings will take place in-person compared to 60% today. The analyst firm also predicts that 74% of companies plan to shift to more remote work — (keyword here is more – not entirely shift)

Source: Gartner (2020)

The interesting piece about the chart above is that Zoom Video leads enterprise players Microsoft and Cisco but is also in a wide lead for consumer. The consumer traction may be Zoom's biggest tailwind as consumer behavior will be hard for a competitor to change.

The strengths that Gartner sees include zoom's user-centric design, service reliability and flexible consumption model. Zoom is also moving into verticals, such as healthcare and financial services, to add to its popularity in education.

The primary risk for Zoom Video is security. As I've stated a few times, it's common for an enterprise to not offer end-to-end encryption as the employer prefers to access the data on their employees. In response to the criticism, Zoom Video offers end-to-end encryption for accounts with more than 200 users.

In another Gartner report for Unified Communications-as-a-Service, Zoom appears for the first time due to the recent launch of Zoom Phone and receives a leadership position with its first mention in the UCaaS report. That's a significant entry. Zoom Video offers Zoom Phone at no additional charge and has secured a partnership with ServiceNow. The company is also partnered with Pinterest on hobbyist classes. Despite the Zoom Phone service being relatively new, it offers a 99.999% availability SLA target.

Source: Gartner (2020)

Visionary CEOs tend to better than competitors who lag because they have a vision for what the space will need next. We see many products rolling out of Zoom that challenge the way video conferencing is done today. As pointed out in the earnings call, Rakuten has partnered with Zoom for the broader UCaaS offering of Rooms and Phone. This is a leader in internet services with 1.4 billion members globally.

OnZoom is a product in beta that will help creators monetize fitness classes, concerts and music lessons. There is also an event discovery feature. Recently, Pinterest has announced a partnership to help creators on their platform reach a larger audience with Zoom.

Analysts on the recent earnings call seemed especially excited about Zoom's ability to sell into the Global 2K with international expansion being a large focus. From Rakuten's recent partnership, plus Lumen/Centurylink and Deutsche Telecom, these larger partnerships with tech providers are my favorite catalyst moving into next year. Essentially, they see Zoom as the best product available (and least threatening) to integrate for unified communications and voice. This is the best evidence that Zoom Video is not a fleeting pandemic stock as large telecommunications providers shift towards cloud.

Zoom Rooms is a software-defined video conferencing system. Eric Yuan is likely tapping into his experience at Cisco as this will be one of the main competitors he takes on with this move to eradicate conference hardware.

The software-defined solution also extends to kiosks for virtual receptionists, will allow for voice control including an Alexa integration and advanced AWS console. The Smart Gallery will use AI to create a gallery-view of participants for hybrid workforces to where the viewpoint of the camera creates the best imaging possible and other whiteboard features are coming in 2021.

Okta

According to most standards, Okta's earnings report was solid and resulted in an uptick in the stock price. However, the growth has been flat for most of this year.

Revenue rose 42% to $217.4 million ahead of estimates for $202.7 million. Bookings (remaining performance obligations) are growing faster than revenue at 53% to $1.58 billion. Calculated billings were up 44% year-over-year. This was a re-acceleration of calculated billings from the previous quarters in FY2021 where the pandemic weighed on budgets.

The company is profitable on an adjusted basis with EPS of $0.04 and free cash flow of $41.6 million, up from $9 million a year ago. Highlights include a growing number of customers in the financial services sector and government.

The guidance was conservative at $221 million to $222 million, representing a growth rate of 32% to 33% year-over-year. The company is also guiding for an adjusted loss of $0.02 to $0.01 EPS. The fiscal year 2021 offered stronger guidance of 40% growth year-over-year for $822 million in revenue with adjusted EPS of $0.04 to $0.05.

According to the investors deck, the company has a combined addressable market of $55 billion across Workforce Identity and Customer Identity. The contribution margins at 70% for fiscal 2017 cohort analysis on page 14 was impressive. The net retention rate is 123% with adjusted gross margins of 78% and adjusted operating margins of 2.5% and free cash flow margins of 19%. The net retention rate saw a re-acceleration to its highest level in two years. Typical NRR is in the 119-121% range. Free cash flow margin was also its highest in two years.

BETH.TECHNOLOGY

Total customer count was up 27% and annual contract value was up 34%. The current outlook for the company is 30-35% CAGR through FY 2024 and free cash flow margins in FY 2024 of 20-25%. The total number of $100,000 plus customers stands at 1780, an increase of 34%. The base of customers with annual contract value of greater than $500,000 grew 50%.

Okta's management pointed to three trends in driving business: Cloud and Hybrid IT, Digital Transformation and Zero Trust security. There is a partnership across Proofpoint, Netskope and CrowdStrike which is classified as a deep product integration for an enhanced product stack.

Okta was also recently introduced to the AWS marketplace and is the only identity vendor in the products for Control Tower, which allows for the management of more complicated AWS environments.

Notably, Okta was given a lower-ranking spot in the leader category of the 2020 Gartner Magic Quadrant for Identity and Access Management. One could argue too much attention is given to Gartner at times as Okta has been through a challenging and anomalous year. However, it should be noted that Okta was in a wide lead on the leader quadrant for 2019 and has been bumped down to equal standing with Microsoft and Ping Identity.

Snowflake

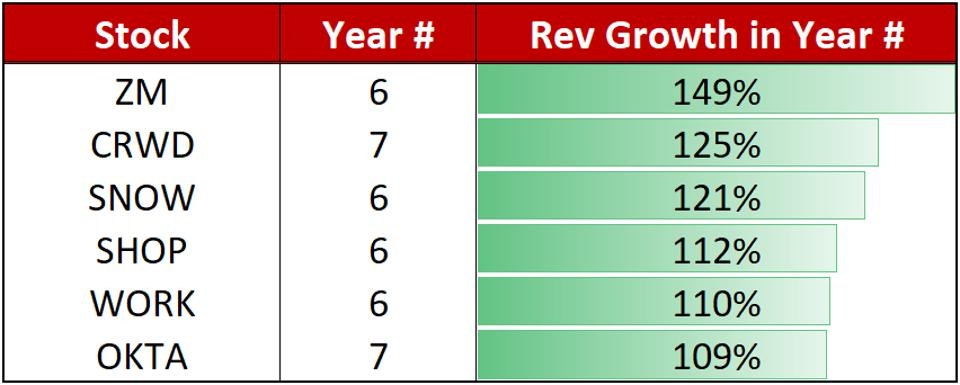

Snowflake grew 119% year-over-year to $159.6 million with remaining performance obligations of $927.9 million, or 240% year-over-year growth. Product revenue grew 115% year-over-year. The net revenue retention rate of 162% is impressive although other companies have exceeded this in their 6th year (Snowflake was founded in 2012 but was in stealth mode until 2014 when it began to work with customers).

BETH.TECHNOLOGY

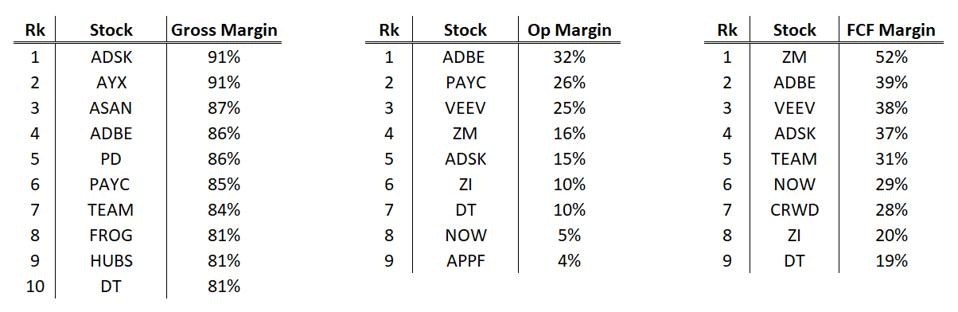

Gross margins are between 58% to 63%, which it's normal for a cloud company to be lower than a SaaS company on margins. However, operating margins were negative (30%) with FCF margins of negative (23%). Probably the biggest issue that Snowflake faces are the sales and marketing costs. In the previous two quarters, they were near or exceeded total revenue and in this quarter they were about 90% of revenue at $134 million compared to the $159 million in revenue.

The issue here is the rapid growth is being paid for in sales and marketing dollars and could slow when the bottom line becomes prioritized. Growth marketing tactics like this can often skew the true growth rate of a company at the expense of the bottom line. When equilibrium is sought, the top line suffers (or the alternative is that profitability is a long way off). Oddly enough, the bleeding operating and FCF margins weren't mentioned by the analysts in the Q&A on the earnings call.

The bigger product announcements on the earnings call include Snowflake expanding from semi-structured to unstructured data (which will be helpful for machine learning), SnowPark which enables users to query in their language of choice (Java, Python, etc). The overarching goal is to consolidate workloads and meet the demand for data governance purposes.

The company issued forward guidance for FY 2021 of revenues between $538 million and $543 million for YoY growth of 113% to 115%. Margin will be decent for adjusted gross at 68% compared to negative (40%) operating margin and negative (18%) adjusted FCF margin.

Snowflake is a strong company. In my opinion, the valuation is a major risk and continues to be considering the high sales and marketing costs that are causing an imbalance between the top line and bottom-line growth. Net retention rate of 169% is impressive although is a consumption model and cannot be compared to SaaS.

CrowdStrike

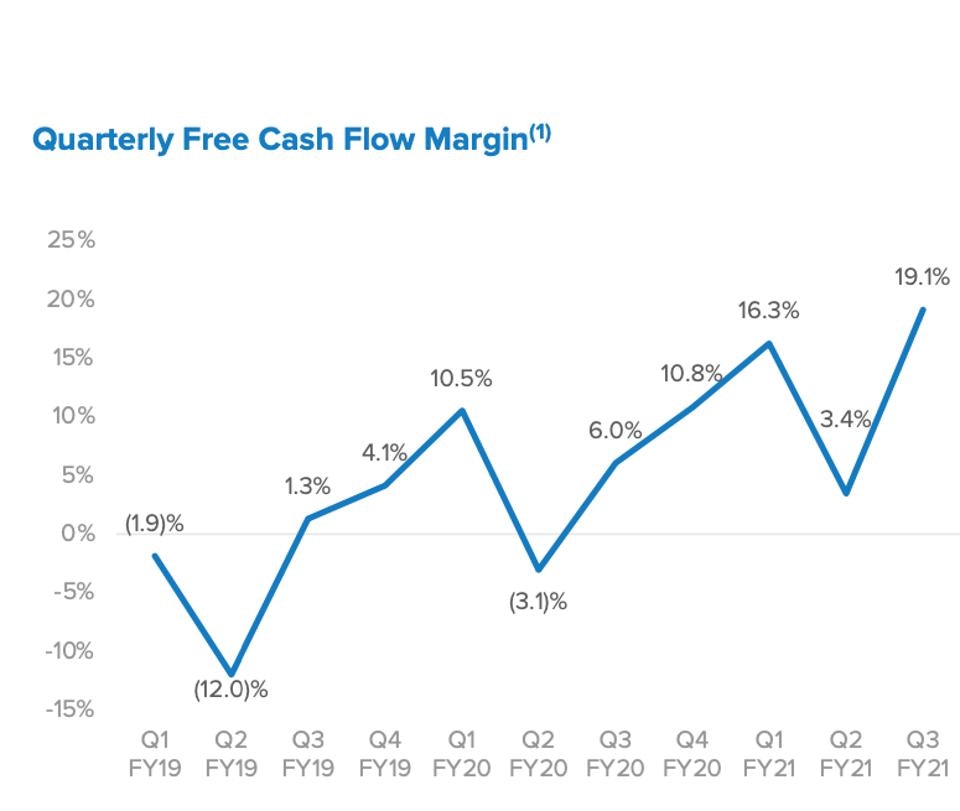

CrowdStrike beat consensus estimates on both the top and bottom lines and raised Q4 guidance. Revenue grew 86% YoY, representing an 8% beat above Wall Street estimates. Subscription revenue increased 87% YoY while annual recurring revenue advanced 81% compared to a year ago. The company also achieved its most impressive quarter ever in terms of profitability, earning $0.08 per share on the bottom line. This was CrowdStrike's third consecutive quarter of positive EPS and its highest total yet. Free-cash-flow margin increased to 33% and gross margin improved to 76%.

Here is how CrowdStrike's FCF margin compared last quarter:

BETH.TECHNOLOGY

In the quarter, CrowdStrike added 1,186 net new subscription customers, representing growth of 85% YoY. CrowdStrike also continues to drive new module adoption in existing customers, as 44% of the company's subscription customers have adopted five or more modules versus 39% in the previous quarter. Management guided for $248M in revenue for Q4 (+63% YoY), representing a 7% raise above expectations.

This was an impressive quarter for CrowdStrike both in terms of increased usage of existing customers and the addition of new customers. As previously mentioned, CrowdStrike continues to excel in its ability to drive new module adoption with 61% of the company's customers adopting 4 or more modules versus 52% in the same period a year ago.

In the quarter, CrowdStrike announced the addition of three new modules to the Falcon Platform, covering cloud security posture, dark web threats, and incident response investigations. The Falcon Platform now encompasses 16 modules in total.

CEO George Kurtz highlighted new module adoption as a key to the company's growth strategy in its Q3 Earnings Call: "I'm pleased to announce that in Q3 we reached a new milestone with 22% of our subscription customers having adopted six or more modules. Driving adoption of our expanding module lineup is a keystone to our growth strategy as it increases the strategic value we provide to customers, which also translates to higher retention rates."

This quarter indicates CrowdStrike is successfully executing on this growth strategy.

The second key to CrowdStrike's growth hinges on its ability to add new customers, a metric that increased 85% YoY in Q3. One key customer win in the quarter was signing Target, which displaced Symantec and deployed Falcon completely across its footprint in less than 10 days.

CEO George Kurtz discussed the marquee win in its earnings call: "a win with Target that highlights how our single agent cloud-native architecture, intuitive console, and rapid re-bootless deployment capabilities continue to be significant differentiators for us. Target Corporation was looking to rapidly move away from Symantec and transition to a single agent cloud solution that could be deployed in days, not months or years."

Zscaler

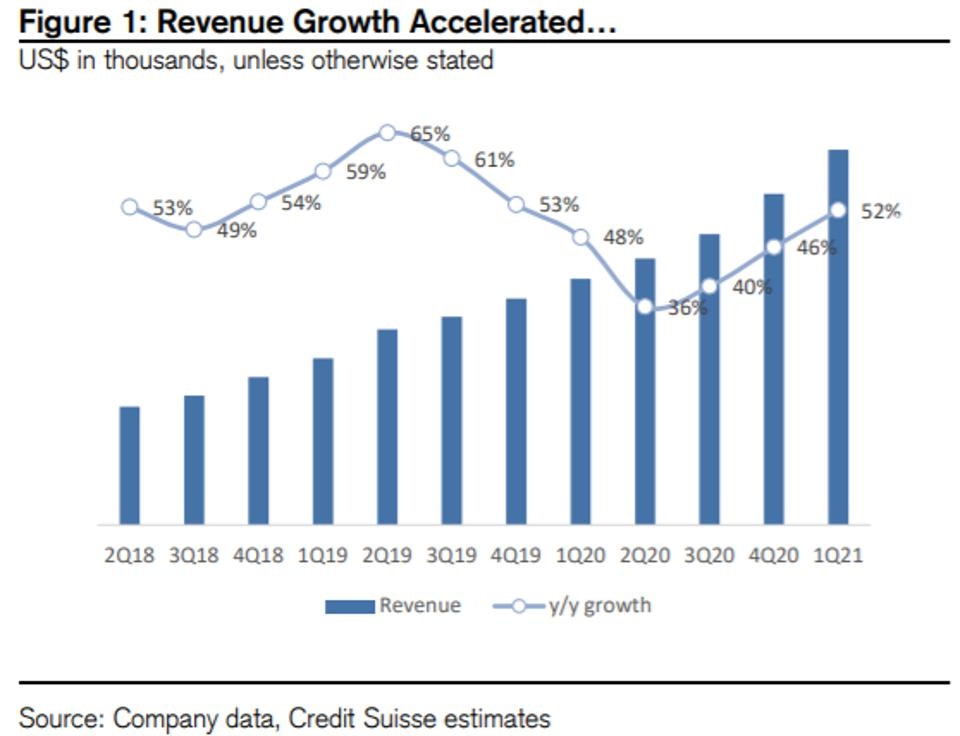

ZScaler announced Fiscal Q1 2021 results that easily cleared analysts' expectations. Revenue growth accelerated to 52% YoY, which represents the company's third consecutive quarter of growth acceleration.

Adjusted billings growth increased 64% YoY, far surpassing the consensus expectation calling for 39% growth. This beat was driven in part by a record quarter of seven-figure deals. The company's net retention rate of 122% advanced from 120% last quarter and 119% the quarter before. Non-GAAP EPS of $0.14 was 8 cents better than expectations while the company also announced an impressive 30% FCF margin. Non-GAAP operating margin of 14% far exceeds the consensus of 2.9%.

CREDIT SUISSE

The acceleration in growth coupled with the record quarter of operating profits and free cash flows makes this one of the best quarters ZScaler has announced.

CEO Jay Chaudry discussed the three main factors that allowed his company to outperform this quarter: "One, building on our growing traction with large enterprises. We closed a record number of seven-figure ACV deals… two, our optimized go-to-market engine is driving significant velocity… Last year, we doubled down on our investment in our sales organization. These efforts are also bearing fruit in two big ways. One, our newly hired sales reps are contributing at a faster pace. And two, our sales productivity is higher than a year ago, despite a high percentage of ramping sales reps… Three, the power of our Zero Trust Exchange platform is resonating with CxOs."

Looking ahead, ZScaler believes that the strong business momentum they have exhibited in the last several quarters will continue. Management raised guidance over 5% for FQ2, now expecting $147M of revenue at the midpoint (+45% YoY). Management attributed the strong FQ1 in part to stronger than expected deal activity and expects these trends to continue into the next quarter.

In its FQ1 Earnings Call, CEO Jay Chaudry touted the company's position amongst a growing opportunity: "I believe in the current challenging environment and in the post-COVID economy, Zscaler will be the go-to-platform for vendor consolidation, cost-saving, increased user productivity, and better cyber protection.."

Elastic

Elastic announced strong FQ2 earnings on 12/2. Total revenue increased 43% YoY, representing an 11% beat above consensus. Total billings grew 42% YoY while SaaS revenue increased 81% versus the same period a year ago. The company's losses also improved significantly, with non-GAAP EPS of -$0.03 coming in 17 cents better than expected. Non-GAAP operating loss improved to -$1.9 million, representing a -1% operating margin versus -10% projected. Gross margins also came in better than expected with 77% versus a consensus of 75%. FCF margin was -13% for the quarter.

Subscription revenue totaled 93% of Elastic's total revenue in the quarter, with 45% of total revenue coming from outside the US. Management views this geographical distribution as a strength in the company's business model. Elastic's net retention rate ticked down several points from last quarter but still remained modestly above 130%. Elastic now has a total of 12,900 subscription customers with 650 of those (5%) having annual contract values exceeding $100K.

At the start of its fiscal year, Elastic's management discussed how COVID-19 would likely create headwinds to calculated billings for a couple of quarters and that they would then see gradual improvement beyond that.

In its FQ2 Earnings Call, management confirmed that the first half of fiscal 2021 played out as expected. The company has observed longer sales cycles and many customers are looking to conserve cash as spending patterns have not recovered to pre-COVID levels. Management updates its outlook for the second half of the year, noting that they expect the trends they observed in the last two quarters to continue in the next two: "given the global situation with the pandemic, our current assumption is that the mixed demand environment that we experienced in the first half will continue for the rest of the fiscal year. Previously we were expecting the environment to gradually improve during the second half." Still, Elastic's strong execution in the first half of its fiscal year gave management the confidence to increase its guidance for the next quarter. Management raised guidance 4% for FQ3, now expecting $146M of revenue (+29%). However, the company expects EPS to decline to -$0.15 on a -7% operating margin for FQ3.

Elastic's management ultimately expects the demand environment to return to pre-COVID levels in fiscal 2022, which would align with the summer of 2021. While the company is certainly facing some headwinds due to the pandemic, the digital transformation has provided tailwinds that have allowed growth to remain strong. Management expects these tailwinds to continue beyond the rest of their fiscal year: "the tailwinds of cloud and our solutions adoption position us well for the rest of this fiscal year and beyond."

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per