Snowflake IPO: In-Depth Analysis

September 17, 2020

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Sep 11, 2020,03:02am EDT

Snowflake is the most anticipated IPO of the year. Investors should decide in advance how much they are willing to pay as Snowflake will test the upper limits of what it means to have a stretched valuation. Heck, the company has even inspired value-legend Warren Buffet to change his thesis and invest in an IPO prior to profitability (!)

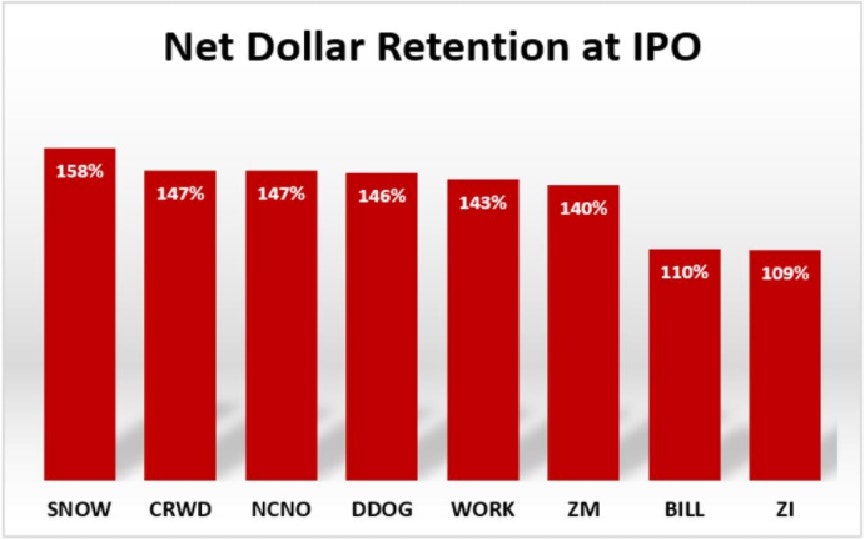

Perhaps because the company delivered sky-high revenue growth last fiscal year of 173% and 121% in the most recent quarter with a record-breaking net retention rate of 158% — which is the highest of any public cloud company at time of listing.

David Marlin

These industry-leading numbers are due to the company disrupting the data warehousing market with a superior cloud data platform that delivers across key differentiators (we review this below). Despite Snowflake demonstrating excellent product-market fit, clear competitive advantages, and strong management — no company is perfect. We go over a few key risks that investors should keep in mind as the bidding becomes fierce on opening day.

Snowflake Financials

Snowflake has strong financials for a tech IPO, yet it’s important to remember the product has been available for only six years and tech growth is typically strongest in the early days. The company delivered 173% growth in the fiscal year ending January 31, growing from $96.7 million to $264.7 million with gross profit margins of 56.2%.

These gross margins are below what cloud companies are capable of yet improved in the most recent period. Revenue grew 133% year-over-year in the first six months of fiscal 2021 ending in July, growing from $104 million to $242 million with improving gross profit margins of 61.5%.

In the most recent quarter, the company reported growth of 121%. Here, we already see the effects of age within a short time period as Snowflake settles from 173% growth to 133% growth and now to 121% growth. This is not a negative by any means (triple-digit growth is to be celebrated) but keep in perspective it’s age when comparing Snowflake to any high-growth cloud SaaS peers.

David Marlin

The bottom line has been varied depending on what period you look at. The losses doubled from fiscal year 2019 with net losses of $178 million increasing to net losses of $348.5 million in fiscal year 2020.

More recently in the first six months of fiscal 2021, the net losses were flat period-over-period at $177.2 million compared to losses of $171.3 million. This could be an encouraging sign or it could be Snowflake tightening the belt temporarily for the public offering before returning to the original pace of worsening losses. There is not enough history to know if the more encouraging flat rate of losses is sustainable. Adjusted EPS was negative $1.63 in the fiscal year ending in January compared to negative adjusted EPS of $0.72 in the first half of fiscal 2021.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Net retention rate for Snowflake is a record 158% — the highest of any company when going public. However, it’s important to remember that net retention rate lowers over time as customers become harder to retain long-term (I cover net retention rates more in-depth here).

The company was founded in 2012 yet the product came out of stealth mode in 2014. When considering the product launch, Snowflake is a very young company of only six years old.

David Marlin

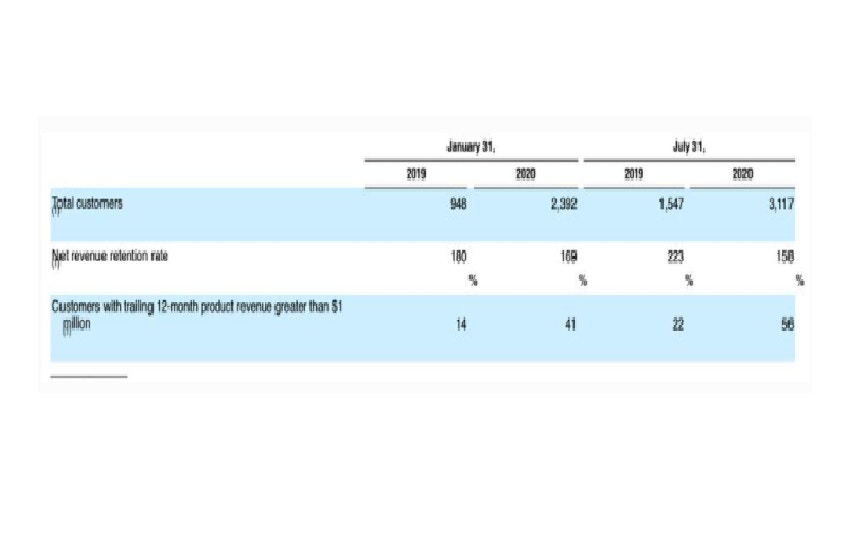

You can see evidence of how net retention is affected by number of years in Snowflake’s S-1 filing as the company had a rate of 223% in the first half of 2019 compared to 158% period-over-period. Annually, the company lost 11 percentage points in net retention rate from 180% to 169%.

SNOWFLAKE S-1 FILING

Regardless, Snowflake has impressive numbers. Perhaps the most impressive key metric in the S-1 filing is the growth in the percentage of customers with product revenue greater than $1 million. This has grown considerably from 14% in fiscal year 2019 to 41% in fiscal year 2020. There is evidence high-end accounts are continuing to grow with the first six months of 2020 at 56% compared to 22% in the year-ago period.

The new CEO, Frank Slootman, clearly knows how to make a company attractive to investors. Not only did the company quicky tighten its belt in regard to net losses, the company also doubled customers from 1,547 to 3,117 over the past twelve months. This includes 7 of the Fortune 10 and 146 of the Fortune 500.

Cash used in operating activities decreased from $110 million to $45.3 million in the first six months of fiscal 2021. The company has cash and investments of $591 million and no debt.

As outlined in the S-1, IDC places the addressable market for Analytics Data Management and Integration Platforms and Business Intelligence and Analytics Tools at $56 billion in 2020 and $84 billion in 2023.

In an effort to narrow this addressable market, I dug up a few more sources. According to MarketsandMarkets, the addressable market for Data Warehouse-as-a-Service is much smaller at $1.2 billion in 2018 and set to grow to $3.4 billion by 2023 at a CAGR of 23.8%. P&S Intelligence reports a similar CAGR of 29.2%, estimating the Data Warehouse-as-a-Service market to reach $23.8 billion by 2030. When combining on-premise, Allied Market Research places the data warehousing market at $34.7 billion by 2025.

You’ll find larger addressable markets in tech but the weight Snowflake brings to the category is considerable.

Snowflake’s former CEO, Bob Muglia, grew the company from 80 customers in 2015 to 1000 customers in early 2018 when he was replaced by Frank Slootman. The change likely happened due to pressure from private investors who want a grand slam exit (and looks like they’ll be getting just that).

Slootman is known for resuscitating Data Domain from nearly running out of money in 2003 to an acquisition in 2009 after the company “grew to sell more than all its competitors combined.” This was detailed in a book that Slootman wrote called: “TAPE SUCKS: Inside Data Domain, A Silicon Valley Growth Story.” Three years later, Slootman took over the CEO role of ServiceNow between 2011 to 2017 and grew the company from $75 million in annual revenue to $1.5 billion. This was achieved by diversifying the product beyond the IT department.

For many investors, management is a key factor in deciding to invest or not. Here, Snowflake fires on yet another cylinder.

Product:

Snowflake’s decoupled architecture allows for compute and storage to scale separately with the storage provided from any cloud provider the customer chooses. By processing queries using massively parallel processing (MPP), where each node in the cluster stores a portion of the data set locally, the virtual warehouses can access the storage layer independently so as not to compete for compute power. With the competitors, such as Redshift, where compute and storage are coupled, more time is spent reconfiguring the cluster.

Snowflake calls this offering a virtual data warehouse where workloads share the same data but can run independently. This is crucial because Snowflake’s competitors combine compute and storage and require customers to size and pay based on the largest workload.

Data warehouses are centralized data repositories that collect and store information across many sources that are both internal and external. The raw data is ingested into the data warehouse and processed to answer queries. To ingest data, warehouses follow the ETL process, which is: (1) Extract the data from the internal or external database or file, (2) Transform by cleaning and preparing the data to fit the schema and constraints of the data warehouse and (3) Load into the data warehouse. The ETL method helps to organize the data into a relational format. Notably, Snowflake supports both ETL and ELT, which allows for data transformation during or after loading.

One key product differentiator is that Snowflake is not built on Hadoop, rather the company uses a new SQL database engine with cloud-optimized architecture. Overall, this translates to faster queries and also reduces costs by scaling up or down for both capacity and performance. This also allows the shift to the cloud while still honoring traditional relational database tools. Just like cloud infrastructure does not require you to hold server space for peak times year-round, a cloud data warehouse does not require you to plan, acquire or manage resources for peak data demand (i.e. elasticity).

The need for resources could change by either increasing or decreasing (scaling up or down). Customers that have a need for storage but less of a need for CPU computations do not have to pay up front and can shrink the environment dynamically. Users either pay for terabytes or are billed on a per-second basis for computations. Notably, Snowflake charges by execution-based usage and is not a cloud SaaS-company that charges by subscription.

Snowflake has a multi-cluster architecture which is unique from single cluster databases. The multi-cluster approach allows the clusters to access the same underlying data yet to run independently. This allows for heavy queries and operations to run very quickly and with fewer errors because the queries are not accessing the same data warehouse.

Queries are made with standard SQL, for analytics, and integrates with R and Python programming languages. The company delivers the ability to handle all incongruent data types in a single data warehouse. Because the data is accessible through SQL, there is widespread developer uptake as it’s the most common database language.

Snowflake supports both structured data and semi-structured data. As machine-generated data grows to include applications, sensors and mobile devices, Snowflake allows semi-structure data to be handled without preparation or schema definitions. The result is handling JSON, Avro, ORC, Parquet or XML data as if it were relational and structured.

Snowflake uses a compressed columnar database. Columnar databases are optimized for the fast retrieval of columns of data and is used for analytic data queries. Other features include centralized metadata management that is stored in a single-key value store that allows cloning of tables and databases. Security is baked into the platform to where Snowflake automatically encrypts all data to the point where unencrypted data is not even allowed. There is third-party certification and validation for security standards like HIPAA.

Beyond the value proposition of separating storage from compute for speed, and also scaling up or down to reduce costs, the third takeaway is that Snowflake is also much easier for customers to use as it’s designed to remove the role of a database administrator for monitoring and/or to tune query performance.

The end goal of choosing Snowflake is that you load data, run queries, and do little else – which is an immense value proposition due to the amount of time wasted prepping, balancing, tuning and monitoring traditional data warehouses originally built for on-premise.

Snowflake is capitalizing on the multi-cloud trend and growing rapidly with customers who want a choice in public cloud provider despite the cloud giants having their own data warehouse systems, such as Amazon Redshift, Azure Synapse and Google Big Query.

Generally speaking, Big Query is a closer competitor as Google’s offering also separates storage and compute. The differences between BigQuery and Snowflake include pricing structure where Snowflake is a time-based pricing model where users are charged for execution time and BigQuery is a query-based pricing model, where users are charged for the amount of data returned from the queries. BigQuery has a serverless feature that makes it easier to begin using the data warehouse a the serverless feature removes the need for manual scaling and performance tuning. Dremel is the query engine for BigQuery.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

When it comes to deciding between BigQuery and Snowflake, it can come down to what you do with the database due to pricing structure differences. For instance, Snowflake is a better choice for concurrent users and business intelligence. It’s also a great choice for data-as-a-service, where you might give client access to your data in the form of analytics. BigQuery is perhaps a better choice for ad hoc reporting, where you have occasional complex reports on a quarterly basis or recommendation models and machine learning that require high idle time. Again, these examples are mainly due to pricing structure.

Despite BigQuery having a strong following with nearly twice the number of companies as Snowflake and growing around 40%, it tested slower than Snowflake in field tests performed by GigaOm in 2019. Vendor lock-in from BigQuery is also undesirable as companies may prefer AWS or Azure and/or more interoperability or best-in-breed solutions – we can see this in the growing trend of multi-cloud. AWS Redshift has the biggest market presence but growth is nearly flat at 6.5% and AWS is the leading partner for Snowflake.

Here's a great write-up from the Hashmap Engineering and Technology Blog that points out why implementing optimized row columnar (ORC) format data loads is ideal for either Snowflake or Amazon Redshift due to the ORC file format. Again, ultimately the choice in which system you use comes down to the individual needs for implementation although Snowflake is designed to be a competitor in nearly every case.

There’s a great write-up from analyst David Vellante that discusses how Snowflake competes with cloud native database giants. His analysis discusses survey responses from CIOs and IT buyers with Snowflake having a lead over the tech giants in spending intentions. The Enterprise Technology Research study he highlights showed 80% of AWS accounts plan to spend more on Snowflake in 2020 relative to 2019 with 35% adding Snowflake as new compared to 12% adding Redshift as new. In Azure, 78% plan to spend more on Snowflake with 41% adding new. On Google Cloud, 80% plan to increase spending on Snowflake. We can see the people have spoken.

A few risks …

Due to Snowflake’s product strengths, the public cloud providers offer Snowflake while at the same time being in competition. The main risk being discussed is that public cloud providers have competing databases, but in reality, the risk may be pricing pressure over time. Snowflake has a great top line; however, the bottom line is affected by its partnership with the competitors. Plus, tech giants can greatly undercut Snowflake on pricing. Therefore, margins may be an inherent issue.

The company pays quite a bit for sales and marketing, which is typical for a company going public as this strengthens the top line yet could make it hard to balance this growth with profitability in the future. (But hey, if Berkshire doesn’t care, why should we!)

In the S-1 filing, it was noted that Salesforce will buy $250 million in stock in a private placement. This could be a risk if Salesforce becomes too intertwined with Snowflake as it’s best possible growth will be achieved by stating neutral, in my opinion. This involvement is something to monitor.

As stated, Berkshire Hathaway is also intending to purchase $250 million in shares in a private placement plus an additional $300 million from an unnamed stockholder in a secondary transaction. As Business Insider pointed out, this involvement from Berkshire is “rarer than a unicorn” and will be viewed as a strength by both institutions and retailers.

There could be risk in Snowflake being cloud-native only and not offering hybrid or on-premise. This can limit the customer pool as enterprises prefer hybrid options. Perhaps the bigger picture for Snowflake’s strength will be leveraging artificial intelligence in applications and business intelligence, and in this case, a hybrid and on-premise offering won’t be as necessary.

Valuation

Snowflake’s amended filing on September 8th shows the company will be priced at $75 to $85 per share with a valuation between $20.9 billion and $23.7 billion. This would raise $2.7 billion. The last private valuation for Snowflake was $12.5 billion when the company raised a Series G for $479 million.

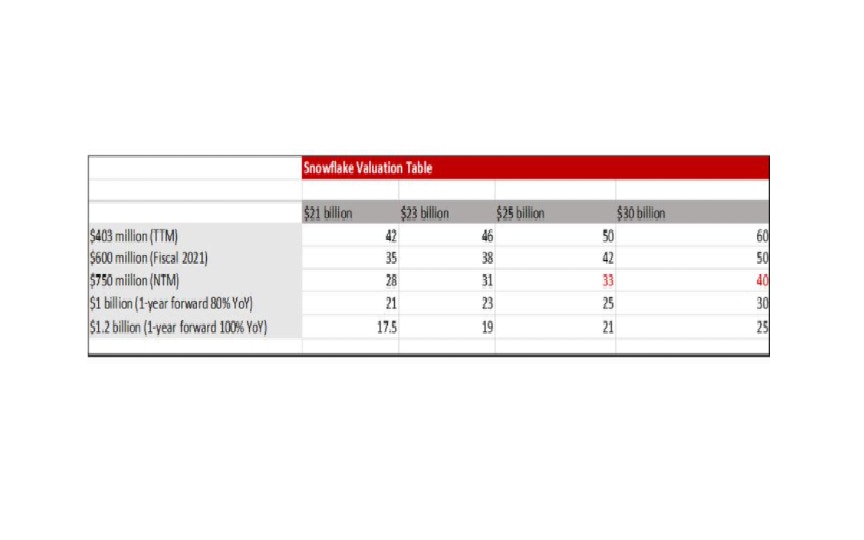

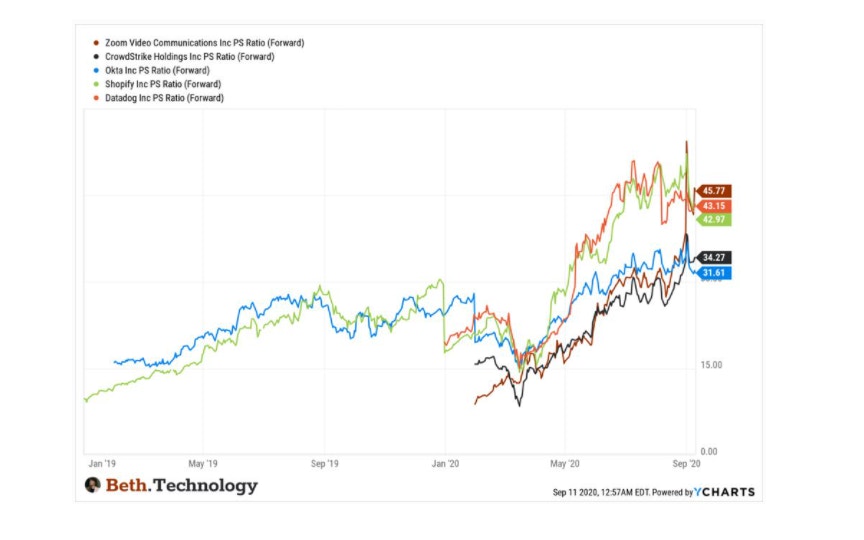

When we look at various scenarios, we see Snowflake hitting 40 forward price-to-sales in the $30 billion valuation range.

Snowflake IPO Valuation Table - BETH KINDIG

Snowflake is not profitable while Shopify, Zoom Video and Datadog are profitable with some showing accelerating revenue. These three have commanded above a 40 forward price-to-sales in perfect conditions only. The majority of their trading history has been beneath a 30 forward price-to-sales. Being profitable should come with a premium yet Snowflake will likely inch its way into this valuation range without demonstrating profitability.

Snowflake's IPO opening price will test the upper limits of high growth valuations. - BETH KINDIG

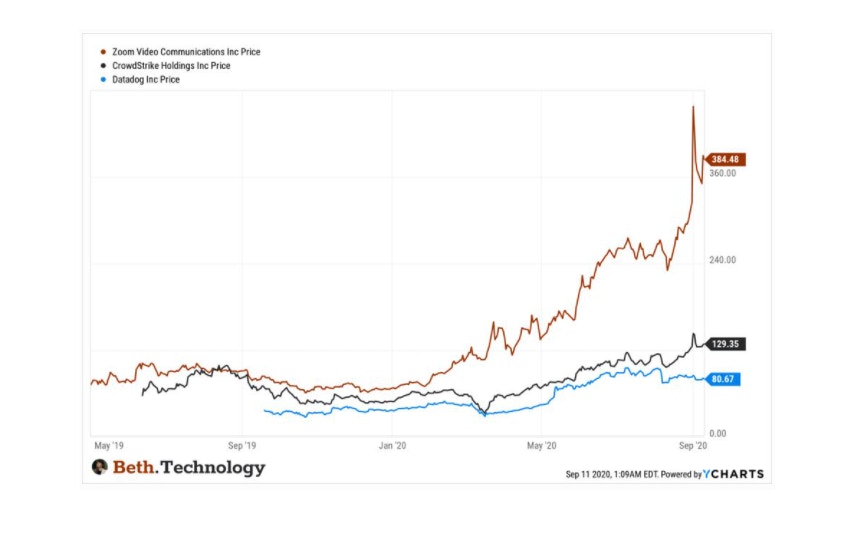

When we look at Zoom Video, Crowdstrike and Datadog, we see these three traded at or beneath their opening IPO price many times in the year following IPO. Crowdstrike saw roughly a 50% drawdown from its opening price.

Snowflake's IPO opening price may not sustain if history is any indication - BETH KINDIG

Therefore, if Snowflake trades at a 30 forward price-to-sales and sustains this valuation, it will be the first high growth company with negative earnings to do so. Even those with positive earnings growth have only traded above this valuation for a brief period over the last three months.

A better strategy would be not pay over this amount and count on history rhyming. At NTM revenue of $750 million, that means Snowflake would have to open at the price listed in the prospectus in order to remain within a reasonable $25 billion valuation (“reasonable” being used loosely here as only a few companies have traded at this valuation in the most ideal conditions/tech market and these comparables were profitable).

Conclusion:

When you were a child, your parents probably asked, “are you going to jump off a bridge if everyone else does?” The goal of the question was to get you to think for yourself in the face of peer pressure.

In this situation, the question that should be asked is, “are you going to invest in a company with triple-digit growth, clear product differentiation, key metrics that prove product-market fit and gravity-defying management … if Berkshire does?” The answer is probably “yes.”

The issue is that we aren’t Berkshire or Salesforce so we will probably overpay. Therefore, the biggest risk of all is how much alpha will be left in the first year of trading by the time retailers are offered the crumbs.

I’ve participated in IPOs out the gate and the only ones that have paid off were under-hyped (Roku). Those that were over-hyped, such as Zoom Video and Crowdstrike, either retreated back to their opening price or saw up to a 50% haircut from the opening price.

I did not participate in either of these over-hyped IPOs but I did snag Zoom Video later in January of 2020. I was able to put that money to use elsewhere while waiting for the lock-up period to expire and the right entry in the low $60s nearly 9 months after Zoom Video had listed.

Even as a Snowflake enthusiast. I may back-off after 30 forward price-to-sales (and most certainly at 40 forward P/S) as I’m confident I can find many great tech companies that are less hyped while I wait it out. We will always see periods of indiscriminate selling across high-growth and I don’t think Snowflake will escape those rotations.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i