Slowing Growth In Cloud Stocks: When Will We Hit A Bottom

December 20, 2022

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Dec 15, 2022, 10:27pm EST

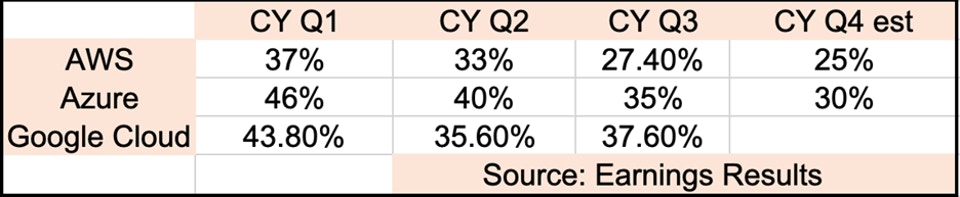

Nearly all cloud companies are reporting a notable, sequential slowdown between Q3 to Q4. Amazon and Microsoft’s cloud infrastructure services slowed from mid-30 percent growth in prior years to 24 percent growth and 30% growth. Only a quarter ago – in Q2 – the growth was at 29 percent and 35%. This quarter marks a 5 percent decline sequentially, which is considered a rapid decline for these two companies.

For many more highly valued cloud software companies, the sequential decline is much steeper and is closer to a 15% sequential decline. On a YoY basis, the Q3 to Q4 growth is 70% lower than it was tracking last year. For example. Snowflake grew 15% QoQ last year and is expected to grow 3% QoQ this year, marking a 12 point decline in its growth rate. This is true for most best-of-breed cloud stocks.

We covered this point on popular cloud software stocks in granular detail in a premium note for our research Members when we said:

“In some ways, the Q4 guides – assuming most come in at or near those guides – marks a historic slowdown for cloud as it’s always been a resilient category.”

The question is, at this rate of rapid decline, when will we hit a bottom on slowing growth?

Gartner, a reputable and accurate third-party analyst firm, is indirectly calling for a bottom in cloud in 2022, per its recent two surveys. However, judging by the most recent earnings results provided by the Big 3 and cloud’s top performing stocks, I believe this could be premature and it’s more likely we bottom sometime in 2023.

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

Gartner 2023 Surveys

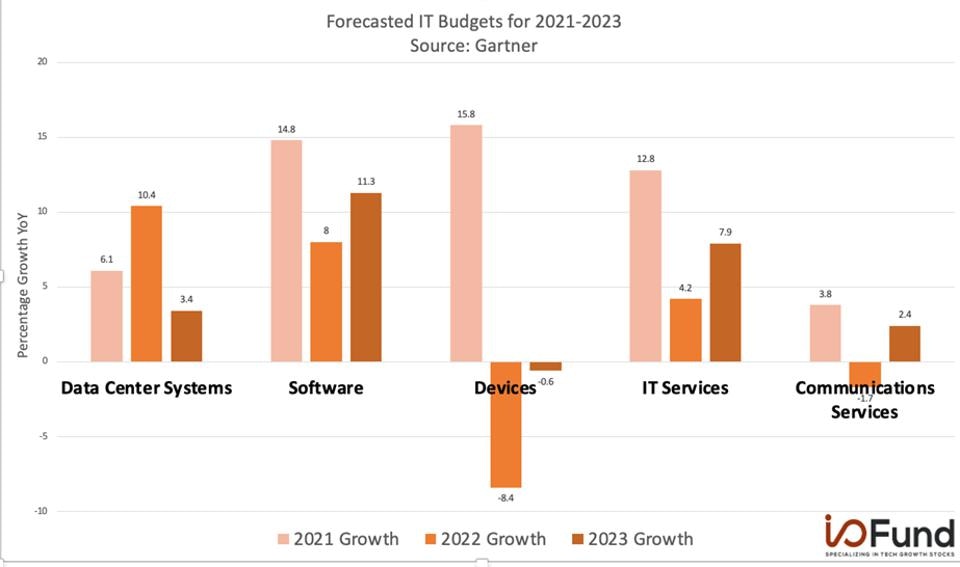

In a recent report, Gartner predicted that in 2023, IT spending will recover from a notable low in 2022 in all areas except Data Center Systems. Devices will still remain negative to flat, yet show a remarkable recovery from (8.4%) to (0.6%), per the CFO 2023 survey. Software will accelerate from 8% to 11.3% while IT services will double in growth from 4.2% to 7.9%.

Across all categories of IT spending, Gartner is calling for combined growth of 5.1% in IT budgets compared to 0.8% growth in 2022. This will be down from 10.2% in 2021.

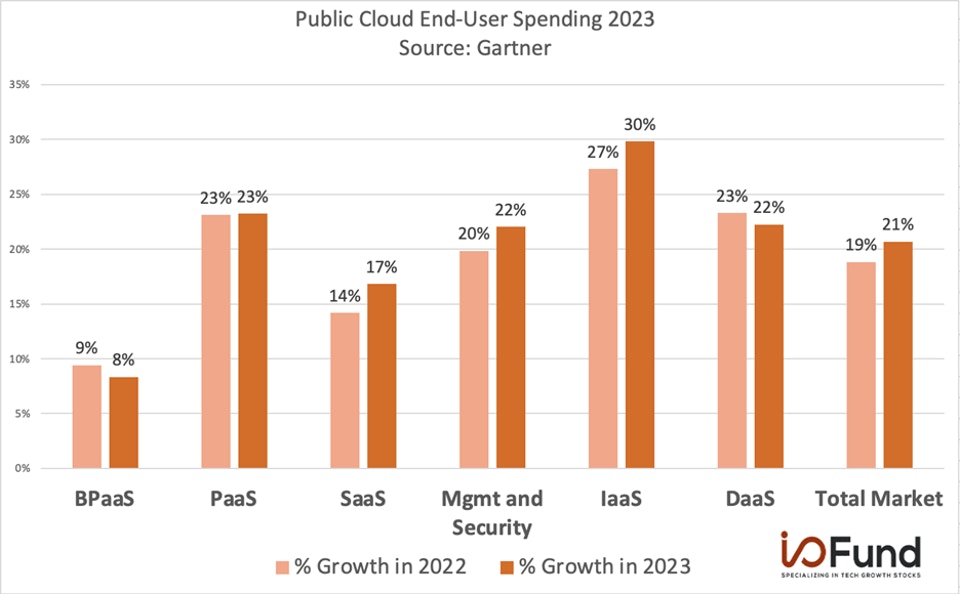

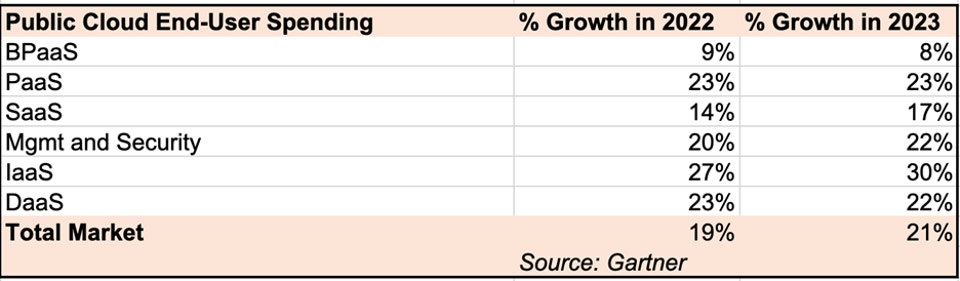

Gartner is also forecasting that 2022 is the bottom for a few public cloud end-user verticals with a year-over-year increase in software-as-a-service (SaaS), cloud management and security, and infrastructure-as-a-service (IaaS).

Of these, Cloud IaaS is expected to see the most growth from 27% in 2022 to 30% in 2023. This is on a large revenue base of $115 billion, expected to grow to $150 billion in 2023. Software-as-a-service is the largest category in cloud with revenue of $167 billion, expected to grow to $195 billion at a rate of 17%.

Notably, some areas are expected to decline, such as BPaaS and DaaS.

Shown below, the overall cloud market is expected to grow 21%, up from 19% in 2022. This will outpace overall IT spending with growth of 5.1% by over 5X.

The 5.1% growth lags the current inflation rate of 6.5%.

Source: Gartner: Public Cloud End-User Spending

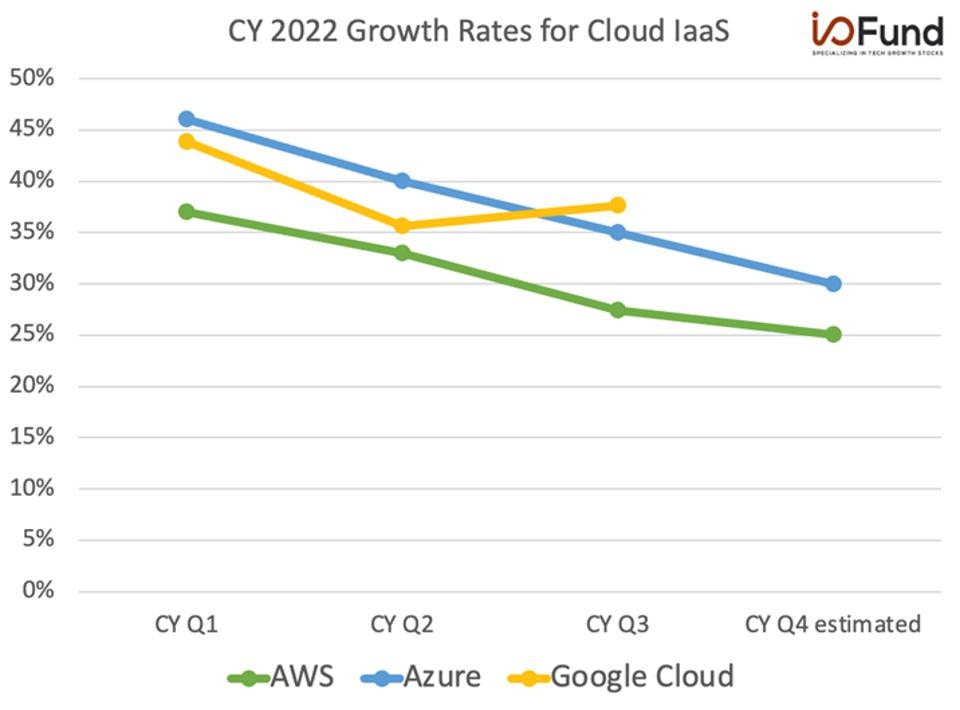

Cloud IaaS Growth Saw 3% Headwind in 2022, More to Come?

Gartner released the 2023 survey results in October, and later that month, Q3 earnings results from Big Tech reported a decline in Cloud IaaS. Perhaps the survey is predicting a rebound from H2 2022 to H1 2023, but this would be hard to determine until budgets are set in the earlier part of next year.

In most cases, we are seeing a 10% deceleration from the early part of the year to the second half of the year. For now, actual results from the Big 3 Cloud IaaS providers disagree with Gartner’s survey predictions that a rebound is coming. This is despite Cloud IaaS predicted to be the more resilient line item in public cloud end-user spending.

The biggest names in tech are reporting their earnings right now, and our premium members are getting updates almost daily. Learn more about about our premium membership here.

Mixed Reports Following Q3 Results

Gartner’s prediction that cloud budgets will expand contrasts with other surveys that suggest the opposite. For example, according to a survey by Wanclouds, 81% of companies were directed by the C-suite to reduce cloud spending or to occur no additional costs.

The venture capital firm Accel published a report that showed private funding for cloud companies dropped as much as 42% across Europe, Israel and the United States in Q3. This often translates to lower valuations and/or lacking a clear path to a strong exit on the public markets or through an acquisition.

This doesn’t mean the migration to the cloud is slowing down, by any means. According to Accel, spending on automation and digital transformation is expected to rise from $1.8 trillion to $2.8 trillion by 2025. The drawback to these kinds of forecasts is that it may slow considerably in 2023 before a rebound occurs.

Conclusion:

Cloud spending may turn out to be softer than industry surveys indicate, especially until inflation cools off. This is because surveys capture a perception while earnings results are the culmination of a 7.1% inflation rate, plus a softer Chinese market and a softer European market.

The Big 3 are the best proxy because their reports represent the layer in the tech stack that tends to be the most resilient in terms of churn. The switching costs are quite high for cloud IaaS services. The Big 3 also afford a more concentrated view by owning 66% of market share across three companies whereas SaaS is spread across thousands of companies.

For our premium members, we dig deeper into mid-cap cloud companies to determine which ones are decelerating more quickly than their peers and also which leading cloud stocks we plan to buy when we sense there is a rebound. You can learn more here.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i