Microsoft Stock: Azure Growth Proves Resilient

August 15, 2022

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Aug 8, 2022,11:06am EDT

Most investors agree that cloud is a critical trend to have in a portfolio as the category’s growth has been resilient due to increasing productivity while reducing costs. This is especially true for software-as-a-service whereas cloud infrastructure as-a-service does not always result in lower costs compared to on-premise servers.

The overall cost savings and/or overhead can often rely on the size of company, where it makes sense for startups to rent servers as they don’t have the budget to own servers and manage an IT department. However, despite the many advantages that cloud offers, it requires scaling through outside vendors, which can result in a hit to margins. A report came out that repatriation, or moving some workloads back to on-premise, has resulted in quite a bit of cost savings for companies like Dropbox and Zscaler, who use hybrid approaches. One example in the report is Dropbox, a company that reported savings of $75 million in two years after repatriation, which in turn, helped the company’s gross margins increase from 33% to 67%.

If you add up the cloud infrastructure, platforms and software costs across a company, it can often become costly to manage and deploy a full cloud stack.

To put it simply, Sayta Nadella said in the fiscal Q3 call in April: “More value for less price means you win.”

The company’s recent results prove that the company is able to better withstand the challenges of the macro uncertainty better than other cloud peers.

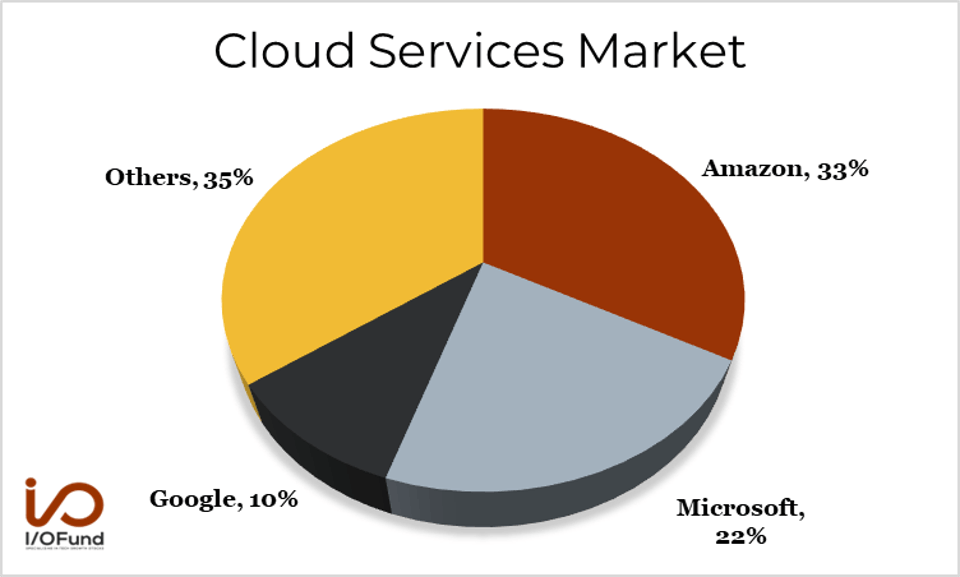

For example, Azure & other cloud services revenue grew by 40% and 46% in constant currency. As stated, Azure’s growth was a major highlight considering Google Cloud’s revenue in the recent quarter increased 36% YoY to $6.3 billion. Notably, GCP is on a lower revenue base which makes Microsoft’s outsized growth even more impressive. The market leader Amazon Web Services revenue grew by 33% YoY to $19.7 billion in Q2.

Here’s how the major cloud IaaS competitors compare:

Cloud Services Market Share - I/O FUND

Furthermore, Microsoft’s Fortune 500 penetration is staggering with 95% using Azure. This was achieved through hybrid computing where Microsoft was first-to-market on serving a mix of on-premise, private and public clouds for their large enterprise customers. We covered Microsoft’s competitive edge on hybrid dating back to 2018 when Azure was frequently doubted by the market as it was overshadowed at the time by AWS.

Today, Microsoft is leveraging its lead in hybrid by undercutting other services on price in order to win the aggregate, long-term contract. By owning the entire cloud stack, Microsoft can offer the ultimate differentiator during macro headwinds, which is “more value for less price” whereas competitors do not own enough of the stack to undercut on price quite like Microsoft.

We originally covered this for our research customers in both our Q2 webinar and a research note last April.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Microsoft’s Financials:

Microsoft’s revenue grew by 12% YoY to $51.9 billion for the Q4 FY2022 ending in June, and for the FY2022 ending in June, it grew by 18% YoY to $198.3 billion.

The company’s strong guidance for the full year was a testimony to the management's confidence as many of its tech peers failed to give guidance. Amy Hood, CFO of the company said in the earnings call, “We continue to expect double-digit revenue and operating income growth in both constant currency and U.S. dollars. Revenue growth will be driven by continued momentum in our commercial business and a focus on share gains across our portfolio.”

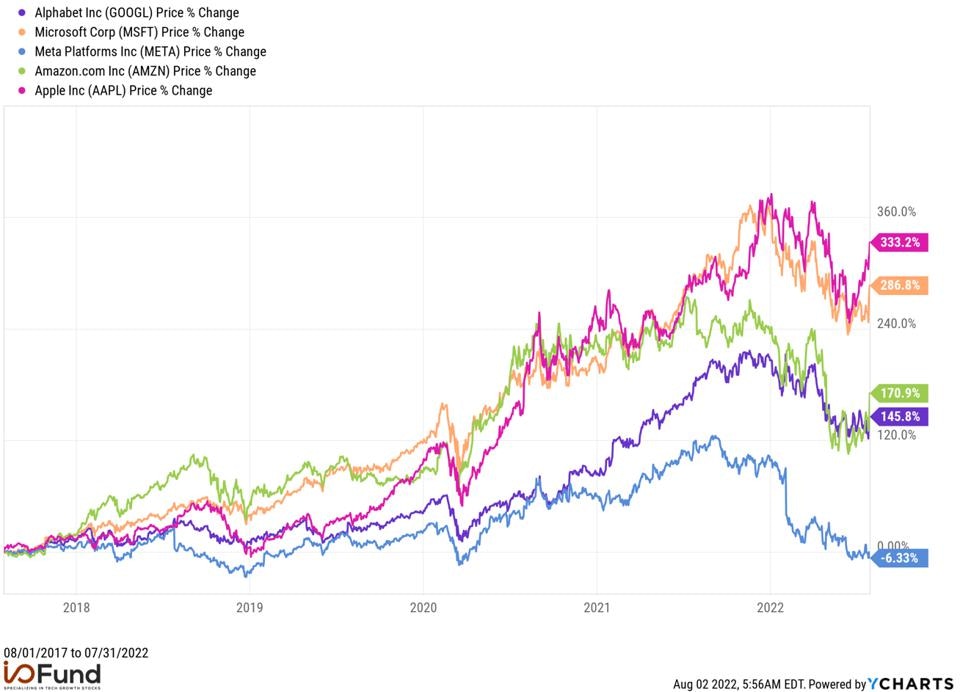

Notably, Microsoft’s stock has outperformed the market with returns of 290% in the last five fiscal years from 08/01/2017 to 07/31/2022. The stock has the second highest returns among the FAAMG stocks, behind Apple which is up 330% during this period.

Microsoft’s stock has outperformed the market with returns of 290% in the last five fiscal years from 08/01/2017 to 07/31/2022. - YCHARTS

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Microsoft’s Revenue Segments:

The company reports its revenues in three segments.

Productivity and Business Processes Segment:

The Productivity and Business Processes segment revenue grew by 13% YoY to $16.6 billion, which includes Office Commercial, Office Consumer, Dynamics, and LinkedIn. LinkedIN came in at 24% growth yet this was lower than the management’s expectation due to a slowdown in advertising revenue. According to management, Teams continues to “take share across every category” and is “seeing higher usage intensity.”

The operating income of this segment increased by 12% YoY to $7.2 billion. The segment accounts for 32% of the total revenue and 35% of the group’s total operating income. The management expects the Productivity and Business Processes segment revenue to be $16.1 billion at the mid-point of the guidance in the next quarter for a slight decline sequentially.

Intelligent Cloud Segment:

The Intelligent Cloud segment revenue grew by 20% YoY to $20.9 billion. The management’s guidance was $21.05 billion, the negative impact from the strong dollar led to the slight miss in this segment. The server products and cloud services revenue grew by 22%, helped by Azure & other cloud services growth of 40%. On a constant currency basis, Azure grew by 46% and the management is guiding for a growth of 43% (constant currency) in the next quarter.

The company also saw strong commitments from its customers as it witnessed a record number of over $100 million Azure and $1 billion deals this quarter. This has a flywheel effect for Microsoft’s data solutions and platforms, as well. Satya Nadella said in the earnings call, “More than 65% of the Fortune 1000 use 3 or more of our data solutions, and we are growing faster than the market.” Cosmos DB data volumes and transactions grew over 100% YoY for the fourth consecutive quarter.

This segment’s operating income increased by 11% YoY to $8.7 billion. The segment accounts for 40% of the Microsoft’s total revenue and 42% of the total operating income.

Intelligent Cloud revenue is expected to be $20.45 billion in the next quarter, or essentially flat sequentially.

More Personal Computing Segment:

The More Personal Computing revenue grew by 2% YoY to $14.4 billion. It was below the management’s guidance of $14.69 billion. The slowdown in this segment was expected since there is weakness in the PC business. Tracking the recent IDC preliminary results suggest that global traditional PC shipments fell 15% in Q2 2022, and the company results were good taking into consideration the macro numbers. Amy Hood said in the earnings call, “Despite the deteriorating PC market, we saw share gains again this quarter and volumes remained above pre-pandemic levels.”

The management expects More Personal Computing revenue to be $13.2 billion in the next quarter, which will be lower sequentially.

Microsoft Flexes Its Muscle on Margins

Microsoft flexed its muscle on margins during a time when many companies are stumbling on the bottom line. This was especially evidenced by Microsoft announcing an accounting change to the life of its servers to offset FX headwinds. We detail this in the section below.

The company’s gross profits increased 10% YoY to $35.4 billion. The gross margin was 68.3% compared to 69.7% in the same period last year. Excluding the impact of the change in the accounting estimate, the gross margin was relatively unchanged.

The operating margin was 39.6% compared to 41.4% in the same period last year. Excluding the impact of the change in the accounting estimate and FX, the operating margin would be relatively unchanged.

The net income was $16.7 billion or $2.23 per share compared to $16.5 billion or $2.17 per share. The strong US dollar negatively impacted revenue by $595 million and EPS by $0.04 in the recent quarter.

The company’s cash flows continued to be strong in the recent quarter. Cash from operations grew by 8% YoY to $24.6 billion (47% of revenue) and free cash flow increased by 9% YoY to $17.8 billion (34% of revenue).

The company has cash and investments of $104.8 billion and a debt of $49.8 billion. The company returned 12.4 billion to the shareholders in the form of share repurchases and dividends in Q4 FY2022, up 19% YoY, and the company spent a similar amount in Q3 FY2022.

FX Headwinds Expected to Ease in 2023

The management expects Q1 FY2023 revenue to grow 10% YoY at the mid-point of the guidance to $49.75 billion. They expect FX headwinds to be higher in the first half of the fiscal year when compared to the second half. For the full year, they expect double-digit revenue and operating income growth. The management expects to complete the acquisition of Activision Blizzard by the end of this fiscal-year and the guidance excludes the impact from the acquisition.

The company also made an accounting change in the useful life for server and network equipment assets from four to six years which will extend the depreciation expenses for the company. This will have an immediate benefit to the company’s bottom line. Amy Hood said in the earnings call, “First, effective at the start of FY '23, we are extending the depreciable useful life for server and network equipment assets in our cloud infrastructure from 4 to 6 years, which will apply to the asset balances on our balance sheet as of June 30, 2022, as well as future asset purchases.

As a result, based on the outstanding balances as of June 30, we expect fiscal year '23 operating income to be favorably impacted by approximately $3.7 billion for the full fiscal year and approximately $1.1 billion in the first quarter.”

On the other hand, Apple did not give the exact revenue guidance for the next quarter. The company’s CFO said in the earnings call, “Given the continued uncertainty around the world in the near term, we are not providing revenue guidance but we are sharing some directional insights based on the assumption that the macroeconomic outlook and COVID-related impacts to our business do not worsen from what we are projecting today for the current quarter.

Overall, we believe our year-over-year revenue growth will accelerate during the September quarter compared to the June quarter despite approximately 600 basis points of negative year-over-year impact from foreign exchange.”

Similarly, Meta Platforms guided revenue of $26 billion to $28.5 billion, or a YoY decline of 6% at the mid-point of the guidance. The guidance considers the weak advertising demand the company experienced in the recent quarter and the foreign exchange headwinds of 6%. Meta’s guidance disappointed investors as they were expecting a return of growth in the next quarter after the revenue declined for the first time in Q2.

Royston Roche, Equity Analyst at the I/O Fund, contributed to this article.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su