Tesla Stock: What You Need To Know About Q1 Earnings

April 16, 2023

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Apr 14, 2023,06:45am EDT

Two months ago, we wrote that after realizing gains of 31%, it was time to take a time out on Tesla at the $208.31 price when our firm stated: “Right now, our technical analysis is at odds with our fundamental analysis, which is often good news, as it means we will be afforded a lower entry on a stock position we plan to build.”

This analysis proved accurate as the stock topped around the time our last article was written and is trading at $180 today. Price action is key, yet what’s most important from our last article is that we clearly laid out the hurdle that is in front of Tesla – a hurdle that the Investor Day could not clear – as evidenced by a lower price following the action-packed annual event.

Rather than Investor Day, what is more important for Tesla are two key data points in the upcoming earnings report. In February, our firm stated:

“The stakes are high for Tesla because if the margins remain healthy, the stock will do quite well. However, if the margins contract, then the bears will be in control. This is a big moment for Tesla, as high average sales price has been a contentious issue for meeting its addressable market. Wall Street will want to see it's possible to do both —- serve a wider total addressable market (TAM) with more affordable prices while maintaining a healthy bottom line.”

Automotive gross margins will be the key focus for the earnings call. There are two different metrics. Automotive gross margins, excluding leases and credits, and reported Automotive gross margins that are released with earnings.

Below, we discuss what Tesla stock investors (and spectators) need to know going into Q1 Earnings in regards to these make-or-break data points.

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

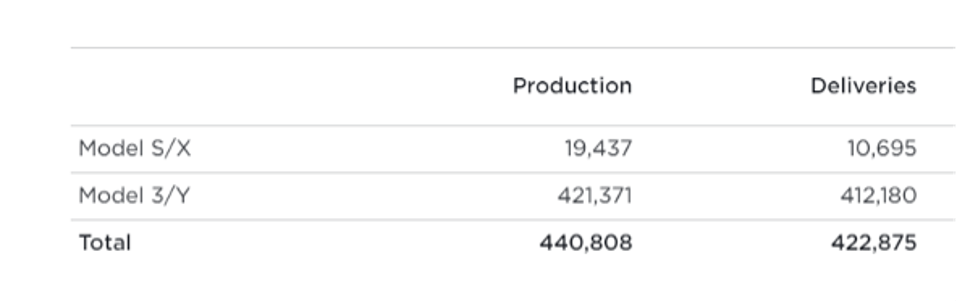

Production target:

Tesla has a production target of 1.8m car units in 2023 and average of 450,000 per quarter. On April 3, 2023, Tesla released their q123 production and deliveries. Although the 440,808 units is slightly below the quarterly average, it was in line with market expectations and on track to meet 2023 goal.

Source: I/O FUND

We will look for indications that quarterly production will increase, if its 2nd half weighted and whether the 1.8m target is attainable.

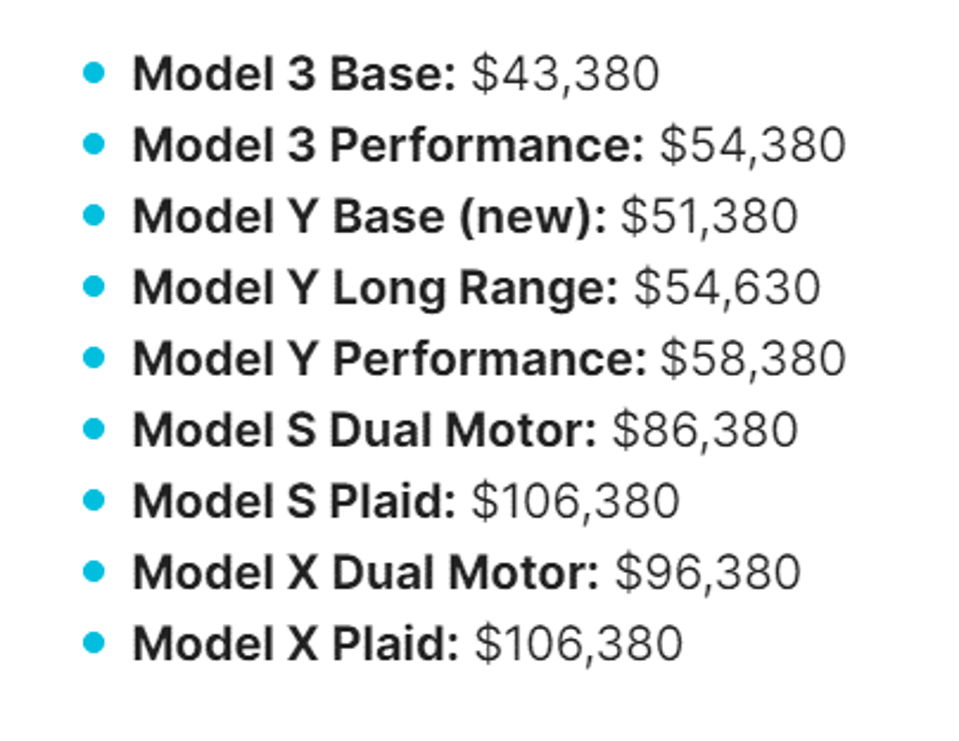

Impact of price cuts on overall ASP:

After announcing price cuts in January, Tesla announced price reductions before the Easter holiday. The April reductions were smaller than the January ones that were implemented so that certain models would qualify for the EV car tax credit. The April reductions were as follows

- Model 3 by $1,000

- Model Y by $2,000

- Model S & Y range from between $5,000 to $10,000

Models 3 and Y comprise the vast majority of overall production. After the announced price reductions, this is the estimated starting price levels as of 4/10/23 by cars.com.

Source: CARS.COM

After the January price reductions, Tesla stated that they expect ASP across all models to be above $47,000. After the April price reductions, we will monitor if Tesla reiterates this ASP target.

The I/O Fund has launched a new$99/year Premium Newsletter called "Essentials" -- this newsletter delivers premium samples for our readers who want more actionable analysis for their tech portfolios. This month, we released a stock pick that we believe will be a leader in 2023 plus a video with the buy plan.

Automotive Gross Margins

Automotive gross margins will be the key focus for the earnings call. There are two different metrics. Automotive gross margins, excluding leases and credits, and reported Automotive gross margins that are released with earnings. The former ended q422 at about 18% and is typically discussed during the earnings question and answer. It is the margin we will focus on. Any improvement will be reflected in the reported Automotive gross margins which ended q422 at 25.9%.

The key to Automotive gross margins, excluding leases and credits, are ASPS and COGS per vehicle. In the q422 conference call this is how Tesla guided future automotive gross margins. They stated ASPS will be above $47k and automotive margins above 20%.

Question

“The next question from investors is, after recent price cuts, analyst released expectations that Tesla automotive gross margin, excluding leasing and credits, will drop below 20% and average selling price around $47,000 across all models. Where do you see average selling price and gross margins after the price cuts?

Zachary Kirkhorn, CFO

So there is certainly a lot of uncertainty about how the year will unfold, but I'll share what's in our current forecast for a moment. So based upon these metrics here, we believe that we'll be above both of the metrics that are stated in the question, so 20% automotive gross margin, excluding leases and rent credits and then $47,000 ASP across all models.

There was a follow-up if cogs could go back down to $36,000. This exchange provided further insight.

Excellent. Zach, actually, I'd like to follow up on the data point you just gave on cost. If I look back at the COGS per car, you guys bottom close to $36,000 in the middle of 2021. And then the number went up as you had to face with inflation in input costs and the ramp of Berlin and Texas. And this quarter, I think we are close to $40,000 and we peaked maybe close to $42,000 at some point last year.

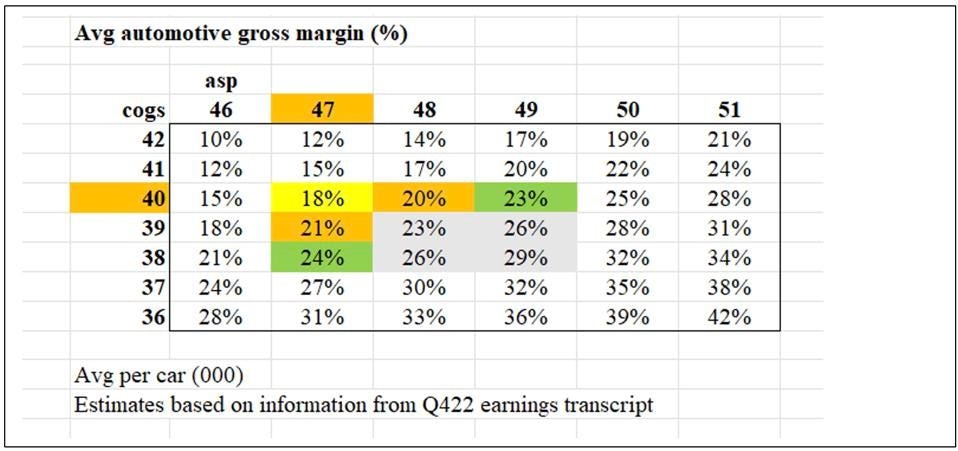

Based on this information, we put together a simple sensitivity analysis between average ASPs and COGs to determine a range of potential automotive gross margins. We estimate that margins ended q422 at 18% (yellow). Tesla has guided for ASPs greater than $47,000 and margins of greater than 20% (orange highlights). In our prior analysis, we assumed that COGs per car would remain at $40k and that higher ASP would result in margins above 20%. For example, an ASP of $48k and $49K result in 20% and 23% margins with COGS steady at $40k.

Source: I/O FUND

However, given the recent weakness in Lithium and Aluminum after the q4 call. There is the potential that Tesla’s margins may benefit even if ASPs remain at $47k. For example, if ASPS remain at 47k and COG go down to $39k and $38k, margins improve to 21% and 24%, respectively. For reference, the recent low in COGS was $36k. Given timing differences, this COGS improvement may not be seen until after Q1. If it’s not seen in Q1, to the extent Tesla discusses the potential lower COGS benefit on automotive margins, the stock will react positively.

Put another way, Tesla potentially now has two levers in can pull to increase automotive gross margins - Pricing and lower COGs per car. Either one or both can contribute to higher automotive gross margins. The result will be the same in that a gross automotive above 20% will remove short-term uncertainty.

How I/O Fund Plans to Manage our Tesla Position:

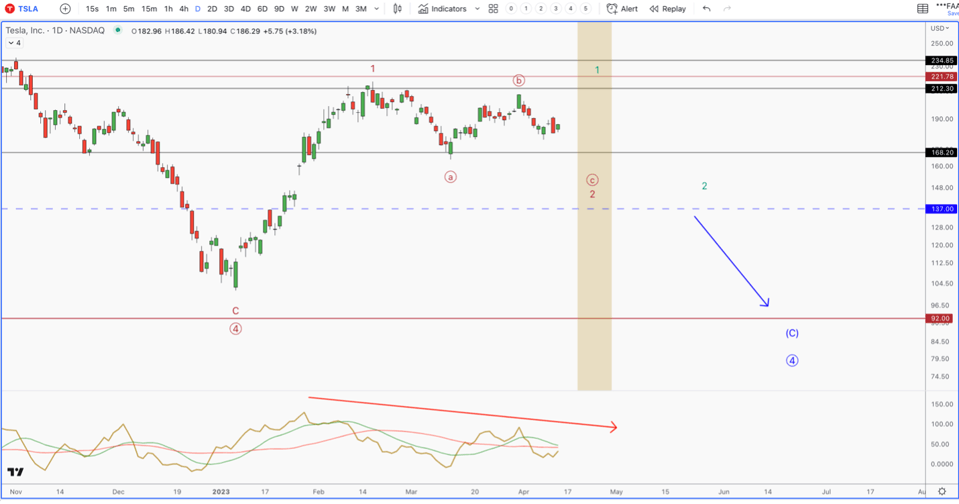

From a technical perspective, Tesla has bottomed out post Investor Day. It appears to be setting up for a fresh high before seeing a bigger pullback on the horizon. Tesla is trading in line with tech equites, so it can be affected by deteriorating macro forces, if this happens, we could see $92 as the next likely target for a major low. As long as we hold $137, this scenario can be avoided.

We could see one more swing high into late April. We do not see this as a buying opportunity. The $231-$235 region will be very strong resistance, which will occur on lower momentum. If this happens, we will look for the following pullback to add.

We have a buy level in mind, which we share with our premium research members. We believe this buy level will set us up for gains in Tesla stock in 2023. We provide in depth macro and individual stock analysis so that readers can better understand why we buy/sell. In this market, we frequently take gains. We also issue real-time trade alerts when we enter and exit stocks. YTD, our firm has held the two top performing assets in the tech industry – Nvidia and Bitcoin — at high allocations. You can learn more here.

Source: I/O FUND

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su