Apple Stock: A New Era of Mobile Saturation

March 22, 2019

Beth Kindig

Lead Tech Analyst

Debuting in 1980, Apple is nearing its 40th anniversary on the stock market. The company has undergone many pivots successfully from computers to improved operating systems, to iPods, iPhones, app stores and music services. Many of these pivots were executed beautifully, with the most recent one being Apple Music, which took a majority of market share in music streaming within 4 years in the United States.

Of course, the iPhone is Apple’s force extender. One quick glimpse at the stock chart history and it’s easy to see something important happened in 2008. The invention has sold over 2.2 billion units with an average price tag of $793. The iPhone altered the United States economy, creating a thriving developer ecosystem while 87 percent of smartphone profits despite selling 18 percent of all smartphone units. With the iPhone’s release, Apple not only became one of the biggest companies in the world, but it also has more cash reserves than most countries’ GDP at $285 billion.

There are many positives to Apple’s story beyond the iPhone, with a wearables business up over 50%, cloud services up 40%, and Apple News readership at 85 million active monthly users. Apple Music is also now the number one streaming service in the United States over Spotify and closing the gap globally with 53M subscribers vs 83M subscribers. Most importantly, Apple has a media announcement planned for March 25th, which will add to the growing services revenue.

Earnings reported on January 29th, 2019 were more encouraging than anticipated following the lowered guidance. Apple beat earnings at $4.17 compared to last years $3.89. Total revenue was lower at $84 billion, down by 4.51% and beat guidance by $312 million. Future guidance expects revenue between $55 billion and $59 billion for this quarter to be reported at the end of April. Gross margins are expected between 37 percent and 38 percent. The company has a hoard of cash and the stock pays an increasing dividend.

Investors should exercise caution, however, as the broader mobile market is slowing down and is at the point of saturation. Mobile has been the de facto leader for tech growth during this historical bull market, and has provided consistent YoY returns that the dot-com bubble would be envious of. Investors should recognize mobile has reached its top as a primary driver across tech growth stocks, and I do not believe the mobile slowdown is over yet, or that the full effects have been completely reflected in earnings.

Apple can (and will) pivot. One day, the company will be known for health services, vehicle software, as a media titan, and more. However, But to expect one quarter of decreasing iPhone sales before the stock resumes previous heights would defy the laws of the tech hype cycle. Apple simply has not hit the iPhone bottom, and the effects of mobile saturation are not fully reflected yet in the company’s earnings.

The Fifth Factor: Mobile Saturation

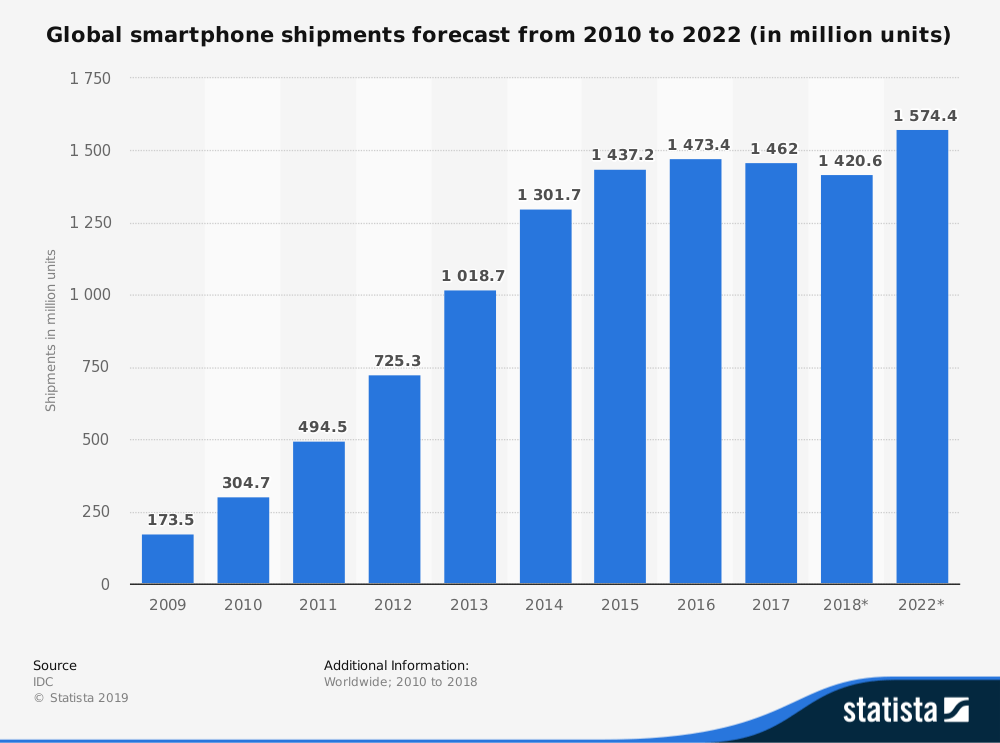

Apple noted four factors that impacted results when the company provided guidance in November: “different iPhone launch timing from a year ago, FX headwinds, supply constraints on certain products and macroeconomic conditions in emerging markets.” I would call this the 1,000 foot-view while the 30,000 foot-view tells us the fifth factor is mobile saturation. Eventually, everyone has a television set and a laptop – and now, a smartphone. This will continue to be the reality that Apple contends with.source: https://www.statista.com/statistics/263441/global-smartphone-shipments-forecast/

The smartphone market contracted in 2017 to 1.462 billion units and in 2018 to 1.42 billion units, and is expected to return to minimal yet positive growth percentages at a CAGR of 2.5%. While 1.5 billion smartphones per year is substantial, the law of saturation is likely to drive prices down, with Android owning 85% of the market today, and we see decreasing iPhone penetration in China where lower-priced competitors gain market share.

IDC estimated Apple will sell 242 million smartphones by 2022 up from 221 million in 2018. The issue with these estimates is that IDC does not break down the percentage of potential decline between 2018 to 2022. The most up to date number available from IDC is an anticipated decline of 0.8% in worldwide smartphone sales in 2019, published on March 6th.

We saw China decline 10% last year in global shipments of smartphones. Taiwanese company, TSMC, is the sole supplier of iPhone core processor chips and told Nikkei Asian Review that the company is cautious about demand for high-end smart phones, which is a nod toward Apple from a main supplier. Samsung Electronic’s Vice President Lee Myung-jin told investors in late January that “demand for memory chips has declined in the fourth quarter as external circumstances worsened and customers adjusted their orders” and he believes the decline “will continue in the first quarter, as key customers keep adjusting their orders.”

Huawei eats market share in Asia and is currently the world’s fastest-growing smartphone seller. The company sold 200-million units in 2018, posting 30% growth from the 153 million units sold in 2017 and has seen a 66x increase from the 3 million units sold in 2010.

Huawei edged out Apple with 14.6% of the global smartphone market compared to Apple’s 13.2% share in Q3 2018. China’s Xiaomi also posted 21.2% growth. Therefore, a resolution to the trade war or other macro conditions may not actually revive iPhone sales as Chinese smartphone makers appear determined to gain domestic ground. In 2018, the iPhone had an average sales price (ASP) of $793 while Huawei’s ASP is $269 in China and about $380 in Europe. The ASP for Xiaomi is $138. Politics and trade war aside, one indication of saturation and post-euphoria consumer behavior is when consumers seek lower prices as a trend becomes more commonplace. Longer replacement cycles and lack of innovation on the device, such as new applications, also point towards a market at its peak.

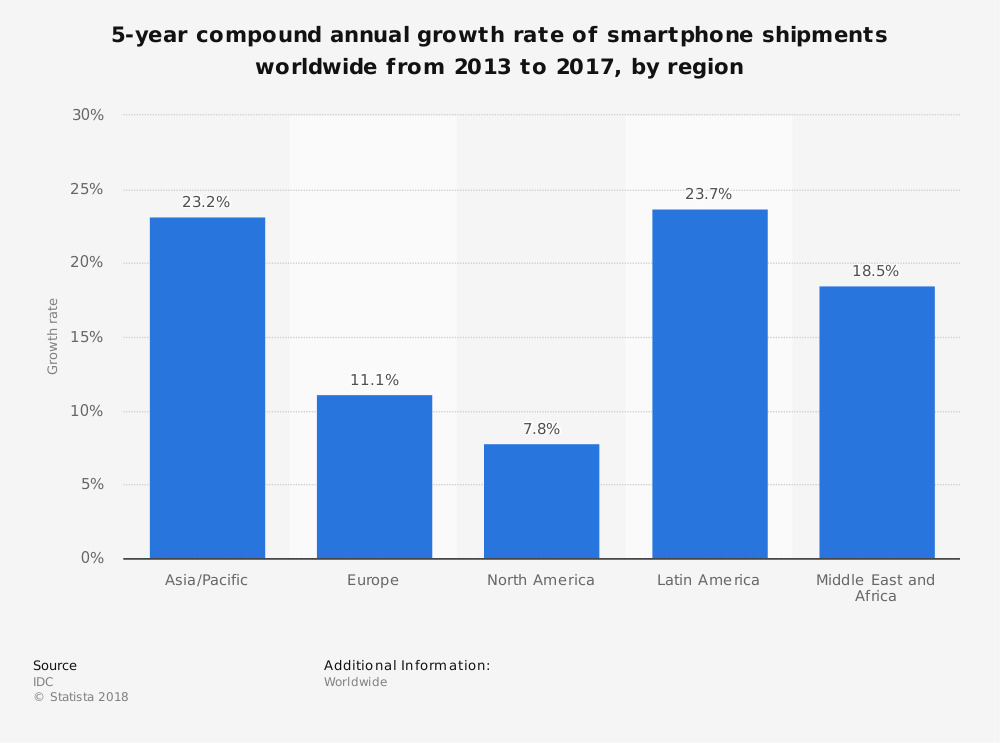

China represents roughly 1/3rd of smartphone penetration compared to the United States at 1/12th. We can see over the last few years that the United States had the lowest CAGR of any region globally. According to Pew Research, 77% of Americans own smartphones, a jump from 35% in 2011. If Apple is losing market share in China, this leaves Latin America, where the average sales price of the iPhone is prohibitive.

Apple’s Pivot to Services

There is no reason for investors to not be hopeful about the upcoming media announcement, although as Apple Music has shown, it may take up to 3 years before it adds significantly to the top line. Many investors may ignore the mobile saturation issues or believe the bulk of the iPhone decline is priced into the stock. If Apple is a core holding, the arrival of a new direction is likely to be welcomed. Today, services account for 18% of Apple’s overall quarterly revenue at $9.9 billion or $37 billion annually with handsome margins of 62.8%. Apple has executed Apple Music beautifully since 2015 and is now the top music streaming service in the United States, much to Spotify’s chagrin. To give you a comparison and a glimpse into the media services possibilities, it took Spotify twelve years to gain 80+ million subscribers while Apple reported over 50 million in three (brief) years. OTT media endeavors require a note of caution, however, especially for those companies creating original content. Historically speaking, Amazon had a content budget of $4.5 billion in 2017 for an audience of 27 million viewers. As Jeff Bezos told Hollywood Reporter at that time, “When people join Prime, they buy more of everything” and the losses on original content are recovered. Apple will also need to recover the losses on original content. Some anticipate that Apple will recoup the costs of original content with a 30% revenue split from the other channels they plan to aggregate on the platform.

While Apple may be able to pull off migrating users from their trusted favorites, such as Hulu, Prime, Netflix, Showtime and HBO, it will be interesting to see how quickly Apple can make back the investment of paying the likes of Oprah Winfrey, Jennifer Aniston and more big names for the original content they plan to offer. There’s also speculation Apple may bundle services like Spotify and Hulu do today, where the two services are offered for about a $3 discount at $17.99. Regardless the monetization strategy, Apple’s media announcement is likely to help the stock, despite the many warning signs of a distressed mobile market.

Takeaway:

Apple has a history of successful pivots, and services will add a projected $100 billion in revenue by 2023. However, I believe we haven’t found a bottom yet on mobile saturation. In 2017, Apple sold 19 percent of the smartphones purchased globally, yet captured 87 percent of the profits. My prediction is that those days of the peak mobile market are over. Even if earnings see-saw for a few quarters, there will be a downward trendline from this peak. Apple will make a better investment once mobile saturation has run its course. I believe the stock price we see today is overly optimistic in regards to the eventual slow down across the mobile industry.

Image credit: Apple

More To Explore

Newsletter

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de