Will We See Another Dot-Com Crash In Tech?

June 05, 2020

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on May 15, 2020,12:42am EDT

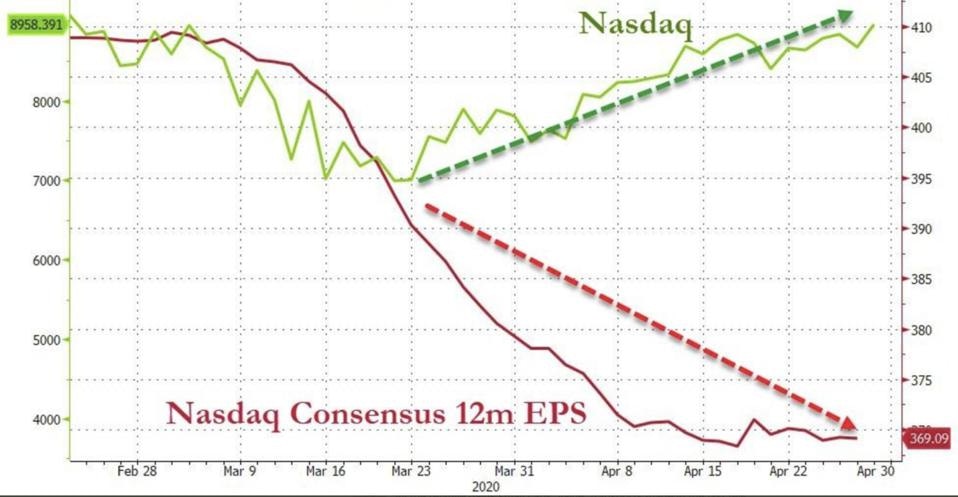

Tech’s comeback since March has been nothing less than spectacular considering the backdrop of record unemployment and contracting GDP. According to a survey of fifty companies by FactSet, 60% had withdrawn guidance for the year. FactSet also estimates that the S&P 500’s earnings for 2020 have fallen 22% since the beginning of the year, while 2021 earnings have declined 13%.

Meanwhile, many tech stocks have reached all-time highs including one-day moves of up to 40% even when companies withdraw guidance. Twilio, for instance, rallied from $122 to $170 based on an 11% revenue surprise with total returns of 140% in the past two months. Twilio is hardly the exception with Teladoc up 115% and Fastly’s one-day move of 40% on May 7th.

Last month, Goldman Sachs analysts said in a financial note that the S&P 500 index concentration in the top tech companies—Facebook, Amazon, Apple, Microsoft, and Alphabet— was the greatest it has been in 20 years. Meanwhile, these mega-cap companies have reported mixed earnings results (Amazon) or pulled second quarter and full-year guidance (Facebook and Apple).

In a picture, this is what that looks like:

Tyler Durden, Zero Hedge from the article “"Poor Decisions" Galore As Newbie Millennial/Gen-X-ersPour Into Expensive Stock Market: https://www.zerohedge.com/personal-finance/poor-decisions-galore-newbie-millennialgen-x-ers-pour-expensive-stock-market

The saying “history does not repeat but it rhymes” has not yet applied to the dot-com bubble, when five years of euphoria burst into a 78% drop in prices over two years. Tech has largely gone unscathed as it has bumped oil from being the number one industry.

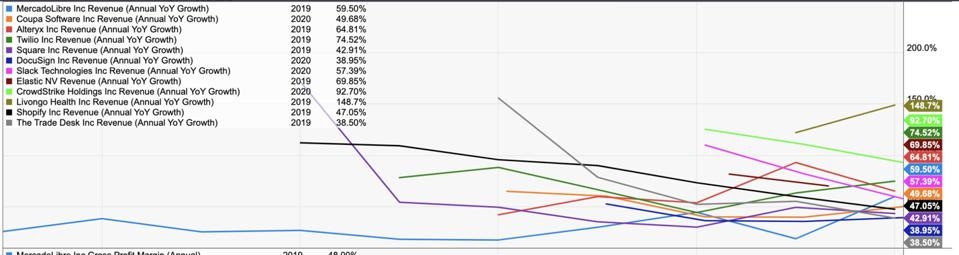

There is some solid support as to why this is not a tech bubble. Mainly, technology now runs nearly every industry. The second reason is that higher valuations are more sustainable today as the revenue growth from tech is much higher than other industries.

Tech Industry Growth has 40-80% growth with outliers up to 148%

TWITTER HTTPS://TWITTER.COM/SAXENA_PURU/STATUS/1256748503050539008

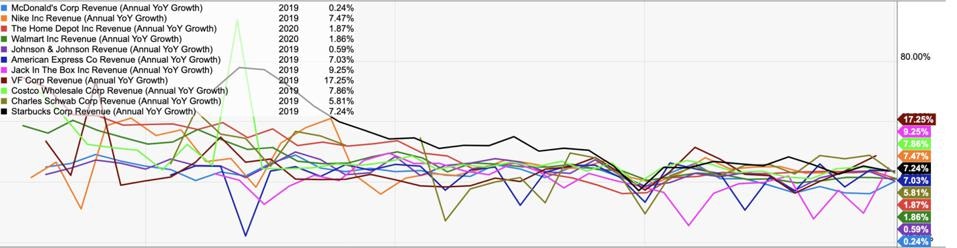

Versus other industries with 1-9% growth with outliers up to 17%

TWITTER HTTPS://TWITTER.COM/SAXENA_PURU/STATUS/1256748503050539008

In addition, cloud software and platforms also allow companies to scale proportionate to revenue growth. There is less overhead and this helps companies keep costs low as you can scale quickly in either direction.

Nearly a decade ago, Marc Andreessen famously said “software is eating the world” in an essay that spelled out how software was disrupting nearly every industry with “real, high-growth, high-margin, highly defensible businesses.” He questioned the low PE ratios of companies like Apple, which at the time was trading at 15 P/E. Notably, Andreessen’s essay came in close proximation to Facebook’s public offering, as well as Zynga, Groupon, Skype and many other exits for his firm’s portfolio.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

At the time, he pointed out that fast-growing companies like Facebook and Twitter were conjuring up memories of the dot-com bubble in 2011: “With scars from the heyday of Webvan and Pets.com still fresh in the investor psyche, people are asking, “Isn’t this just a dangerous new bubble?”

Perhaps just as dangerous as thinking any fast-growing tech company with a high valuation is not a bubble is the idea that any fast-growing tech company with a high valuation is a bubble. This is because the market has a way of doing what you least expect.

Pre-Pandemic, Silicon Valley Grew Quiet

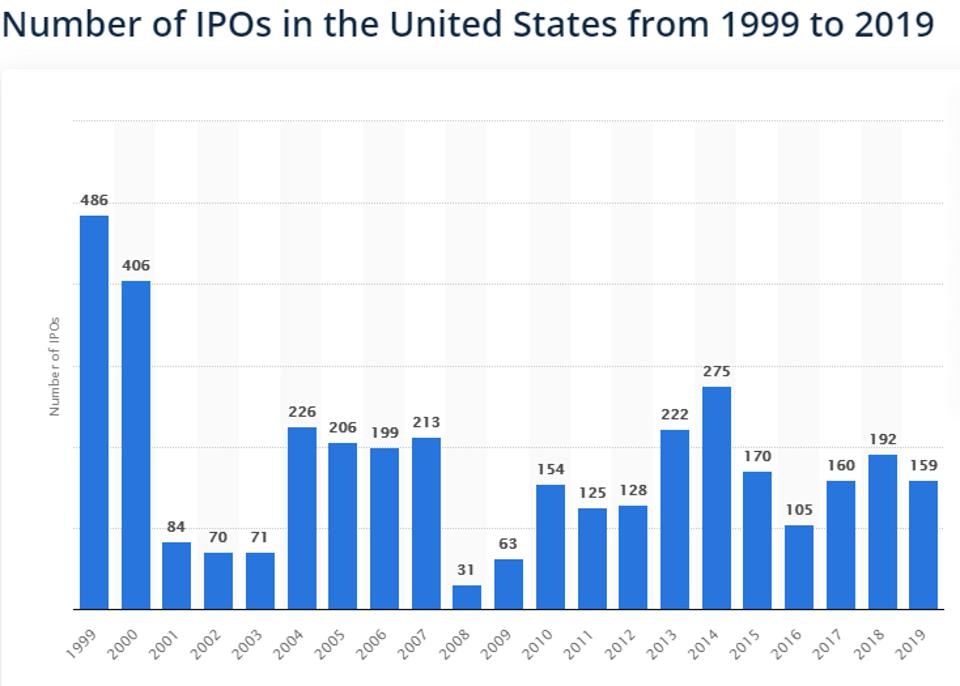

If looking at the number of IPOs, we are not in a bubble as the years 2018-2019 saw less than half the number of IPOs during 1999-2000.

Beth.Technology

However, the value of IPO exits does look bubble-like. According to Pitchbook, the value of exits for venture-backed companies hit a record $256.4 billion in 2019. 82 venture-based IPOs accounted for 78% of the total value, or $198.7 billion – more than the previous four years combined (this was partly due to Uber and Lyft).

The exits were successful for venture capitalists as the $223 billion in post-money valuations came from $35 billion in venture investment, or a return of 637%. In turn, this means the public markets paid a significant premium.

Also, the years that followed the dot-com bust saw a serious leveling off. It is the absence of early stage deals in tech right now that is more concerning. Pre-pandemic, Silicon Valley was already noticeably quiet.

Forbes also recently reported on the slowdown in venture capital being ill-timed with the effects of the coronavirus forcing many startups to shut down. This followed a 16% drop in venture capital deals in Q4. The CEO of Starsky Robotics stated, “the downpour of investor interest became a drizzle.” As the article points out, the failure rates of 2020 could end up resembling 2001.

Recently, I published on the lack of venture funding in the Series A and Series B stage for tech companies. When combined with the data on initial public offerings from last year, we see a clear signal from venture capitalists that the exit window may be closing (or is already closed).

For instance, as reported by The Information, early-stage software deals in 2019 declined from 388 deals down to 279. In the seed stage, the number was below 200, or the lowest in six years. According to Inc.com and CB Insights, the estimate for Series A funding has dropped from one in three startups to one in six startups with an estimated 1,000 startups not receiving funding this year.

Meanwhile, the public market is flooded with high growth software companies that report over 40% growth due to an inverse law of small numbers. Basically, it’s easier to post rapid growth early-on but harder to sustain this growth.

Conclusion:

Many investors focus on valuations as the indication for a bubble. As pointed out, this can be misleading as hypergrowth companies are often outliers. In fact, the companies that challenge key metrics the most are often the ones that see the most upside. Amazon and Netflix are prime examples.

Valuations aside, there is a glut of high-growth software companies on the market that have not been tested by a less-than-ideal economy or slowing business cycle. This may not create a bubble, but it can create losses for both institutional and retail investors as the market attempts to guess the winners and is confronted by those that fizzle out.

The more that startups shut their doors, as well, the fewer cloud software customers there will be as the two ecosystems are closely intertwined. The recent pullback in March did not afford the opportunity to find the stable winners before hyper-speculation resumed.

More To Explore

Newsletter

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i

Google TPU v8 vs Nvidia: How Inference Is Rewriting the AI Market

In April, Google announced it would begin selling its TPUs to select third-party data center operators, which is something the market has anticipated for nearly a decade. The TPU-versus-Nvidia-GPU deb