Lyft: Risky Valuation and No Intellectual Property

March 14, 2019

Beth Kindig

Lead Tech Analyst

Who doesn’t love the ease of using a mobile application to order a ride rather than stand awkwardly on a street corner hailing a taxi? Once I downloaded Lyft and Uber, I said goodbye to the rejection of occupied taxis forever. Lyft and Uber represent free market evolution by offering a better service than the outdated competition. The apps shave off valuable time with door-side pickup, and the overall cost is cheaper than taxis too. In San Francisco, these apps have become ubiquitous, but these biases have to take a backseat to investment discipline.

There is a tinge of glam to the upcoming Lyft IPO road show, and the anticipated IPO from Uber in 2019. Silicon Valley produces a lot of winners; however, I believe investors should be careful with both of these IPOs due to exuberant valuations, accelerating net losses, and a lack of geographic expansion opportunities. Yet, another concern is the liquidity event the large cap IPO provides, and the level of PR that can be bought leading up to the IPO, which will likely focus on the growing sales. There is evidence the growing revenue has been subsidized, therefore, revenue is not a safe bet when evaluating these particular stocks, and the prospectus fails to outline a clear path to profitability.

1. Risky Valuation with Accelerating Net Losses

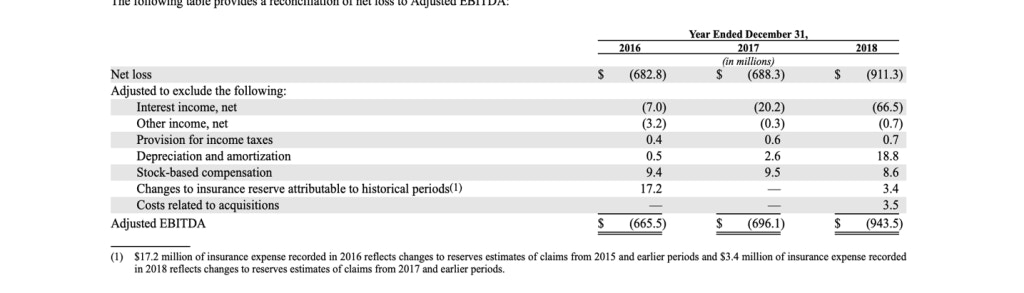

Lyft went from a $7 billion valuation in 2017 to a $15 billion valuation in 2018 and is now seeking a $20-$25 billion valuation on the public markets. The problem with this rising valuation is that losses are progressive with $2.6 billion in revenue in 2018 but a $911.3 million loss. Due to these losses, Lyft may need to borrow or raise more equity after its first year on the public market, which means debt or dilutive stock offerings.

Lyft’s sales, on the other hand, appear positive on the surface with incredible growth year-over-year from $343M in 2016 to $1.05 billion in 2017 and 100%+ growth in 2018 at $2.15 billion. The problem is that the losses are also accelerating.

Lyft’s filing also points to an important issue with growth marketing tactics for user acquisition (UA) and user retention. I’ll copy the paragraph here verbatim from the S-1 Filing and translate my understanding of how ridesharing apps subsidize UA.

“Ability to Cost-Effectively Attract and Retain Riders and Increase Our Share of Their Transportation Spend

We grow our business by attracting new riders to our platform and increasing their usage of our platform over time. To effectively attract riders, we focus on driving organic adoption in our rider base, and do so with investments in brand and growth marketing to increase consumer awareness. We also offer incentives for first time riders to try Lyft, as well as incentives for existing drivers and riders to refer new riders. Once riders start using Lyft, we provide a quality experience and a diverse offering of products to accommodate different transportation use cases, retain riders and encourage repeat usage. We often also provide incentives to existing riders to encourage them to expand their use of our platform. If we fail to continue to attract riders to our platform and grow our rider base, expand riders’ usage of our platform over time or increase our share of riders’ transportation spend, our results of operations would be harmed.”

The translation here is that Lyft and Uber pay incentives to acquire and retain users. In gaming, a company might spend $8 to acquire a user with a lifetime value of $15 per user for a profit of $7. The problem with ride-sharing apps is that the incentives offered do not cover the costs of the ride, and that is one reason we see strong sales growth mired by accelerating losses.

Reuters has some historic information on this dated back to 2015, when Uber passengers paid only 41 percent of the actual cost of their trips. At the time, Reuters reported that this creates an “artificial signal about the size of the market” with Uber releasing limited financial data that showed losses of $708 million per quarter.

Going back to Lyft, the takeaway is that these incentives are creating an artificial signal about revenue, which is ultimately overshadowed by net losses. The problem with subsidizing rides is that public market investors aren’t able to determine what will be required for profitability, how much the cost of the ride will have to increase, and if that will impede the demand to ride share.

2. “Human Resources” Business Model is Not Profitable

Lyft and Uber have scaled their companies but it comes with the variable cost of human labor. Ideally, you want fixed costs for R&D on platforms, software, hardware and other products to create the margins that technology is known for. Lyft and Uber are mobile applications, but the business model is more of a large-cap human resources department with many variables around wages, and potentially regulations due to independent contractor classifications. (There was a recent $20 million settlement due to the misclassification of drivers in California).

As you’ll see below, the mobile app holds very little intellectual property, with the primary value of the product resting in the mobilization of a massive work force of nearly 2 million people, per Lyft’s S-1 Filing. To some regard, Lyft and Uber are not technology companies, rather they are very large human resource departments run through an application. Whenever you are involved with labor at this level, regulations and wages eat at profits.

3. Autonomous Vehicles 5-10 Years Out

This leads us to the only hope for ride-sharing to become profitable, which would be to remove the human driver through autonomous vehicles. Here’s some information from my autonomous vehicle analysis published in October on AV delays as it pertains to the timeline of when Lyft or Uber could potentially deploy driverless and how investors should exercise caution here:

“The regulation hurdles between Level 2 and Level 3 and delayed deployments will put immense pressure on stocks that are overvalued based on AV speculation. ABI Research, an advisory firm that reports on market-foresight trends, predicts 8 million consumer vehicles with Level 3 to Level 5 autonomy will ship in 2025. Compare this to the 94.5 million vehicles sold in 2017 which equates to 8.5% of sales. This is a small and fairly insignificant percentage of market share to be chasing 7-years ahead of deployment. Yet, investors are pouring cash into hyped up stocks- and the press plays a large role in this. Headlines are a continual churn of autonomous vehicle “moments” – every partnership, every mile driven, every make and model that adds another feature. To be clear, we’ve only gone from a Level 1 to Level 2. We are not able to release Level 3 AV right now – and yes, that includes Tesla.

Note: I was the first to write about the issues around autonomous vehicle deployment and how this will affect stocks (this prediction was before GM announced layoffs and before Tesla reported AV deployment issues, as well).

4. Total Addressable Market & Lack of Intellectual Property

I saved some of the best for last, as a paramount risk to both Uber and Lyft is total addressable market. Room for geographic expansion is limited beyond the United States, other than a few outlier countries like Saudi Arabia. Of course, the underlying issue with TAM is a lack of intellectual property with an easy-to-duplicate mobile application that leverages common app features such as GPS location and SMS/voice. Although it is common to discuss the ridesharing ecosystem as “Lyft Vs. Uber,” the fact is the global competitors in their respective geographies are a serious deterrent to future growth.

Here is a summary of the global ride-sharing market:

Asia: China’s Didi surpassed Uber as the world’s most valuable startup. Both Uber and Didi have something in common too; their investor is SoftBank. Grab is Singapore’s ridesharing service and bought Uber out of the market in Southeast Asia. (Uber was losing money here). India has a domestic ridesharing company named Ola, who can operate for as cheap as 8 cents per kilometer.

Europe: Taxify and MyTaxiApp: I went to MWC in Barcelona about two weeks ago and hailed about thirty rides in one week through a ride-sharing app called MyTaxi. One interesting feature behind the MyTaxiApp is that it leverages unionized cab drivers through the app rather than mobilizing independent contractors. The fares are cheaper than Uber, too, which is why Uber wasn’t able to capture Europe.

Middle East: The Dubai-based ride-hailing app Careem serves the Middle East and Africa with 33 million users.

Latin America: Uber is doing well in Latin America with 25 million monthly active users, a presence in 200 million metro areas and is in 15 countries. Lyft is unlikely to compete with Uber here. China’s Didi is moving forward on competing in Latin America.

Japan: Japan could be a potential market although the overall sentiment is that Japan has major regulatory hurdles and the high-quality taxi system does not need much improvement.

Takeaway: Due to the reasons I’ve outlined, my concern is that the valuations and late-stage IPO is better for private market liquidity and not a sustained growth story for the public markets. The accelerating losses tell a different story than the 100%+ revenue, and if investors are subsidizing rides, then buying PR focused on sales is cheap. There is also no clear path to geographic expansion for near-term growth. Will Uber and Lyft be around in 5 years? Sure. Yelp, Snap and Zynga are still around …

More To Explore

Newsletter

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i

Google TPU v8 vs Nvidia: How Inference Is Rewriting the AI Market

In April, Google announced it would begin selling its TPUs to select third-party data center operators, which is something the market has anticipated for nearly a decade. The TPU-versus-Nvidia-GPU deb