DLocal: Strong Growth, Premium Valuation

June 17, 2022

Royston Roche

Equity Analyst

Fintech companies are disrupting the global economy with new and innovative products. Technological advancements have led to considerable investments in this sector and traditional finance companies have not been able to efficiently cater to changing business needs. Of the recent fintech quarterly earnings, D-Local stood out for its strong bottom line. The company’s cloud-based payment platform is popular in the emerging markets of Latin America, including Brazil, Argentina, Mexico, Colombia, Uruguay, and Chile. It allows international enterprises to operate in the emerging markets by using the company’s payment platform to receive and make payments, and comply with local regulations, taxes, foreign exchange, and fraud management. The payment service is used by companies such as Amazon, Microsoft, Didi, Mailchimp, Wix, Shopify, Wikimedia, etc.

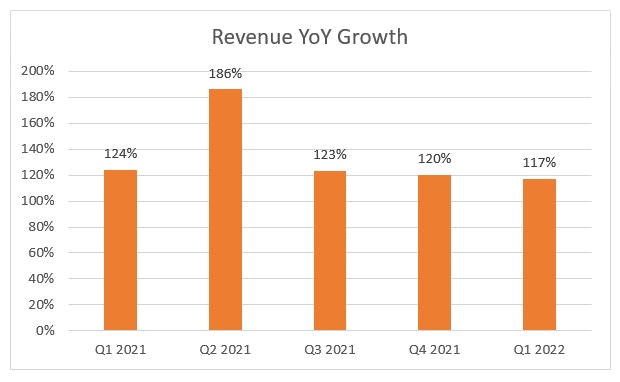

DLocal released its Q1 2022 results last month. The company’s revenues grew by 117% year-over-year to $87.5 million. It beat the Wall Street revenue estimates by 5.9%. The company also reported a 30% net profit margin in the recent quarter. The solid top-line growth, earnings beat, and good profits sent the stock soaring 15% the following day of the announcement of the results.

Below, we discuss the market opportunity, the company’s background and a full financial picture on this hot fintech stock.

Market Opportunity

According to Vantage Market Research, the fintech market is expected to reach $332.5 billion by 2028 from $112.5 billion in 2021, growing at a compound annual growth rate (CAGR) of 20% from 2022 to 2028.

KPMG published a Pulse of Fintech H2’21 report suggests that the investment in the fintech sector was strong in 2021, and the trend is expected to continue in 2022. According to the report, the global fintech investment reached $210 billion in 2021. The payments category drew a record in venture capital funding. The report also highlights the record investment in emerging markets like Latin America and Africa.

Mike Louw, Partner, Head of M&A KPMG South Africa, said, “The northern hemisphere is a crowded marketplace and multiples are at an all-time high. This makes Africa an attractive alternative. Global PE firms and investors are seeing the opportunity. It’s put the continent on the fintech map.”

Ricardo Anhesini, Head of Financial Services, LATAM KPMG Brazil said, “The growth of fintech in Latin America is a classic example of ‘leapfrogging’ — fintechs have leveraged the need for financial inclusion amongst large swathes of the population to move straight to a new generation of services.”

Company Overview and product niche

The company was founded in 2016 in Uruguay. The shares were listed on the Nasdaq stock exchange in June 2021. Through its single API, technology platform, and a single contract, the company helps global enterprise merchants to be paid (pay-in) and make payments (pay-out) in the countries it operates. The company’s cloud-based platform can make cross borders and local payments in 37 countries while enabling global merchants to connect to over 700 local payment methods.

The company’s Marketplace payments solutions allow its sellers to receive payments in the local payment methods through credit or debit cards, bank transfers, and cash. The company makes it easier for global enterprises to operate in the region by partnering with a local payment platform by saving the hassle of complex regulations and solving difficulties that arise due to the lack of efficient banking facilities in these countries.

The company’s tie-up with alternative payment methods (APM) providers plays a role in the unbanked population. In Brazil alone, there were 34 million unbanked adults, according to a study by Instituto Locomotiva conducted in January 2021.

The company also cited in the F-1 the research from Americas Market Intelligence (AMI). In Brazil, domestic credit cards constituted 55% of the total e-commerce payment volumes, followed by alternative payment methods at 21%, cash at 14%, and the rest 10% of international credit cards. It highlights why the company has been popular in emerging markets and can easily bridge a gap in places with a high percentage of cash transactions and consumers using local payment providers.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

For example, one of Brazil’s popular alternative payment methods is Boleto Bancario. Boleto means a ticket with a due date and the amount to be paid. Previously, it was only cash, and now the payment can also be made through bank accounts or in various branches, post offices, and ATMs to use the goods and services. Boleto payments were typically confirmed in 2-3 days, however, this time is reduced to a few minutes through the company’s API’s. This shows how the company’s tie-ups with APM providers are successful.

The company has been a boon to global enterprises by solving the problem of dealing with tough regulations, tax complications, and fraud detection. The emerging markets are witnessing rapid e-commerce growth. Due to the under penetration of the digital economy, emerging markets are the hot spot for fintech companies.

Pay-In

The company’s pay-in solution helps merchants to offer services and receive payments in various payment methods like international and local cards, bank transfers, cash, and other alternative payment methods. Examples include: Microsoft sells its products in Nigeria and can accept payments from local payment providers. Due to the company’s single API they can easily expand to all countries where DLocal operates.

Pay-Out

The company’s pay-out solution facilities global companies to make payments in the countries in which DLocal operates. The company ensures that the payments are to the registered bank accounts of the users in accordance to the regulatory requirements. For example, Ride-hailing companies can make secure payments to their drivers in the emerging markets through the DLocal platform.

Marketplaces

Marketplaces allow sellers to sell internationally and receive money in their local currency. For example, in many cases, international sellers will not be able to sell in emerging markets since they will not have local bank accounts to collect payments. In this case, the marketplace onboards the sellers as they need to comply with local regulations and DLocal will facilitate receiving the payment in the local country and then send money to the international sellers.

Financials

The company has delivered strong top-line growth with good profit margins. In the recent Q1 2022 results, revenue grew by 117% YoY to $87.5 million. It was the fifth consecutive quarter of triple-digit growth. While the triple-digit growth rate is not sustainable into the future, Wall Street analysts still expect strong revenue growth to continue as they forecast revenue to grow 74% in the next quarter, followed by 58% in Q3 and 59% in Q4.

For the full year 2021, revenue grew by 134% YoY to $244 million. Wall Street analysts expect revenue to grow 73% YoY to $422 million in 2022 and 52% YoY to $640 million in 2023.

Source: YCharts

The company earns revenues from fees charged to the merchants for payment processing services. The company’s total payment value (TPV) accelerated by 127% to $2.1 billion. The take rate was 4.2% in Q1 2022 quarter compared to 4.1% in Q4 2021 and 4.3% in Q1 2021. The formula for take rate is revenues/ total payment volume.

The company’s business is not dependent on a single industry and has a diversified base of more than ten business verticals. The company is also geographically diversified to over 37 countries which is positive.

The LatAm region revenue grew by 116% YoY to $78 million and accounted for 89% of the Q1 2022 revenue. The Asia Africa region’s revenue grew by 127% YoY to $10 million and accounted for the remaining 11%. The company expects the revenue share from Asia and the African region to gradually increase over a period of time as the company cross-sells to merchants that originally began their relationships in the Latin American area.

The company has been able to grow its revenues with its existing customers, which is demonstrated by the strong net retention rates (NRR). The NRR in the Q1 2022 was 190% compared to 198% in Q4 2021. The high NRR is not sustainable, and the management expects the NRR to be over 150% for the full year of 2022, which is still good.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Sebastian Kanovich, CEO of the company said in the recent earnings call, “So we built the whole platform in local on the premise that it's one API, one contract and one platform for everything we do. So it's extremely simple for merchants to expand with us. That's the key driver behind our NRR. Merchants start with us in one geography, and they continue to move into other products and geographies without any friction. That's why you see us continue expanding geographically. We want to make sure we have more attachment.”

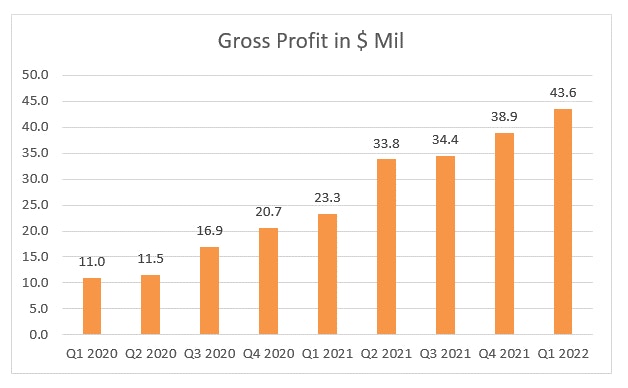

The company’s gross profits grew by 87% YoY to $43.6 million, with a gross profit margin of 49.8%. The company’s CFO, Diego Canay, said in the earnings call, “We continue to expand our gross profit and EBITDA. Starting with our gross profit, as we have mentioned in the past, our commercial focus is to increase our gross profit dollars per merchant. As a result, our gross profit continues to grow at a healthy rate.”

The company’s CEO also echoed a similar tone. He said, “When we ask our commercial teams and the way we incentivize them, it's purely on gross profit dollars to make sure that we are adding more dollars to [our] P&L.”

Source: YCharts

The company’s net profit came in at $26.3 million compared to $16.9 million for the same period last year. The net profit margin was 30% in Q1 2022, which is at the same level as the H2 2021 and lower than the 42% in Q1 2021.

The adjusted EBITDA margin was 38% in Q1 2022 compared to 38% in Q4 2021 and 44% in Q1 2021. The adjusted EBITDA margin was partly lower due to the higher share-based compensation in the recent quarter. However, the management is guiding an above 35% EBITDA margin for the full year, which is positive.

Risks:

The company’s revenue growth is slowing down from the triple-digit growth in the past five quarters is a risk to consider. The company’s costs have increased due to the return of in-person marketing and travel expenses. Also, the stock is currently trading at a forward P/S ratio of 17. The high valuations are another risk to consider with rising interest rates and macro uncertainty.

Our firm tends to be wary of IPOs in general and we covered the risks associated to IPOs last year here. We are particularly sensitive to companies that go public with very high growth rates that decelerate quickly, in this case, DLocal will have decelerated by nearly 50% from 186% in Fiscal Q2 to 74%.

Conclusion

The company has demonstrated strong revenue growth with good profits. It has developed a niche in the fast-growing emerging markets. However, considering the current macro uncertainty and the risks mentioned above, we are not interested to buying the stock at the current levels.

Please note: The I/O Fund conducts research and draws conclusions for the company’s portfolio. We then share that information with our readers and offer real-time trade notifications. This is not a guarantee of a stock’s performance and it is not financial advice. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis. Beth Kindig and the I/O Fund do not own DLocal at time of writing and have no plans to enter the stock in the next 72 hours.

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su