Netflix Stock Could Rally With Ad-Supported Content

June 29, 2022

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Jun 24, 2022,01:43am EDT

Netflix’s stock is down a staggering 71% year-to-date. The stock’s fall from grace includes dropping its FAANG-status as the company’s market cap has decreased from $300 billion to $75 billion. This was partly due to the company reporting it lost subscribers for the first time since 2011, with a loss of 200,000 subscribers in the most recent quarter. The company also forecast a decline of 2 million paid subscribers for the second quarter.

The earnings report caused the stock to immediately lose 35% of its value. Bill Ackman sold his Netflix shares for a loss of $450 million in three months, with some goading him for his decision while others congratulated Pershing Capital for being bold and walking away from a losing position.

Meanwhile, our focus was elsewhere. In our Netflix coverage following its earnings report, we had stated “we can’t help but salivate” over which ad platform Netflix might choose to power ads to hundreds of millions of viewers. Primarily, this is because we have consistently discussed why the trend of CTV ads has plenty of runway even during an epic market selloff.

The key point is this: the global juggernaut in media is essentially stating that CTV ads are the future for streaming.

Below, we discuss why a new perspective is needed as the 200,000-miss last quarter and the 2 million miss this quarter pales in comparison to the 100 million viewers who are sharing passwords that Netflix intends to monetize. In other words, I would argue the day that Netflix’s stock price dropped 35% was consequently one of the most important days in the company’s history in terms of its chances for a boost in revenue and a renewed uptrend. Patience, though, will be required, as Netflix has work to do (minimum one to two years for full global roll-out). Yet the path to adding more subscribers is finally clear for Netflix and will pay off long-term especially during times of inflation or muted consumer confidence as it drives down household costs across fragmented subscriptions.

Netflix’s Q1 Earnings

The company reported revenue of $7.9 billion, up 10%. Excluding FX headwinds, the revenue growth in the quarter was 14%. The company guided for 10% growth in the upcoming quarter for $8.05 billion in revenue. Net cash from operations was up from $777 million to $923 million.

Netflix has maintained a healthy operating margin above 20% for most quarters and EPS beat estimates at $3.53 compared to $3.75 EPS a year ago. However, the issue with Netflix has been the lumpy free cash flow since the company began producing original content with the majority of the company’s history being deep in the red on cash flow. The recent quarter was positive $802 million, yet the company still holds gross debt of $14.6 billion on the balance sheet and net debt of $8.6 billion.

Netflix reported a subscriber miss of 200,000, yet excluding Russia, the company had net adds of 500,000 as Russia contributed to a miss of 700,000. Regardless, it’s the upcoming quarter that has the market concerned as Netflix is guiding for a loss of 2 million subscribers.

Notably, Netflix has moved towards staggered releases of hits such as Stranger Things, which could reduce churn and help renew subscriber strength.

Netflix Entering the Ad-Supported Market

We had written an editorial a year ago on Forbes called the Crucial Difference between Netflix and Roku Stock. At the time, we pointed out that: “we believe first-party data for connected TV ads is a significant trend moving into 2021 and an important distinction from subscription-video on demand (SVOD) […] Ad-Video on Demand (AVOD) has an approximate ten-year runway as the trend began taking shape when Roku launched its ad platform in late 2018/early 2019. There were AVOD players in the space before this, but the budgets were negligible.”

During the most recent earnings call, Netflix’s management team discussed the company’s plan to introduce ad-supported content:

“And one way to increase the price spread is advertising on low-end plans and to have lower prices with advertising. And those who have followed Netflix know that I've been against the complexity of advertising and a big fan of the simplicity of subscription.

But as much I'm a fan of that, I'm a bigger fan of consumer choice. And allowing consumers who would like to have a lower price and are advertising-tolerant get what they want makes a lot of sense. So that's something we're looking at now. We're trying to figure out over the next year or two. But think of us as quite open to offering even lower prices with advertising as a consumer choice.”

Although Reed Hastings stated “the next year or two,” the New York Times later reported that Netflix told employees an ad-supported tier could rollout by the end of 2022. There were also rumors that Netflix may buy Roku, yet upon hearing the news, we quickly refuted this idea on Twitter:

Netflix’s debt load is one reason why it’s unlikely Netflix will buy Roku as the company has a current valuation of $12 billion. This would nearly double Netflix’s debt or the company could dilute shareholders which would weigh heavily on a stock already down 70% YTD. Plus, Netflix has its hands full as a content creator competing with Hollywood, which was referenced on the call: “We've been doing this for a decade. Well, first of all, that's about 90 years less time than all of our competitors have been at it.”

Here’s How Netflix Stock Could Make a New High

If Netflix pulls off the feat of making a new high, fundamentally it will need to be correlated to the global roll-out of ad-supported content. I anticipate the company will test an ad-supported tier in lower yielding markets before rolling it out in the United States and Canada where the company has an additional 30 million it can monetize. Due to the testing this is required, UCAN region is unlikely to see a roll-out in 2022, rather look for this in H2 2023.

On a technical level, Netflix is the only other FAANG, along with Google, that has not made a lower low. There are always two paths a stock can take: going lower or going higher. The probabilities improve that a certain direction is favored once a stock breaks specific price targets. The below chart is tracking the 5-wave move from the 2012 low.

What we will want to see for Netflix to make a new high is a break above $405. At this point, the odds are in the stock’s favor that the bulls are in control again. Typically, after a stock reaches new highs, it has to be monitored again to make sure the price holds. If this happens, we will revisit our analysis - which is published weekly in our free newsletter.

Because we deal with probabilities in the sentiment-driven tech sector, it’s also important to point out that below $115 is what we call no man’s land, where a bottom may be particularly tough to form. We call it “no man’s land’ when a stock can potentially be in free fall and we avoid even the best fundamental stories in these zones.

The chart above shows rare, bullish divergences in the chart which would point towards $450 being more probable than a break in support at $115. There are only two other times since 2012 that this pattern has manifested, and they both marked a turning point was close.

Netflix is also trading at a 10-year record for a low valuation, which sets up the stock for a sizable rebound. In fact, the company has not traded this cheap in terms of PE Ratio for over 10 years.

When you look at top line growth, the company has not traded this cheap since 2012:

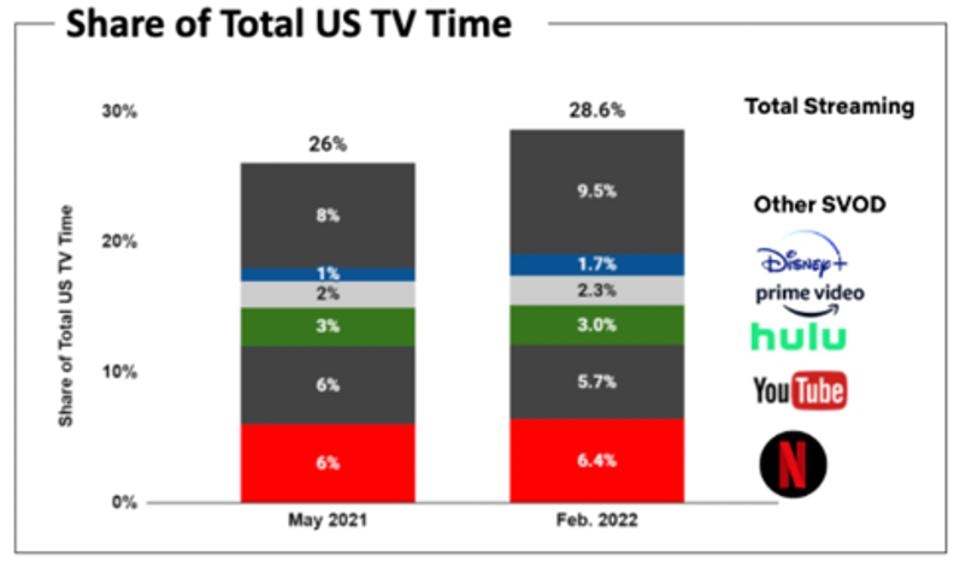

Notably, Netflix must curtail content costs while competing in a market with many big players. However, despite the nominal subscriber miss, Netflix has actually gained market share from 6% to 6.4%.

Conclusion:

Ultimately, the market has read the situation wrong as Netflix is going to monetize nearly 50% more subscribers in the near-term (1-2 years). The ARPU from advertising is unlikely to be as high yielding as the subscription tiers, yet premium CTV content sees $40 in average revenue per user. We think Netflix could set a new record on ad-supported ARPU due to its premium content and captive audience. Despite a clear path to drive record revenue and record active accounts, the stock is trading at its lowest valuation on the top line and bottom line in 10 years.

My firm’s preference is to wait until we are closer to the ad-supported tier rollout before considering a position in Netflix. When we do enter positions, we issue real-time trade alerts to our Members and publish deep dive analysis to accompany the entries we make. Please consult with your financial advisor on any stock trades you make.

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per