FuboTV Delivers Record Numbers; Fantasy and Sports Betting on Deck

August 13, 2021

Beth Kindig

Lead Tech Analyst

According to Fubo’s recent earnings call, a free-to-play app is scheduled to launch in Q3 and a sports betting app is scheduled to launch in Q4. As we stated over the past two quarters, owning a live sports audience will convert for a lower customer acquisition cost and better lifetime value on both free-to-play fantasy and sports betting compared to the competing sports betting companies who must find media partners. Fubo management refers to this as a flywheel, and we agree there is substantial potential for a flywheel effect specifically due to the enthusiasm of sports fans.

Below, we review the company’s record-breaking audience growth, the much-debated gross margins, the likelihood that Fubo will have to raise money (and when this might occur), plus what we hope to see in Q3 from the company.

Perfect 10.000 on Audience Growth

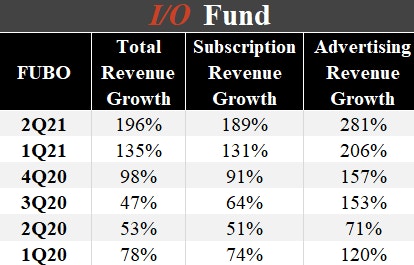

We had made the point that short sellers were exploiting the one-time event of live sports being canceled last year. The results of a live sports comeback are seen clearly in Fubo’s results with 196% growth year-over-year in revenue to $130.9 million, beating analyst estimates by $9.46 million. Subscription revenue grew by 189% YoY to $114.4 million and advertising revenue grew by 281% YoY to $16.5 million.

The most important number was the sequential growth, as Fubo certainly had tailwinds from low Covid comps. In this case, sequential revenue grew QoQ by 9%. This is key because Q2 is a seasonally low quarter for sports. My first guess was that this was due to the NBA playoffs. However, according to management’s earnings call, it was due to “engagement reach[ing] record highs as we added exclusive sports streaming rights with CONMEBOL and began beta testing predictive, free-to-play gaming integrated into our streaming platform ahead of our expected launch this fall.”

Going into Q3, we had published Apptopia data showing that the company was already illustrating strong downloads and DAU growth, likely from the Olympics. The return of sports events is a major boost for the company’s year-over-year top line growth, yet the sequential strength is where Fubo provides a glimpse of a more sustainable trajectory. The management now expects the fiscal year 2021 revenue from $560 to $570 million, which represents an increase of 116% at the mid-point. Previously, it had estimated revenue to be $520 to $530 million.

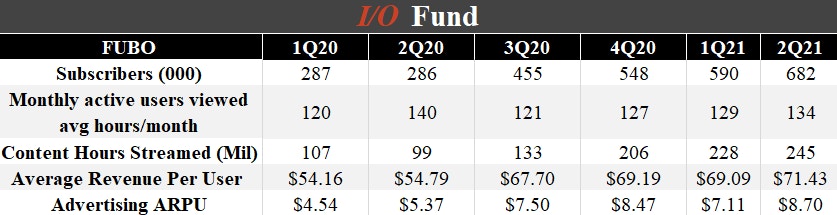

The monthly average revenue per user (ARPU) increased by 30% to $71.43; this was one of the key drivers for the increase in margins. The adjusted contribution margin came in at 8.3%, up from -4.4% in the same period last year. This is a step in the right direction, although there’s more work to be done on profitability before we see institutional interest pick up.

Fubo is in a high-growth phase. It’s not uncommon for a rapidly growing company to show losses; however, we want to see a deceleration of these losses as the company scales. Fubo’s gross losses shrunk from $4 million in Q1 to $2 million in the recent quarter. Considering that their gross losses were $18 million in the year-ago quarter.

It’s also important to point out that Fubo’s cash balance of $400 million supports about 9 quarters of operations ($406 million in cash / $47 million in Q2 adjusted EBITDA). Therefore, it’s reasonable to expect the company may raise money in the near term, which can dilute shareholders. As an investor, I am not too concerned about this (Tesla did it many times), although my preference would be that Fubo raises cash in Q1 or Q2 after the launch of its betting app so the market can understand and assess the company’s full potential.

Source: Fubo Investor Relations

As seen above, the advertising revenue growth was the best ad revenue quarter in the company’s history. Advertising ARPU grew by 62% YoY to $8.70, up 22% on a QoQ basis. The company has a goal to double the advertising revenue this year.

My main contention is that as long the company can grow its audience, the market will reward it in the long-term. Our previous analysis was focused on the microtrend of live sports OTT and we think these users are stickier than Wall Street realizes.

Source: Fubo Investor Relations

The company has successfully been able to increase its paid subscribers. The customers continued to prefer fuboTV over legacy pay TV services due to the unique customer experience, innovative product experience, and bundled wide premium content. The company added 91,291 net subscribers in the recent quarter bringing the total to 681,721. This beat the analysts’ estimate of 602,000 and the management guidance of 600,000 to 605,000.

The company also increased the full-year subscriber guidance to a range of 910,000 to 920,000, from previous guidance of 830,000 to 850,000.

It’s crucial to not only grow the audience but also retain them. The company has been able to improve the churn rate by 203 basis points year-over-year. The company’s investment in subscriber intelligence and insights helps to lower the churn rate. Management points towards its first-party data for reaching household income above $85,000 and mainly males. This can help the company reach its target of $35 CPMs with current CPMs in the low $20s.

Fubo users streamed over 245 million hours which is an increase of 148%. The company’s monthly active users (MAUs) watched 134 hours per month on average, demonstrating strong customer engagement – we hope this engagement translates well for the free-to-play and sports betting app.

Improving Bottom Line Already with Sports Betting on the Way

The company’s margins are improving with increasing revenue and the management expects this trend to continue. Operating expenses as a percentage of total revenue were 155% compared to 252% in the Q2 2020. Subscriber-related expenses, primarily include content cost, accounted for 92% of total revenue compared to 120% in 2Q 2020. Sales and marketing expenses were 16% compared to 18% in Q1 2021.

We think the market has over-penalized the company for its gross margins with evidence that DraftKings’ sales and marketing costs exceed Fubo’s subscriber costs & broadcasting and transmission fees (when we compare operating margins). Meanwhile, DraftKings trades at a 300% higher valuation. Therefore, if Fubo can illustrate its sports betting capabilities, it should fetch a higher valuation.

Net loss per share was ($0.68) compared to ($2.08) in 2Q 2020. Adjusted net loss was ($51.3) million compared to ($51.5) million in the 2Q 2020. The adjusted EBITDA improved from (95%) to minus (36%) in Q2 2021.

The launch of the company’s Sportsbook is an important driver of the overall strategy as it aims to develop a flywheel that turns passive viewers into active participants. The monetization here can be substantial if Fubo sees cohorts spending more than $100 on their platform. As stated, the income of over $85,000 and persona of their viewing audience lends itself perfectly to sports betting, which is men watching sports. You really can’t get a better audience than that to target a sports betting app.

Fubo Sportsbook will represent an industry-first live sync integration between video and the Sportsbook. Recently, the company has released a short video presentation that is worth watching. The short sellers accused Fubo of buying a headline with Balto Sports, which was surprising to me to find out these analysts don’t know that YCombinator often incubates small teams. This is common knowledge in tech.

The unique feature is that FuboTV’s sports betting app will allow its users to watch and bet from the same platform. Fubo announced last month that it had completed a market access agreement in Pennsylvania with The Cordish Companies. Currently, the company has market access deals in 4 states, namely, Pennsylvania, Iowa, New Jersey, and Indiana.

FUBO commands about 6% of the virtual MVPD space. So, it’s very likely that over the long-term, the company is aiming between 3% and 6% of the total betting TAM. Right now, sports betting is expected to be a $218 billion market globally.

In the words David Gandler, “The secular decline of traditional television; the shift of TV ad dollars to connected devices; and online sports wagering, a market opportunity which we believe complements our sports-first live TV streaming platform.”

Analyst views

Evercore ISI analyst Shweta Khajuria responded to the results by repeating her Outperform rating and lifting her target price to $40 from $33.90. “We continue to view Fubo as a key beneficiary to three industry trends,” she writes in a research report. “Cord cutting, as viewers shift away from linear TV to streaming; mix-shift of advertising dollars from linear TV to [streaming]; and growing demand for online sports betting.”

Likewise, Oppenheimer analyst Jed Kelly reiterated his Outperform rating, while lifting his price target to $42 from $32. Kelly cited stronger-than-expected subscriber growth, driven by a “strong sports calendar,” and improved churn. “Most OTT providers have focused on low-cost entertainment offerings, forcing sports fans to remain tethered to pay TV,” he writes. “FuboTV is exploiting the opportunity in sports by providing a comparable viewership experience at a lower cost than its pay TV counterparts.”

What’s next for Q3

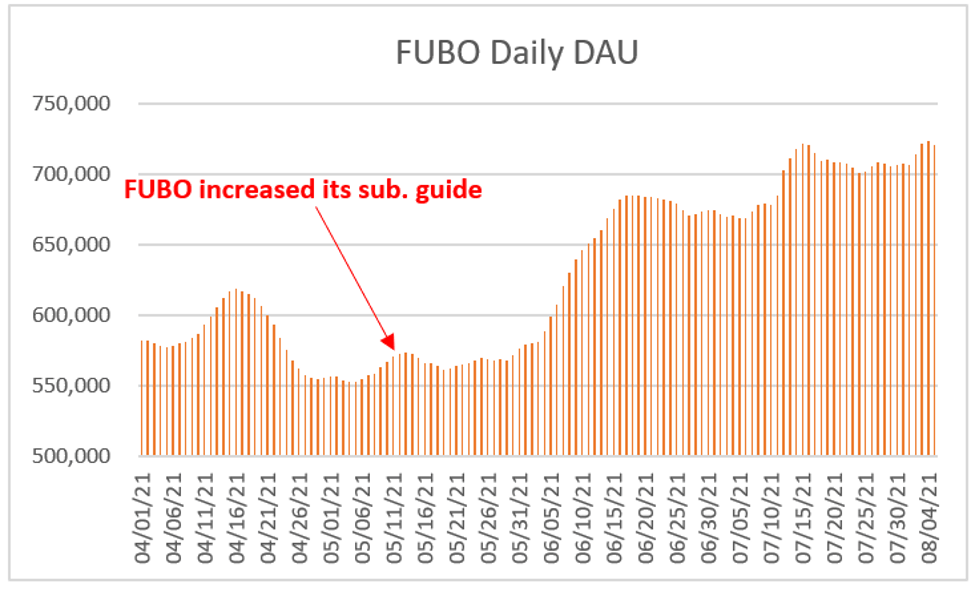

We have already published Apptopia data that shows July was strong in terms of audience growth. You can view the full article on Forbes here.

Source: Apptopia

Also, the company’s exclusive rights to South American World Cup Qualifiers is a game-changer as it helps to solidify the company’s brand ahead of next year’s FIFA World Cup. The company was also able to increase the number of consumers in the recent quarter through the launch of LG Smart TVs. It has also partnered with Vizio to launch on their popular SmartCast platform.

Additionally, with the NFL football season, we would expect the growth in the DAUs to continue in the second half of the year. If the company can launch the free-to-play soon, then we may see the flywheel effects of this as soon as Q3.

I/O Fund has partnered three times now with Apptopia to deliver pre-earnings numbers – twice for our free newsletter subscribers and once for premium. Stay tuned for our next pre-earnings coverage next quarter.

As stated in the article, Beth Kindig and I/O Fund currently own shares of FUBO. This is not financial advice. Please consult with your financial advisor in regards to any stocks you buy.

Royston Roche contributed to this article.

More To Explore

Newsletter

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i

Google TPU v8 vs Nvidia: How Inference Is Rewriting the AI Market

In April, Google announced it would begin selling its TPUs to select third-party data center operators, which is something the market has anticipated for nearly a decade. The TPU-versus-Nvidia-GPU deb