FuboTV: Solid Positioning For Sports Betting

January 05, 2021

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Dec 31, 2020,11:45pm EST

Recently, FuboTV has been hit hard by short sellers. The criticism is based on FuboTV’s trailing financials and negative gross margins. We recommended FuboTV at $16 and have a blended cost basis of $20.10 and want to take this opportunity to connect a few dots on this company for anyone interested in hearing why we remain long.

Our analysis starts with audience growth because this is the predominant key metric in media. We also discuss the financials including the forward guidance. Lastly, we discuss why live sports OTT is a unique opportunity and why we think FuboTV is positioned well for free-to-play fantasy games and sports betting.

The main argument against FuboTV is the negative margins. This is a lagging argument as the company has laid out a path to increase monetization through sports betting. We are in a speculative period for this, however, we spell out a few key reasons we think the company can execute on this new path for monetization.

Key Metrics and Financials:

Fubo TV announced Q3 results on November 10th, the company’s first earnings report since its October IPO. Management described the quarter as the “strongest in company history.”

Revenues of $61.2 million increased 47% YoY on a pro forma basis, or +71% excluding 2019 licensing revenue from the FaceBank AG business, which was sold in July 2020.

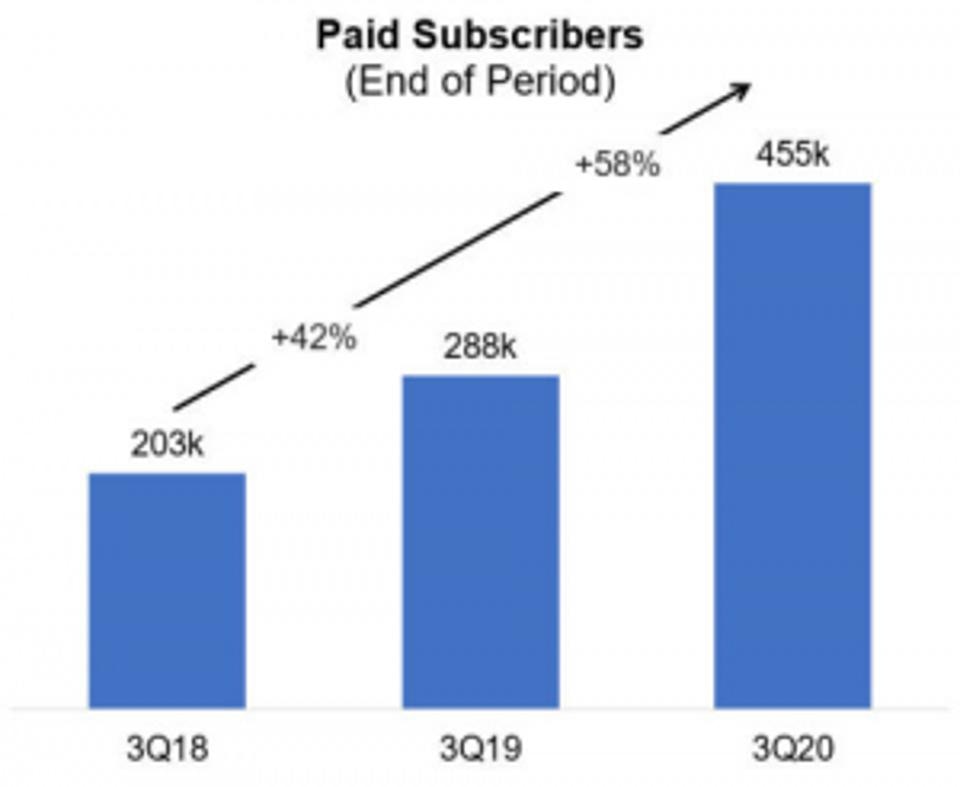

Subscription revenue increased 64% YoY to $53.4 million, while advertising revenue increased 153% YoY to $7.5 million. Paid subscribers grew 58% YoY and totaled 455K at the end of the quarter, an acceleration from the 42% subscriber growth the company posted last quarter.

Fubo Press Release

Average Revenue per User (ARPU) increased 14% YoY to $67.70, while total content hours streamed by FuboTV users (paid and free trial) in the quarter increased 83% YoY to 133.3 million hours. Monthly active users (MAUs) watched 121 hours per month on average in the quarter, an increase of 20% YoY.

Operating margins were -145.9% and gross margins currently stand at -16%. This would be a concern if FuboTV had not outlined a new path for monetization (see below). Related expenses and sales & marketing expenses increased by 20% and 60% respectively in Fubo’s latest quarter.

Management noted that they use adjusted contribution margin to measure variable costs against subscriber revenue. In Q3, adjusted contribution margin was positive 16.1%, up from 0.5% in Q3 2019.

The company is expecting margin improvement over time, as discussed in its Q3 Shareholder Letter:

“We expect margin improvement to continue over time, aided by a number of initiatives. This includes the growth of advertising on our platform along with strong attachment rates on value-added services, such as cloud DVR storage and the ability to stream on multiple devices.”

The company also raised Q4 and FY guidance significantly. Management now expects Q4 revenues to be $80-85 million, a 51% to 60% increase YoY. They also expect to end Q4 with 500,000-510,000 paid subscribers, an increase of 58% to 62% YoY.

As a result, FY 2020 revenue is expected to increase 65% YoY to $246M. Most impressively, management is guiding for an acceleration of revenue growth in 2021 to 70% YoY, with total revenue reaching $415-435 million.

Sign up for I/O Fund's free newsletter with gains of up to 403% -Click here

FuboTV App Downloads and Sessions:

The short seller report from Kerrisdale Capital did not name the source of the app intelligence it was quoting. There is no reason to not name the source as app download and session data is factual and inherently unbiased. This is the first I’ve seen data referenced in any article or report without the source being named.

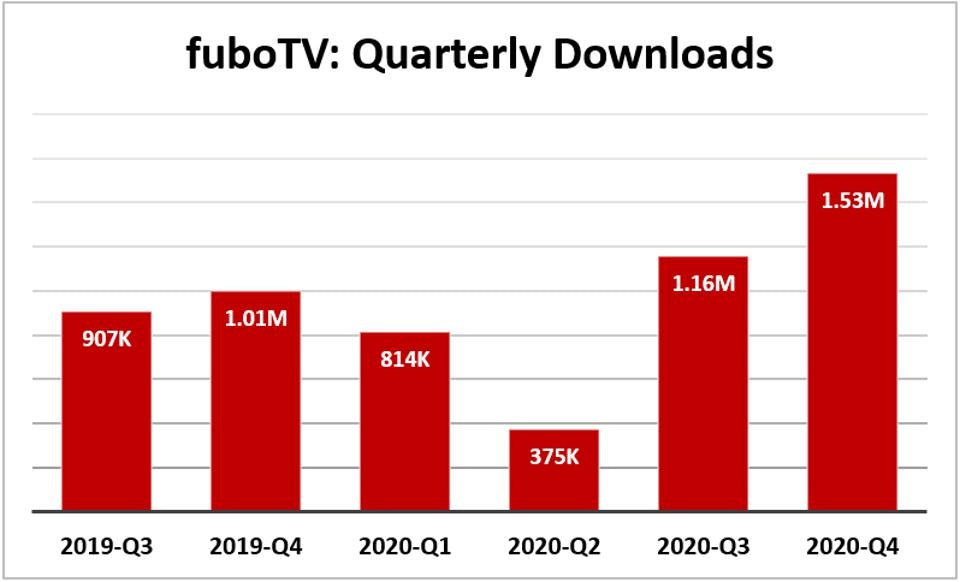

There are three main providers for app intelligence: Apptopia, AppAnnie and SensorTower. Apptopia has provided the following data showing that downloads are up for the quarter from 1.16M in Q3 2020 to 1.53M in Q4 2020.

Apptopia

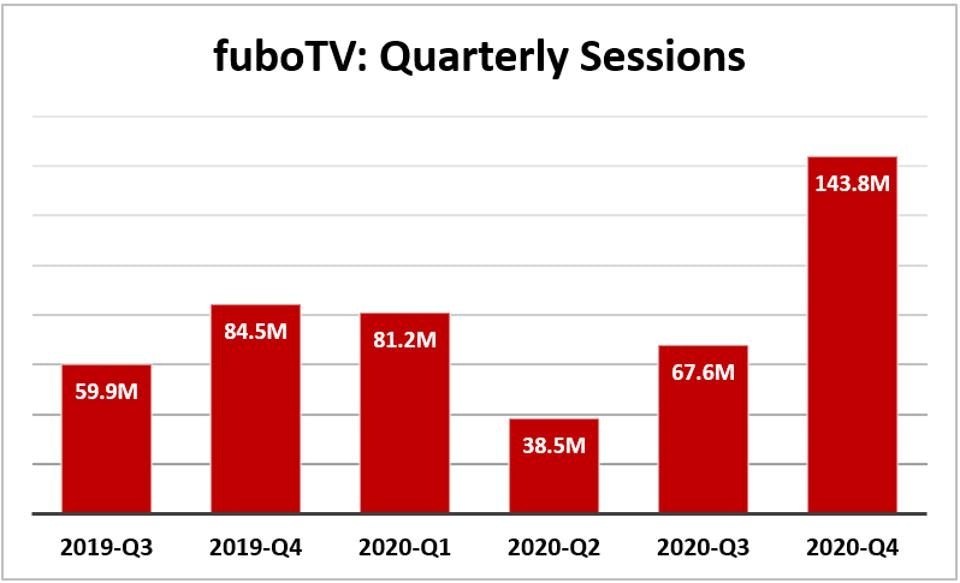

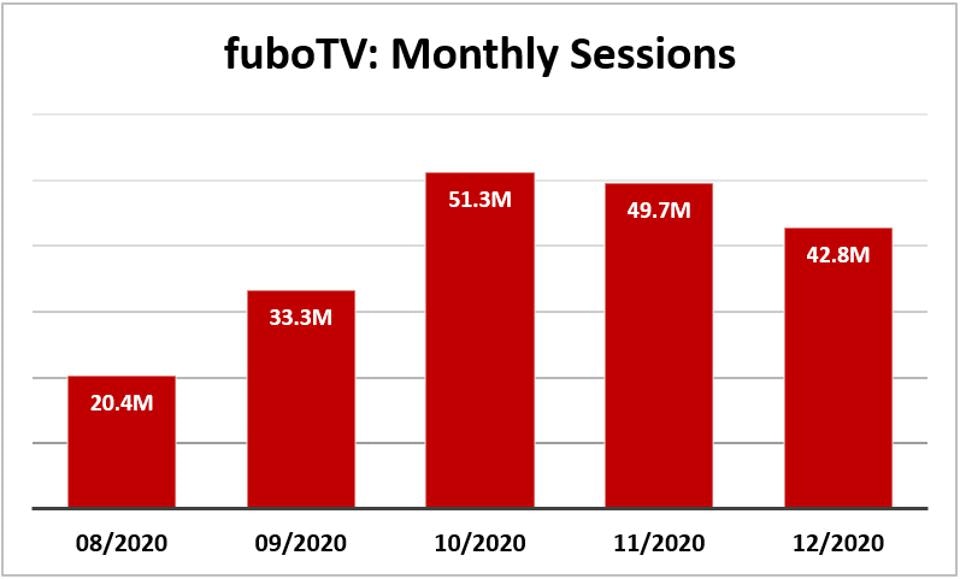

According to Apptopia, FuboTV is up about 50% year-over-year on downloads from 1.001 million in Q4 2019 to 1.53 million in Q4 2020 and up about 70% in sessions from 84 million in Q4 2019 to 143.7 million in Q4 2020.

Apptopia

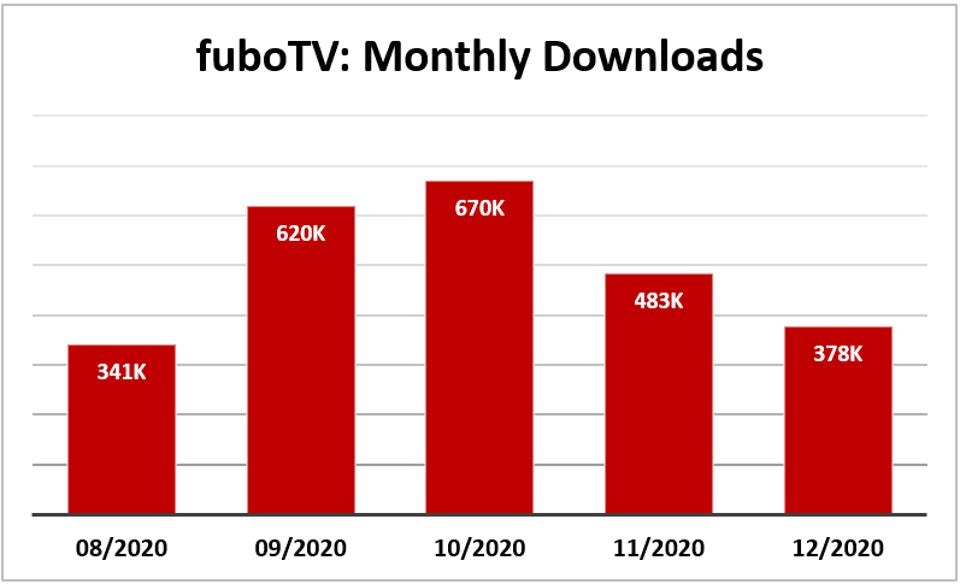

There is a dip in December when broken down monthly on downloads but sessions remain strong. This does not include a full month as the data was pulled through December 29th.

Apptopia

Despite downloads being lower on a monthly basis, we see sessions are higher in December than September. Downloads could also be affected by new subscribers joining for football at the start of the season, therefore, these fans already having the app downloaded. For this reason, sessions are important to cross-reference.

Apptopia

We think the dip in December downloads should recover with the start of the basketball and hockey season to create a new seasonal spike in downloads. The NFL Network is a competitor and has exclusive content while basketball does not.

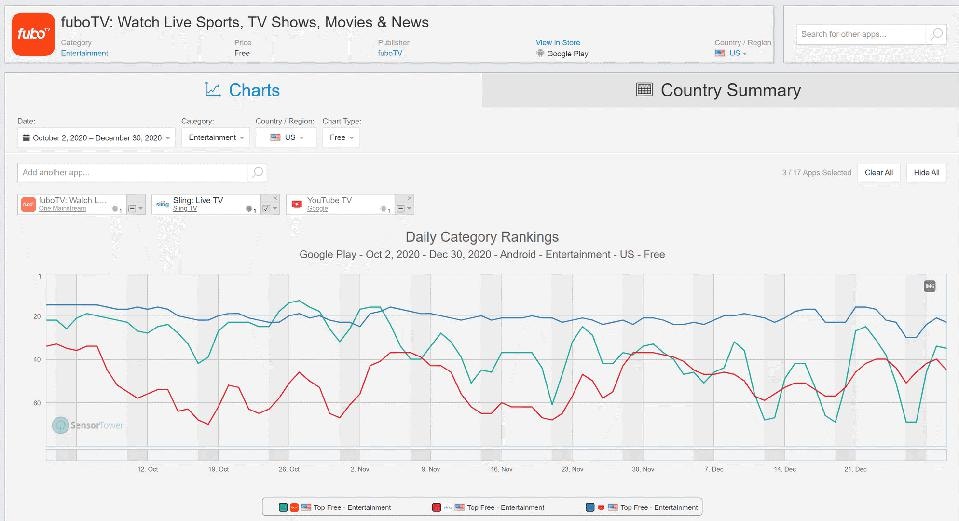

SensorTower data does not raise any flags either although it appears the viewership is lumpy with more popularity on the weekends. In this picture, Fubo is green, Youtube is blue and Sling is red.

SENSORTOWER

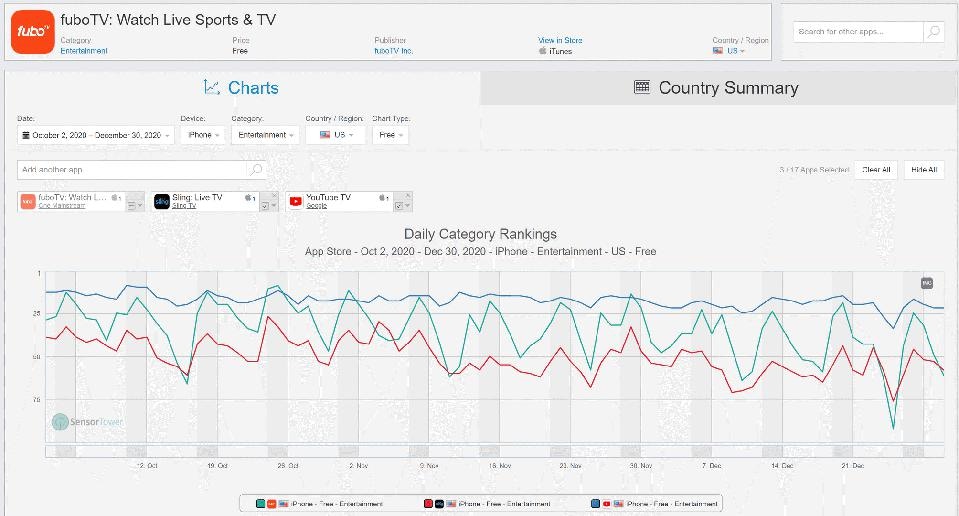

FuboTV looks similar on the iPhone where weekends are more popular.

SENSORTOWER

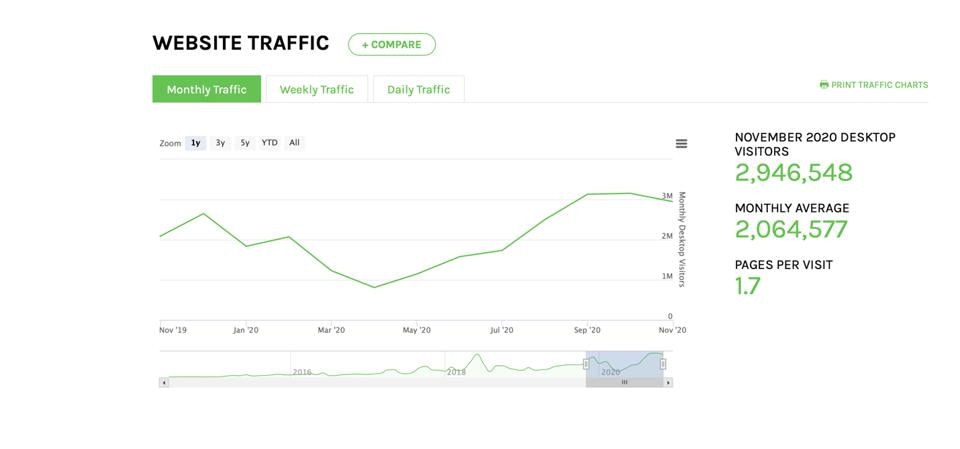

Here’s more information regarding how FuboTV’s website traffic has recovered nicely since April when there were no live sports. We see no issues here. Notably, this does not include December.

WEBSITE IQ

Apptopia is available through the Bloomberg Terminal and along with SensorTower was used to predict the spike in Pinterest from iOS 14, Disney Plus downloads when it first launched and the recent information on HBO Max being the fastest growing SVOD service.

Sign up for I/O Fund's free newsletter with gains of up to 403% -Click here

Live Sports:

Live sports is known as the “holy grail” because it’s the last stand for cable television. Loyalty to live sports is the primary reason as to why customers have not cut the cord with 81% of sports fans subscribing to pay-TV and 91% stating they subscribe to pay-TV for access to games. According to Pricewaterhouse Coopers, 82% of live sports fans have stated they would cut their subscription if they could access live sports elsewhere.

This is substantiated by the fact FuboTV – a relatively unknown name —- can command a high fee for its content of $65. This is three times more than Netflix. We are less concerned with the margins at this time and more interested with how Fubo has been able to compete with the largest MVPDs on price – Comcast, Charter, Hulu+ and YouTube — and most importantly, what the willingness to pay a high subscription fee could mean for free-to-play fantasy games and sports betting in the future.

Sports Betting:

FuboTV has stated they will first go into fantasy league free-to-play games and then move into sports betting. FaceBank is a company that is known for its animated digital humans, such as Tupac Shakur during Coachella. However, more importantly, the merger gives FuboTV access to the Facebank Group’s Nexway e-commerce and payment platform with a presence in 180 countries.

We think this payment platform will be useful for global sports wagering and will help FuboTV scale for sports wagering quickly.

Per the April 2020 press release:

fuboTV intends to continue its global expansion with FaceBank’s Nexway AG, a global ecommerce and payment platform with a business presence in 180 countries, accepting payments in roughly 140 currencies.

Please note: This article is updated to reflect that Nexway was sold and is no longer part of the merger with FuboTV, per a disclosure on November 16th. The tool that FuboTV will use to expand into fantasy games is Balto Sports, acquired in early December by FuboTV. Balto Sports is a graduate of Y Combinator, the incubator that has worked with many startups including Stripe and AirBnB in their early days. Balto Sports is co-founded by Joe Montana’s son and has the ability to become a sports book.

Over the past few years, Sky Media led investment rounds in FuboTV along with Fox for a 39% stake. This investment round was increased in late 2017/early 2018 with Sky Media holding Board positions. The former NBA commissioner was also part of the last $15 million round. Media has gone through some very big M&A shifts at the top-level with Comcast acquiring Sky and Disney acquiring 21st Century Fox. However, for FuboTV’s formative years, the company was influenced by arguably the top sports betting company in the world – Sky Media from the UK. The Comcast-owned Sky Media is still a backer for FuboTV along with Disney.

We think FuboTV is an excellent route for these more traditional media companies to have exposure for free-to-play games and sports wagering without involving their mainstream entities, like Hulu. Sports betting can be controversial and FuboTV allows the content to be funneled to another MVPD. We see the same thing happening with DraftKings – where Fox was a backer, and now through acquisition, Disney.

There are debates on who will dominate the free-to-play fantasy and wagering market in the United States but the successful model to replicate is nearly unanimous – which is Sky Media’s model. The company has numerous brands for betting and fantasy football (soccer) and is the largest betting organization in the UK by number of subscribers. Perhaps it is simply a coincidence that Sky Media has been the largest stakeholder in FuboTV along with Fox over the past few years — and now FuboTV is pursuing a similar monetization path as Sky Media – but we don’t think this is a coincidence. We like this synergy and the direct access Fubo has had to Sky in its formative years.

Analysts:

Perhaps the most compelling thing about the market’s reaction is how quickly short sellers with less of a track record were listened to over sell-side analysts who must maintain a high level of credibility. (In one case, the short seller has a #17,000 rank on TipRanks!)

If the company is going bankrupt soon, then the following analysts have produced the first goose egg in their careers.

BMO Capital (12/23):

BMO Capital Markets analyst Daniel Salmon downgrades from Outperform to Market Perform. The big move had taken the stock well north of his $33 price target, which is now lifted to $50. Salmon says FUBO offers "a more promising path to profitability than most new investors expect," but secular and execution tailwinds are already included at this valuation. His raised price target remains lower than last night's close, with Salmon saying the downside "is more a reflection of recent volatility than an incrementally negative view.

Wedbush (12/16):

Wedbush analyst Michael Pachter initiated coverage of FuboTV with an Outperform rating and $40 price target. The rating is initiated as the analyst expects cord-cutting and cord-shaving to continue for the foreseeable future, and thinks that a sizeable portion of the population will grow up as 'cord-nevers', preferring customized content.

Needham (12/22):

Needham boosts its rating on FUBO to Buy from Hold off the 2021 upside drivers it sees for the company. "We believe FUBO will continue to have strong upside momentum into 2021 owing to: a) FUBO is taking share from competitors; b) its Hisense partnership lowers SAC; c) upside from sports betting; d) OTT multiple expansion; e) short covering; and, f) CTV upside," sums up analyst Laura Marting on the bull case. Despite the huge runup in share price since fuboTV's debut in October, valuation is called inexpensive in comparison to OTT comparables.

Roth Capital (12/22):

FuboTV price target raised to $55 from $36.50 at Roth Capital. Analyst Darren Aftahi raised the firm's price target on FuboTV to $55 from $36.50 and keeps a Buy rating on the shares. Recent market research from Antenna suggests FuboTV gained share from larger virtual multichannel video programming distributors Hulu and YouTube TV in the months of October and November, growing 100 and 200 basis points, respectively, from September to 19% in November, Aftahi tells investors in a research note. While part of this gain can be attributed to seasonality around the launch of the football season in the United States, the overall market trend of cord-cutting, along with FuboTV's growth initiatives, should lead to a higher subscriber outlook for the first half of 2021, says the analyst. Aftahi says share gains, categorical growth, further implementation of artificial intelligence to aid acquisition and retention, and the rollout of an initial entree into sports betting expected in fiscal 2021 substantiate his "bullish thesis" on FuboTV.

Oppenheimer (12/7):

FuboTV price target raised to $30 from $21 at Oppenheimer. Oppenheimer analyst Jason Helfstein raised the firm's price target on FuboTV to $30 from $21 and keeps an Outperform rating on the shares after hosting meetings with the company's CEO and CFO. While management sounded confident in its ability to meet near-term targets for core subscription/advertising, the majority of investor focus was on the recent acquisition of Balto Sports, marking FuboTV's first move toward online sports betting, the analyst notes. While there are clear synergies between live sports content and OSB, Helfstein acknowledges that there are significant hurdles to enter this market. However, he is taking a first "stab" at sizing the OSB opportunity at $742M, assuming $295M in 2020 revenue based on a 16% attach rate and comparable margin structure to OSB leaders.

Is FuboTV the next Roku?

I was the first analyst to cover Roku at $30 and to discuss its story at length. While the market argued it was hardware; I detailed how it was an ad exchange and why that was important. This was before Roku reported any ad revenue in its fundamentals. Now, as you know, Roku has more ad revenue than hardware revenue and the market now “likes” Roku for Connected TV ads.

Source: Knox Ridley on Twitter

One argument I’ve continually made is that SVOD (subscription video on demand) is a mature market while AVOD (ad video on demand) is many years behind because Pay-TV advertisers had not migrated. This is why Roku was a developing story while Netflix is a mature story. The market has had a very challenging time understanding where Roku is in the hype cycle.

Of course, FuboTV is not like Roku because it is not an operating system or ad exchange. However, it’s important to know that FuboTV is in the most nascent area of OTT and the peak growth will be years behind Roku due to live sports being the last content type to convert to linear OTT.

Therefore, to require a perfect story and fundamentals right now in linear OTT for live sports is incredibly myopic. Investors will need to come back in two years to find a better fundamental story in linear OTT live sports — and they must be willing to have fewer gains for a surer thing. What short sellers are calling a dumpster fire is actually a market in its infancy. We are not dealing with just a general linear OTT channel. The product is live sports and this was the last to convert for cord cutters.

What Roku and FuboTV do have in common is solid subscriber growth and high ARPU. They’re also both continually under pressure from the market due to margins. Netflix, for that matter, has also been continually attacked for its free cash flow margin. We understand that licensing and distributing sports content has created an issue with margins but we also know that small companies with loyal audience can (and do) successfully pivot frequently.

Although we agree with the short sellers that the gross margins need improvement, that is the only thing we agree with them on. The rest of the reports were opinions that offered no citations on the data. The quotes and sources “from experts” were also unnamed. Finance is a regulated industry and we feel any data or interviews that cause people to lose money should be sourced.

Notably, the shorts had great timing. There was a run-up in price and an over-extension on the technicals and the reports came out during a period of low volume over the holidays (one report came out on Christmas Eve). The reports were also timed to the lock-up expiring. As far as timing goes, it was a perfect storm.

Regarding valuation, there are concerns about the number of shares that have become available which stands between 140 million, according to Oppenheimer. Keep in mind, DraftKings has a similar subscriber number in the 500,000 range and FuboTV makes similar revenue as DraftKings did in 2019 — yet DraftKings trades at a high valuation of 36 with a $18 billion valuation. If Fubo cracks sports betting on the same size audience (that is growing at and proven to already spend a sizable $65 for month for their content) then we think it could end up there.

Conclusion:

We believe the company will be successful in its pivot to a new monetization method as pivoting is something that nearly every small company does as they look for product-market fit. What matters for a pivot is the audience. This is the core strength to any media company and FuboTV’s key metrics are strong. If the audience continues to grow, then FuboTV has a high likelihood of delivering its new path of monetization which is free-to-play fantasy to maintain growth and reduce churn, and later, sports betting to increase revenue and improve margins. As stated above, sell-side analysts believe sports wagering could come as soon as fiscal 2021.

To conclude, we are long FuboTV and our thesis is not changed at this time.

More To Explore

Newsletter

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i

Google TPU v8 vs Nvidia: How Inference Is Rewriting the AI Market

In April, Google announced it would begin selling its TPUs to select third-party data center operators, which is something the market has anticipated for nearly a decade. The TPU-versus-Nvidia-GPU deb