Roku Q3 Earnings: Choppy But Unshakeable Long-Term

November 08, 2019

Beth Kindig

Lead Tech Analyst

Roku is a company that has proven nearly every bearish prediction wrong with consistent revenue growth despite being surrounded by steep competition and tech heavyweights in over-the-top media.

Roku investors that have been long since its IPO have lived through three fifty-percent drawdowns. Therefore, the reaction to earnings this quarter was unlikely to phase anyone who has followed this stock for any length of time.

I encouraged my readers to not be phased by market reactions when Roku was priced at $30, when it was priced at $60, and when it was priced again at $30. During that sell-off, I said the company would become a tech darling and reach $100 in stock price in two years, which was bold to predict 200% returns. Of course, the company went on to reach 350% returns in a short time span of about one year.

Also Read : Update on $ROKU – Will Roku Miss Earnings?

A version of this article appeared in MarketWatch on November 6th.

Roku Earnings Report Review

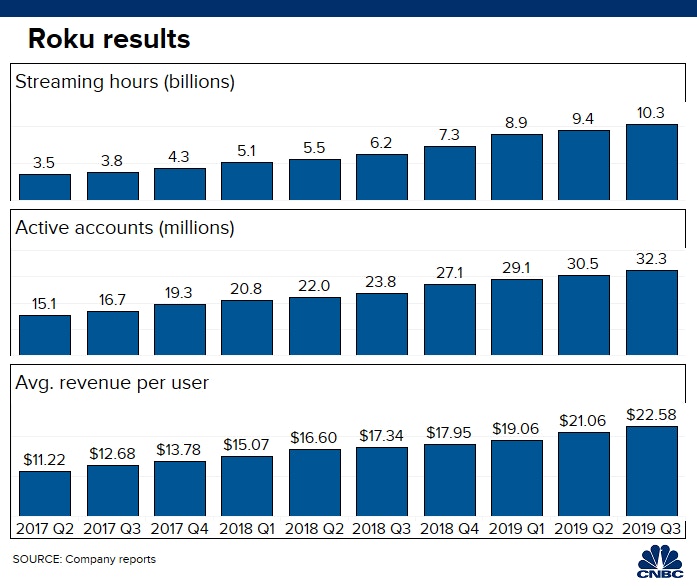

The market received Roku earnings report on Wednesday after the market closed. Streaming hours passed 10 billion hours in the third quarter, while active accounts increased to more than 32.3 million. The most impressive number in the Roku quarterly earnings was the average revenue per user, which increased to $22.58. This number has more than doubled since the second quarter of 2017.

The Roku earnings report showed that quarterly revenue increased to more than $261 million. Platform revenue grew by 79% while ad revenue more than doubled. This was a 50% YoY growth and was above the consensus estimates of $256.9 million. The company lost 22 cents a share, which was 6 cents above the consensus estimates of 28 cents a share.

Overall, the company beat the consensus estimates, raised guidance, reported strong user growth, and increased ARPU.

However, Roku has double-digit negative EPS and will for some time. Roku financial statements show that EPS is declining QoQ. Its consensus EPS forecast of -$0.28 compared to -$0.09 in the year ago quarter. Annual EPS won’t improve either, per analyst consensus, with -$0.50 ending in fiscal year December 2019 and -$0.43 ending in fiscal December 2020.

Also Read : Here’s Why Roku Will Be The Next Tech Darling

Source: CNBC

We’ve already seen a few companies get crushed by the market if they have a small miss, which is the paradox for growing tech companies who are often penalized by the market by foregoing earnings to capture peak growth, which in turn, becomes rewarded by the market once it materializes into earnings. In other words, if Roku misses anytime in the next couple of years, it’ll be with EPS rather than revenue. The market, which is confused by the many OTT streaming services and hardware players, will penalize Roku. This most certainly will not be the last time the stock sees double-digit pullbacks.

I also foresee the market abandoning Roku and many other solid tech stocks that aren’t profitable yet during the inevitable value rotations. Keep in mind, investors also did this with Netflix, Google, Apple, Microsoft and Amazon during 2009.

Misunderstood Competition is an Edge

As is always the case, the market has a record of underestimating small companies that are battling with other big companies like Apple, Disney, Google, and Comcast. This is why Roku still remains one of the most volatile stocks in the market. This also proves the affinity investors have towards brands rather than technology. Yet, it is the latter that drives growth in new markets.

The nuances in strategy and technology are terribly important to understand in the crowded OTT space as it helps to have conviction when a stock drops 50% or more, yet then goes on to be the best performing stock of the 712 stocks with a market capitalization over $10 billion in 2019.

Let’s break down what I mean by Roku having very little direct competition.

SVOD vs. Connected TV Ads

Roku does not compete with Disney+, Netflix, or HBO Go because these are subscription services. Subscription video on demand (SVOD) is in a category of its own as the opportunity Roku is capitalizing on is Connected TV ads (CTV Ads). Advertisers are paying a premium for CTV ads, which is Roku’s market. The distinction between markets is important, and one that Wall Street missed when discounting Roku as a long-term opportunity by labeling it a hardware company for its first couple of years on the market.

Roku directly competes with Amazon and Hulu, as they compete for Connected TV ad dollars. However, as the market is well aware, data is king as it allows for better targeting. Hulu has to barter data as it’s a single application without a platform or hardware (i.e., it shares and connects third-party data, including with Facebook). Third-party data is always weaker targeting than first-party data and could be subject to privacy issues.

Razor-Razor Blade Model

Discounting the hardware and taking a loss is an excellent strategy to maintain a moat on data for advertising. Both Amazon and Roku own the hardware, and at current prices, the hardware likely causes negative or very thin margins. This is similar to the razor-razor blade model, where you discount the razor to sell the razor blades for life.

This positions Amazon and Roku for first-party data across OTT applications. Anything data related is subject to privacy issues and anti-trust issues. This is at the core of the controversy with Facebook and Google.

Roku is again set apart here, as the company only does OTT. The company does not share the data beyond the OTT player it owns. Amazon, however, is collecting data in a way that could come under anti-trust scrutiny as they take e-commerce data and broker this on the OTT player, which is anti-competitive with other ad exchanges.

Amazon is well aware of this, and is being proactive rather than reactive by opening up its demand-side platform to other DSPs, such as The Trade Desk, which was announced in July of this year. On a side note, Facebook learn from Amazon’s playbook as reputational damage is hard to shake.

Roku, however, does not need to worry about this as data never leaves the OTT hardware that they own, where they have a first-party relationship.

Valuation:

Connected TV ads are ballooning because they combine audience data with the viewability and completion rates of linear television. Roku’s valuation at 14 price-to-sales seems high at first, yet the one-year forward price-to-sales is trading at 9.3 due to the forward growth opportunity in Connected TV ads. Roku earnings estimates for 2020 and 2021 are $-0.29 and $0.6178 respectively. Therefore, the market may still be lukewarm with knee jerk reactions throughout 2020.

For example, last November, video-first SSP Beachfront reported that ad requests for CTV had increased 1,640% from November of 2017. While this is only one company’s growth in a single segment, the opportunity is so ripe, it’s hard to quantify. More astonishing is that Connected TV ads surpassed mobile last year for capturing the largest number of impressions and video completion rates.

Roku’s revenue growth will be exciting; however, the company is not likely to be profitable until 2021. In the third quarter Roku income statement report showed that revenue grew by almost 60%. This was almost double that of Netflix and triple that of Google.

Traditional metrics show that Roku is not a cheap company to own. Its forward EV to EBITDA ratio of 393, which reflects the lack of profitability. It’s not surprising the stock is trading in the range of $127-$131 following earnings, which was former support.

Depending on macro trends, we could see Roku trade around $100 again as this is an important psychological level, as shown below. It is also along the 50% Fibonacci Retracement level and along the 200-day exponential moving average. Long-term, I see Roku as one of the most promising tech stocks on the market and have provided projections to my premium subscribers.

Also Read : Roku’s Stock Price

Knox Ridley, technical analyst, will be covering Roku in-depth with technicals next week. He has guided many successful entries on this stock for our premium members, including entries lower than $100.

A version of this analysis appeared in MarketWatch prior to earnings on November 6th, 2019. It has been updated and lengthened post-earnings.

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i