FuboTV: Why I Like This Stock Better Than DraftKings

May 25, 2021

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on May 21, 2021,12:31am EDT

FuboTV has been dismissed by quite a few analysts and investors for its negative gross margins. This dismissal, that leans heavily on the lagging financials, is reminiscent of the many times that tech stocks have been misunderstood.

As a tech analyst who is trained in product, I see a sizable runway in live sports OTT and sports betting with Fubo having key advantages over DraftKings. The management has to execute, and while the market calls this speculation, I call it a product road map.

First, FuboTV must continue to grow its audience. I made the argument that this is the most essential piece over the coming quarters when the shorts attacked this company. The bearish reports ignored the most important piece to a media company: audience growth. Fubo has handily overcome the challenge of growing its audience year-over-year regardless of the seasonality in sports. The last two quarters could not have gone better in this regard.

Second, FuboTV must execute on launching a sports betting book. This is easier than the public markets think as Fubo has every required ingredient. Most importantly, competitors such as DraftKings do not have all of the essential ingredients that FuboTV has, and we expect Fubo will see a healthy uptake for this product launch.

You can read my previous write-up on FuboTV here.

Financials do matter, of course, and as mentioned Fubo is the ultimate challenge for those who rely on financials alone and ignore product. This is because live sports were canceled last year. Short seller reports that dissect a live sports company following covid are exaggerating the effects of a lagging, one-time event. Forward-looking, we have an ad rebound in digital ad spend from 5% last year to 17% this year. Plus, the World Cup is on deck (and hopefully the Olympics) which bodes well for point #1 – audience growth.

The more popular bet is to go with DraftKings. However, DraftKings is a well-known story that is fully priced. We like the risk/reward of Fubo better due to the fact that this particular company is capturing the live sports OTT trend and will be able to convert high-value users for the sports playbook because they own their audience.

Audience Growth

FuboTV put quite a few triple digits on the scoreboard in the last earnings report, which was the strongest first quarter in company history. Due to the seasonality of sports, Q1 is typically lighter in terms of growth for Fubo, yet the company reported sequential revenue and subscriber growth.

GAAP of -$0.59 missed by $0.03 and included -$0.02 from expenses associated with the launch of sports betting and -$0.02 due to paying off debt related to senior convertible notes.

Prior to the earnings report, we reached out to Apptopia to check the app data on Fubo. Apptopia is a provider of competitive intelligence on mobile applications.

With the information, we issued the following note to our subscribers on April 20th: "Fubo guided to end Q1 with subscribers of 520,000 to 530,000, representing growth of 82% YoY at the midpoint. Data from Apptopia shows that Fubo ended March with approximately 585,000 daily active users (DAU) versus the Q1 guide for 525,000 paid subscribers at the end of Q1."

On May 11th, the company went on to report 105% year-over-year growth and 8% sequential growth for 590,430 MAUs with subscription revenue increasing 131% YoY to $107.1M. Therefore, we were within 6K subscribers on the estimate.

Net subscriber additions were approximately 43,000 versus a loss of 28,000 in the same quarter last year, which the company achieved while reducing sales and marketing as a percentage of revenue. Monthly ARPU increased 28% year-over-year and advertising ARPU was up 57%.

Paid and trial users streamed more than 228 million hours, up 113% YoY. MAUs on average watched 129 hours per month, up 8% YoY.

This is the second time we accurately tracked Fubo’s audience growth with Apptopia data. The first was when we pointed out during a flurry of short reports that the audience growth in Q4 was quite healthy.

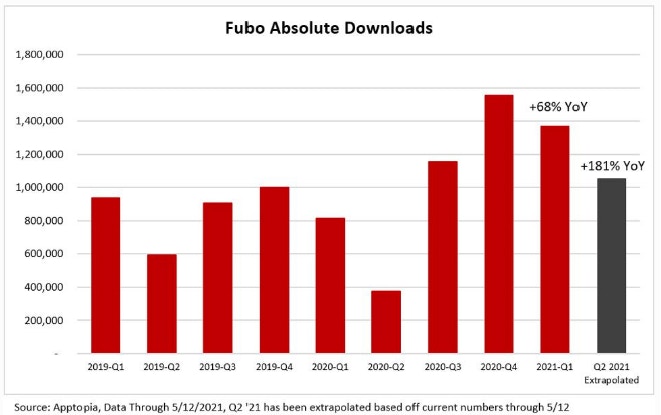

According to Q2 data from Apptopia, as of May 12th, Fubo’s growth remains strong on a year-over-year basis. We are currently seeing app downloads tracking at 181% YoY against weak Q2 ’20 comps due to the cancellation of sporting events last year.

Please note that we have extrapolated the data through May 12th to the end of Q2 and we were roughly 46% through the quarter as of last week.

Note: this data is not for earnings calls and readers must do their own due diligence. We are simply sharing information from a mobile analytics firm, which is one of the many channel checks we do when looking at tech stocks.

Fubo is tracking for a sequential QoQ decline in downloads in Q2, but it should be noted that Q2 is historically a weaker quarter than Q1 for Fubo, as evidenced by 2019 pre-pandemic data.

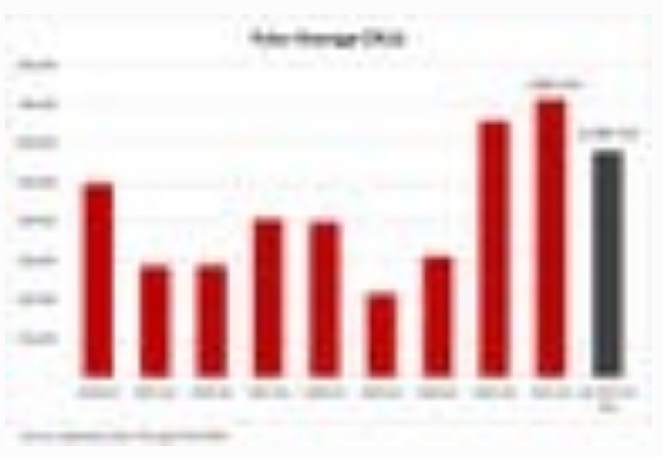

We are seeing similar trends in average daily active users (DAUs) thus far through Q2, with Fubo on pace for 172% YoY growth and a modest decline sequentially.

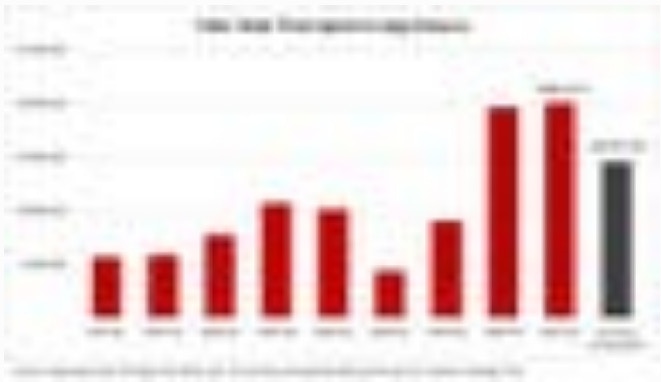

Total time spent in the Fubo app is currently on pace for a large YoY increase of 237%, with another modest decline sequentially from Q1. This helps support how sticky Fubo’s product is to its audience.

Fubo raised guidance and expects Q2 revenue of $121M at the midpoint, up 174% YoY, versus consensus of $98.37M, and FY2021 revenue of $525M at the midpoint, up 101% YoY versus consensus of $472.69M.

The company also raised guidance for subscribers. For Q2 the company expects 600,0000 to 605,000 subscribers, up 111% YoY and for the full year expects 830,000 to 850,000 subscribers, up 53% YoY at the midpoint.

Live Sports OTT

Not surprisingly, we saw the biggest drop ever in households with cable packages this past year with a record 7.5% decline. Tech Crunch recently stated the 2020 pandemic accelerated the projected cord cutting rate to 31.2 million households last year and is expected to reach 46.6 million households by 2024.

Even more pertinent, according to a survey compiled by Parks Associates, 55% of cable subscribers state that live sports is an important factor in why they are staying with expensive cable packages. That means of the 77.6 million currently subscribing to cable, satellite and telecom packages, 42 million are live sports fans. This is 10 million more than the size of the current cord-cutting audience, which has taken nearly 15 years to amass (circa 2007).

In September of last year, AT&T paid $3.75 billion for the exclusive rights to segments of major league baseball. This is a renewal of prior contracts and is a 65% increase from their prior exclusive price tag. The fact that ATT is willing to pay a 65% premium from their last contract shows the importance placed on live sports.

We can see a similar evidence as to the value placed on live sports with Amazon’s purchase for the exclusive rights to the Thursday night NFL games through 2033 at an astounding $100 billion.

As an investor, I understand FuboTV will not stream every game in every league, and I am aware exclusive rights to various sports may shift through negotiations. In fact, the Tokyo Olympics may be canceled. However, FuboTV is offering me a pure play and the company only needs to corner a percentage of live sports cord-cutters in order to be successful. FuboTV could end up owning 5% of the market or 20% of the market – both look good from this market cap.

When asked about competitors, Anthony Wood of Roku has stated a few times that any cord-cutting is a windfall for their platform. Similarly, I believe that any NFL fans cutting the cord will be a windfall for Fubo.

On that note, Fubo offers comprehensive sports coverage. According to a March 2021 press release, Fubo offers “42 of the top 50 Nielsen-ranked networks across sports, news and entertainment channels,” plus more than 30,000 movies and TV shows on-demand.

It’s also important to note that Fubo has the exclusive streaming rights to the South American Qatar World Cup 2022. When you consider there are 3.5 billion soccer fans globally, suddenly Amazon’s Thursday night NFL deal doesn’t seem so make or break (far from it, Thursday is the least popular night).

Sports Betting

In the United Kingdom, sports betting is a $20 billion industry today. There are projections that sports betting will be a $155 billion industry by 2024. To find an opportunity with exposure to this market at a $3 billion market cap is worth a closer look.

Fubo acquired Balto Sports on December 1st in the company’s first strategic move to launch free-to-play games this year. Balto Sports develops tools and contest automation software for users to organize and play fantasy sports games and is a Y-Combinator graduate.

There was criticism from the short sellers that FuboTV had bought a headline. Yet, there is nothing unusual about a stealth product that needs to attach the technology to an audience. In fact, Fubo plans to beta test its free gaming experience in the next few weeks and this rapid release is likely due to the incubation period that Balto Sports underwent beginning with its time at Y Combinator.

In Q1, Fubo acquired Vigtory, a sports betting and interactive gaming company, for $37.2 million. The company was founded in 2019. The company is co-founded by a former gaming executive at MGM Resorts and has regulatory approval in New Jersey. Notably, the app has not gone live which is reflected in the price.

Fubo Sportsbook is expected to launch in Q4. The company has $400 million cash and is planning to spend less than $50 million to launch sports betting, per the Q1 earnings report. Fubo plans to deliver streaming and gaming in one data analytics platform, offering users a seamless experience. We expect the company will see lower customer acquisition costs as a result of owning the audience. Fubo’s CEO, David Gandler, said during the most recent earnings call that 30% of users are willing to participate in free-to-play, according to surveys done on the platform, while 22% of paid subscribers are willing to place bets on Fubo.

Despite short sellers not seeing how or why a sports betting app could merge with live sports content, we now see DraftKings partnering with Sling/DISH. I guess content and sports betting does go together, after all (yes, I’m being sarcastic!) It’s surprising that the critics said it cannot be done despite Sky Media having the most successful sports betting model globally.

From purely a user acquisition standpoint, in-app ads with your own content is nearly frictionless and you have a mountain of data to effectively target. Fubo’s ability to gather audience data and appropriately market them, with a deep understanding of preferences, is an advantage that is currently understated. Fubo has first-party data and can specifically tailor an experience, which will either result in higher ARPU from betting or higher ARPU from ad spend.

DraftKings, meanwhile, has partnered with the number six over-the-top provider, DISH Network/Sling. We think DraftKings sees the potential threat in Fubo having access to first-party data and a closed-circuit loop for user acquisition in sports betting. Notably, DraftKings faces friction here when introducing a new brand name that is not DISH/Sling. Essentially, whatever DraftKings can do with the #6 partnership, Fubo can do better. For example, Fubo can give free sports content away to high value users who spend over $100 on sports betting and offer other rewards that are not possible unless you own the audience. The CEO talks about this here.

Fubo is already on par with DraftKings in terms of ARPU and has not added sports betting yet. These numbers show that with sports betting, Fubo could potentially see $100 ARPU or greater.

Notably, DraftKings spends an exorbitant amount on sales and marketing at 82% of revenue. This reflects the cost of acquiring users when you don’t own an audience. It’s interesting, of course, that the critics of Fubo do not look at the $1.5 billion in net losses that DraftKings accrues on its bottom line. On a forward basis, DraftKings is estimated to report ($2.82) EPS for fiscal year 2021 compared to Fubo’s estimated ($1.96) EPS.

Notably, despite having 1/3 the revenue and audience size of DraftKings, Fubo is trading at 1/6 the market cap. It’s not hard to see the potential here, and clearly a healthier bottom line isn’t the reason that DraftKings trades at a 300% higher valuation.

Conclusion:

We officially recommended FuboTV in October and did not hesitate to challenge the shorts in January before the last two earnings reports confirmed the company’s strong growth. We specialize in spotting opportunities in tech growth based on product and we were the first analyst (anywhere) to recommend Roku, we were very early to call Nvidia the future for AI during the crypto bust nearly two years before AI drove the data center segment, and we said Zoom’s product would go viral six months before covid.

We are not concerned with broader market weakness that affects short-term price movements. Instead, we look for companies that are executing on a product road map, are capturing a microtrend and are able to scale. Not only do we think Fubo can do this, but we think Fubo will overtake DraftKings in the next 2-5 years.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i