Microsoft Earnings Likely to Prove Cloud Isn't Slowing Down

October 22, 2019

Beth Kindig

Lead Tech Analyst

This week, Microsoft’s earnings will shed light on whether the fear over cloud valuations is warranted or not.

Just last week, IBM results showed that its cloud segment grew by just 14%, boosted by its Red Hat acquisition. In more signs of trouble in the industry, Workday (WDAY) stock declined sharply last week after the company said that growth in its once-lucrative human capital management was slowing to 20%. This led to analyst cuts from Stifel, Deutsche Bank, and RBC. Morgan Stanley (MS) and Evercore ISI analysts have also rushed to downgrade the cloud industry ahead of the busy earnings extravaganza. Companies like Slack, Okta, Splunk, and Salesforce have dropped by 27%, 25%, 20%, and 8% respectively in the past three months.

This week, Microsoft earnings will be important because they will provide a picture about whether this sell-off and pessimism is warranted. Microsoft is important because it is the biggest cloud computing company in the world. It’s impressive growth in cloud has pushed it to become the second-biggest company in the world with a valuation of more than $1.07 trillion. Don’t be surprised if the sector ignores the market sentiment and reports impressive earnings.

Microsoft will provide a good indication of the cloud sector because of its broad offerings. The company has a large portfolio of cloud software (SaaS) and cloud infrastructure (IaaS) products. The IaaS and SaaS industries have grown to almost $40 billion and $95 billion in the past decade. This growth is expected to accelerate in the coming years as global corporation and governments embrace the efficiency of cloud. The industry revenue could double in the next three years. Although there will be many winners in the cloud race, Microsoft is well-positioned because of its scale and its approach of the industry. Just this week, the company acquired Mover, a small company that will help it simplify and speed migration to Microsoft 365.

Also Read : Why Microsoft (Not Amazon) Will Win the Pentagon Contract

Cloud Cycle

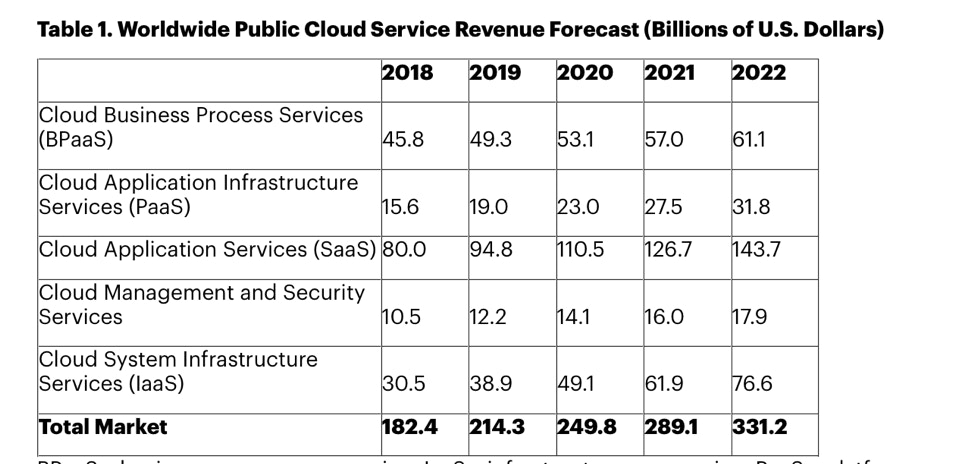

The cloud sector has had impressive growth in the past decade. This growth is just getting started. According to Gartner, cloud spending will accelerate at nearly three times the rate of the overall IT sector through 2022. The research firm expects IaaS sector to grow by 27.5% in 2019 to $38.9 billion. It is expected to reach $76.6 billion by 2022, which is an incredible growth.

Not only this, Gartner expects other cloud sectors like Platform-as-a-Service (PaaS) and SaaS to nearly double. Another estimation is that 90% of companies will purchase these products from a single company. As a market leader, with a diverse suite of PaaS, IaaS, and SaaS products, Microsoft will likely be a potential beneficiary in the cloud cycle.

To be clear. Quarterly results will be inconsistent. It has been like this in all fast-growing sectors.

Source: Gartner

Microsoft

The past few months have been challenging for technology stocks. Yet, Microsoft has been a better performer. In the past one year, Microsoft’s stock has soared by 27% compared to Amazon’s 1.2%, Alphabet’s 13%, and Apple’s 9.6%.

Microsoft has beaten its peers mostly because of its approach to the cloud sector. The company was early to embrace hybrid cloud strategy, which started to take hold in 2018. This was two years after the company’s first technical preview in 2016.

Also Read : Here’s Why Microsoft Stock Could Overtake Amazon on Cloud Infrastructure

This growth has happened even as the company’s valuation has gotten cheaper. The company has a trailing PE ratio of 27.5, which is much lower than last year’s ratio of 46. This implies that the 27% stock gain has been well-earned.

In the past quarter, the company reported great results. Its revenue of $33.72 billion beat the consensus estimates by $920 million. The EPS rose to $1.37, which was 16 cents better than what the market was expecting. In the previous quarter, Microsoft’s revenue of $30.57 billion was $760 million higher than the consensus estimates. Since 2014, the company has had just one EPS miss and three revenue misses.

In the most-recent quarter, the company’s growth momentum continued. Commercial cloud grew by an annualized rate of 39% while Azure grew by 64%. Dynamics 365 grew by 45% while Office 365 grew by 31%. These are excellent numbers for a company that was ignored and ridiculed by the investment community.

Investors should pay close attention to hybrid cloud when looking at Microsoft. Looking at it carefully will give them perspectives about how the company is positioned to set itself apart from other cloud companies like Microsoft and Google.

Hybrid cloud is a technology which enables companies to store some of their data on their own servers while simultaneously sending other data to the private and public cloud. Companies love hybrid cloud because it is cost-efficient, transparent, and safe. Azure’s strength in hybrid computing has made it the main player in the industry. The product is used by 95% of Fortune 500companies.

Government agencies like the Department of Defense are starting to invest in this technology. Last year, I wrote a long-form article explaining why Microsoft would be a better contender for the $10 billion Joint Enterprise Defense Infrastructure (JEDI) contract. In August, the department, which had favored Amazon paused the procurement process on Amazon security concerns. There were also concerns over why single-sourcing was used for such a sensitive contract.

The decision by the DoD to pause means that Microsoft could be at play to win the contract. Microsoft is a leading contender because of its track record with the DoD. Recently, the department awarded the company a software computing contract worth about $7.6 billion. The Defense Enterprise Office Solution (DEOS) will provide productivity tools to the U.S. military.

Microsoft’s cloud products are also used widely in the country’s intelligence sector. In May 2018, the U.S. Intelligent Community announced that it would continue to use Microsoft’s products like Azure Government, Office 365 for US Government, and Windows 10. In the announcement, Microsoft said that its Microsoft Cloud for Government solutions were used by over 10 million government customers.

In 2018, the company won a $480 million contract to supply about 100k augmented reality devices to the US military. The company won this contract after competing with other companies like Magic Leap, Lockheed Martin, and Raytheon. The military bought these devices because it wanted to incorporate night vision and thermal sensing in its training.

The U.S. Department of Defense has partnered with Microsoft on more projects. This means that there is a possibility that the company could be a leading contender on the JEDI project.

Also Read : Microsoft Stock Price: Technical Analysis

Conclusion

Microsoft will release its Q1’20 earnings on Wednesday. Analysts expect the company’s earnings to increase to $1.24 from $1.14 a year ago. Revenue is expected to jump from $29.08 billion to $32.24 billion. As with all of its earnings, the market will be focusing on the cloud segment. There is no evidence that this revenue will slow down. While uncertainties on trade and economic growth could lead to some fluctuations, Microsoft has an advantage because of its cloud strategy and execution.

A version of this article originally appeared on MarketWatch October 22nd, 2019.

More To Explore

Newsletter

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su

Nvidia, CoreWeave, and Nebius: Inside the Circular Financing of the GPU Boom

Neoclouds are one of the more hotly debated AI business models, with CoreWeave and Nebius being the two most widely recognized names. These companies have seen their sales, backlog, and share prices s

AMD, Nvidia, Arm, Intel: Inside the $120 Billion CPU Gold Rush

CPUs have gone from an afterthought to becoming the AI trade’s next great bottleneck – and with AMD, Nvidia, Arm and Intel circling a market that is doubling nearly overnight, the only question left i