Here’s Why Microsoft Stock Could Overtake Amazon on Cloud Infrastructure

December 06, 2018

Beth Kindig

Lead Tech Analyst

The cloud infrastructure market is expected to reach $83.5 billion by 2021, up from $40.8 billion in 2018. Amazon Web Services was launched in 2006, which means it took twelve years for the infrastructure-as-a-service (IaaS) market to reach $40 billion – but will take only three years for the next $40 billion to accumulate. Therefore, the investment window for cloud infrastructure stocks is far from over.

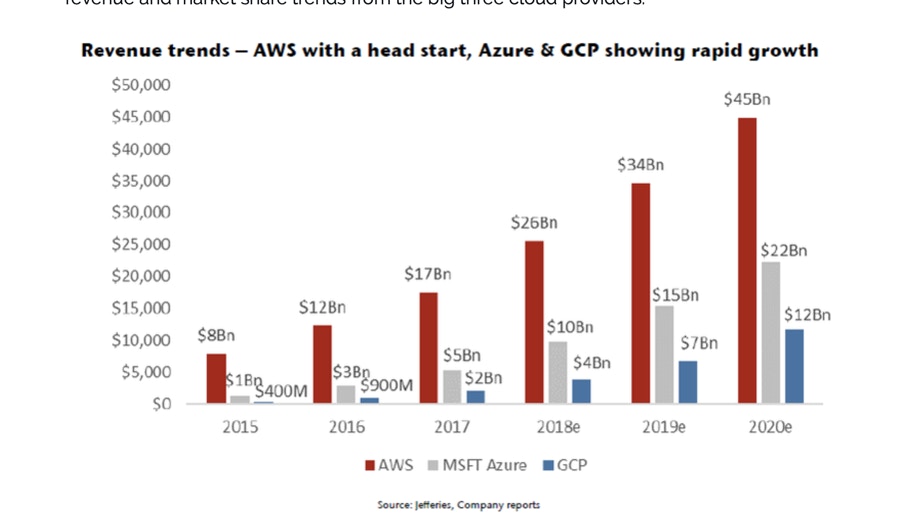

The IaaS segment is currently Amazon’s most profitable revenue stream comprising 55% of its quarterly operating profit, and is also the top growth-driver for Microsoft at 89%. Considering these are two of the three companies vying for most valuable company in the United States, it’s easy to see why IaaS could be the determining factor on who will remain in this position. AWS has a formidable lead in cloud infrastructure with estimates of $26 billion in sales last year compared to Microsoft’s $10 billion.

However, there was an important strategic acquisition Microsoft completed last month which will narrow its position in second place – and it’s my prediction that this specific acquisition will be a primary driver that will propel MS into first place in the next 2-3 years. Before I discuss the acquisition, I think it’s important to provide an overview of the IaaS segment.

Also Read : Why Microsoft (Not Amazon) Will Win the Pentagon Contract

Brief Overview of IaaS Cloud Stocks

Gartner analysis bumped Oracle and IBM from the leader quadrant this year, while placing Google Cloud in third behind AWS and Microsoft. For all intents and purposes, these are the three cloud infrastructure companies remaining for serious stock investors after a period of fierce consolidation. At one point, Amazon had more market share than the trailing 14 cloud infrastructure companies combined. It now has the market share of the trailing 5 companies combined. This reflects Microsoft and Google’s growth as the territory Amazon has forfeited was primarily gained by MS Azure and also Google Cloud Platform (GCP).

AWS has an outstanding lead at 33% of the market, with Microsoft at 13% and Google at 5-6%. These margins are why Amazon posts 40% growth while Microsoft posts 98% growth – there is simply more territory that MS can gain as a second-place participant. GCP claims the most growth because its revenue is small enough to post these gains.

Suffice to say, current revenue is not a solid indicator of who will capture the $40 billion projected growth over the next three-year period. In fact, I believe AWS will have its hardest years ahead as Microsoft’s singular focus has been to grow Azure, and this strategy will be reflected in earnings between 2019-2022. AWS is the most mature provider in this category, but Microsoft has deeper experience with strategic IT dominance. The effort at which Microsoft is driving adoption to .NET CORE and Azure is, surprisingly, not something we see with AWS (more on this below).

To some extent, this reason could easily be explained by Amazon’s ever-expanding focus. The company may be too distracted with growing its e-commerce dominance, such as Prime deliveries and also Prime OTT streaming, plus the Whole Foods acquisition, as well as its plans to disrupt the healthcare industry and the connected home. It’s easy to see how Amazon might lack the focus in strategic investments that the competitive cloud infrastructure market will demand. Microsoft, on the other hand, is putting its entire weight behind IaaS, and the next couple of years will be interesting to see how this plays out.

Also Read : Microsoft Earnings Likely to Prove Cloud Isn’t Slowing Down

Microsoft’s Strategic Move to Acquire the World’s Largest Open Source Repository

Microsoft’s dedication to become the cloud infrastructure leader was demonstrated last month with the acquisition of Github for $7.5 billion, which is a repository for developers to upload projects and files. There are 28 million active developers collaborating on GitHub. In other words, every single developer in the world is on GitHub. In fact, GitHub’s user base is larger than the total number of developers globally, which is an impossibility the founder pointed out last year, proving the platform’s omnipresence.

“Git” refers to version control systems, which developer-talk for an open version of all the modifications made to projects (like writing code), that is stored in one central repository. Collaboration and sharing are at the essence of open-source software, and Github provides a social environment for this to occur. There is a ton of innovation which happens here, and almost every developer hosts their code and projects here for the world to see (or even for employers to review during job interviews). Developers can “fork’ a project, or split a project, by creating a new project off an existing one. Or they can issue a pull request to have the original developers of a project incorporate new code.

My newsletter subscribers get this information first. Sign up here.

Ironic is the best word to describe Microsoft’s venture into open source technologies and repositories. At one time, the company was loathed by the developer community for their closed standards, as the Founder Bill Gates adamantly believed software should be proprietary. In the late 90s, leaked documents showed Microsoft had attempted to contain the open source movement, and to prevent Linux from competing with Microsoft software by locking customers into proprietary protocols. (Linux is the free and open-sourced software operating system that launched in the early 90s and Android is built on today; Windows is the anti-thesis to this operating system).

Developers seek open source environments so they can learn from each other, and to support more innovation. Today, AWS excels when it comes to open source development due to being an early supporter of Linux. However, Microsoft is attempting a complete one-eighty by embracing the open-source community, and if MS succeeds, it will pay in dividends for Azure as it goes head to head with AWS.

This venture into open-source advocacy has been planned for some time. Over the last few years, Microsoft became the top contributor on Github with 2 million projects, which helps position Microsoft as an advocate while evangelizing the .NET framework and the .NET CORE that runs on Windows, MacOS, and Linux. Microsoft now claims that 40% of Azure’s virtual machines are running Linux.

Furthermore, MS acquired Xamarin two years ago, the leading mobile application development platform. The tools help developers navigate across the various programming languages required by different platforms, such as iOS and Android on native, web applications, or a mix of both with 75% of the code re-usable. This greatly reduces development time and resources, and also demonstrates that MS is ready to host and support competing operating systems in order to gain on cloud infrastructure.

Takeaway: Microsoft is courting developers because they are a primary decision maker as to which cloud service a company will use. MS Azure’s current customers are enterprise level, such as Fortune 500 companies. Microsoft’s strength is that most businesses at this level have a significant investment in MS products, and it is easier to go with MS because it is what they know, and the transition is easy as the IT department won’t have to be trained on AWS or Google Cloud.

However, Microsoft’s blaring weakness is open source, and the some 28 million developers that are on smaller teams, and who socialize on Github, are decidedly open source. For $7.5 billion, Microsoft has done what every great company should do – acquire to address your weakness.

Both Xamarin and Github are highly strategic acquisitions. Microsoft paid 25 times the value of Github, which has revenue of about $300 million. Alphabet was also interested in purchasing Github, according to inside sources.

Also Read : Microsoft Stock Price: Technical Analysis

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su