Nvidia Stock Is Ready To Rumble With RTX 40 Series And H100 GPUs

September 28, 2022

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Sep 23, 2022,04:33pm EDT

Nvidia had a big week with GTC 2022 and management is clearly ready to rumble against any excess inventory from crypto mining. The negative catalyst from crypto mining and Nvidia's price action is eerily similar to Q4 2018/Q1 2019 —- yet the company is not the same company it was four years ago. This is apparent by Nvidia flexing some major product muscle by timing it's best-ever gaming release and it's best-ever AI chip to hit the market in October.

We draw important parallels (pun intended) between the last crypto mining selloff and this selloff with key reasons as to why this time the stock's comeback will be quicker.

Nvidia stock has been in the clutches of a steep drawdown after the company has faced nearly every headwind imaginable: United States-China tensions, supply chain disruptions spanning many components, tough comps on the data center, tough comps on gaming, and a less-than-rosy macro environment.

The most impactful headwind, however, was Ethereum’s merge to Proof of Stake (PoS), which ultimately lowers demand for gaming GPUs. This contributed to a $2.5 billion cumulative miss in revenue driven by the gaming segment.

Nvidia’s stock performance in 2018 and 2022 feels eerily similar as the stock sold off 54% in 2018 specifically because of a gaming miss tied to crypto mining. Today, Nvidia is currently 57% YTD.

It took eighteen months for Nvidia to recover its all-time high from the Q4 2018 selloff (Sept 2018 through Feb 2020). Despite the uncanny similarity that 2018 and 2022 may have — Nvidia is actually a much stronger company today than it was four years ago.

Below, we discuss a few key reasons Nvidia stock will recover quicker this time around.

Drilling into Parallels Around the Gaming Miss

During the Q3 2018 results released in November 2018, Nvidia gave Q4 2018 revenue guidance of $2.7 billion, below the analysts’ consensus estimate of $3.4 billion. In January 2019, the company again lowered revenue guidance from $2.7 billion to $2.20 billion, which suggests a total revenue miss of $1.2 billion. Gaming revenue in Q3 2018 was $1.76 billion, up 13% YoY and down 2% QoQ. In Q4 2018, gaming revenue was $954 million, down 45% YoY and down 46% QoQ.

In the most recent quarter ending July 2022, the company missed on gaming with revenue of $2.04 billion, which is 33% lower than the year ago quarter and 44% lower sequentially. The company is expecting a further decline in gaming sequentially for Q3. According to one analyst on the call, they are modeling for a further 30% sequential decline in gaming and professional visualization offset by low to mid-single digit growth in data center and automotive. The CFO affirmed this understanding is correct.

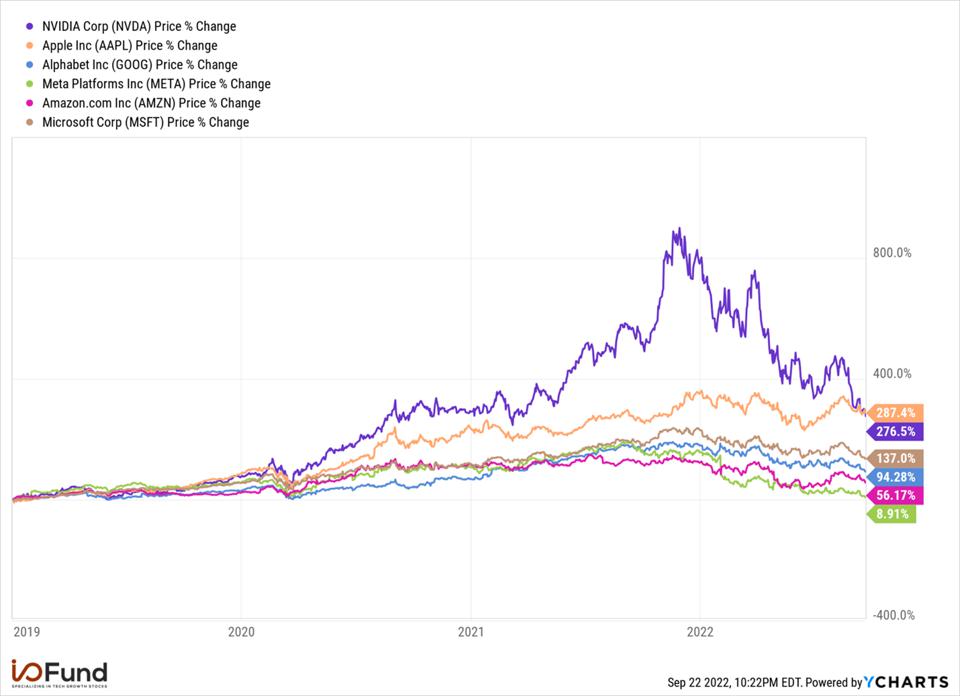

After 2018, although it took Nvidia eighteen months to reclaim its all-time highs, in 2020-2021, Nvidia would go on to stage a remarkable turnaround as the stock led tech mega cap stocks in gains. This was not simply because all tech performed well during those years – if you compare Nvidia to Meta, Amazon and Google, you’ll see something unique occurred with Nvidia that caused the stock to outpace its peers. In all cases except Apple, Nvidia doubled, tripled or quadrupled the performance of other mega cap stocks.

Source: YCHARTS

Perhaps most impressive, Nvidia is still in the lead over all mega cap stocks despite a 57% drawdown this year. It’s the company’s past performance that makes it well worth the time to answer: can Nvidia do it again?

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Nvidia’s GeForce RTX 40 Series is Perfectly Timed

Next quarter, Nvidia was expected to report $6.92 billion and the company guided for $5.9 billion. This is down from $7.10 billion in Q3 of last year. This will be a 17% decline in revenue. Due to this, analysts expect Nvidia to end fiscal year 2023 with 0.8% revenue growth, or $27.13 billion in total revenue.

It’s not only the top line valuation that is affected by this cut in guidance but it’s the bottom line, as well. In previous quarters, high average sales prices drove $2 billion to $3 billion in operating profits and net profits, whereas in the most recent quarter, the company is reporting $500 million and $656 million, respectively.

The GAAP EPS reported was $0.26 compared to $0.94 in the year ago quarter. Adjusted EPS was $0.51 versus $1.04 for the year ago quarter.

Although it’s tempting to redirect the conversation toward higher-growth segments, the $2.5 billion total miss between two quarters came from gaming and it’s prudent for investors to start here (for now) when analyzing the stock for a potential recovery.

The company stated the miss was driven by both lower units and lower average sales prices including reduced consumer demand. The company is not commenting on crypto as they state they have no visibility here as to how the GPUs are being used, however, it’s certainly contributing to the bulk of this decline.

Notably, AMD reported gaming growth of 32% to $1.7 billion which provides a better picture of reduced gaming demand minus crypto. Nvidia believes some of their weakness is also from preparation for a new product generation that will be announced this month.

Per the earnings call, there are two ways that Nvidia plans to overcome the crypto mining selloff which could produce a faster rebound than 2018.

First, Nvidia is restricting supply on its current gaming model. Per the CFO: “Across those two quarters, the Q2 of ‘23, the Q3 of ‘23, we have likely undershipped gaming to our end demand significantly.”

Following the call, we estimated for our premium members that the amount undershipped is a minimum of $1 billion. The reason behind this is to help keep prices stable and to increase demand for the RTX 40 Series.

Second, Nvidia announced its GeForce RTX 40 Series at the GTC 2022 Conference this week.

The new Ada Lovelace architecture which uses 76 billion transistors and a 4nm production process. In the keynote, the CEO stated: “Nvidia engineers worked closely with TSMC to create the 4N process optimized for GPUs. This process let us integrate 76 billion transistors and over 18,000 CUDA cores, 70% more than the Ampere generation.”

The improvement from 8nm to 4nm means more transistors on the GPU, which results in better performance as the 4nm processes data faster.

In the gaming world, this much anticipated release is expected to be 2-4X faster than the RTX 3090 Ti. The flagship AD102 GPU model will have 144 individual streaming multiprocessors (SMs) in one die compared to 84 SMs in the Ampere architecture. As stated, the AD102 will also have a 70% increase in CUDA cores over the RTX 3090 Ti.

In addition to this, Nvidia is releasing a new feature called Shader Execution Reordering (SER) which will improve ray-tracing performance by 3X with 25% faster frame rates. Rather than deliver workloads sequentially, the GPUs are able to reorder the workloads to process more workloads at once which results in more power and better performance.

Deep learning super sampling (DLSS) refers to using AI to predict the next pixel. The new DLSS 3.0 not only predicts pixels but will also use AI to predict frames. This results in “up to four times” better performance over traditional rendering.

The first release date for the RTX4090 models is October 12th with a starting price of $1,599. There is a second release date in November for the RTX4080 models with prices of $1,199 and $899. Notably, mid-range RTX 40 series will outperform the previous generation’s high end models. This is due to the Ada Lovelace architecture which offers 1,400 Tensor TFLOPs versus 320 Tensor TFLOPs which means the DLSS is superior and the high-end RTX 30 Series cannot compete with the mid range RTX 40 series.

The popularity of this release will help determine if Nvidia can stage a comeback in the gaming segment. Here is what analysts are saying:

“Morgan Stanley analyst Joseph Moore said his "biggest takeaway" from the keynote at Nvidia's GTC conference were the higher prices of gaming GPUs, which increases his conviction about the pace of gaming revenue recovery next year. Prices that are 28% higher than the baseline price from two years ago for the higher volume 4080 should drive material growth in revenue, said Moore, who sees revenues in the gaming segment rebounding from the current quarter run rate of $5.5B or so to $9.5B next year.”

“Given the channel inventory work downs in the July and October quarters, the products should be "strong demand catalysts" into 2023, Harlan Sur of Chase tells investors in a research note.”

Nvidia Continues to Build a GPU Moat with H100

In 2018, we stated in our free newsletter that Nvidia had built a moat in the GPU-powered data center. This was a bold statement as the company would go on to have negative year-over-year data center revenue in 2019. Yet, fast-forward and it’s quite clear that Nvidia is unshakeable in this segment, which has surpassed gaming as Nvidia’s most valuable segment.

I’ve written quite a bit about Nvidia, which you can reference here and also here. However, I will keep it simple by saying the A100 GPU is what led the company’s gains since Q2 2020 (detailed here) and the Hopper H100 GPU is what will lead the company’s gains for the next two years.

In the most recent quarter, data center revenue of 61% is down from 83% last quarter yet accelerated YoY from 35% growth in the year ago quarter. The earnings call reviewed some of the challenges Nvidia faced in the quarter that led to the 1% sequential growth.

First, Chinese hyperscalers slowed their infrastructure investment this year yet the slowdown is unlikely to last much longer. Due to being a large market for Nvidia, the data center growth was impacted by this. The reason Nvidia was able to meet expectations is because “North America doubled year-over-year in revenues.” As of now, supplying the Chinese military is restricted for Nvidia, but this does not include supplying the hyperscalers.

Second, demand continues to outstrip supply yet there are many components to Nvidia’s systems and they are experiencing supply chain issues.

“We were challenged this quarter with a fair amount of supply chain challenges because as you know, we don’t just sell the GPU chip, but these systems are really complex with a large number of chips in the system components that we offer like HGX […] all of the components that have to come together for us to be able to deliver the final component.”

H100 Hopper Coming in October

On the earnings call, an analyst asked if the company expects data center growth to re-accelerate when Hopper ships: “Do you think that Hopper, as that comes fully available, it sounds like in fiscal 4Q, that you actually see Data Center growth reaccelerate as that product cycle materializes.”

The CFO Kress stated: “Our Data Center yes, we do expect it to grow. It may grow about what we just saw between Q1 and Q2. We’ll continue to look at it.”

I believe this means the data center will accelerate above 61% but not to exceed the 83% from Q1. Ultimately, the CFO may not have full visibility into Hopper sales until the units ship and are tested by customers, who in turn, often buy more if the product exceeds expectations.

On that note, the new 4nm chips are bound to impress. The H100 GPUs and the DGX H100 server pods and super pods offer Nvidia the next leg-up as the company has solved an important bandwidth issue.

Hopper tackles some of the bigger issues around previous generations like speeding up algorithms by offering dynamic programming on GPUs to break down problems to simpler subproblems. The new GPUs also boost bandwidth by 3X with SHARP in-networking computing and Infiniband Switches, and the H100 can leverage NVLink to connect eight H100s into one giant GPU for 640 billion transistors, 32 petaflops, 640GB of HBM3, and 24 terabytes per second of memory bandwidth.

The H100 has about 50% more memory and interface bandwidth than the A100. That’s 1.5X more bandwidth with the NVLink connection and PCIe 5.0 doubling the bandwidth of PCIe 4.0. The H100 will ship with support for 80GB of HBM3 memory at 3 TB/s speed

Where the H100 really stands apart is the leap in performance with about 3X more performance than the A100 and the H100 is up to 6X faster. The A100 lacked support for FP8 compute at default whereas the H100 will leverage a transformer engine to switch between FP8 and FP16, depending on the workload.

According to Nvidia, the H100 delivers 9X more throughput in AI training, and 16X to 30X more inference performance. The company also states in HPC application-specific workloads, the H100 is 7X faster. The goal of the H100 was not only to add more transistors and make the H100 faster, but to also offer function-specific optimizations. This is achieved through the transformer engine.

Last week, MLPerf published artificial intelligence performance tests. The parent company MLCommons provides the industry standard for benchmarking deep learning, AI training, AI inference and HPC. The H100 Tensor Core GPUs delivered 4.5X more performance than the A100 in offline scenarios and 3.9X more in the server scenario compared to its predecessor the A100.

The Hopper H100 GPUs are in full production and availability starts next month and will have over 50 server models by the end of the year and “dozens more in the first half of 2023.”

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Nvidia’s Automotive Opportunity is Massive

Nvidia’s lead in automotive across dozens of OEMs requires its own analysis, which we will write for our free newsletter subscribers next year. Hyperion 8 is shipping in 2024 and Hyperion 9 will ship in 2026. However, as long-term Nvidia investors, now is a good opportunity to remind my readers of the long-term vision for yet another large and sweeping revenue segment.

Although a small segment today of only $220 million, automotive grew 59% sequentially and 45% year-over-year. The company has a $11 billion automotive design win pipeline.

At GTC this week, Nvidia announced a new superchip named “Thor” which will deliver 2,000 teraflops of performance, up from 200 teraflops from the current generation “Orin.” The chip has a transformer engine which can process video data as a single perception frame and offers 8-bit floating point (FP8) precision to avoid task loss when converting model data from one platform to another platform.

More on the Omniverse

We’ve covered the Omniverse platform in the past including an interview with Nvidia’s Richard Kerris you can view here.

At GTC this week, Nvidia launched Omniverse Cloud, which is a infrastructure-as-a-service software offering to reduce the complexity around building 3D virtual worlds and assets. This removes the need for local compute power and opens up the ability for more creators to access 3D world creation.

Regarding the China Restrictions

The United States government is restricting sales of high-performance chips to China as Nvidia’s AI chips could be used for military purposes. A spokesperson for Nvidia stated the products where the new licensing requirement applies is the A100, H100 and systems that include DGX.

The restrictions apply to Russia yet Nvidia has stated there is no exposure to Russia for their products. In a recent SEC filing, the company stated: The Company’s outlook for its third fiscal quarter provided on August 24, 2022 included approximately $400 million in potential sales to China which may be subject to the new license requirement if customers do not want to purchase the Company’s alternative product offerings or if the USG does not grant licenses in a timely manner or denies licenses to significant customers.

At this time, Nvidia has applied for an exemption and there has also been a clarification that Nvidia can continue to develop the H100 in China through September 1, 2023 through the company’s Hong Kong facility.

Per the SEC Filing dated August 31, 2022:

The U.S. government has authorized exports, reexports, and in-country transfers needed to continue NVIDIA Corporation’s, or the Company’s, development of H100 integrated circuits after the Company filed its Current Report on Form 8-K with the U.S. Securities and Exchange Commission on August 31, 2022. The authorization also allows the Company to perform exports needed to provide support for U.S. customers of A100 through March 1, 2023. Additionally, the U.S. government authorized A100 and H100 order fulfillment and logistics through the Company’s Hong Kong facility through September 1, 2023.

Some analysts have stated that being granted an exemption is “feasible.” Mark Lipacis of Jefferies is modeling for a $200 million hit to October rather than the $400 million identified risk. Harlan Sur of JP Morgan noted AMD is working on getting export licenses for its customers and helping them transition to products that fall below the performance threshold to help mitigate the downside risk.

According to a new report, Nvidia has asked TSMC to rush high-end GPU orders before the US sanctions begin. The report says that TSMC has a special program to speed delivery of orders at a higher negotiated price and can help to cut the delivery time in half. This could lead to a surprise bump in Q4 revenue for the company.

Conclusion

Nvidia is not the same company that it was four years ago. In 2018, Nvidia was a gaming company with promising AI tailwinds. Today, Nvidia’s AI products serve nearly every enterprise company’s artificial intelligence and machine learning ambitions.

The company has an impressive launch schedule starting in October for two flagship products – the RTX 40 Series and the H100 GPU. The timing of these releases is no coincidence as it’s a rapid two months following the crypto/gaming revenue miss. Suffice to say, Nvidia’s management team is prepared to rumble —- putting its very best release in gaming and its most powerful AI chip to-date up against the crypto mining selloff. If history is any indication, the turnaround will only be a matter of time.

Please note: The I/O Fund conducts research and draws conclusions for the company’s portfolio. We then share that information with our readers and offer real-time trade notifications. This is not a guarantee of a stock’s performance and it is not financial advice. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis. Beth Kindig and the I/O Fund own shares in NVDA at the time of writing and may own stocks pictured in the charts.

More To Explore

Newsletter

Updated Nvidia Stock Price Target - AI “Bubble” Narrative Ignores Re-Acceleration in Big Tech Capex

In the analysis below, my firm crunched the hard data on Q2 capex numbers and what is coming down the pipe for Q3. If you are an AI investor like we are, this is an analysis you will not want to miss

Oracle Soars After Earnings – Is ORCL Stock Still a Buy?

The market is clearly excited about this report, and for good reason. Remaining performance obligations (RPO) grew 359% YoY with cloud RPO growing “nearly 500%” on top of 83% growth last year. Another

Nvidia Stock Forecast: The Path to $6 Trillion

Two years ago, the April 2023 quarter delivered a historic 18% beat, followed by an even bigger 30% beat in July 2023. Compare that to the most recent quarter ending July 2025 — just a 4% beat, the sm

Bitcoin Bull Market Guide: When to Hold, Trim, or Re-Enter (Webinar)

Our track record including a more recent 600% move in Bitcoin is not the product of hype but of a systematic framework—one built on technical analysis, on-chain metrics, and a close watch on global li

Reddit Stock Blows the Doors Off - Can it Last?

Reddit’s stock has surged 62% in one month, easily placing the company’s earnings report as one of the best to come out of the tech sector this quarter. The world’s leading forum site has only 416 mil

ServiceNow Q2 Earnings: Inside the AI Push Toward $1 Billion ACV by 2026

Last month, after ServiceNow reported second quarter results that exceeded expectations on multiple fronts, shares of NOW rose by 6%. The company is attempting to reposition itself beyond a provider o

Is Bitcoin’s Bull Run Nearing a Top? What the Herd Missed at $16,000 and is Missing Now

In late 2022, when Bitcoin was trading near $16,000, the I/O Fund issued a Strong Buy Alert. At the time, many of the market’s biggest crypto bulls were silent. Fast forward to today, Bitcoin is up ov

Is the S&P 500 Overdue for a Correction? 2025 Forecast & Buy Levels to Watch

In our last Broad Market Report titled, Historic Uncertainty Meets $7 Trillion Dollar Debt Wall: What Comes Next For The S&P 500, the S&P 500 was trading near 5800 and still well below its February hi

Google Stock Clears Major Hurdle, Yet One Serious Concern Remains

This week, Google cleared a major hurdle with Search accelerating from 10 points of growth last quarter to 12 points this quarter -- putting to rest many doubts that Search monetization is at risk giv

Can Oracle Become the Next $1 Trillion AI Stock?

When it comes to AI cloud leaders, Oracle is not often mentioned, yet the company is quickly positioning itself to lead among Microsoft, Amazon and Alphabet when it comes to cloud growth over the next