Tesla Stock Faces Recalibration of Growth Expectations

April 17, 2025

I/O Fund

Team

It was no surprise that Tesla’s Q1 deliveries came in below estimates, given the multitude of data points across Europe and China that pointed to significant YoY declines in demand. We pointed out in the first week of March when we last covered Tesla’s stock that given this weakness in core regions and transitory production impacts from the refreshed Model Y, there was a risk that Q1 deliveries would fall to well below 400,000 vehicles, whereas consensus estimates at the time were calling for more than 410,000.

Tesla’s stock is now facing a recalibration of expectations after Q1’s delivery report missed by a wide margin, with revenue and EPS growth estimates falling sharply into its earnings report next week. Below, I dig into the risks Tesla’s revenue faces in Q1, growth expectations for the year, and the bigger picture ahead.

Tesla’s Q1 Deliveries Miss Mark

Tesla reported 336,681 deliveries in the first quarter, more than 40,000 shy of the 377,592 estimate, representing the worst performance in two years. This represented a (13%) YoY decline in deliveries, while production fell (16%) YoY to 362,615 vehicles, the lowest quarterly production since Q2 2022. Tesla said that the transition to the refreshed Model Y led to “several weeks” of lost production.

Q1 saw a sharp decline in Tesla’s production and deliveries to the lowest levels since 2022. Source: I/O Fund

These delivery and production figures provide a few clues for the upcoming earnings report and for Q2 as well:

1) Outsized revenue impact due to ASP deterioration and delivery decline

2) Margin headwinds, not just from idle capacity and the refreshed Model Y ramp, but also incentives

3) Possible inventory build-up with production outpacing deliveries by ~26K vehicles, which may force more aggressive financing activity to sell down excess inventory in Q2

4) Recalibration of expectations for 2025 growth

Recalibration of Growth Expectations

The delivery weakness looks to be snowballing into something much larger – a recalibration of growth expectations for Tesla for the full year. Even in the six weeks from our previous update, revenue and EPS estimates for Q1 and for 2025 have continued to drop considerably, marking a rapid shift in expectations impacted by the weak delivery print.

At the start of 2025, Tesla was expected to report $25.98 billion in revenue in Q1, up 22% YoY, with EPS of $0.71, for YoY growth of 58%. These estimates had been little changed since July 2024.

Now, less than a week from Tesla’s report, Q1 revenue is pegged at $21.54 billion, for growth of just 1.1% YoY. Q1’s EPS estimate is $0.43 for a (4%) decline.

Tesla’s Q1 revenue and EPS estimates saw sharp changes heading into the end of the quarter, with revenue estimates coming down more than $2 billion in March. Source: YCharts

Essentially, in just four months, Tesla has shaved off 20 points of revenue growth and more than 60 points of EPS growth, assuming it meets estimates for Q1. This is a sudden, sharp recalibration of growth expectations for the quarter that has carry-over effects for full-year growth.

Now to the full year: at the start of 2025, Tesla was estimated to generate $116.7 billion in revenue, up nearly 19.5% YoY, with EPS of $3.15, up 30% YoY.

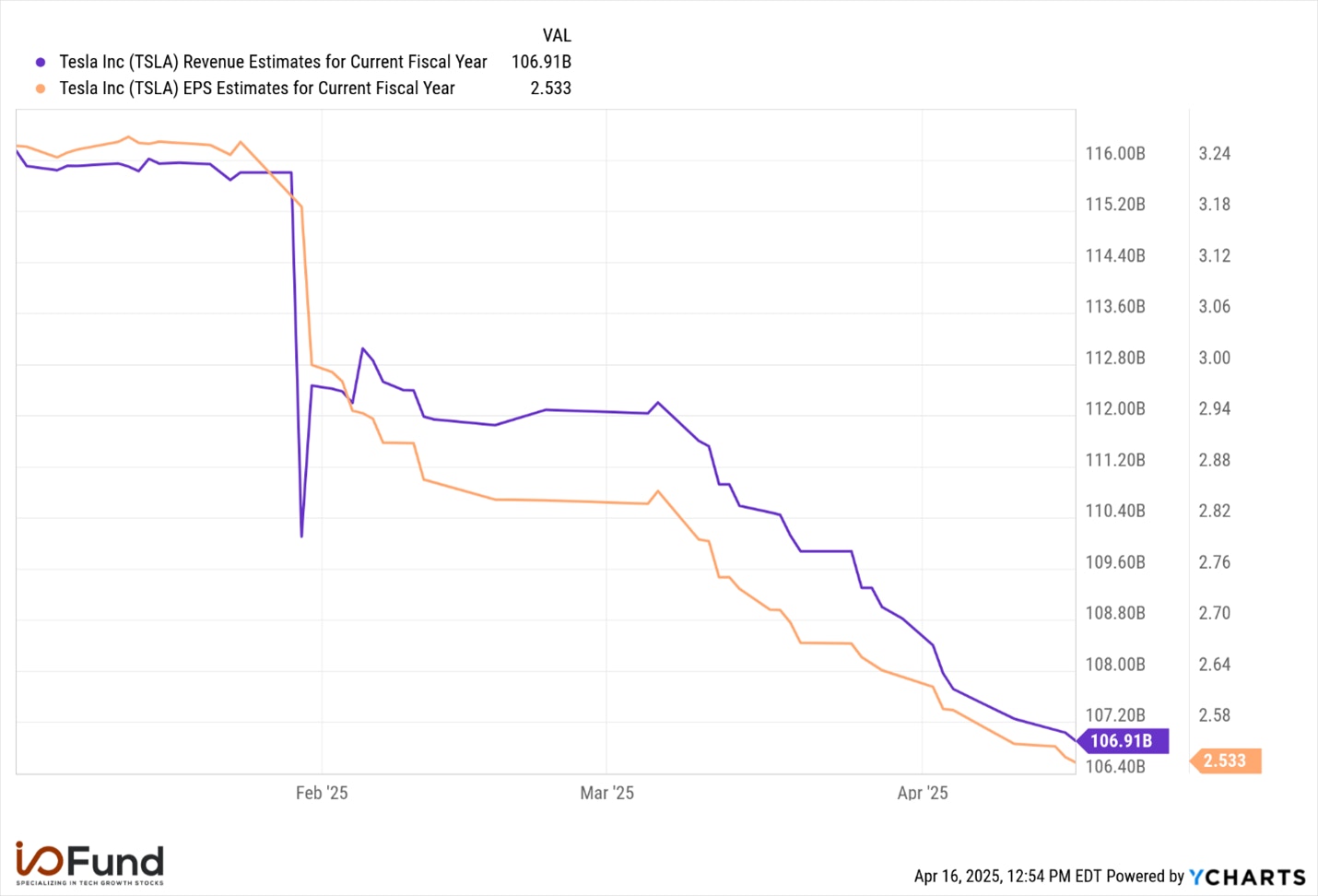

Now, 2025 revenue is expected to be $106.7 billion, $9 billion below where it entered the year and representing growth of just 9.4% YoY, while EPS is estimated to be $2.55, (19%) lower than at the start of the year and representing growth of just 4.6% YoY.

Tesla’s revenue and EPS estimates have fallen sharply since the beginning of the year, with EPS estimates now 19% lower and revenue now nearly 8% lower. Source: YCharts

In just four months, Tesla’s full year revenue growth estimate has fallen 10 points to the high-single digit range, while its EPS growth estimate has declined more than 25 points to the mid-single digit range. This is not solely due to Q1, as Q2 and Q3 estimates have been revised (2%) to (4%) lower as well after Q1’s weak report.

ASP Weakness Exacerbating Tesla’s Delivery Decline

Q1’s revenue is likely to be pressured as weak pricing weighs on Q1’s weak deliveries, providing additional challenges for automotive revenue, its primary revenue segment at 77% of revenue in Q4.

Tesla’s automotive revenue faces amplifying headwinds in Q1, with weaker ASPs weighing on an already large (13%) YoY decline in deliveries. This presents broader growth challenges given that Energy Storage revenue has decoupled from deployment growth, and as a result, Tesla may run the risk of revenue coming in below $20 billion in Q1.

Here’s why:

Tesla has not increased its ASPs on a QoQ basis since Q2 2022. Compared to last year, ASP was ~$3,700 lower YoY in Q4. This alone presents a 9-point additional headwind to automotive revenue growth (excl. leasing and reg credits) simply due to the swift pace of price declines.

In Q1, ASPs faced a complex environment, from continuing promotional efforts (0% APR loans, referral discounts, etc), combined with price hikes for the Model X, slight increases in average transaction prices in the US near the end of the quarter, and the launch of the Model Y Juniper, which may actually provide a drag to ASP this quarter.

Impact of Tesla’s New Model Y

Model Y Juniper’s popularity in China may dent ASP in Q1, as the new variant is priced lower than its US counterpart: the RWD variant is priced at 263,500 yuan, or ~$36,000, while the Long Range AWD is priced at 303,500 yuan, or $41,500, versus $48,990 for the LR AWD in the US before federal tax credits.

The new model reportedly saw nearly 60,000 orders in the first 5 days in China, becoming the country’s top-selling model in March with 43,370 deliveries. The RWD variant is priced nearly 10% below Tesla’s Q4 global ASP in US$ figures, while the AWD variant is just over 3% higher, suggesting that if a majority of sales volumes were for the cheaper RWD variant, global ASPs will face some pressure.

While Juniper carries a higher price tag than the previous Model Y variant, it was only available in the US in mid-March, leaving little time for deliveries to commence in volume. Tesla also has reportedly discontinued the Launch Series, meaning the new model no longer has its $11,000 more expensive option available for sale, limiting its ability to positively impact ASPs.

Tesla Could See Q1 Revenue Below $20 Billion

Assuming ASPs remain approximately flat QoQ due to the aforementioned factors – slight price hikes, base Juniper variant priced below global ASPs in China with strong deliveries, and financing/incentive offers – automotive revenue could decline nearly (22%) to $12.9 billion. Including approximately $1.2 billion in leasing and regulatory credits, total auto revenue could be just under $14.1 billion, or down (19%) YoY.

Energy Storage decoupled from deployment growth in Q4, as revenue grew less than 2% from Q2’s peak despite 17% higher deployments. On a YoY basis in Q4, deployments rose 244%, yet revenue rose just 113% YoY, a staggering 131 point difference pointing to pricing pressures. This suggests that growth is likely to remain pressured in Q1, as Energy deployments declined more than (5%) QoQ in Q1 to 10.4 GWh.

Should Energy Storage revenue follow that pattern of revenue growth weaker than deployment growth, at something such as a (8%) QoQ decline, or up 73% YoY, while Services revenue increases 4% QoQ, this would project total Q1 revenue out to $19.85 billion.

Even assuming 10% QoQ growth in Energy Storage revenue, or up 106% YoY, a 2% increase in ASP (this would be the first time in 11 quarters), $1.2 billion in leasing and regulatory credit revenue, and the 4% QoQ Services growth, revenue would project out to $20.6 billion.

To hit the current consensus of $21.54 billion, which has declined from $22.46 billion since deliveries were reported, Tesla would need a massive 7.5% QoQ increase in ASP, or up $3,000 sequentially, plus 10% QoQ revenue growth in both Energy Storage and Services, with $1.2 billion in reg. credit and leasing revenue, an unlikely scenario.

The I/O Fund specializes in covering lesser-known AI stocks on our research site with trade alerts and weekly webinars. Learn more here.

Lingering Margin Pressures – New Lows Likely Ahead

Tesla is facing a slew of headwinds to margins, as production and delivery numbers are suggesting inventory buildups, alongside known impacts from ramp-related costs. The combination of weaker deliveries and weaker automotive revenue growth is also likely to weigh on already thin margins.

Q4 already saw increased margin pressures from aggressive financing efforts to clear out excess inventory, and average gross profit per vehicle was on the brink of falling below $5,000 as a result. In Q1, Tesla now must contend with much weaker automotive revenue on top of additional ramp related costs for the refreshed Model Y. Ramping Megapack and Powerwall output in Shanghai also is likely to weigh on operating margin in the quarter.

For Q2, margins are likely to face additional pressure from tariff impacts. Tesla acknowledged that tariffs “will have an impact on our business and profitability,” and while the administration has floated “possible temporary exemptions” on imported auto parts and vehicles, nothing is set in stone. Reports from Anderson Economic Group estimate that for US-assembled small crossovers, sedans, and mid-sized SUVs, tariffs costs could be $2,500 to $4,500.

According to NHTSA, for the 2025 model year, Tesla’s vehicles source 20% to 25% of its part content outside the US, primarily from Mexico, opening it up to some tariff risks. Additionally, Tesla was said to have suspended plans to source some components for the Cybercab and Semi following increasing China tariffs, disrupting production timelines for the two vehicles, which were originally expected to start trial production in October.

1.48M More Deliveries Needed to Return to Growth in 2025

We said in our March 6 analysis, Tesla Has a Demand Problem; The Stock is Dropping, that if Q1 did come in weak due to global sales weakness and transitory production impacts, Tesla would have to “make up substantial ground in the back half of the year” to reach optimistic delivery targets.

As you may recall, Tesla quietly shifted its tone on 2025 deliveries growth, with Musk originally stating that 20% to 30% growth was achievable in 2025 in Q3 2024’s earnings call, while Q4’s earnings call shifted the outlook to just a ‘return to growth’.

Now that Q1 deliveries have been officially announced, we can see where Tesla stands on its path to growth. 2024 deliveries totaled 1.81 million, meaning Tesla would need to deliver 1.48 million more vehicles from Q2 to Q4 to return to growth this year.

Q2 is unlikely to ease growth fears, as expectations similarly have been lowered quickly as uncertainty around tariffs and vehicle demand looms. Initial estimates currently point to deliveries between 350,000 to 375,000 for Q2, versus nearly 444,000 in the year ago quarter, though it is still quite early in the quarter and subject to change.

Tesla reportedly halted shipments of Model X and S vehicles to China due to high tariffs, though this is expected to have a minimal impact on deliveries considering the X/S accounted for <5% of global deliveries last year, with China a portion of that. As a whole, China is a major market for Tesla accounting for approximately 37% of deliveries last year, and rising geopolitical tensions could put some of that at risk.

Returning to growth in deliveries this year would require Tesla to deliver over 491,000 vehicles on average each quarter for the rest of the year, based on how Q1 started. This would require Tesla to increase deliveries at ~20% QoQ each quarter, which would culminate in 580,000 in Q4, or a fresh record and pointing to 17% YoY growth, a figure that Tesla has not hit in any of the past nine quarters. Put another way, given Tesla’s annual capacity of >2.35 million vehicles, or 587,000 quarterly, Tesla would need to be producing and delivering at almost maximum capacity come Q4.

The Bigger Picture Ahead for Tesla

As we said in our March analysis, price often bottoms before fundamentals, and it’s clear that Q1 and even Q2 are expected to be the weakest point of the year before the fundamentals improve heading into 2026.

As it stands currently, Tesla is expected to see revenue growth significantly reaccelerate beginning in the back half of the year, with EPS following in 2026. Estimates point to growth bottoming at 0.3% in Q2, before accelerating to 14.3% YoY to end 2025 and 25.7% in Q1 2026, representing a quick 25 point growth acceleration in four quarters.

Tesla’s revenue growth is currently forecast to bottom in Q2 before accelerating to nearly 26% in Q1 2026. Source: I/O Fund

EPS growth is expected to be choppy this year, with only Q2 expected to see growth against a much weaker comp. However, Q1 2026 is expected to see the sharpest YoY growth in EPS in more than three years at 54.2% -- again against a soft comp.

We have continuously reminded our readers that margins have been the #1 metric to focus on for nearly two years as margin compression led to 2024’s large YoY declines in EPS. Tesla has had to continue cutting ASPs to promote vehicle affordability, not relieving any of this margin pressure.

In Tesla’s case, however, sentiment often takes precedence above all, in part due to a massive advantage it has in physical AI and (speculative) trillion-dollar opportunities in robotaxis and humanoid robotics with Optimus.

Tesla is witnessing exponential growth in FSD-driven miles, nearly tripling from ~1 billion in March 2024 to almost 3 billion by December 2024. It is also still planning to launch a driverless robotaxi service this year and begin scaling Optimus production. While neither of the two are expected to be meaningful contributors to growth for this year, the materialization of either AVs or humanoid robotics could open tremendous growth potential for the company in the future.

Timing has always been tricky for Tesla, especially when it comes to autonomous vehicles. However, timing investments is one of the I/O Fund’s strengths, actively managing positions with real-time trade alerts for every buy and sell we make in our leading portfolio with 210% returns since inception and 27.6% annualized returns. We also offer frequent deep dive research, weekly webinars and an automated portfolio hedge. Learn more here.

I/O Fund Equity Analyst Damien Robbins contributed to this report.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

Recommended Reading:

More To Explore

Newsletter

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de