Supply Chain Issues Could Recover In Q3 2022

April 06, 2022

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Apr 1, 2022,01:24pm EDT

Aggregate Inventories Have Recovered but Auto Inventories Remain Under Pressure:

Supply chain issues have been a well-publicized event that has been hard to predict. While there have been improvements in supply chain management since the harsh production halts enforced during the pandemic, semiconductors continue to be a bottleneck in numerous industries, especially automotive.

Furthermore, the semiconductor bottleneck has had a ripple effect and has impacted industries outside of automotive production, such as ad-tech. In fact, ad-tech has been one of the most beaten-down industries due to the supply chain crisis. This is because automotive is a significant category of ad spend, and without inventory to sell, advertising budgets have been slashed. Nonetheless, we expect that this is only a temporary concern and that ad-tech will rebound in 2022 as supply chain issues begin to normalize. We especially look for discounts in tech that stem from a transient yet external issue outside of any individual company’s control.

The I/O Fund team went beyond relying on management commentary and studied the data to better understand the supply chain bottleneck. We found that aggregate inventory levels have generally recovered, but automotive inventories remain under pressure. I/O Fund Financial Analyst Bradley Cipriano notes that an analysis of automotive inventory composition suggests that the supply-chain issues have likely bottomed and will improve going forward.

The I/O Fund chose to be aggressive during the Q4 earnings season between January and March by building ad-tech positions for this reason. We expect that improving inventory trends will lead to a sharp rebound in automotive advertising in the back half of the year, driving topline growth for the ad-tech sector. We discuss why we believe that the supply chain crisis will ease around H2 2022 below.

Supply Chain Management: Aggregate Inventories Have Recovered but Auto Inventories Remain Under Pressure

The pandemic began in early 2020 and resulted in a whipsaw effect that impacted both supply and demand. With governments enforcing strict shelter in place orders, production of goods declined in 2020 but consumers still demanded goods. Government stimulus further bolstered demand and there was less of a contraction in total demand than there otherwise would have been. This dynamic led to the supply shortage that many sectors have been working through.

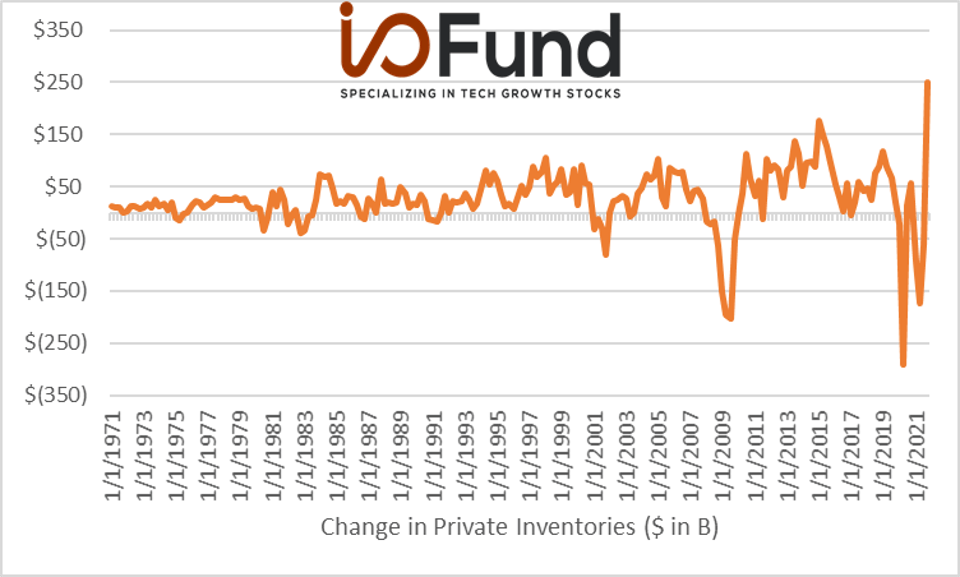

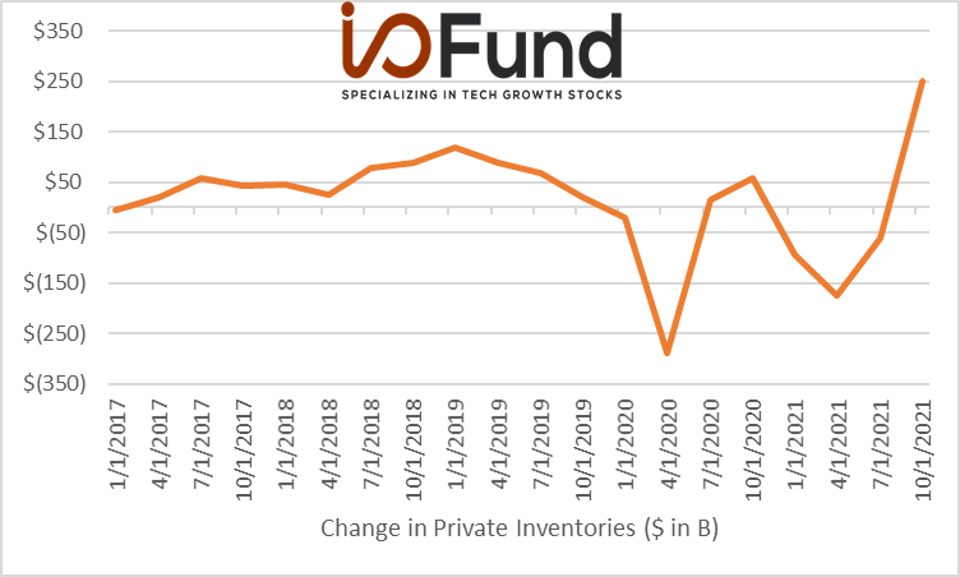

Since inventories are essentially the difference between production and sales over a period of time, the dynamic of reduced production but increased demand led to a sharp reduction in inventories in 2020 and 2021. As shown below in Chart 1, changes in private inventories, which is a measure of the value of the physical volume of inventories that businesses maintain to support their production, materially declined in Q2 2020. In fact, the $300 billion drawdown in inventories in Q2 2020 was the steepest drawdown in history.

However, while Q2 2020 represented the steepest decline on record, Q4 2021 represented the largest increase on record, as inventory levels bounced back by over $200 billion. This sharp rebound helps highlight that production is catching back up with demand

Chart 1. 50-year Trend of Changes in Private Inventories

Source: U.S. Bureau of Economic Analysis - I/O FUND

Source: U.S. Bureau of Economic Analysis - I/O FUND

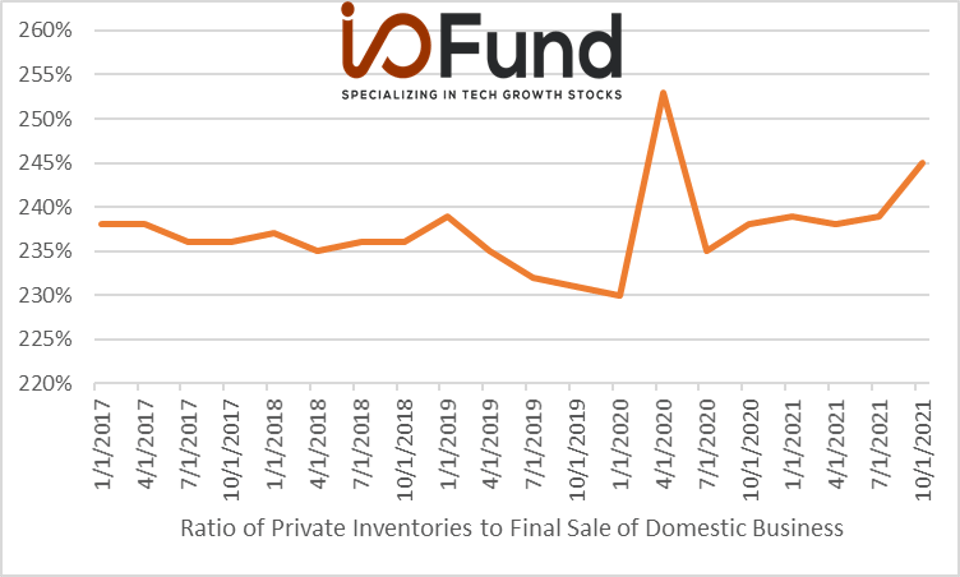

In Chart 3 (below), inventories are also rising relative to sales, suggesting that there has been a build in inventory levels. Furthermore, the metric is above the five-year average, implying that inventories are not tight on a systemic scale.

Chart 3. Five-Year Trend of Private inventories to Final Sales

Source: U.S. Bureau of Economic Analysis - I/O FUND

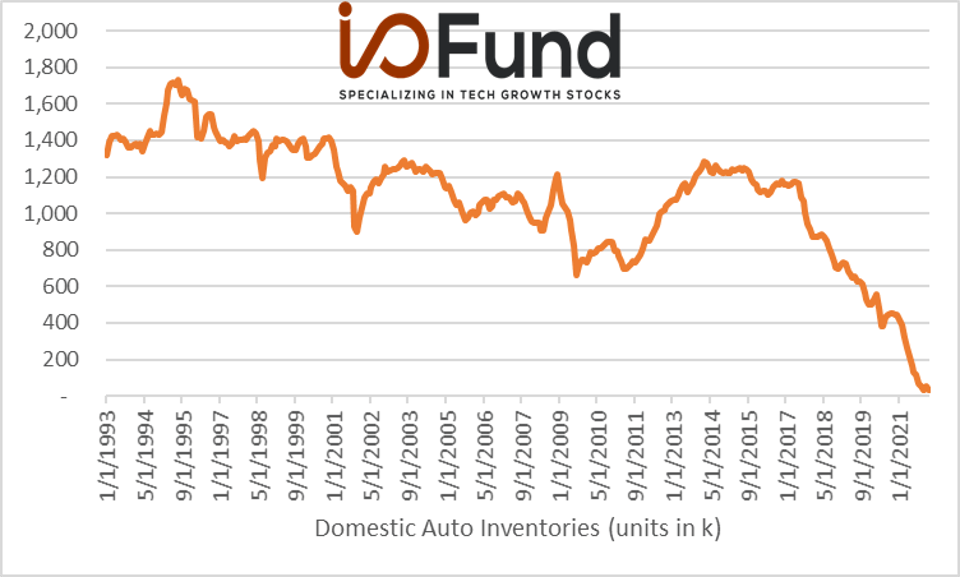

While the above charts highlight that there has been a strong recovery in inventory levels in the economy, it fails to take into account the types of inventories. Specifically, despite the recovery in aggregate inventories, automotive inventories have fallen to all-time lows.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

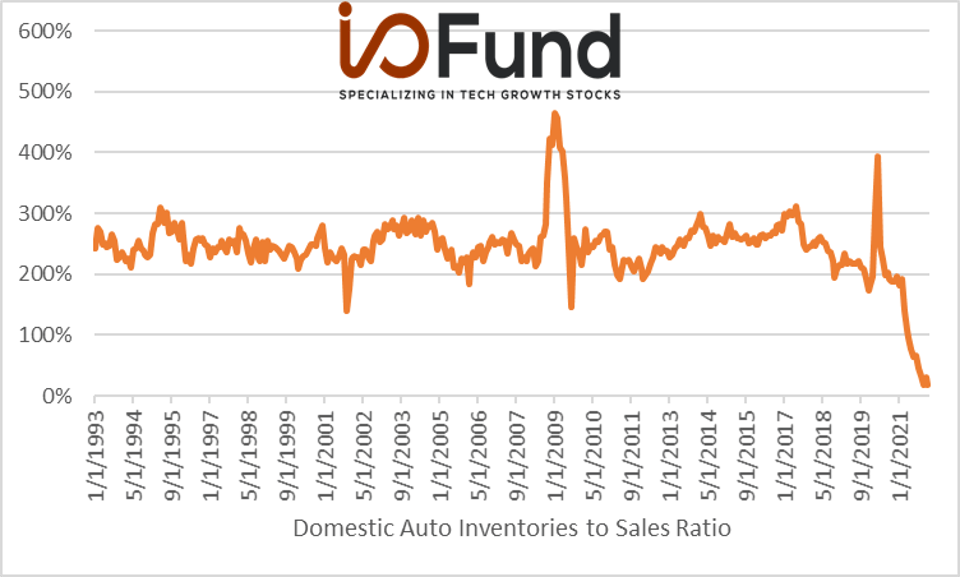

The below chart from the U.S. Bureau of Economic Analysis shows that auto inventories have declined to a record low and are hovering just above 0. Without much inventory to sell, there is little incentive to spend on advertising, which has negatively impacted ad-tech.

Chart 4. Domestic Auto Inventories

U.S. Bureau of Economic Analysis - I/O FUND

Chart 5. Domestic Auto Inventories to Sales Ratio

Source: U.S. Bureau of Economic Analysis - I/O FUND

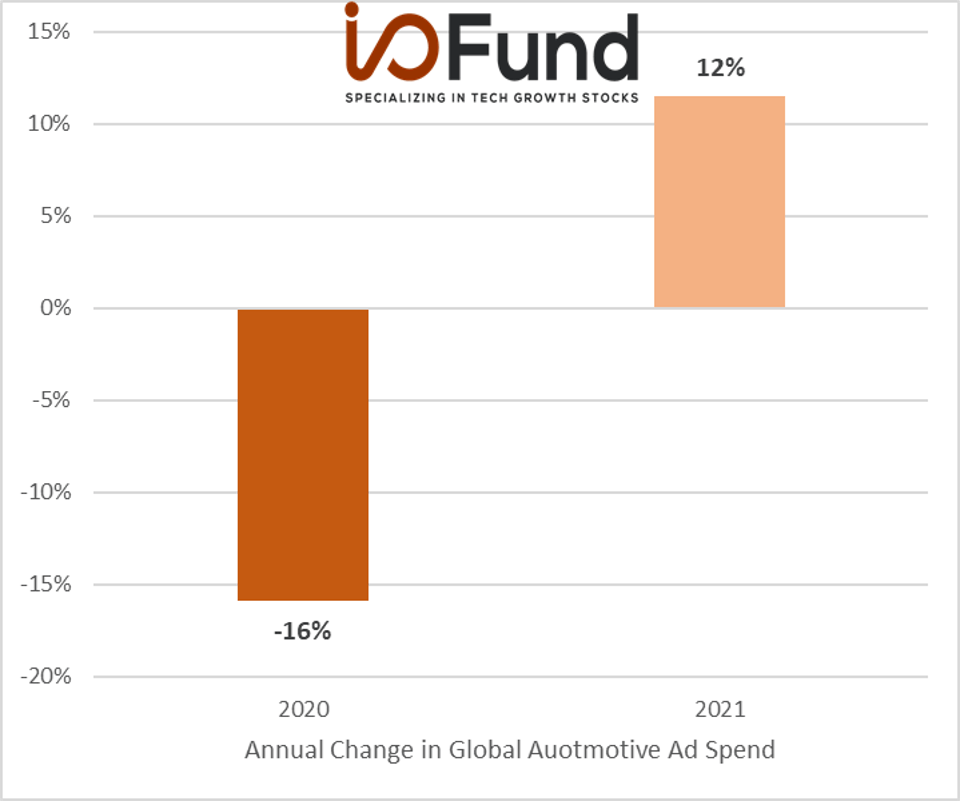

Data from Dentsu’s Global Ad Spend Report highlights how automotive spending is still below 2019 levels. As shown below in Chart 6, global automotive ad spend declined 16% YoY in 2020, and rebounded just 12% in 2021, meaning that global automotive ad spending was still ~6% below its pre-pandemic levels. Since automotive advertisers spend an outsized amount of their budgets on TV ads, ad-tech companies exposed to connected TVs have been especially impacted by the soft recovery in auto ad budgets shown below. As I’ll discuss in more detail below, we believe that automotive ad spending has bottomed and will be a tailwind for ad-tech going forward.

Chart 6. Automotive Global Paid Search Ad Spend

Source: Dentsu Global Ad Spend Report - I/O FUND

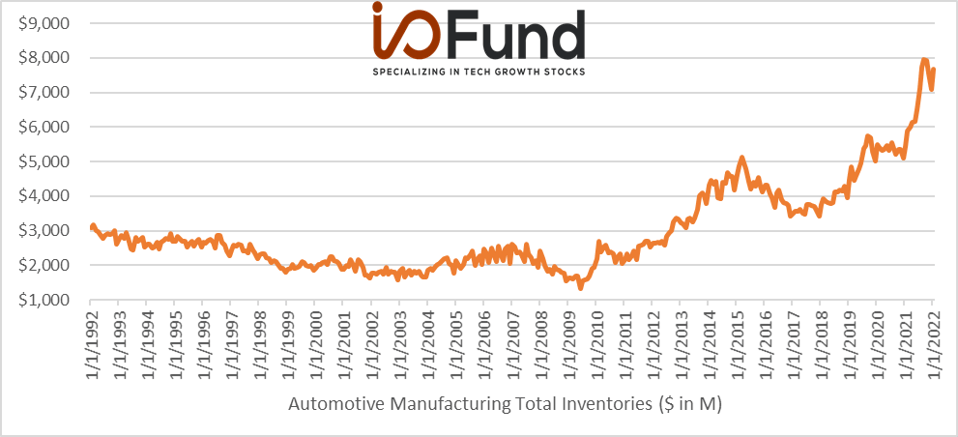

Curiously, despite the fact that auto inventories are at record lows, automobile manufacturers’ inventories are also at an all-time high. As shown below in Chart 7, total inventory levels in the automotive manufacturing industry have surged throughout 2021 and into 2022.

Chart 7. Automotive Total Inventories

Source: U.S. Census Bureau - I/O FUND

These disparate trends are driven by the well-publicized semiconductor bottleneck. As Chart 7 highlights above, automotive manufacturers have large amounts of nearly completed inventory that is sitting idle until semiconductor supply arrives.

Once the supply of semiconductors arrive, automotive manufacturers should be able to quickly ramp and turn work-in-process inventory into finished goods that can be sold. Moreover, this should also drive demand for advertising as auto manufacturers look to quickly convert their inventory into cash.

Fortunately, there are signs of improvement for supply chain issues, specifically from the automotive industry. For instance, Volkswagen Group’s management team explained on their Q4 call that they “expect semiconductor supply bottlenecks to continue in 2022, but gradually improve in the second half of the year” (03/15/22).

General Motors echoed similar sentiment during its Q4 earnings call. GM CEO Mary Barra stated that “by the time we get to third and fourth quarter [of 2022], we're going to be really starting to see the semiconductor constraints diminish” (02/01/22).

However, this sentiment was not shared by all automotive executives. CEO of Stellantis, maker of Dodge RAM, Fiat and other brands, stated on the company’s Q4 call (2/23/22) that the size of the automotive market will be driven by the supply of semiconductors, adding that “hopefully, things will get a little bit better. But we believe it's going to be very slow. It will take time. And 2022 is not going to be from that perspective, the year where we can say we are back to normal. We don't think that will happen”

Looking forward, automotive manufacturers have outsized raw material and work-in-process inventory that will help them quickly ramp production once semiconductor supply improves. The timing of this ramp remains unknown, with some auto executives expecting H2 2022 to be a return to normal, and others forecasting a longer horizon.

Next Tuesday, we will discuss the signs of improvement at key automotive semiconductor suppliers and what this means for ad-tech including one strategic bet the I/O Fund made in ad-tech during the January-March selloff.

Bradley Cipriano, Financial Analyst, CFA, CPA at I/O Fund, contributed to this analysis.

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su