Roku Stock May Rebound From Easing Supply Chain Issues

April 13, 2022

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Apr 7, 2022,11:53pm EDT

Last week, we discussed signs of improvement at key automotive semiconductor suppliers and why this was affecting ad-tech stocks. Supply chain issues are causing a ripple effect due to automotive being a significant category of ad spend and due to low inventory, advertising budgets are being slashed. As stated in last week’s analysis, our expectation is that supply issues will ease by Q3 causing both automotive and ad-tech to rebound.

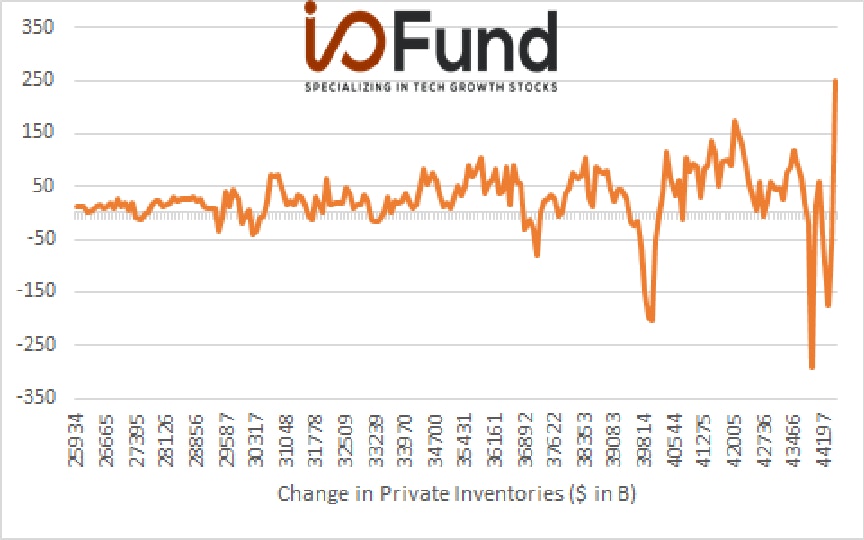

Specifically, it’s the extremes of seeing a $300 billion drawdown in inventories in Q2 2020 followed by the largest increase on record of inventory levels in Q4 2021. We believe this sharp rebound helps highlight that production is catching back up with demand.

Supply Chain Impact to Roku Stock and Ad-tech Going Forward

Below, we discuss why Roku stock could be set to rebound when supply chain issues begin to ease due to extreme oversold conditions based on transient headwinds. We also discuss more in depth the supply chain rebound we are forecasting for some time around the second half of 2022.

Source: U.S. Bureau of Economic Analysis (I/O Fund)

While supply chain constraints are expected to remain tight in 2022, there are numerous signs that the bottom is in. For instance, aggregate inventories rebounded strongly in Q4 2021 and have made up most of the decline from production halts during Q2 2020. Moreover, inventories relative to aggregate sales are at multi-year highs. The rebound in aggregate inventories suggests that supply chain constraints are normalizing for the broader economy.

Connected-TV (CTV) is particularly exposed to automotive advertising budgets, and a rebound in automotive inventories will be a tailwind for CTV ad-tech companies such as Roku. Automotive ad spend was just 15% of its pre-pandemic levels, largely due to the shortage of automotive inventories.

During the Q4 earnings call (02/17/22), Roku’s management explained how automotive was ‘soft’ during the quarter, yet they expect this to be a temporary trend. Roku CFO Steve Louden made a good point during the Q4 call, stating that automotive manufacturers are much stronger today than they were at the start of the pandemic, meaning that these brands have increased capacity to market their brands going forward.

For instance, if the top two automotive ad spenders (Volkswagen and Toyota) grow their topline by the midpoint of their respective guides and if their sales and marketing margins normalize to pre-pandemic levels, then aggregate ad spending could rise by about ~25% YoY in 2022, up from the ~6% YoY rise in 2021. Rising ad spend from these two leading manufacturers will likely spur marketing investments from peers.

Despite lower growth in Q1, Roku reiterated full year 2022 growth in the mid-30s. Going into the report, analysts were expecting 36% annual growth. The ad platform missed analyst expectations at $703 million compared to $732 million expected.

EBITDA was a miss with company guiding for $55 million compared to the consensus for $79 million in the upcoming Q1 quarter. The company plans to spend $1 billion on operations, which translates to investments in headcount, The Roku Channel (which is producing originals), and the Roku TV program (which means growing operating system market share).

The $1 billion in expenses is not overly concerning although it’s certainly an adjustment in expectations as the Street may have believed that Roku’s earnings were quickly scaling, but this was impacted by a slowdown in expenses during covid, and now those expenses need to ramp in the upcoming year to remain competitive.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

I/O Fund Financial Analyst Bradley Cipriano stated in a research note to our clients that Netflix's operating expenses ramped nearly $1 billion YoY when it passed $3 billion in revenues in 2011, which Roku is nearing. Viewed differently, the expected revenue growth in FY2022 of $830 million will be accompanied by a $1 billion rise in expenses, meaning that each $1 of expenses will drive just $0.76 of revenue, which is the lowest value in Roku's history. This suggests that growth is much more expensive than in prior years.

However, this is likely due to the slowdown in investments made during 2020 and 2021, and the three-year average for the above metric is 1.08x (including FY2022), meaning that each $1 of expenses resulted in $1.08 in revenues. This is above the prior three-year average of 1.04x (2019-2017), highlighting that over a longer time frame, Roku is in fact demonstrating leverage, albeit it is lumpy. FY2021 and FY2022 also includes the Player gross loss headwind that wasn't the case in prior years, and adjusting for this, the three-year average would be even higher. The takeaway is that the rise in expenses seems in-line with historical trends once we account for COVID.

The lower EPS this year is a headwind to the company's valuation, but it is expected to be profitable in FY2023. The company should be cashflow positive in FY2022 and with $2.1 billion in cash on balance, likely should not need to dilute shareholders despite the losses. There is also some leverage to improve earnings as there were $82m in one-time expenses during the most recent year.

If we widen our view, we will see that 2020 was the first year Roku was EBITDA positive and the company is expected to remain EBITDA positive this year. Most importantly, Roku has leverage with a gross profit of $1.4 billion and they are choosing to spend for top line growth.

Overall, Roku is a more complex product story because the strategy is to conquer from many angles. It’s an ad exchange, it’s a content channel, it’s an operating system and it’s a hardware player. It also owns the best first-party data available on CTV ads and I tend to stick with the data in terms of ad-tech. So, that’s primarily the reason we own Roku and continue to own Roku.

Regarding Roku’s recent price action, we look for dislocations within the markets and we believe transitory supply chain issues have caused the dislocation seen below in Roku’s valuation and its forward estimates. Most of tech has seen a dislocation between January-March, although Roku’s dislocation is particularly steep.

Regarding Roku’s recent price action, we look for dislocations within the markets and we believe transitory supply chain issues have caused the dislocation seen below in Roku’s valuation and its forward estimates. Most of tech has seen a dislocation between January-March, although Roku’s dislocation is particularly steep. (I/O Fund)

What is most striking about the divergence above is that the current selloff has provided a much cheaper stock than during the pandemic when many businesses were shut down entirely and ad budgets halted.

Despite strong growth estimates in the second half of the year, the forward PS on Roku reached 4x, which we consider to be extreme to the downside. We took this opportunity to begin building up Roku and other key ad-tech allocations. We also believe that Q4 2021 will likely represent a ‘bottom’ in automotive supply constraints, and that ad spend from automotive manufacturers will rebound going forward as supply chain constraints begin to ease.

More Data Supports Supply Chain Issues Easing in Q3

Please reference our first article “Supply Chain Issues Could Recover In Q3 2022” for additional data points.

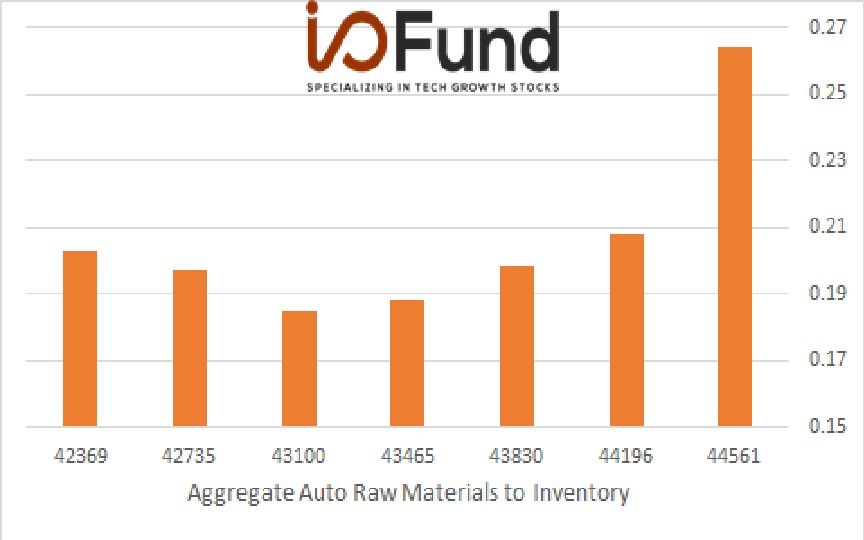

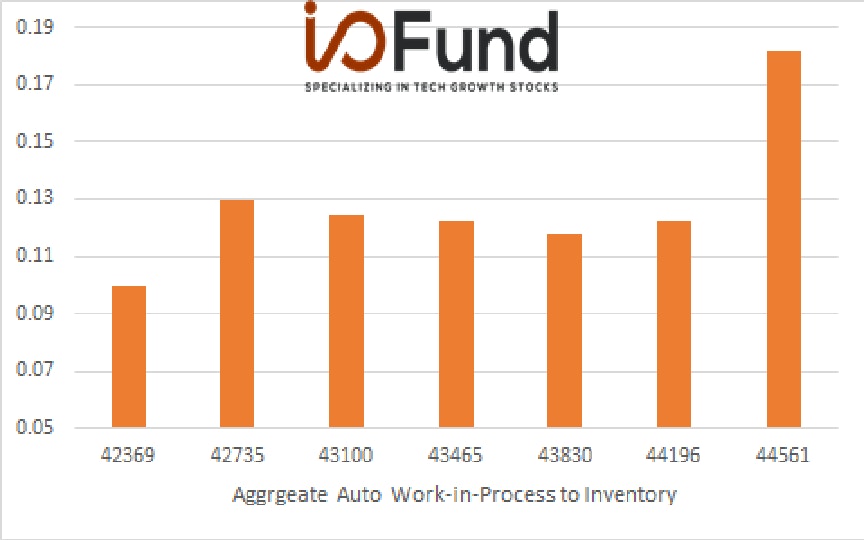

The surge in raw materials and work-in-process inventory at major auto manufacturers adds further support that auto companies are positioned to quickly ramp production. As shown below in Chart 8 and 9, both aggregate automotive raw materials and work-in-process inventories have increased to a five-year high relative to total inventory.

Chart 8. Aggregate Automotive Raw Materials to Inventory Ratio

Source: Auto manufacturer filings (I/O Fund)

Chart 9. Aggregate Automotive Work-in-Process to Inventory Ratio

Source: Auto manufacturer filings (I/O Fund)

What this trend shows is that automotive manufacturers have high levels of working capital stored in near-complete inventory. Once semiconductor supplies arrive, we should expect automotive manufacturers to quickly convert this inventory into finished goods. A build in finished goods inventory should also lead to a strong rebound in advertising budgets from the automotive industry.

Sign up for I/O Fund's free newsletter with gains of up to 403% - Click here

Since the semiconductor shortage is a systemic issue, we should expect auto manufacturers to ramp spending at the same time. Furthermore, auto manufacturers will likely look to quickly offload their inventory to avoid oversupply and capture market share. This trend should help drive demand for ad spend going forward.

Notably, the timing of this ramp remains unknown, with some auto executives expecting H2 2022 to be a return to normal, and others forecasting a longer horizon. We discussed this trend in more detail in last week’s analysis.

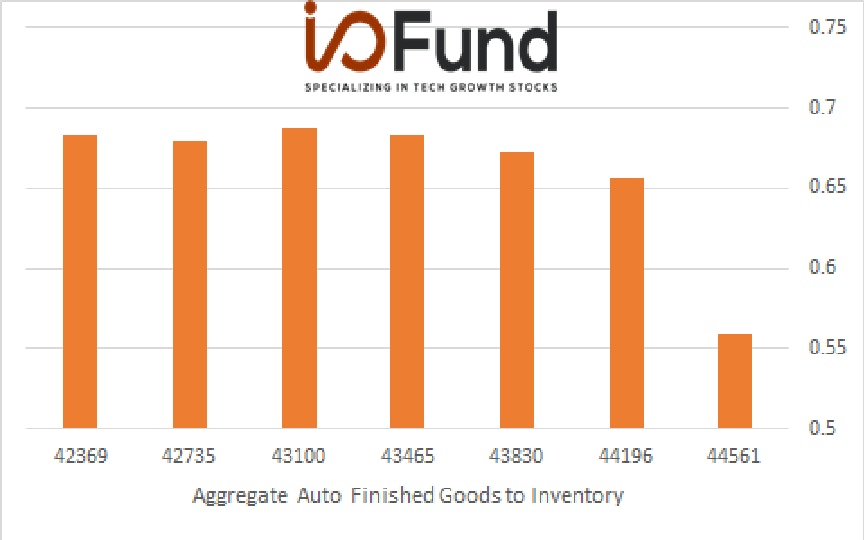

Chart 10. Aggregate Automotive Finished Goods to Inventory Ratio

Source: Auto manufacturer filings (I/O Fund)

Automotive semiconductor OEMs report rising inventories and increasing capex

IHS Markit estimated that North American vehicle production in 2021 increased just 1% YoY to 13.1 million. In 2022, vehicle production is expected to rebound and increase 13% YoY to 14.7 million units in 2022 but remain below the 15 million vehicles produced in 2019.

Nonetheless, the rebound in production should support a rebound in ad spend going forward.

While there remains considerable uncertainty due to the cadence of the ramp in vehicle production, there are signs of improvement from key automotive semiconductor suppliers.

For instance, Infineon Technologies, a key supplier of inverters for automotive applications, stated during their latest earnings call (02/03/22) that “the December quarter was the first one in a while where we did not experience [supply] disruptions”. Management added that tightness remains in securing foundry supply, but that wafer supplies are expected to materially improve in the second half of 2022.

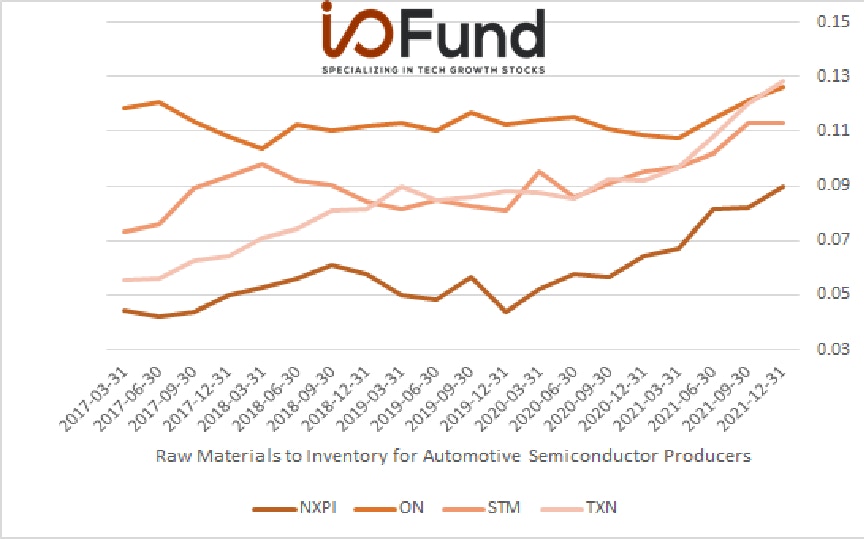

The below charts highlight how raw material inventories have been rising for key automotive semiconductor suppliers, a trend that supports a rebound in supply going forward.

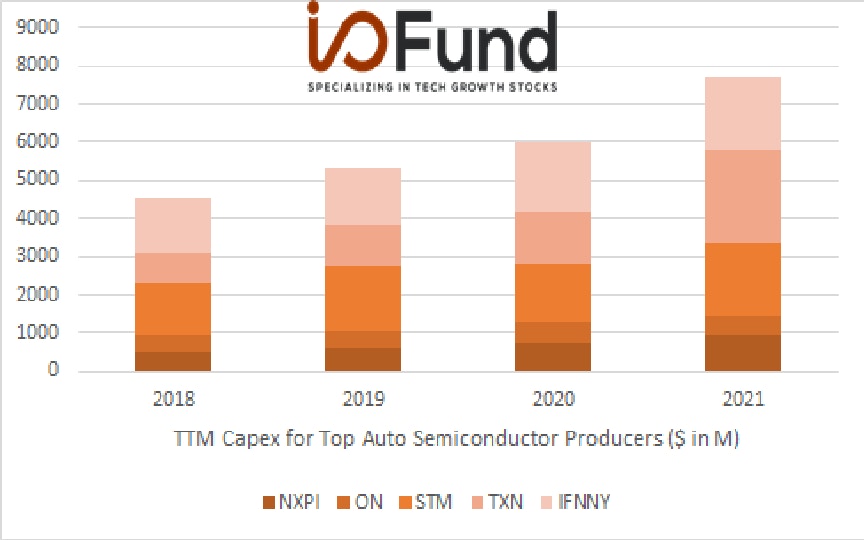

A rise in raw materials signals that companies are expected to ramp production in the near term. Furthermore, these automotive semiconductor suppliers have also ramped capacity, as aggregate capex for the group increased 29% YoY to nearly $8 billion. A rise in capex signals that management is increasing supply capacity in anticipation of future demand growth. The concurrent rise in raw materials and capex signals that supply will improve going forward, suggesting that we are nearing a trough in semiconductor imbalances in the auto industry.

Chart 11. Recent Trends in Raw Material Inventories for Automotive Semiconductor Producers

Recent Trends in Raw Material Inventories for Automotive Semiconductor Producers (I/O Fund)

Chart 12. Recent Trends in TTM Capex from Automotive Semiconductor Producers

Source: Company filings (I/O Fund)

We believe that 2021 will likely represent a ‘bottom’ in automotive supply constraints, and that ad spend from automotive manufacturers will rebound going forward as supply chain constraints begin to ease. However, semiconductor supply is expected to remain tight throughout 2022, which is the main bottleneck impacting the ramp in auto production. With record levels of idle work-in-process inventory, we believe that auto manufacturers will quickly ramp ad spend to turnover their inventory once semiconductor supply reaches them. With semiconductor OEMs reporting a ramp in both capacity and raw materials, we believe that automotive ad spend will be a tailwind for ad-tech going forward, with a significant ramp in H2 2022 and into 2023.

Roku has been a strong and steady performer in terms of revenue growth and improvement in the bottom line since going public. In six years, Roku has been able to grow its revenue 850% from $398 million in 2016 to an estimated $3.72 billion for FY2022. The Trade Desk will have grown 687% on a lower revenue base while trading 3X higher.

Even with increased spending of $1 billion, it’s important to consider that the company has leverage in its business model. Critics will point out that TTD has a much better operating margin – but time will tell if Roku has chosen the correct strategy to own the real estate. To me, this is arguably the better business model considering the average consumer owns their connected TV for seven years. If so, the current valuation for Roku is too low compared to its forward growth, which made it a buy in Q1.

Financial Analyst Bradley Cipriano, CFA, CPA at I/O Fund, contributed to this analysis.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

More To Explore

Newsletter

Big Tech’s AI Revenue Is Surging, but Suppliers Will Still Be the Bigger Winners

Big Tech’s AI Capex has stomped estimates for multiple years and analysts are now calling for capex to surge to $1 trillion in 2027. However, hyperscalers have long battled investor concerns around wh

AI Capex to Hit $1 Trillion – And Estimates Are Still Too Low

Big Tech capex is the driving force behind the AI infrastructure trade, yet Wall Street has repeatedly underestimated the sheer scale of the buildout. Currently, in 2026, the guidance for $732.5 billi

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per