Top 5 Stocks Of 2022: Year In Review

January 11, 2023

Beth Kindig

Lead Tech Analyst

This article was originally published on Forbes on Jan 6, 2023,09:04am EST

In this analysis, rather than prognosticate on the top stocks of 2023, we think it’s more productive to go back and review the stocks that performed well under new macro conditions in 2022. This exercise helps to inform tech portfolios for the upcoming year as investors can reasonably assume 2023 will look more similar to 2022 than the preceding years.

2022 was a very volatile year for the stock market with rising rates, inflation, and geopolitical tensions leading to sudden sell-offs. All three main U.S. indices ended the year with negative returns, with Dow Jones Industrial Average down 6.86%, S&P 500 index down 18.11%, and Nasdaq down 32.54%. Despite the indexes being in the red, some stocks greatly outperformed the broad market.

We think it’s important to pause and draw some parallels around the stocks that performed well in 2022 to form an opinion on what might perform well in 2023. This is assuming macro will be more similar to 2022 than the preceding years, which is a reasonable assumption to make at this time.

Below, we review the top five stocks of 2022. These stocks were chosen based on their price action and strong fundamentals. Choosing a top 5 means many great stocks were left off this list, yet this sample helps to form conclusions around how 2022 was a different trading environment from years past.

Source: Ycharts

Sign up for I/O Fund's free newsletter with gains of up to 221% - Click here

Super Micro Computer (SMCI)

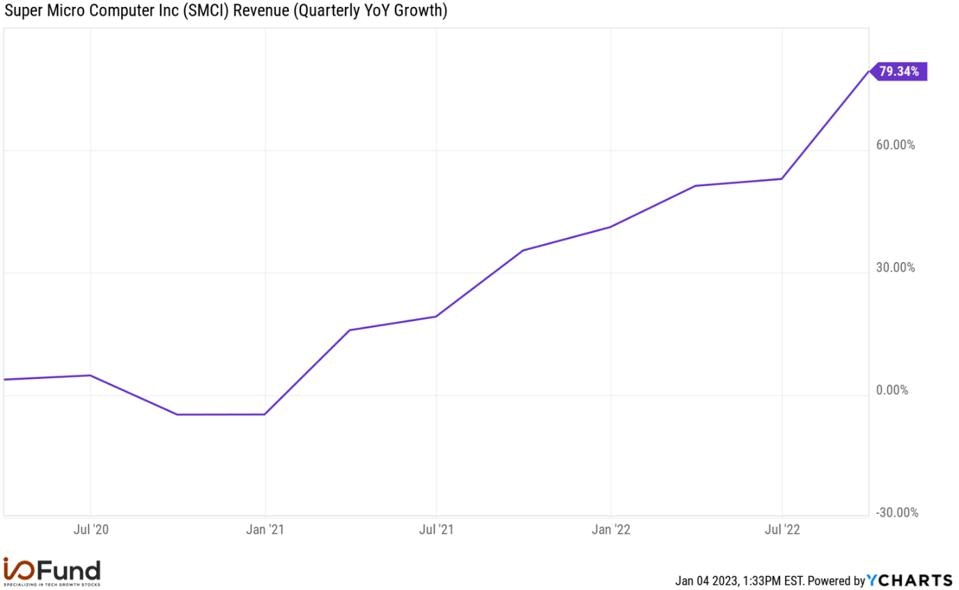

Super Micro Computer stock had 2022 returns of 86.8% and is the best-performing stock in our tech universe. Below is a chart that shows the quarterly year-over-year revenue acceleration Super Micro posted in 2022, which helped support its 2022 winning streak.

Pictured above is SMCI’s Qly revenue YoY growth. - Ycharts

The company provides server and storage solutions to data centers, cloud computing, 5G, AI, and edge computing markets. The company was recently added to the S&P MidCap 400 Index and enjoys tailwinds from leading semiconductor companies such as AMD, Nvidia, and Intel.

In the recent earnings call, the founder and CEO of the company, Charles Liang said, “For Intel, we are engaged with many large opportunities with Intel’s upcoming Gen 4 scalable Xeon CPU codenamed Sapphire Rapids. We now have hundreds of early seeding engagements including several dozen early shipments. Similar programs have been executing with AMD, and we have seen very strong demand for our upcoming Genoa CPU based platforms.”

“With respect to NVIDIA, not only do we have the most complete portfolio of systems supporting H100 GPUs, but we have also developed many brand new architectures for the leading Metaverse and Omniverse partners.”

The company’s revenue in the recent quarter, Q1 FY23, grew by 79% YoY to $1.85 billion. The gross margin improved to 18.8% in Q1 FY23 up from 13.4% in the same period last year. The company’s profits have grown steadily with net income of $184 million compared to $25 million in the same period last year. The stock is currently trading at a P/E ratio of 10.3 and a fwd P/E ratio of 8.1.

Source: Ycharts

Microsoft (MSFT)

Microsoft was one of the best performing tech mega cap stocks last year ending the year down (28%), compared to Meta and Tesla, which ended the year down (64%) and (65%), respectively. Notably, Microsoft narrowly beat the Nasdaq in 2022.

The company is positioned for outsized growth due to its exposure to secular tailwinds such as Artificial Intelligence (AI), Machine Learning (ML), and the build out of the 5G edge network. Microsoft could take a substantial share of these markets at the infrastructure level due to its relationships with the Fortune 500 and Global Fortune 2000.

In addition to top-down enterprise penetration across the Fortune 500, Microsoft is also focused on developers to help complete Microsoft’s customer cloud strategy. Microsoft addressed its previously poor reputation in open-source communities by acquiring GitHub for $7.5 billion in 2018. Developers help determine the cloud IaaS service an enterprise or SMB customer will choose, so in-roads into this community could help Microsoft hedge the developer favorite, Amazon Web Services.

The company’s Q1 FY23 revenue grew by 11% YoY and down 3.4% QoQ to $50.1 billion.

Operating income increased by 6% YoY to $21.5 billion. Net income was $17.6 billion compared to an adjusted net income of $17.2 billion in the same period last year (adjusted net income in the previous year as the company received income tax benefit last year).

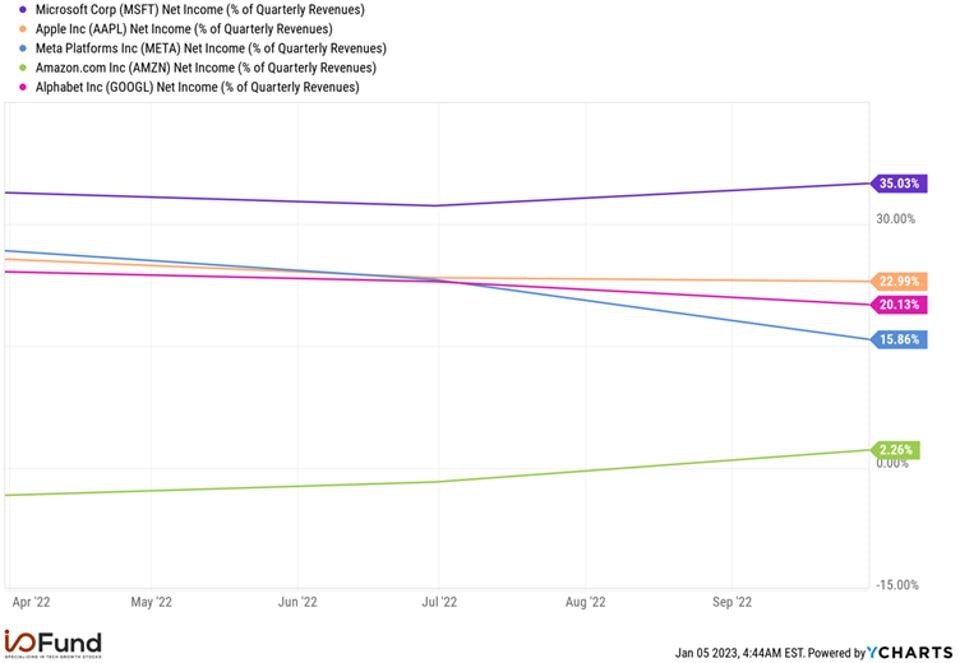

The net profit margin was 35% in the recent quarter.

Microsoft has proven it has many levers it can pull during a tougher macro compared to its mega cap tech peers – primarily seen in the consistency of its profit margin.

Source: Ycharts

Due to Microsoft being a leading tech stock that the I/O Fund plans to buy on any weakness, we have included a YouTube clip from Portfolio Manger Knox Ridley of the 2023 price action we are expecting for Microsoft including sample entries.

Subscribe to I/O Fund's Essentials:

The I/O Fund has launched a new $99/year Premium Newsletter called "Essentials" -- this newsletter delivers premium samples for our readers who want more actionable analysis for their tech portfolios. This month, we released a stock pick that we believe will be a leader in 2023 plus a video with the buy plan.

ASML Holding (ASML)

ASML Holding is benefitting from strong semiconductor equipment demand from the leading foundry companies. As new fabs are built, these companies will need equipment in the coming years. The company’s fiscal year 2022 revenue analysts estimate rose 12% in the last 2 months. The company raised the 2025 revenue guidance to be between €30 billion and €40 billion, up from the previous guidance of €24 billion to €30 billion. The company in its press release acknowledged, “While the current macro environment creates near-term uncertainties, we expect longer-term demand and capacity showing healthy growth.”

The company’s Q3 revenue was €5.8 billion compared to €5.2 billion in the same period last year. The management expects Q4 revenue to be between €6.1 billion to €6.6 billion. The gross margin was 51.8% compared to 51.7% in the same period last year. Net income was €1.7 billion (net profit margin of 29.4%) compared to a net income of €1.7 billion (net profit margin of 33.2%) in the same period last year.

The company has a strong backlog of over €38 billion. The company’s CEO Peter Wennick said in the earnings call, “And as a matter of fact, our 2023 shipment demand is still significantly above our build and shipment capacity for next year. And this is supported by the record bookings this quarter, of €8.9 billion and our largest backlog ever of over €38 billion. Almost 85% of this backlog is for EUV and immersion, which is used for advanced nodes and related wafer capacity expansions.”

Palo Alto Networks (PANW)

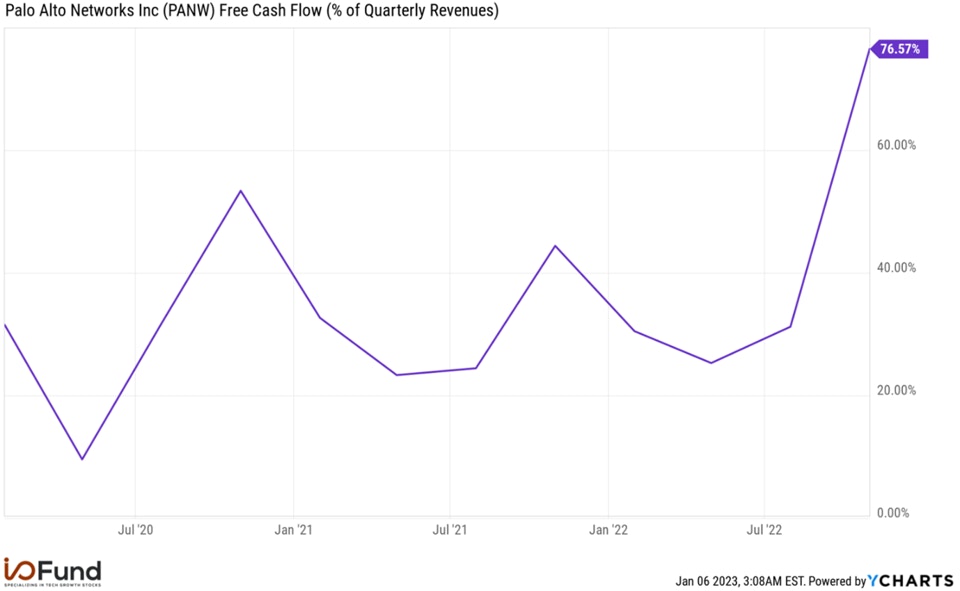

Leading cybersecurity company Palo Alto Networks has a strong free cash flow margin, which is rare in the cloud and cybersecurity category. The company has been GAAP profitable for the last two quarters. The company’s revenue in the Q1 FY23 grew by 25% YoY to $1.6 billion, which was above the management guidance of $1.535 billion to $1.555 billion.

The company’s margins are improving. The company reported a GAAP net income of $20 million compared to a GAAP net loss of ($103.6) million in the same period last year. The adjusted net income was $266.4 million compared to $170.3 million in the same period last year. Consistent GAAP profitability is key in this macro environment.

The company reported free cash flow of $1.2 billion (76.6% of revenue) compared to $554 million in the same period last year (44.4% of revenue). Dipak Golechha, CFO of the company, said in the earnings call, “This cash flow performance was largely driven by strong collections in the quarter, that we expected based on the strength of our business in Q4.” The management has guided an adjusted free cash flow margin in the range of 34.5% to 35.5% for the FY23.

Dipak Golechha said, "We exceeded our top-line guidance while generating $1.2 billion in free cash flow and expanding our operating margins," He further added, "We will continue to balance growth with profitability and cash generation to further strengthen our position in the market."

Source: Ycharts

First Solar (FSLR)

Solar stocks were the leading sector in tech last year. First Solar ended the year on fire with a return of 72% compared to the (33%) return of the Nasdaq. The sector got a boost from the Inflation Reduction Act of 2022, which we covered last year in our free newsletter when we said:

“The solar industry will benefit since Inflation Reduction Act includes the extension of Production Tax Credits (PTCs) and Investment Tax Credits (ITCs) for the construction of wind and solar projects beginning before January 1, 2025. It means a three-year extension for PTCs and a one-year extension for ITCs.

It also extends the 30% federal tax credits for installing solar panels on rooftops by another 10 years, from 2022 to 2032. Solar installations are eligible for 26% tax credit for installations in 2020 and 2021. It now extends till 2032 for 30% tax credits, and in 2033 the tax credit will be reduced to 26% and 22% in 2034. There will be no tax credit after this period unless Congress renews it. Home battery systems that store energy generated by solar systems for later use will also be eligible for a 30% tax credit.”

First Solar is a leading provider of photovoltaic (PV) energy solutions. It is one of the major beneficiaries of the IRA in the form of solar manufacturing tax credits. The company was also recently added to the S&P 500 index.

The company announced last year its plan to invest $1.2 billion to expand its solar module manufacturing in the U.S. It includes a $1 billion investment for a new manufacturing facility in the Southeast U.S. and $185 million for the upgradation of the existing Ohio facility.

Mark Widmar, CEO of the company, said in the Q3 earnings call, “In our view, by passing and enacting the Inflation Reduction Act of 2022, Congress and the Biden-Harris administration has entrusted our industry with responsibility of enabling and securing America's clean energy future, and we recognize the need to meet the moment in a manner that is both timely and sustainable.”

The company’s Q3 2022 revenue was up 7.8% YoY to $628.9 million. It reported a net loss of ($49.2 million) compared to a net income of $55.8 million in Q2 2022 and $45.2 million in the same period last year. The company benefitted from the gain from the sale of the Japan project development platform in the Q2 2022 and also experienced higher logistics charges in the recent quarter.

Mark Widmar, CEO of First Solar said, “Our focus continues to be on setting the stage for long-term growth, and from this point of view, 2022 has so far proven to be foundational,” He further added, “This year we have developed the potential for our CdTe semiconductor technology by progressing our next-generation Series 7 and bifacial platforms, set in motion plans to scale our global manufacturing capacity to over 20 GWDC by 2025, and secured record year-to-date bookings of 43.7 GWDC with deliveries extending into 2027.”

Conclusion:

The I/O fund is an actively managed tech portfolio that is audited and we carefully choose our positions to reflect the current macro environment for tech. Therefore, our analysis is very actionable and I strongly feel that looking back at 2022 is providing clues for tech investors as we move forward into 2023.

This week, I recently stated on our research site’s private forum:

“My concern for retailers is that the underlying tone is that macro will clear up quickly and tech darlings will return. It's more likely macro will be throwing curveballs for some time. To put it another way, it's obvious that 2022 was terribly bad for investors, but what if the real issue is that the previous years were so terribly good/easy. Will those good/easy conditions return?

Part of the good/easy conditions was fueled by the venture capital cycle. When every tech company going public has high growth rates yet is losing on the bottom line, and it's clear the market is still awarding the poor bottom lines with sky high valuations, what you get is a runaway train of a bull market.”

The stocks above have proven they do not need good or easy conditions to perform well. It can be hard to have a repeat year as often investors will take gains, and there’s certainly gains to take in the names listed above. Therefore, we are looking for a pattern rather than attempting to exactly repeat 2022. This pattern is expanding margins, strong free cash flows, and any hint or sign of accelerating revenue.

Royston Roche, Equity Analyst at the I/O Fund, contributed to this article.

Please note: The I/O Fund conducts research and draws conclusions for the Fund’s positions. We then share that information with our readers. This is not a guarantee of a stock’s performance. Please consult your personal financial advisor before buying any stock in the companies mentioned in this analysis.

More To Explore

Newsletter

Token Growth is Surging - Here Are the Beneficiaries

The reality of AI demand growth has shattered early estimates for token processing, yet expectations continue moving up and to the right. In the second installment of our token processing series, we e

AI Token Demand is Shattering Forecasts

Total annual token processing is no longer measured in billions or trillions of tokens, but in the quadrillions and beyond. As annual token processing is now tracked in units with 15 trailing zeros, i

Nvidia and Google Are Crowding TSMC’s N3 Node - Can Intel Fill the Gap?

Nvidia is moving its next-generation Rubin GPUs from 4nm to 3nm, yet Google’s latest TPUs are already on N3 and are expected to remain there. Meanwhile, a growing number of AI CPUs from Nvidia, Amazon

Intel vs TSMC: How CoWoS Packaging Constraints Could Create an Opportunity for Intel Foundry

Taiwan Semiconductor (TSMC) is the single, most important company to the AI industry. However, to compete with the incumbent, Intel does not need to beat TSMC at leading-edge manufacturing. It only ne

Big Tech’s Free Cash Flow is Turning Negative – Who's Next?

Big Tech’s AI revenue is accelerating, but free cash flow is moving sharply in the opposite direction. Across Google, Microsoft, Meta and Amazon, capex is rising much faster than operating cash flow a

Big Tech Earnings Preview: Is AI Monetization Finally Catching Up to Capex?

The most pronounced difference between 2026’s tech rally compared to rallies in the past is which companies have been left out of it. The names most associated with the AI trade have hardly participat

Nvidia, CXL, and the Battle to Improve AI Inference Economics

This is Part 2 of our two-part series on AI inference economics. In Part 1 — Why Nvidia's Next AI Battle Is About Tokens per Watt, we laid out why tokens per watt has become the defining metric for in

Why Nvidia’s Next AI Battle Is About Tokens per Watt

As hyperscalers move from building AI infrastructure to monetizing it, tokens per watt helps to reflect if revenue is scaling and if profitability is improving. Offload engines can increase tokens per

Micron Is Up 900%. Here’s Why the AI Memory Trade May Still Have Room to Run

Over the past 10 months, memory chip stocks have gone from being solid beneficiaries of the AI boom to capturing a massively outsized piece of the return pie. The inflection in Micron’s performance de

Why the S&P 500 Shrugged Off the Iran War — and What Could Finally Break the Rally

On February 28th, the U.S. went to war with Iran, and the market was handed the kind of shock it hasn't contended with for years. The conflict set off a chain reaction across the region: an ongoing su